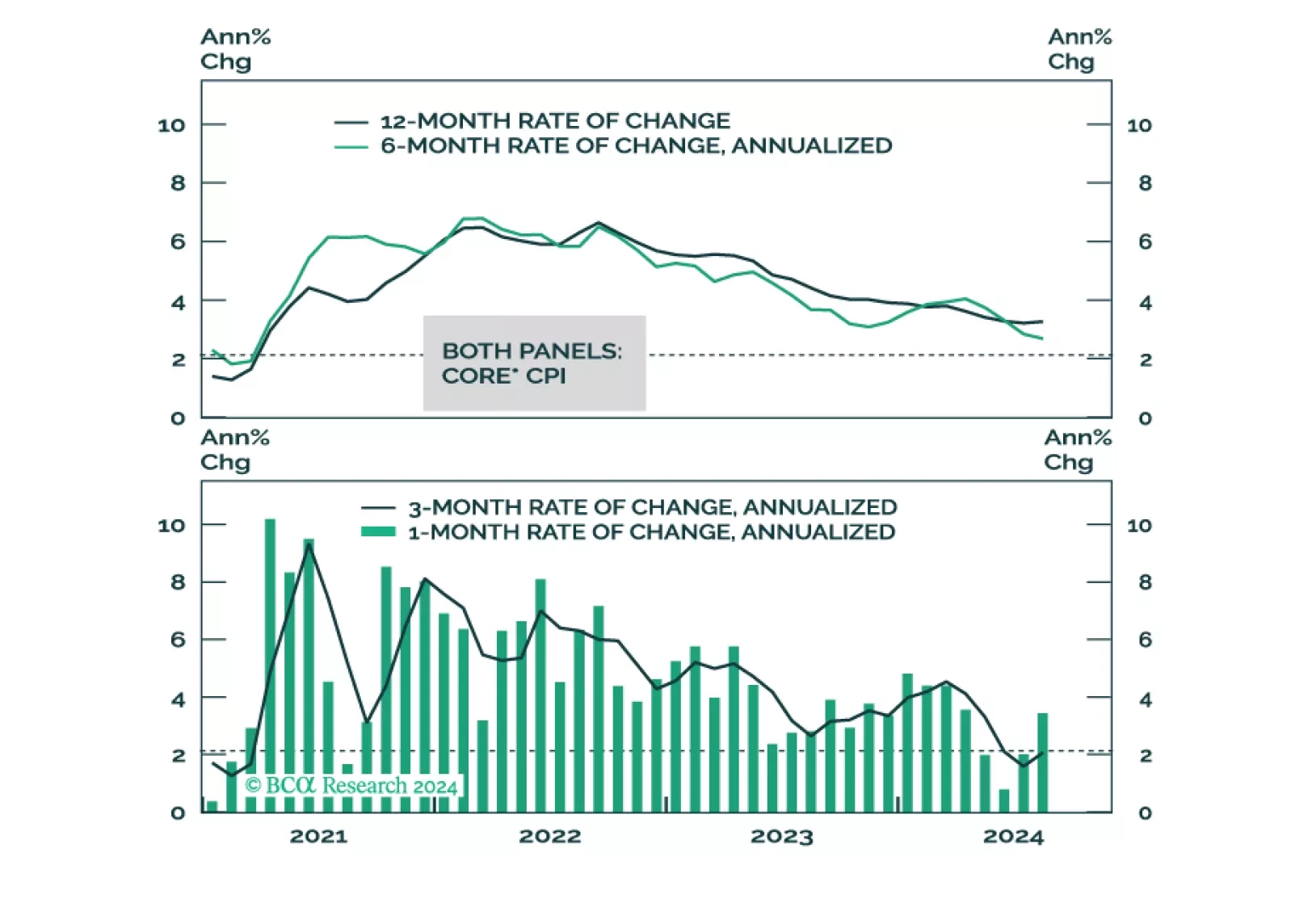

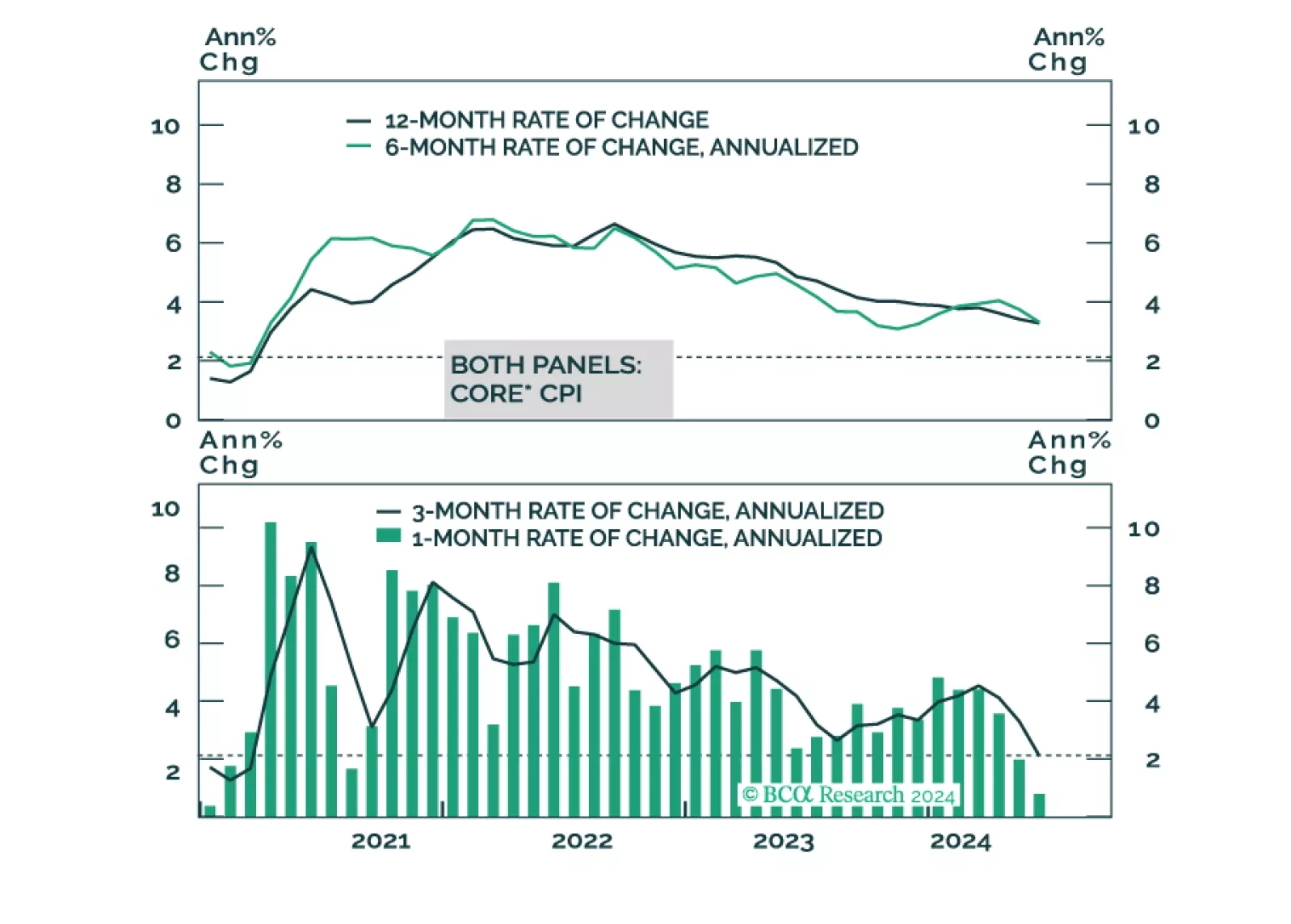

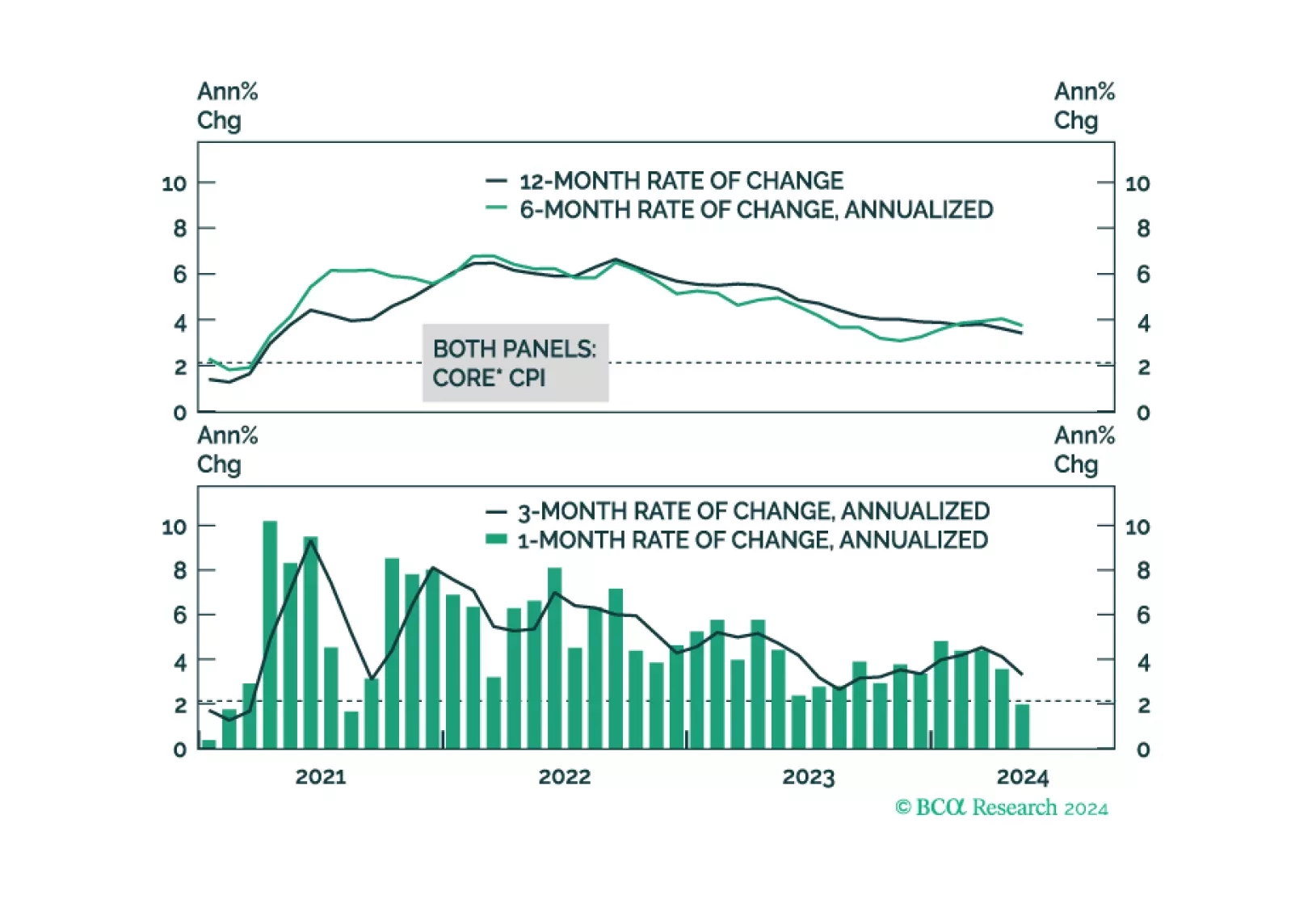

Inflation

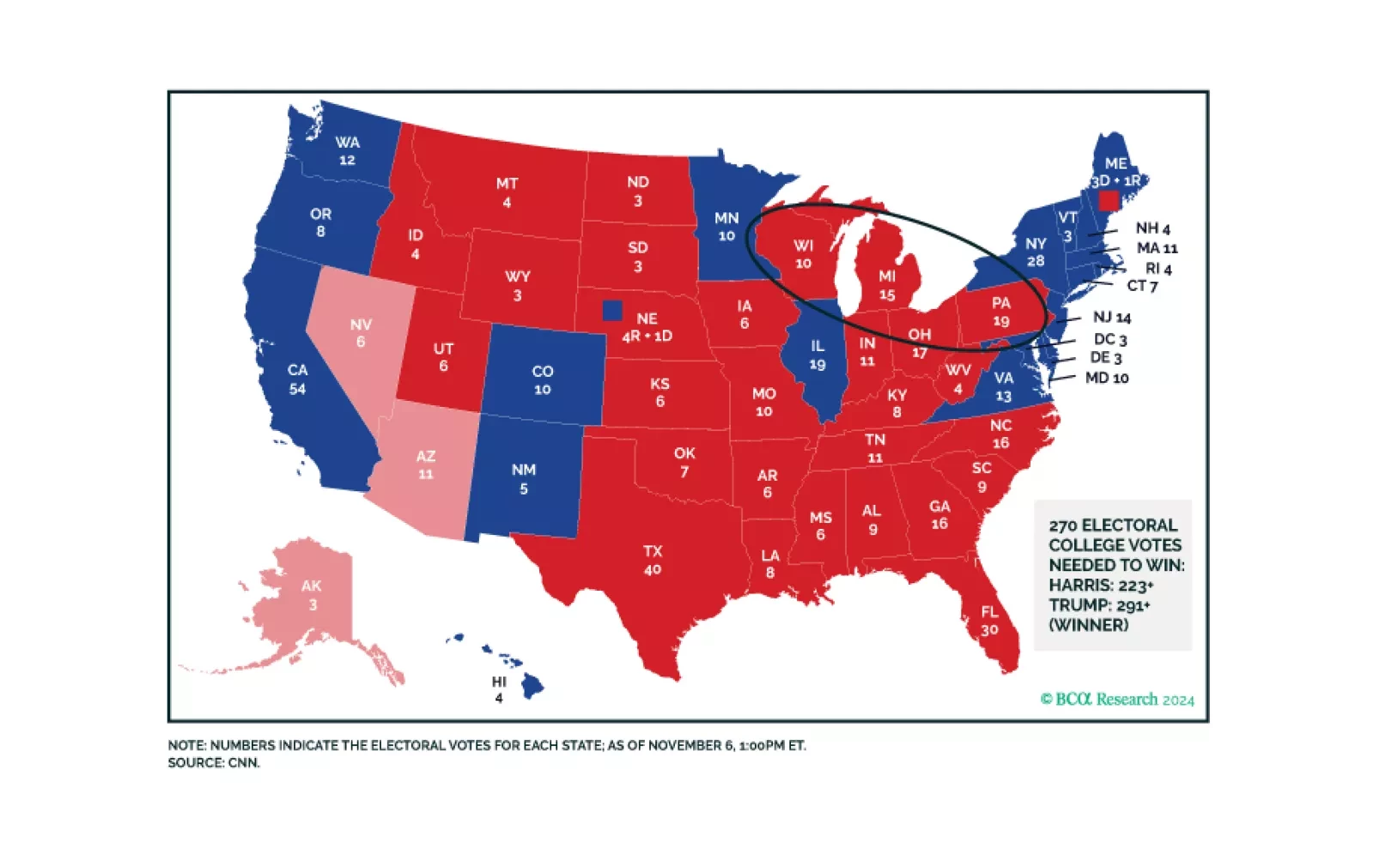

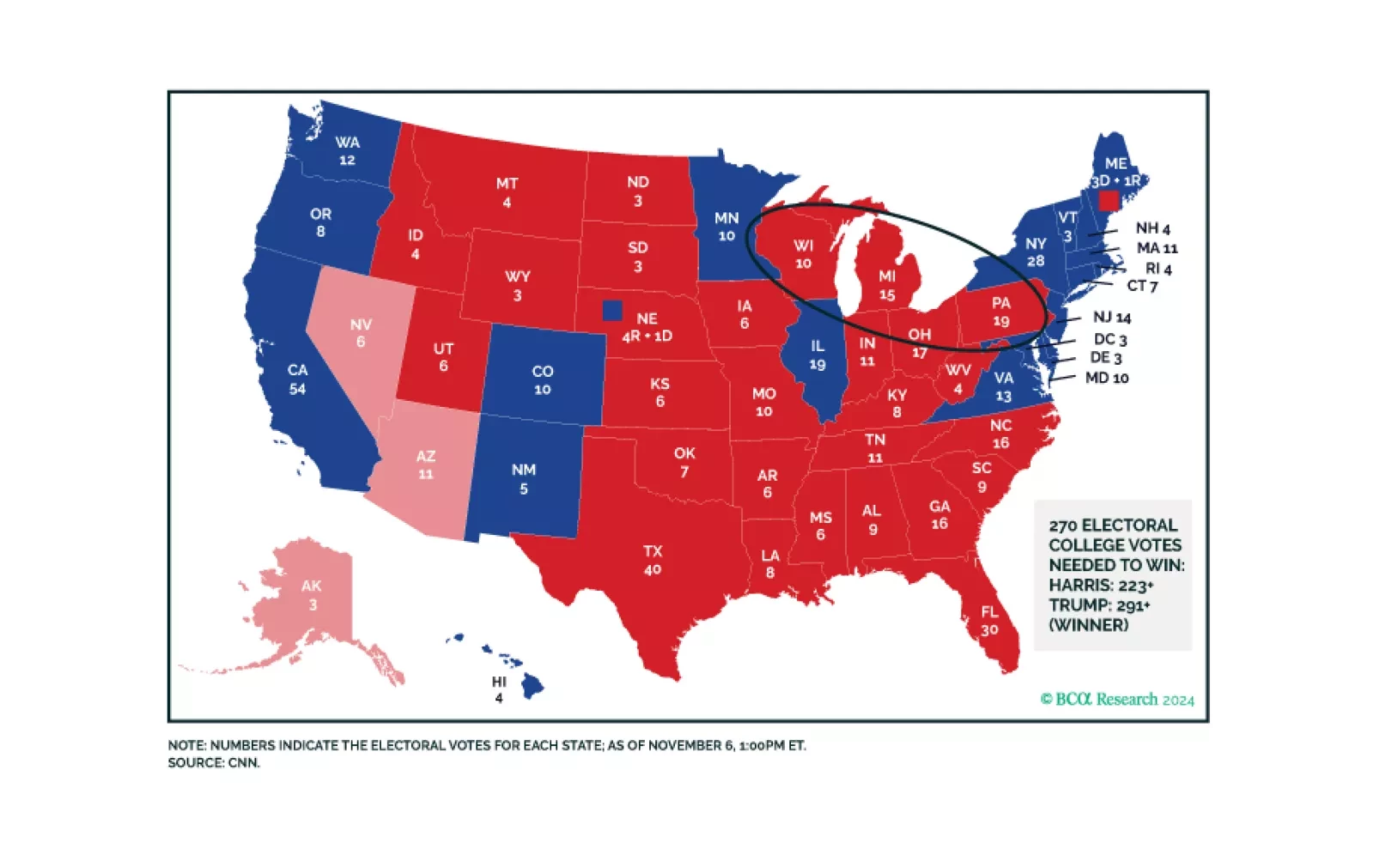

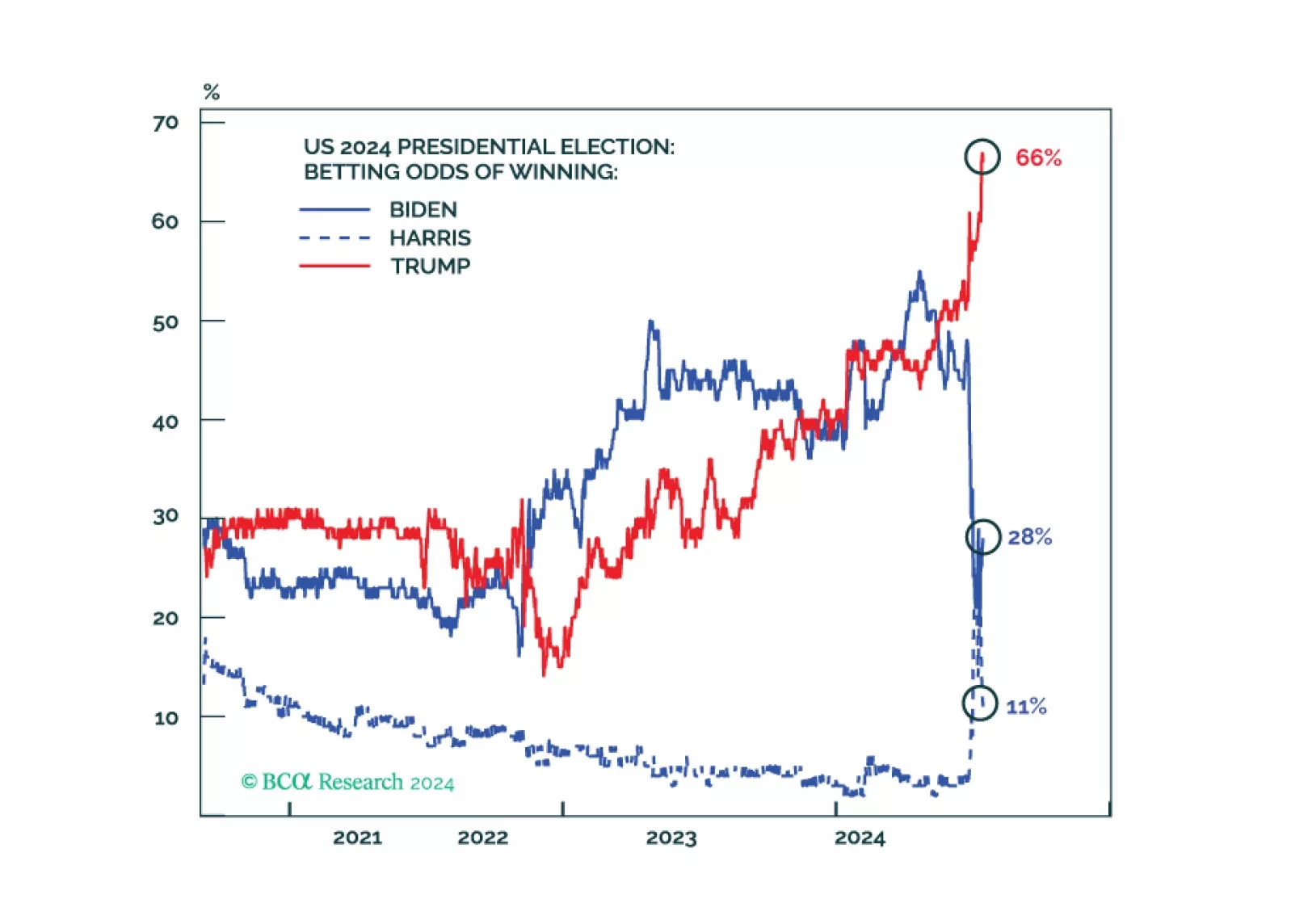

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

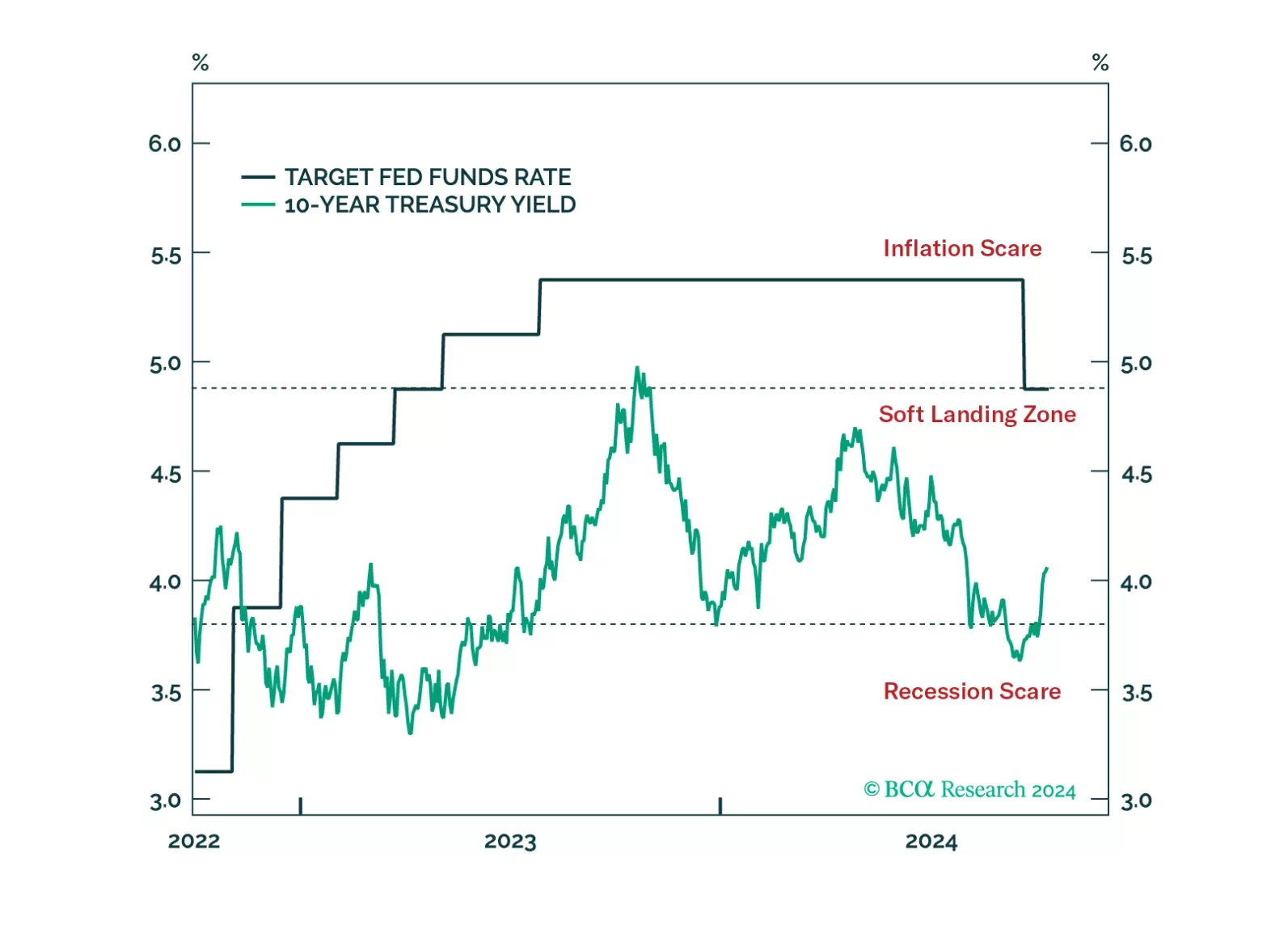

We give our thoughts on this morning’s CPI release and (lack of) market reaction. We also close our short position in January 2025 fed funds futures.

Our reaction to this morning’s CPI report and what it means for Fed policy.

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

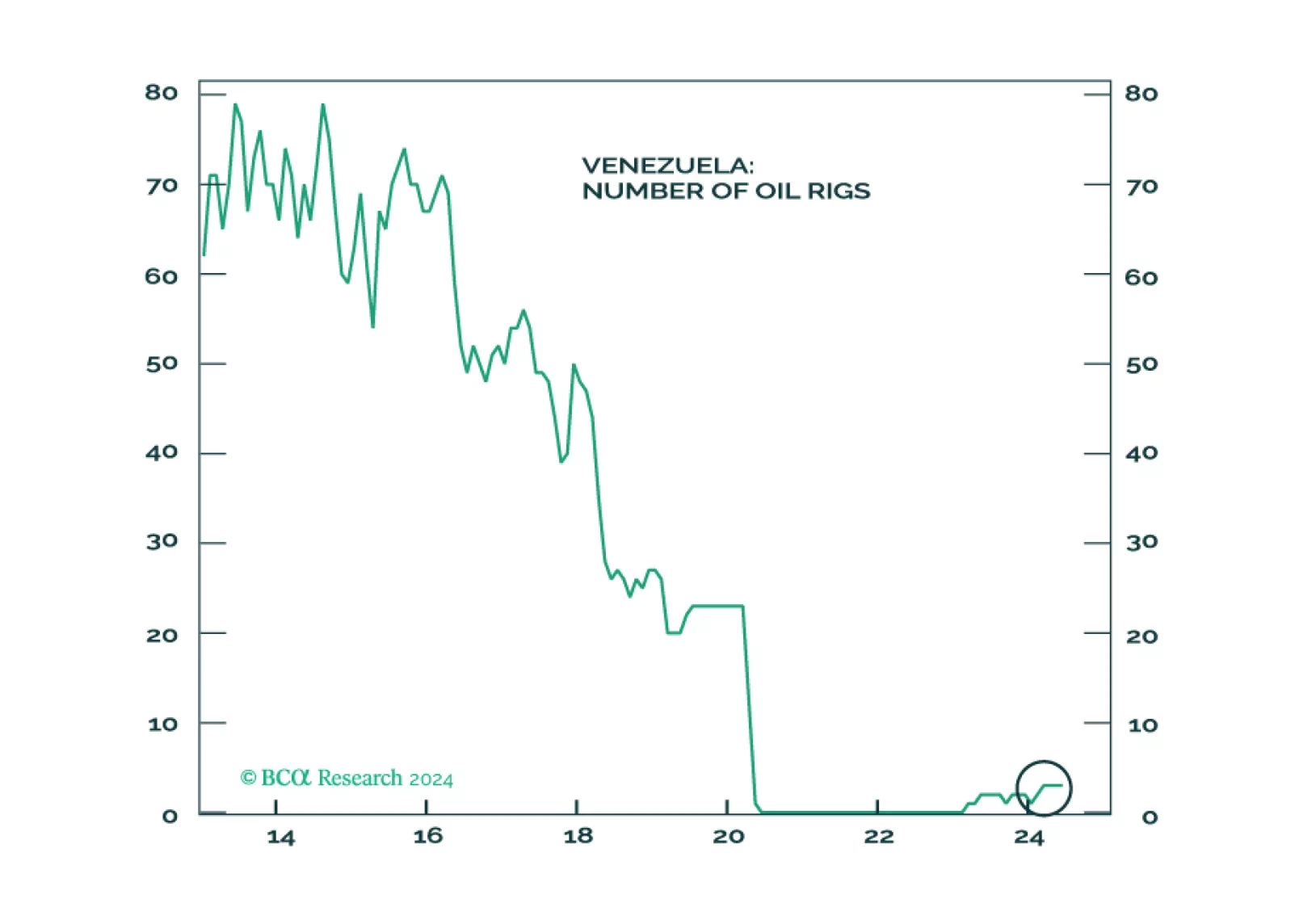

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

The cyclical economy is slowing today. Republicans are now more likely to win a full sweep, crack down on immigration and trade, and at least modestly stimulate the economy. Uncertainty and volatility will rise.

In light of last week’s employment report and this morning’s CPI, it’s time for the Federal Reserve to cut rates.

We consider the outlook for CPI inflation over the next 12 months. Our baseline forecast calls for core CPI to hit 2.40% during this timeframe and for headline CPI to fall between 1.74% and 2.49%.

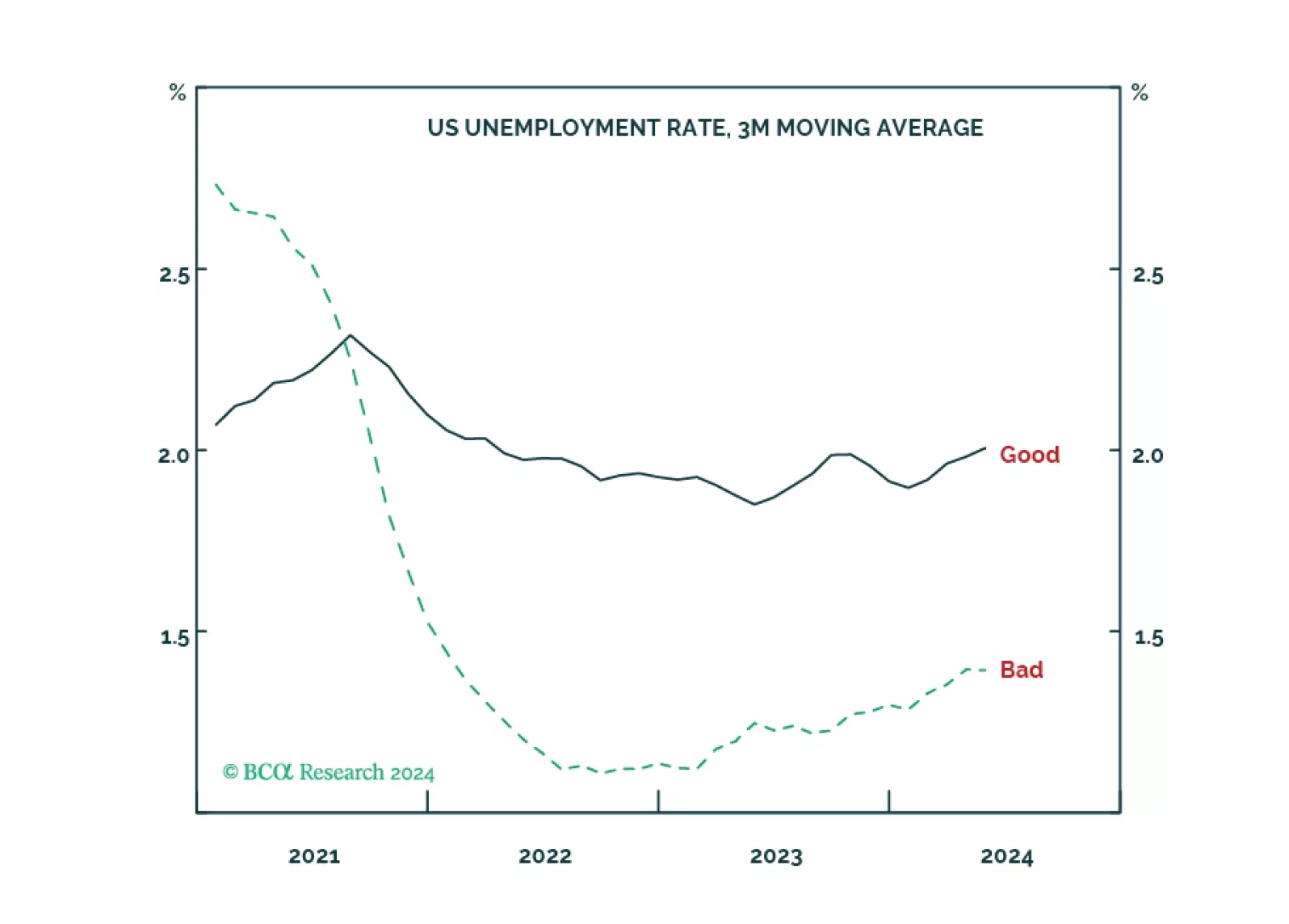

We explain how to distinguish between ‘good’, ‘bad’ and ‘ugly’ unemployment, why bad unemployment is a much better gauge of the jobs market than headline unemployment, and what this means for the tactical positioning in bonds and stocks. Plus: base metals (XBM) have already sold off sharply, so take profits in the short position and open a tactical overweight in global materials (MXI).