Inflation

Some thoughts on this morning’s CPI report and its implications for the Fed and Treasury yields.

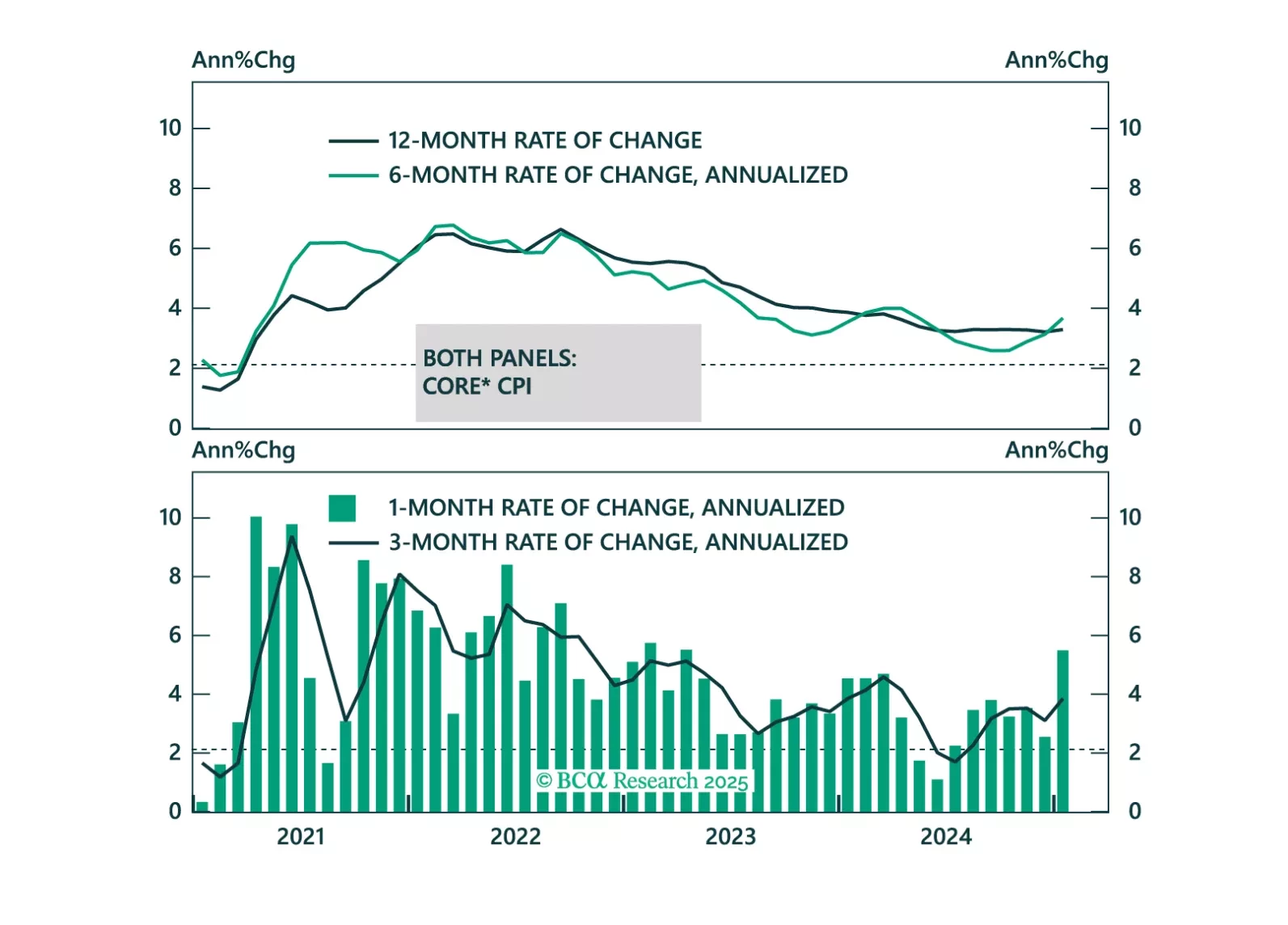

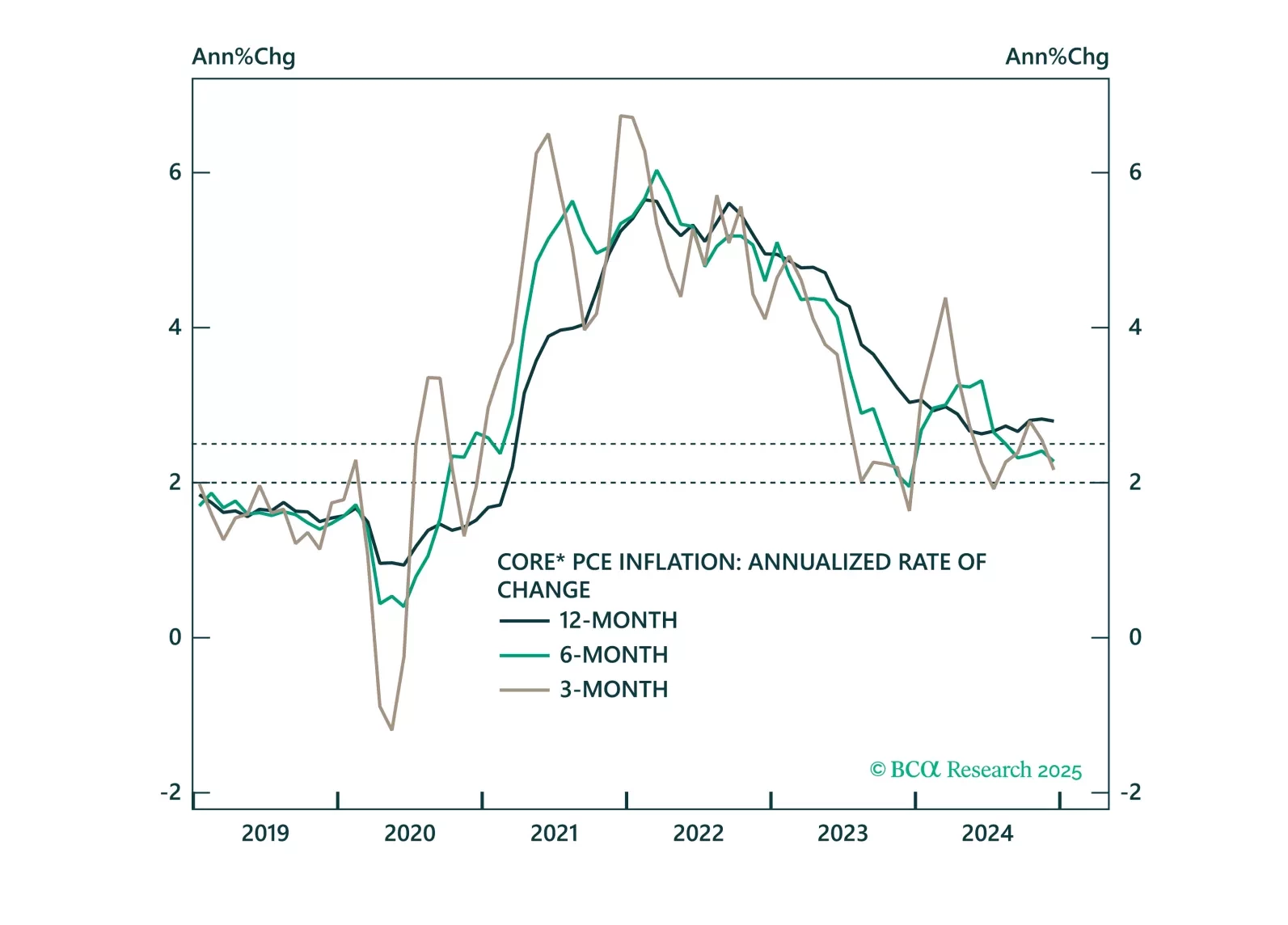

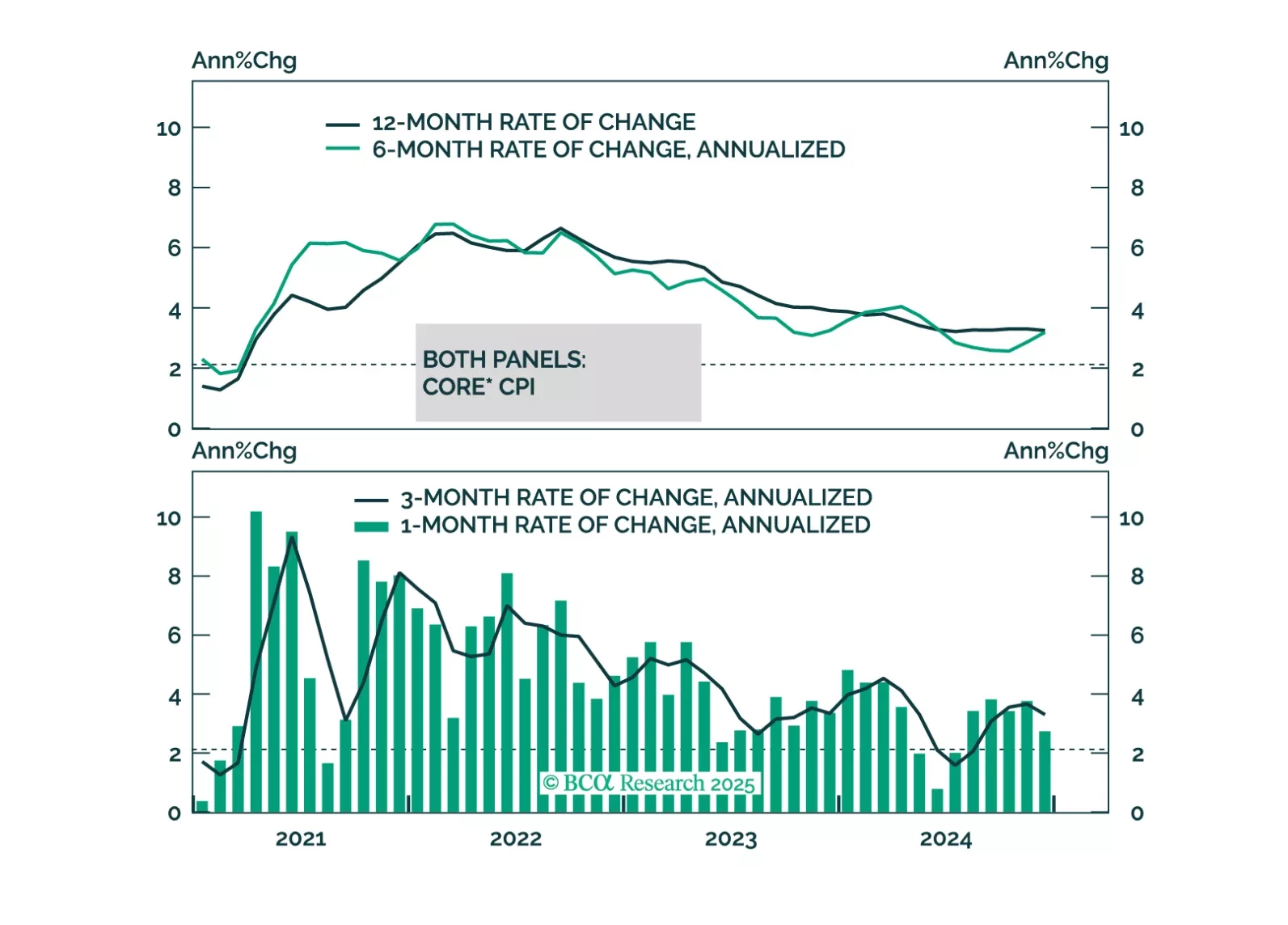

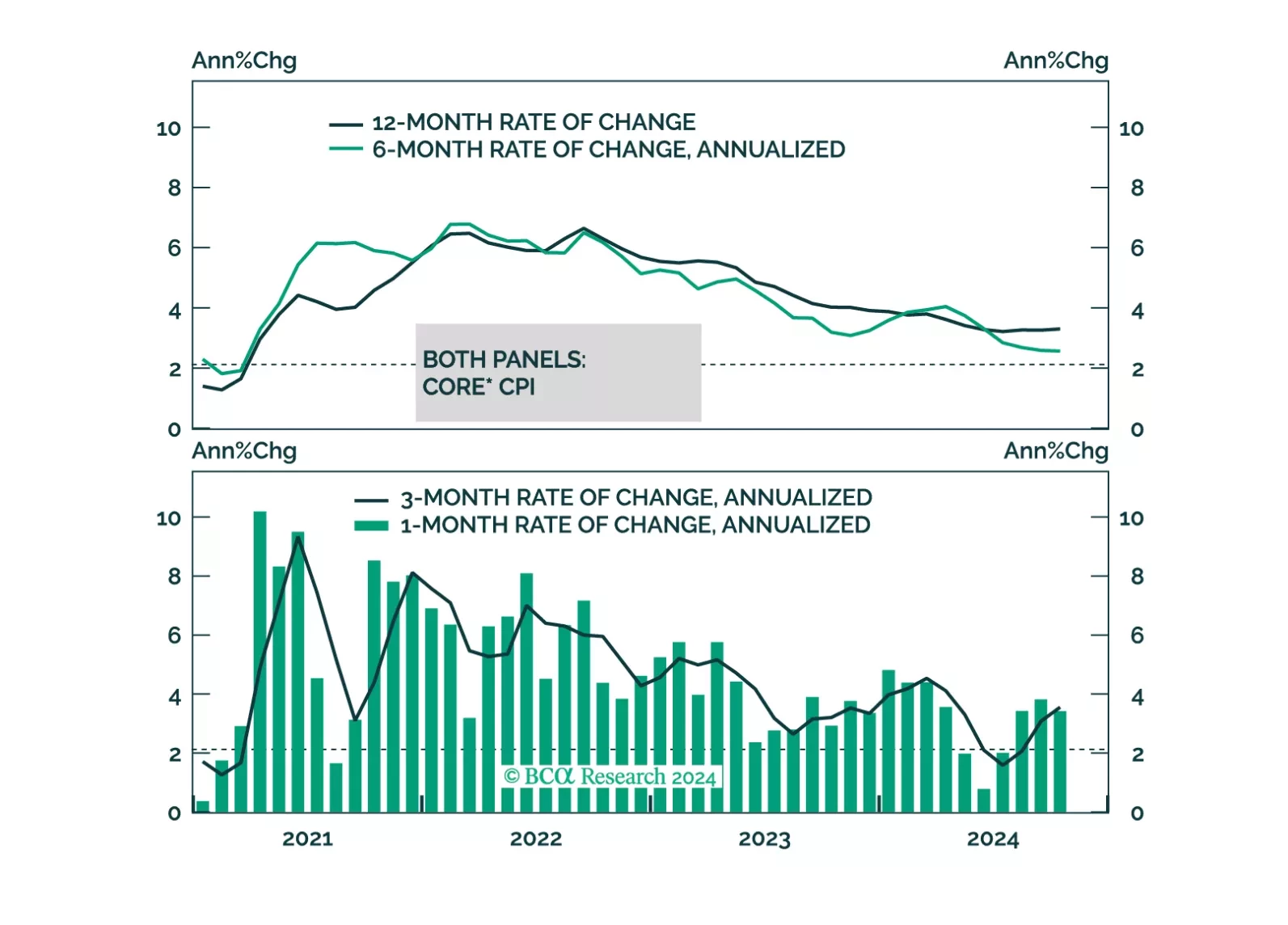

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

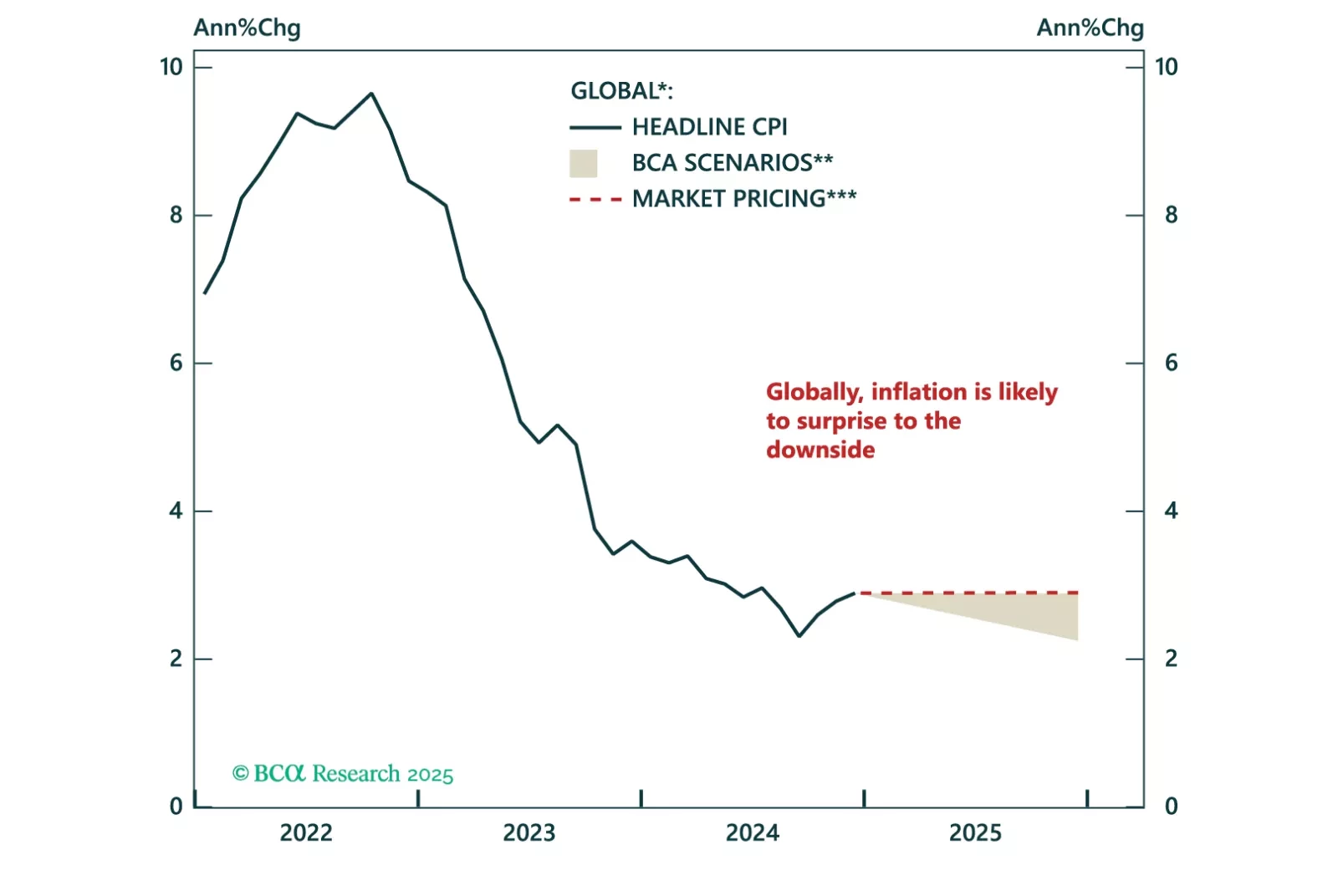

Inflation concerns are starting to ramp up again due to potentially inflationary policies from the new Trump administration. These concerns mostly affect the US inflation outlook. Evidence from forward-looking indicators shows that the global disinflationary trend remains intact. Today’s Special Report covers the global inflation outlook in 2025 and the implications for inflation-linked bonds.

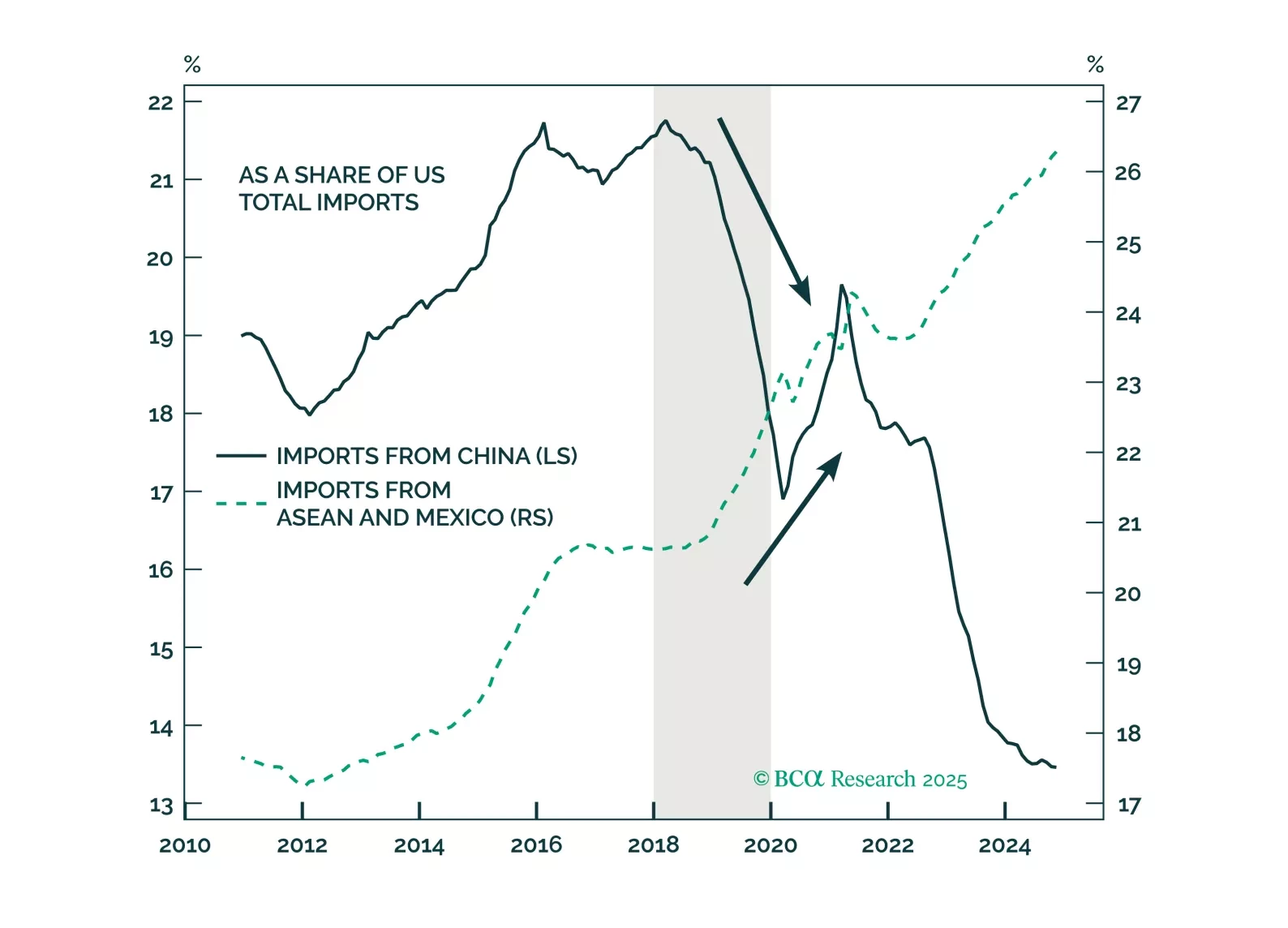

We anticipate decisive tariff measures early in Trump’s second term. In this Special Report, we explore how the costs of higher tariffs might be distributed among foreign suppliers, U.S. importers, and consumers.

Our thoughts on this morning’s CPI release and some upside risks to inflation that could flare up in the months ahead.

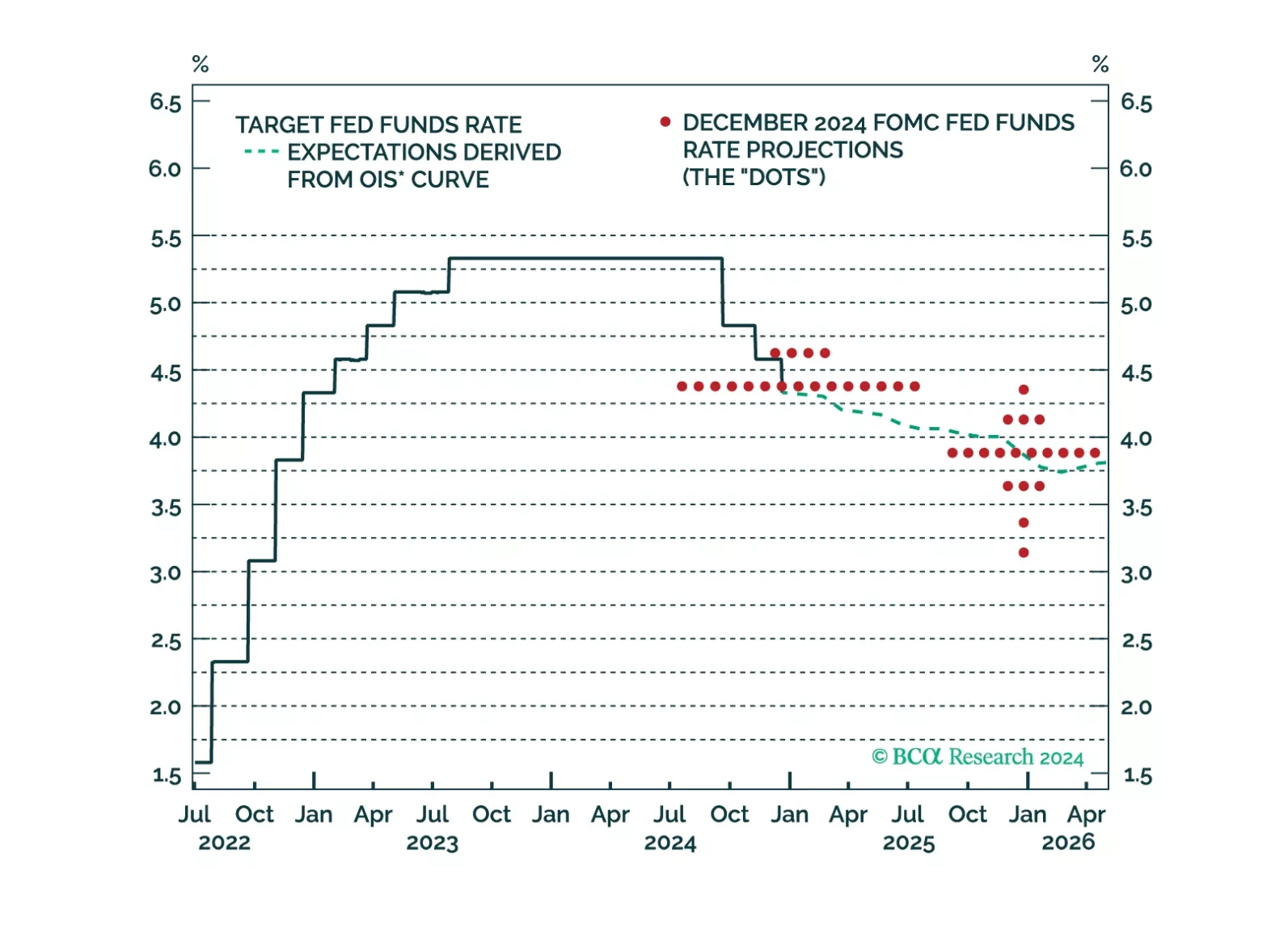

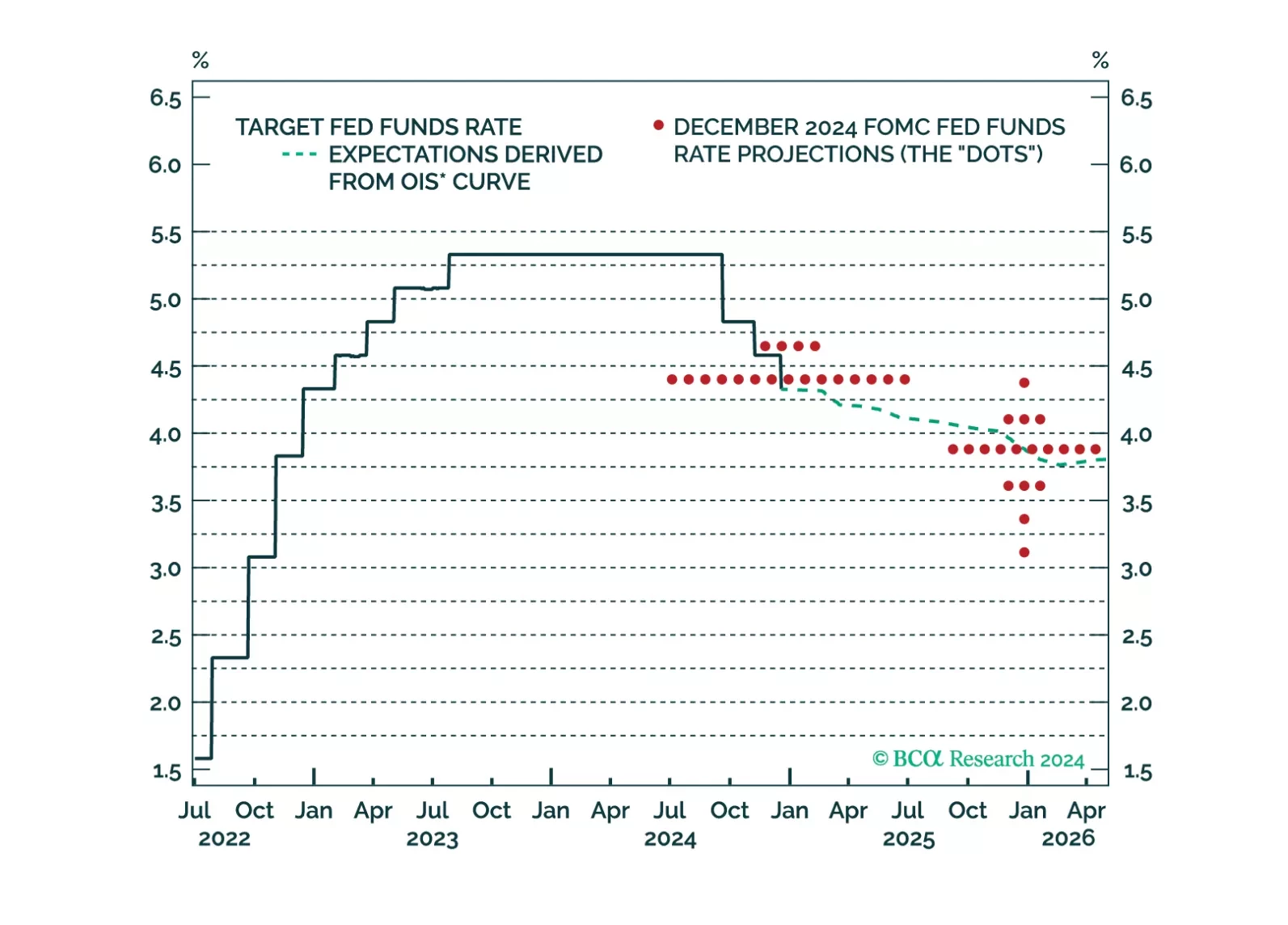

Our outlook for Fed policy in 2025 discusses our expectations for interest rates, the Fed’s balance sheet and the 2025 strategic review.

Our thoughts on this afternoon’s Fed decision and the bond market reaction.

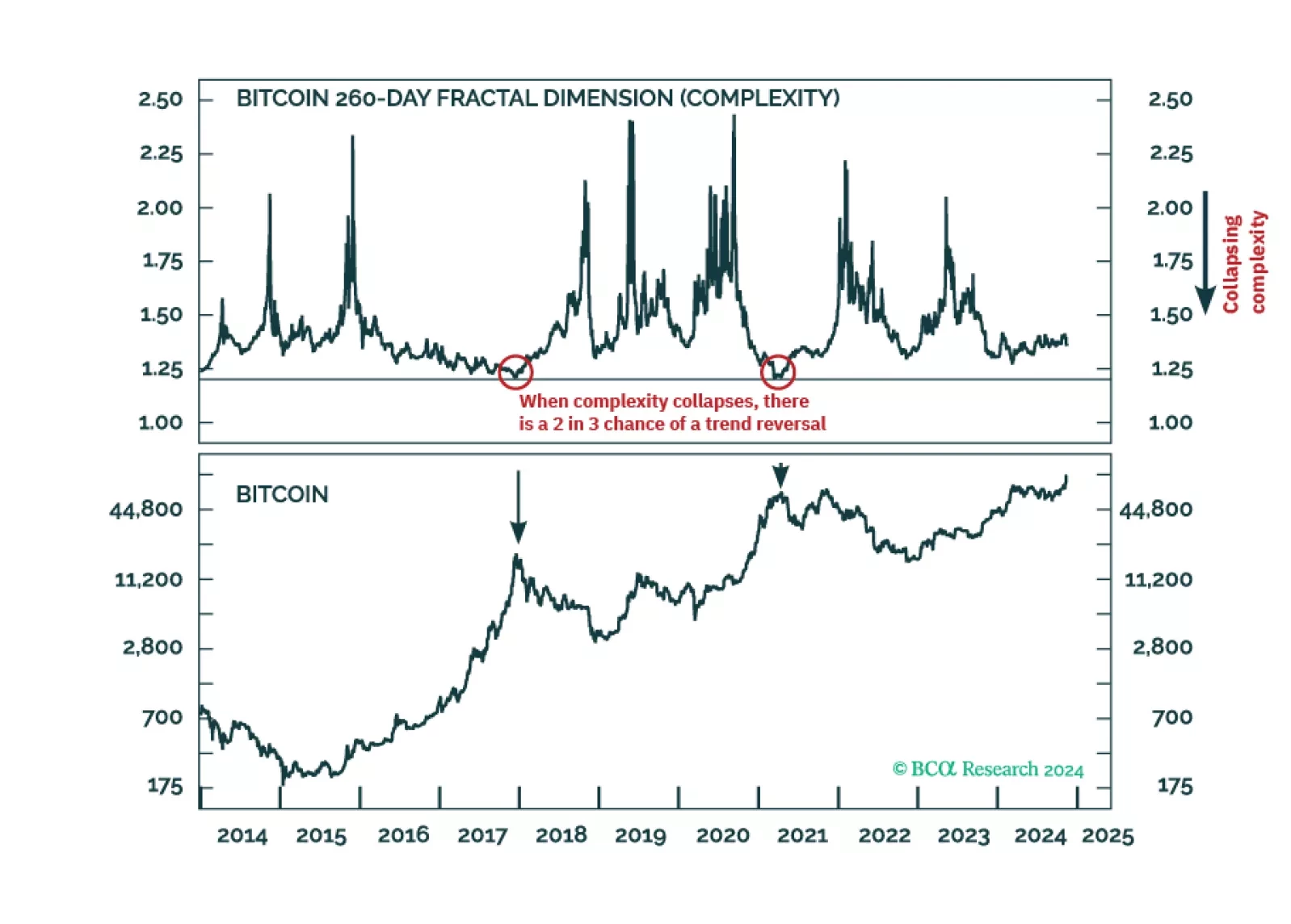

The value of both gold and bitcoin comes from the collective belief that they are the non-confiscatable assets to own in a fiat monetary system, as an insurance against hyperinflation, banking system failure, or state expropriation. As global wealth rises, the value of both gold and bitcoin will also rise. But as bitcoin takes market share from gold, bitcoin has considerably more upside than gold, with an ultimate destination of $200,000+. Plus: 10-year T-bonds and Portuguese stocks are tactically oversold.

We update our inflation forecast following this morning’s CPI release, concluding that TIPS breakeven inflation rates have room to fall.