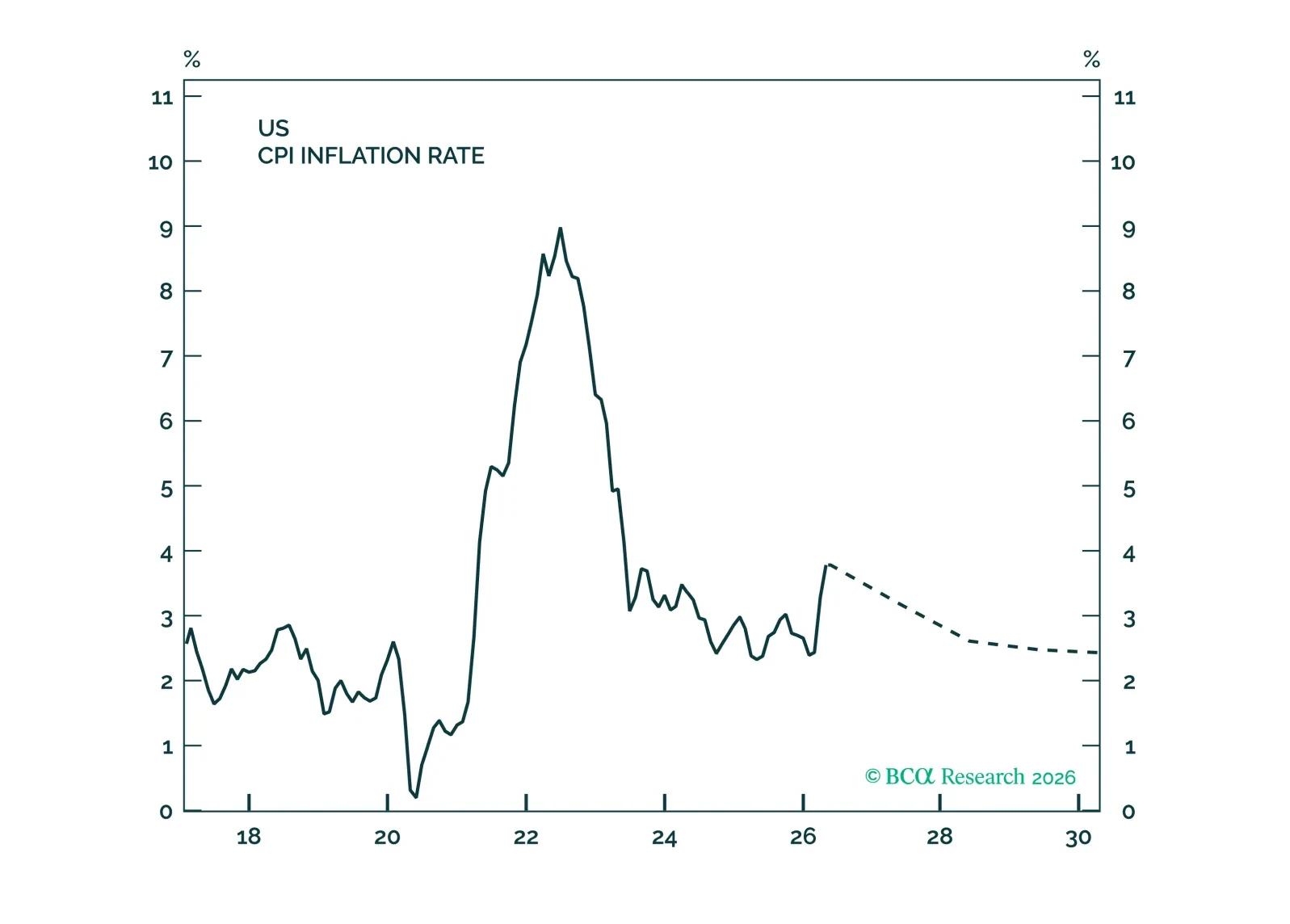

Inflation

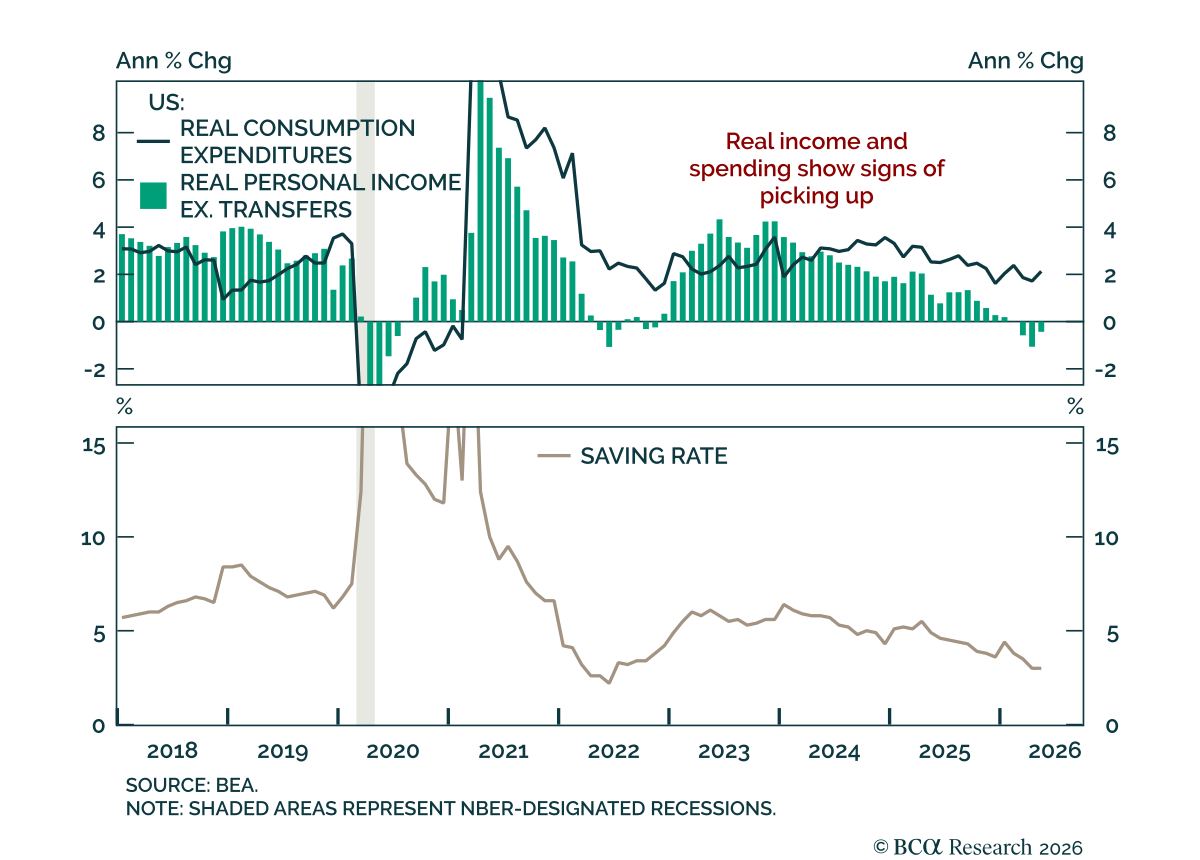

The May Personal Income and Outlays report beat estimates, showing firmer consumer momentum but still-sticky inflation. Both nominal and real spending beat estimates, rising 0.7% m/m and 0.3%, respectively. Personal income was also strong at 0.7%, while real…

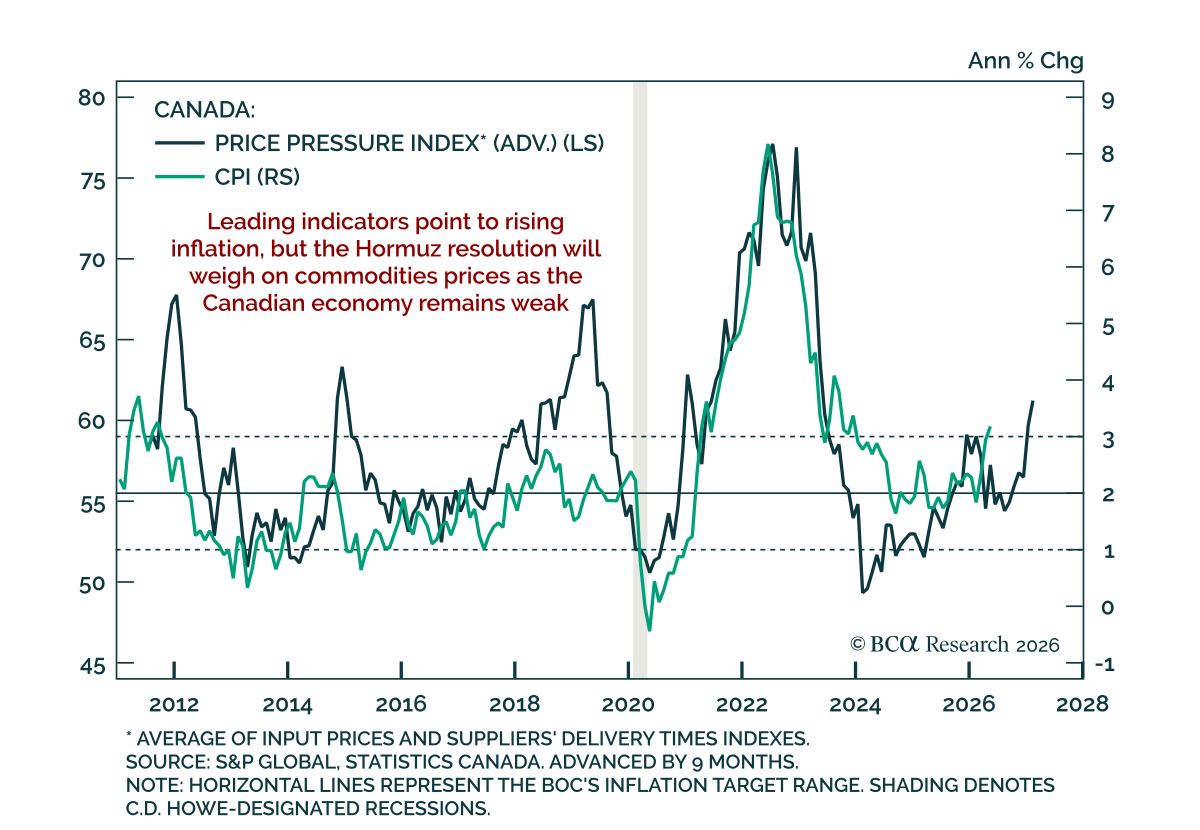

Canadian May inflation was hotter than estimates, but the underlying inflation picture remains much more muted. Headline CPI rose to 3.2% from 2.8%, moving above the Bank of Canada’s 1%-to-3% target range. The increase, however, was driven by energy, which…

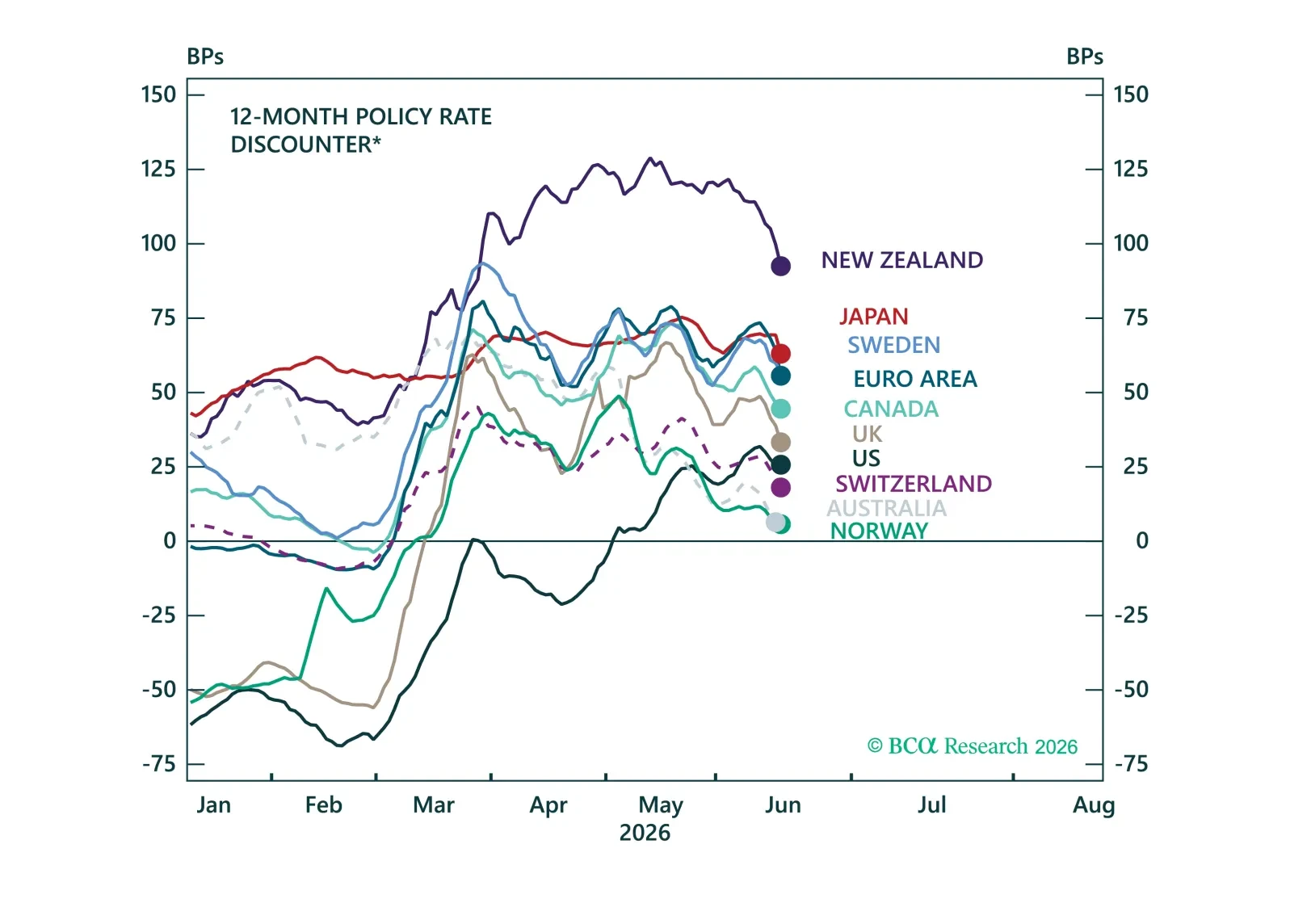

We react to DM central bank meetings this week and highlight the opportunities emerging across global fixed income and currency markets.

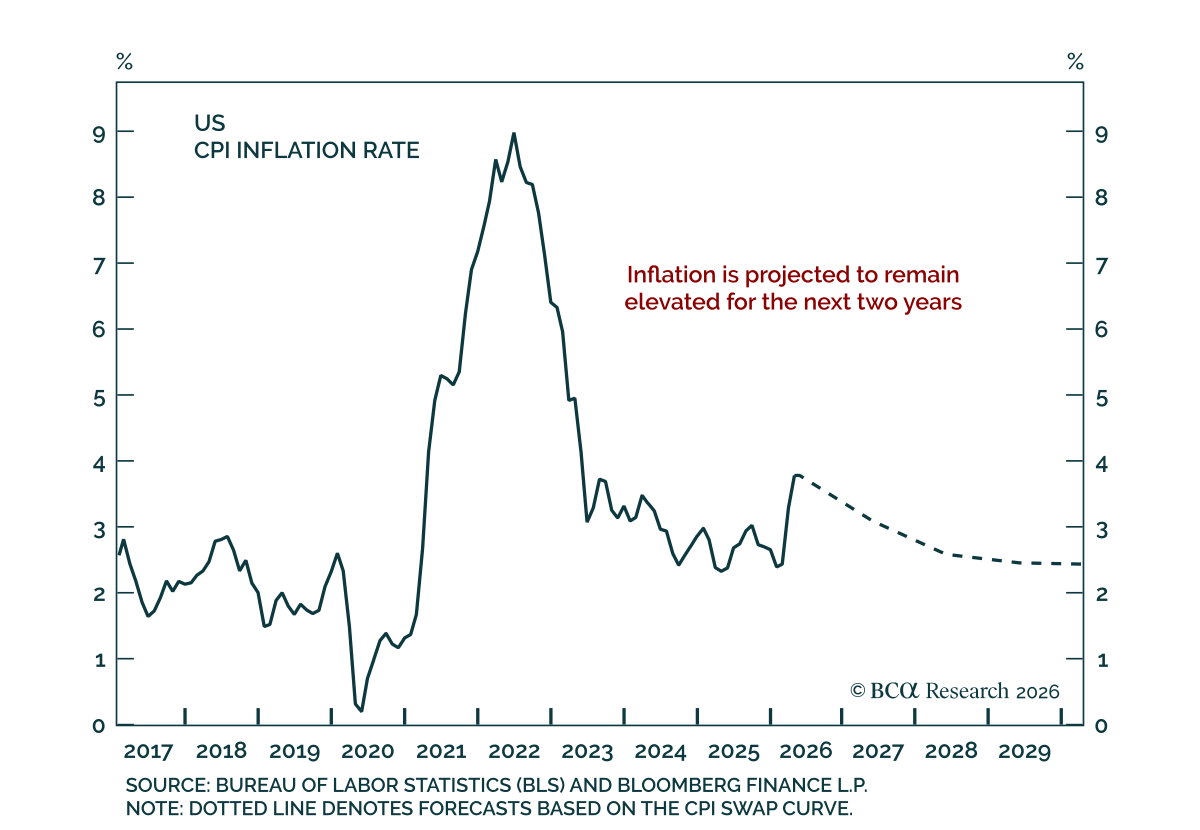

May US CPI was roughly in line with estimates and still shows no evidence of energy passing through to core inflation. Headline CPI rose 0.5% m/m, accelerating to 4.2% y/y from 3.8%. Core came in cooler than estimates at 0.2% m/m, down from 0.4% in April,…

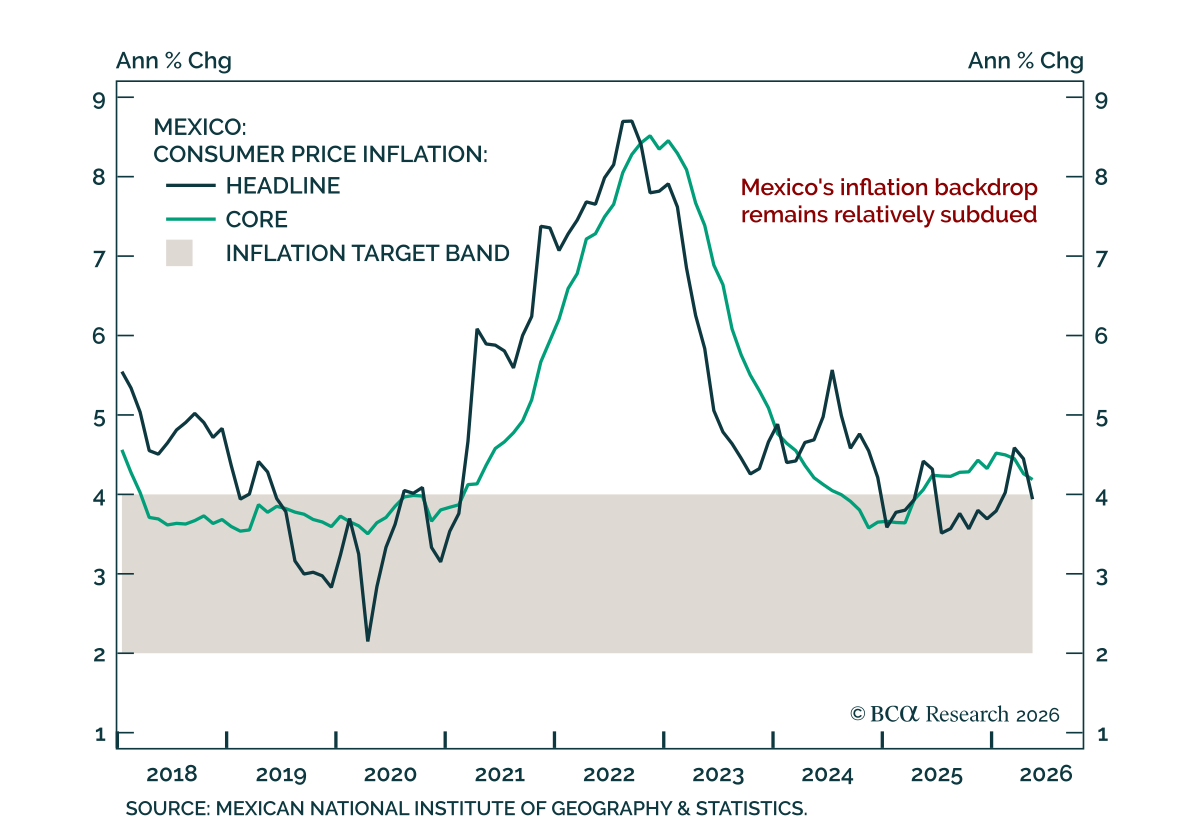

Mexican inflation has eased back to the high end of the target range, but Banxico likely still has room to cut over a cyclical horizon. Some concern around core price pressures remains, and Banxico ended its two-year easing cycle last month. Our Emerging…

Our June BCA Views meeting concluded that the near-term case for staying overweight equities remains intact. The discussion centered on whether the Middle East conflict, sticky inflation, and a maturing AI capex cycle are enough to challenge that view. The…

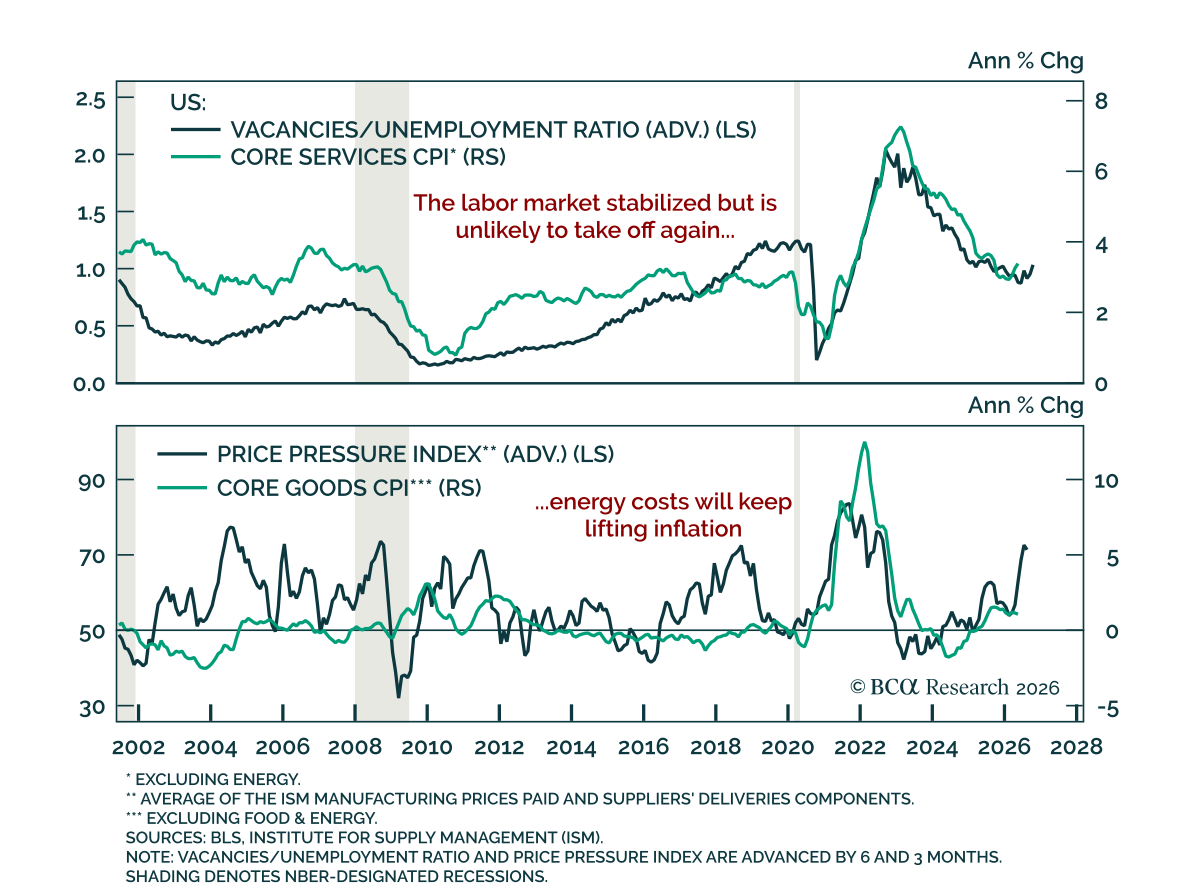

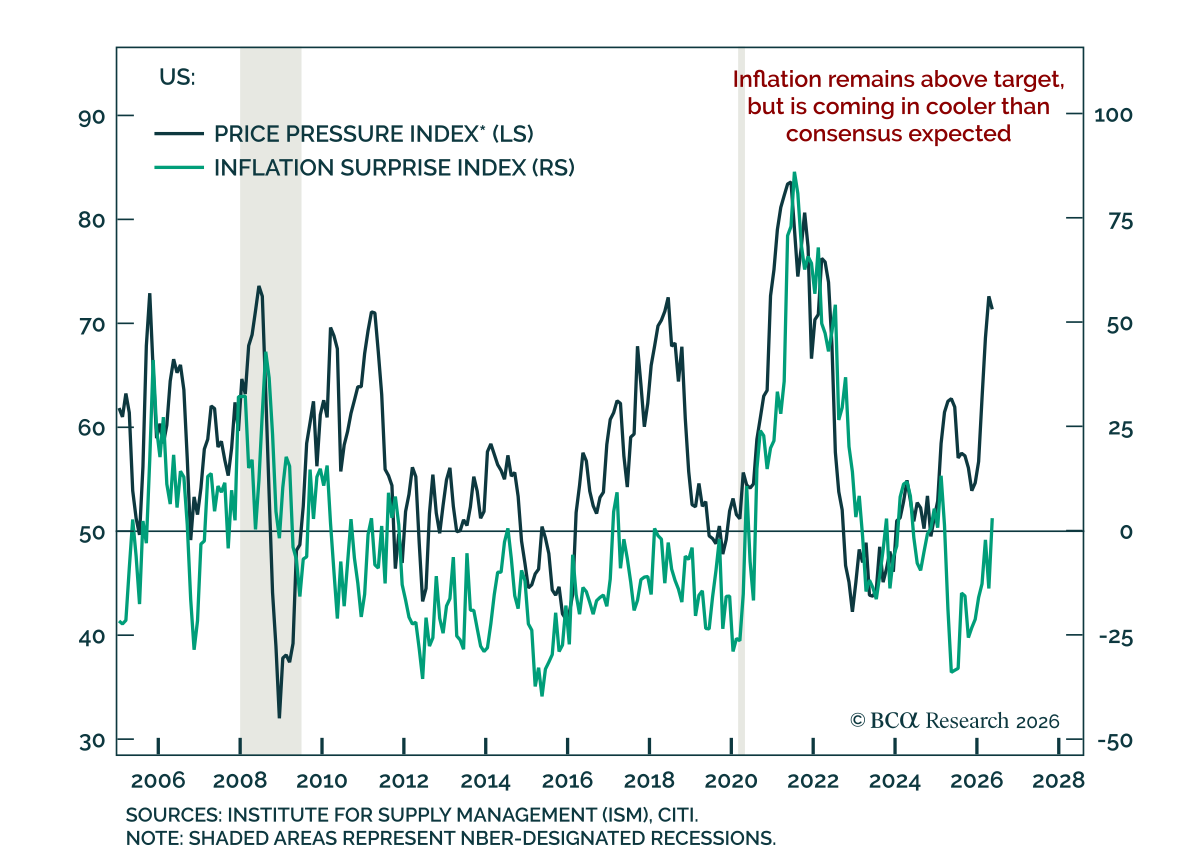

A notable pattern is emerging globally: inflation remains above target, but it is coming in cooler than consensus expected. US inflation came in below estimates. The same pattern has appeared in European developed and emerging markets, including Switzerland…

BCA’s Global Investment Strategy team challenges Fed Chair Kevin Warsh's view that AI will prove disinflationary, particularly on the near-term inflation impact. Our colleagues argue AI is currently pushing up costs across a range of inputs, including power…

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

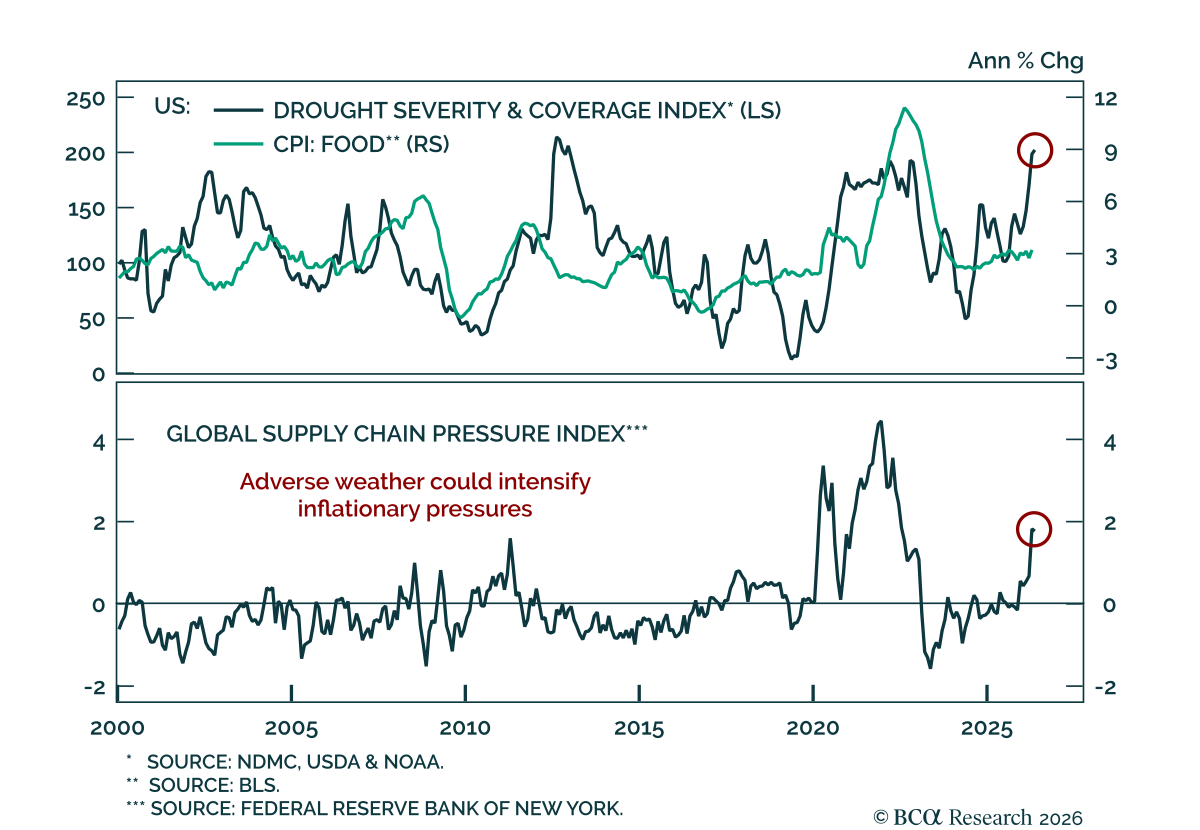

Severe US droughts reinforce an already inflationary backdrop and highlight risks of overshoots, warranting close monitoring. Close to 60% of continental US territory is in drought conditions, making this one of the worst drought episodes on record, according…