Inflation

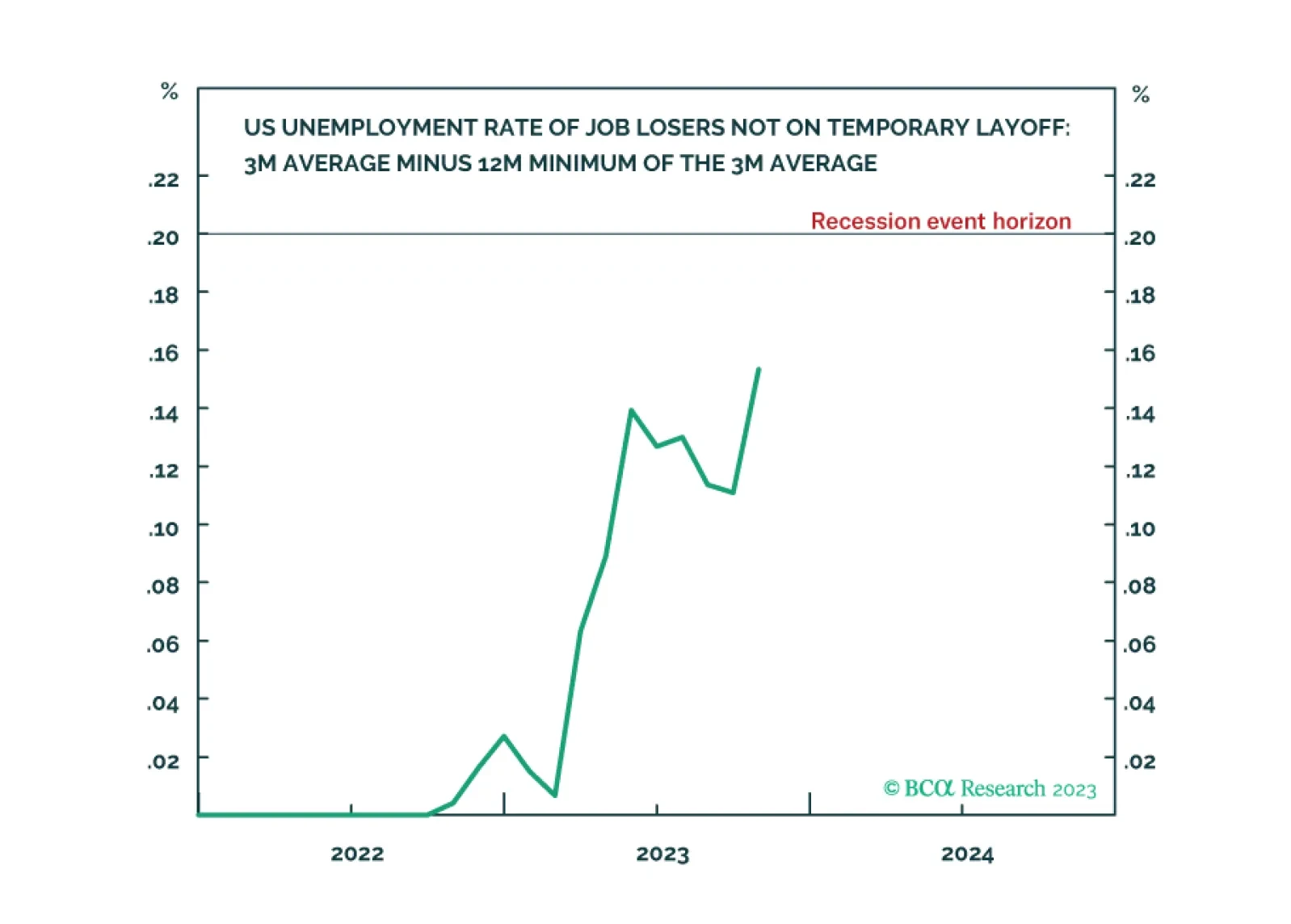

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.

In financial systems, cracks typically begin on the periphery and then expand to the center. Hence, the ruptures on the fringes often act as an early warning. These fissures tend to widen and spread to the core, causing a breakdown in the S&P 500. Investors should consider buying US Treasurys aggressively when the S&P 500 slips below 4,000.

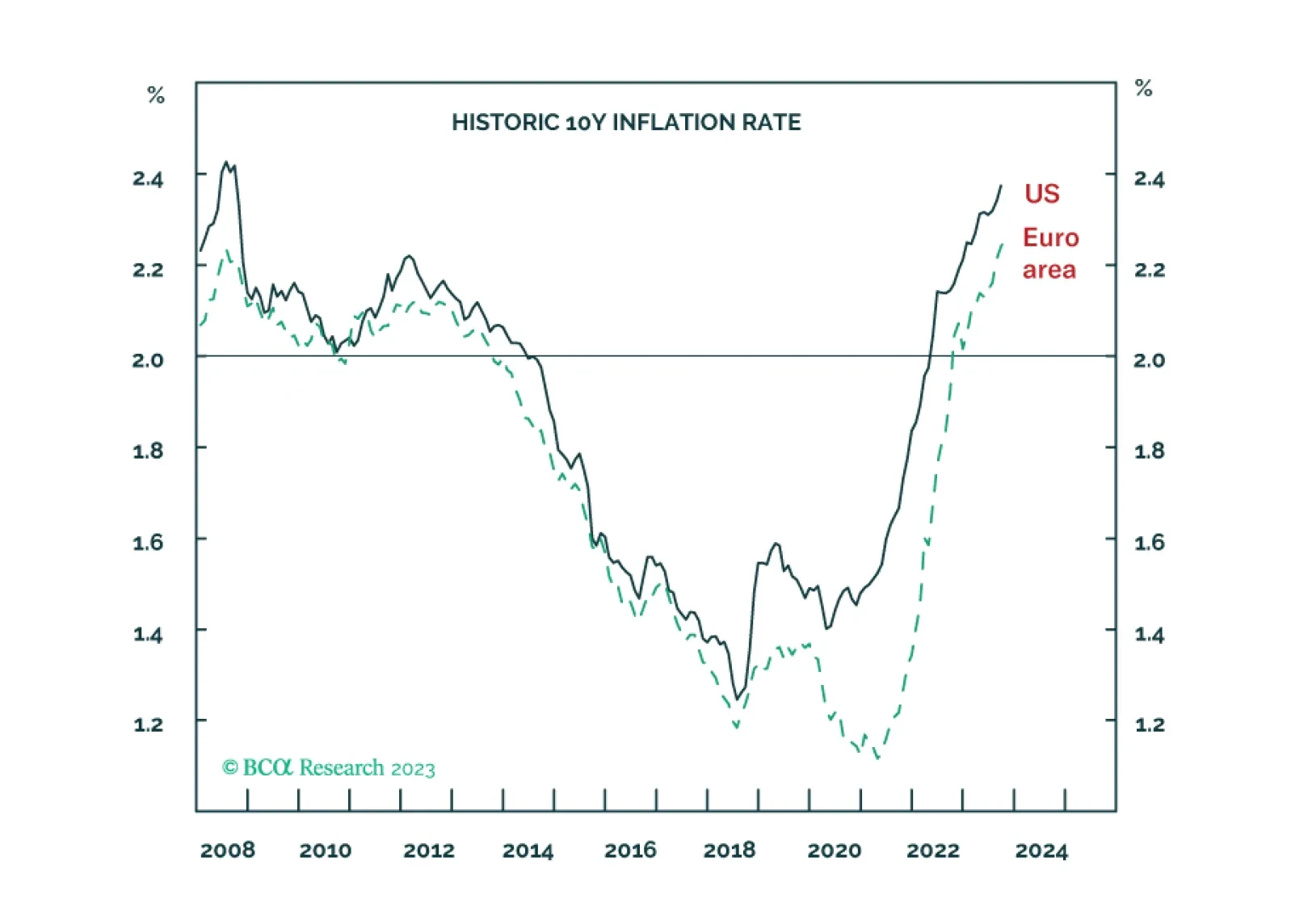

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.

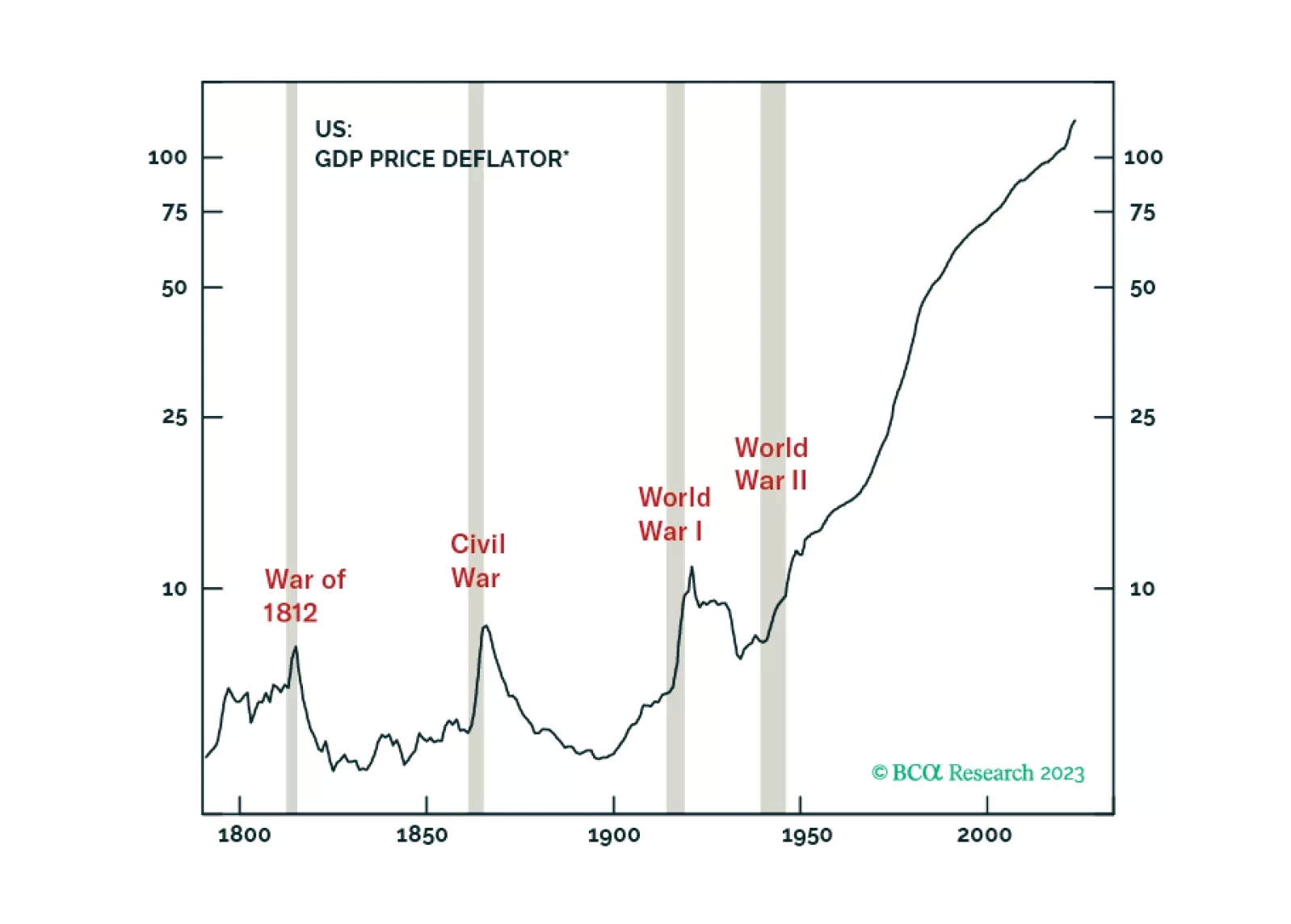

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

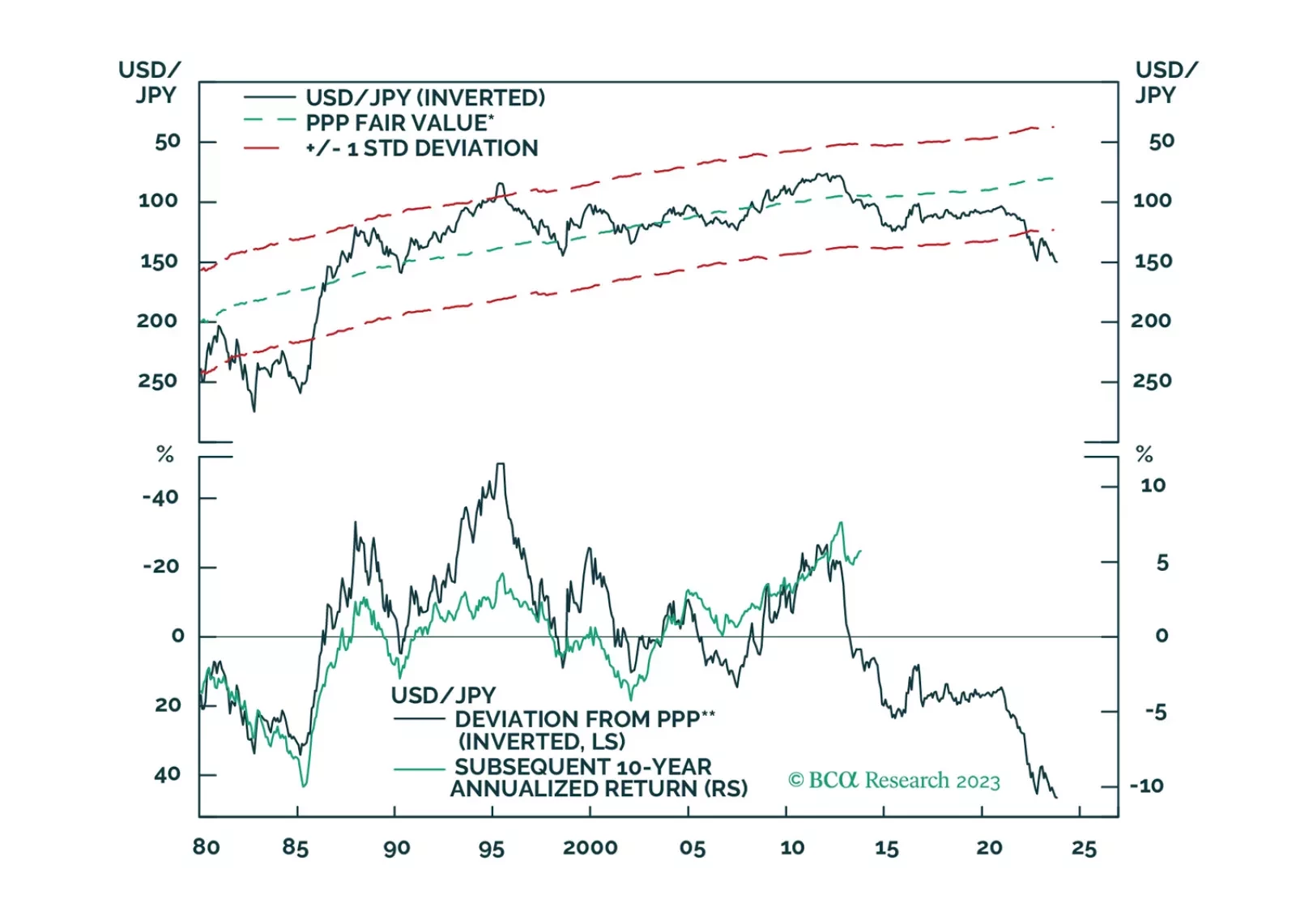

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

The Hamas attack against Israel, timed almost 50 years to the day after a similar surprise attack on Yom Kippur of 1973, has evoked parallels with the 1970s. Parallels not only with Middle Eastern geopolitics then and now, but also with inflation, economics, and financial markets. In this report, we explain what went wrong in the 1970s and whether the mistakes will be repeated. Plus: the sharp sell-offs in some Latin American currencies are reaching a potential turning-point.

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

The sharp sell-off in long duration bonds (ticker TLT) has reached the collapsed 130-day complexity that implies a probable and playable rebound. More strategically, long-duration bonds yielding close to 5 percent are an excellent structural investment assuming central banks choose to slay inflation and the cost is a near-term recession. We discuss how to time and how to play the potential rebound.

The bear market in US bonds will likely end with a bang rather than a whimper. Even during the secular US bond bull market of 1982-2021, cyclical bond bear markets ended only after an eruption of financial turmoil. It would be strange if this current ascent in bond yields ended without significant casualties in the global financial system.