Inflation

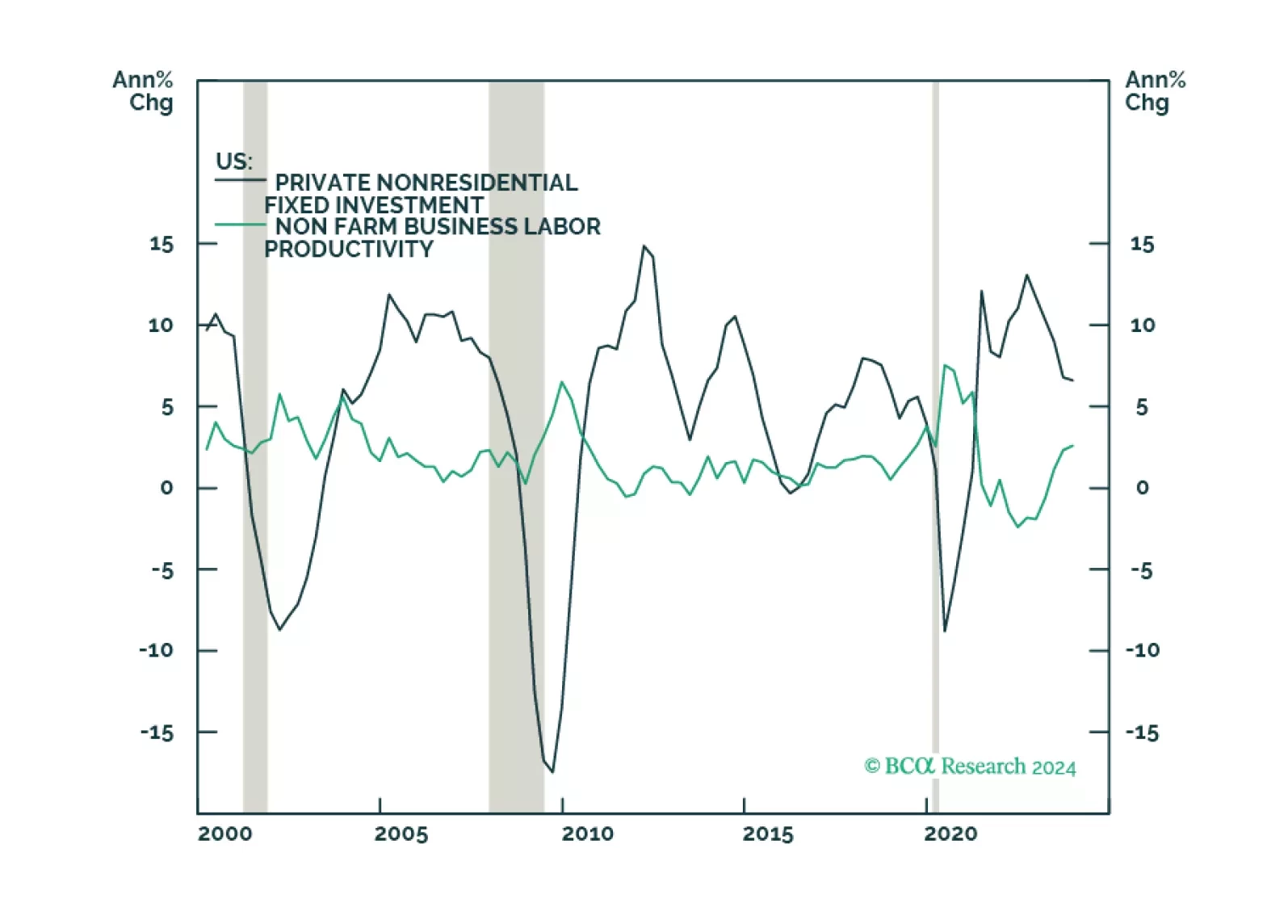

Inflationary pressures this year will remain subdued as labor-productivity growth – driven by strong capex and R+D spending – continues. This will make the Fed more confident in beginning its policy-rate-cutting cycle in June, and will keep gold well bid. We are raising our gold target to $2,300/oz. We continue to expect no recession this year.

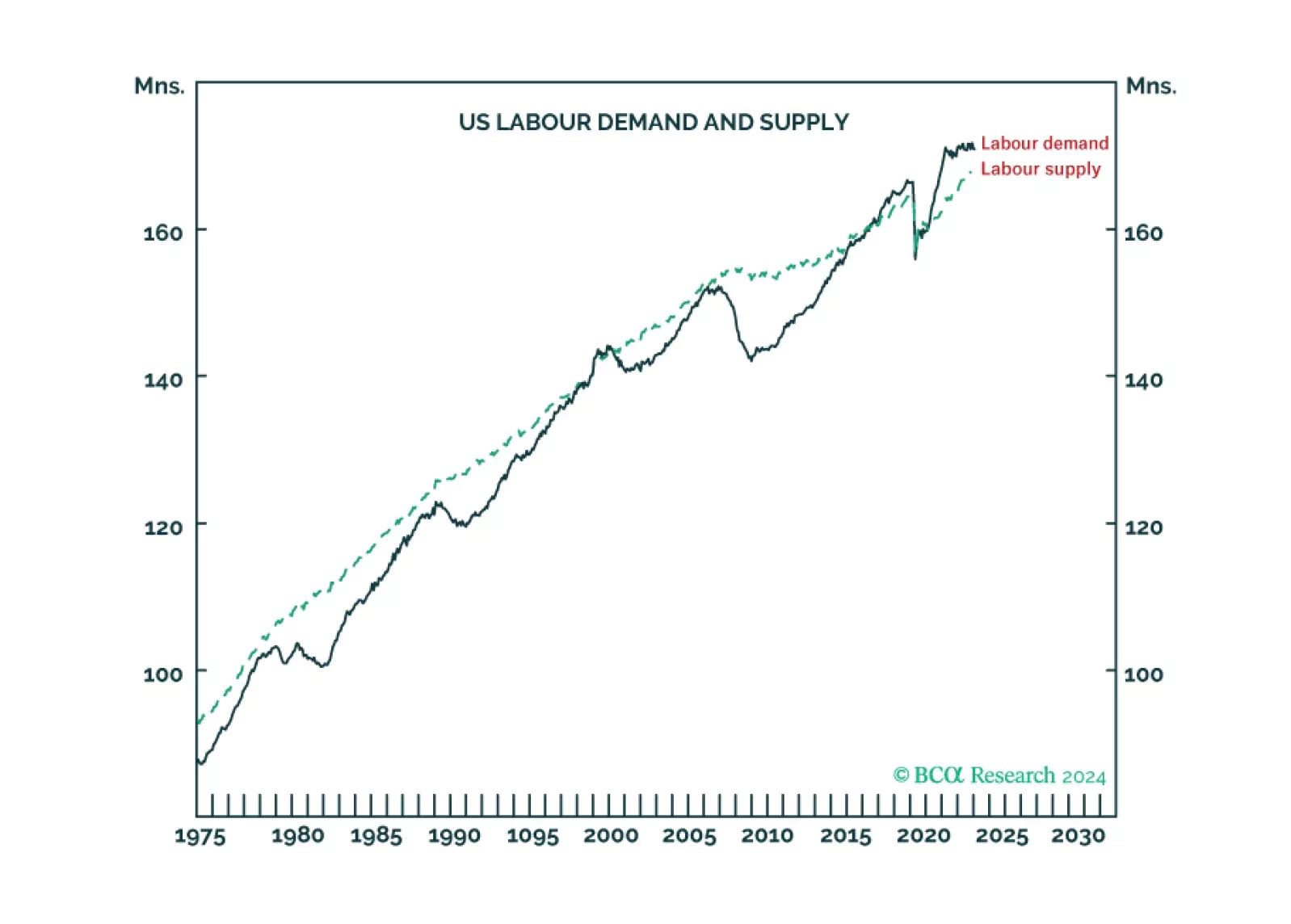

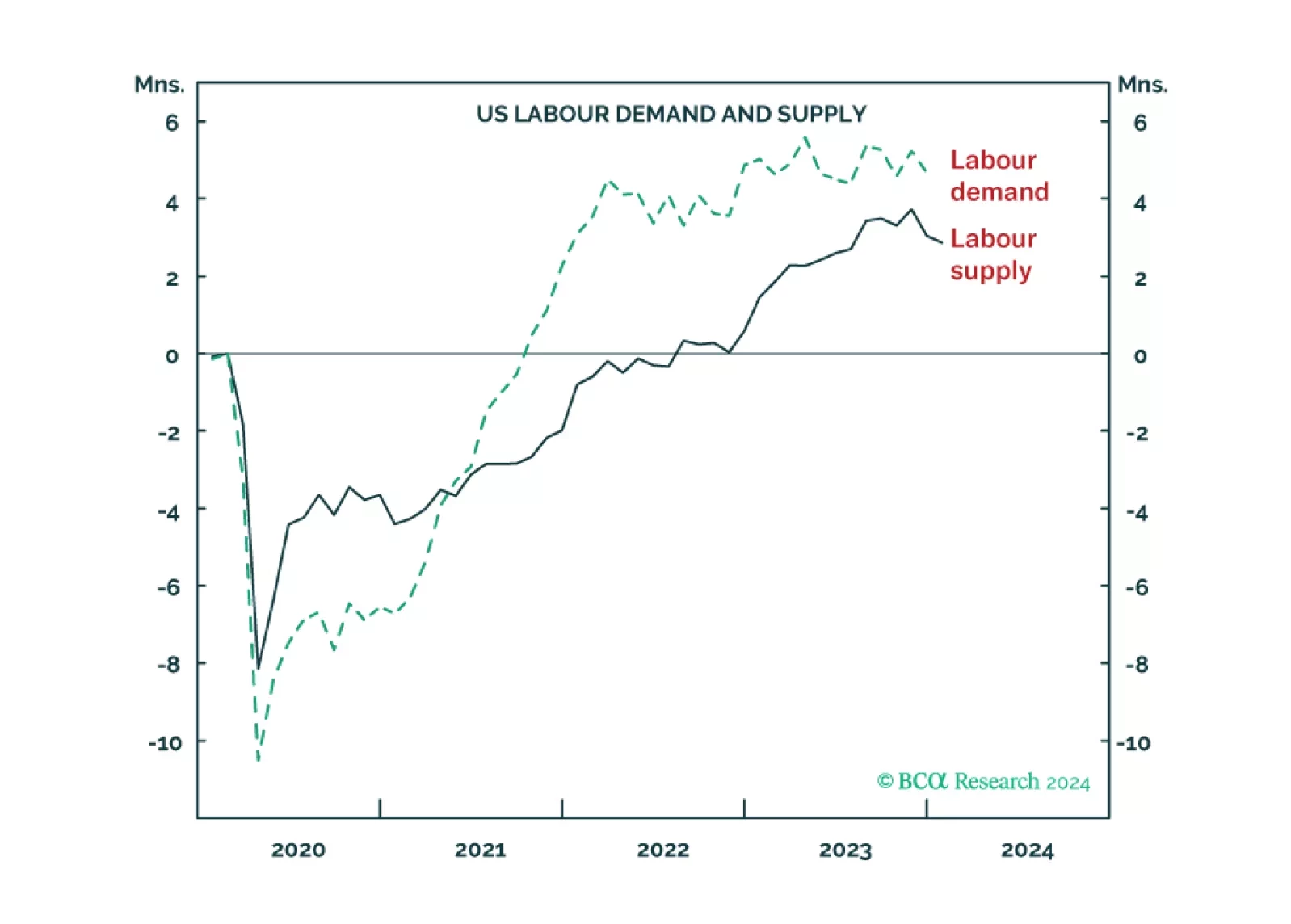

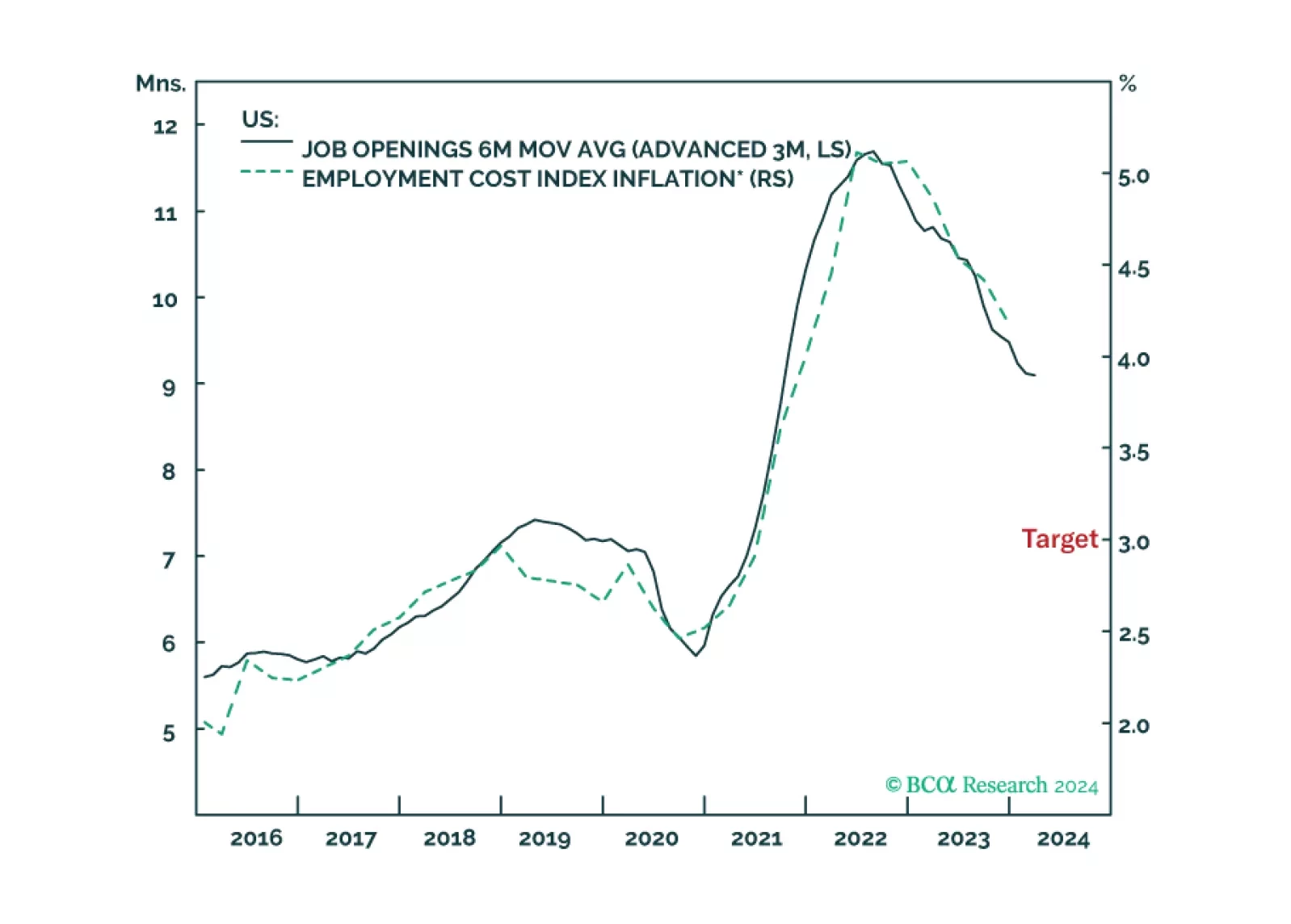

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and asset allocation. Plus: NVDA is at a consolidation point.

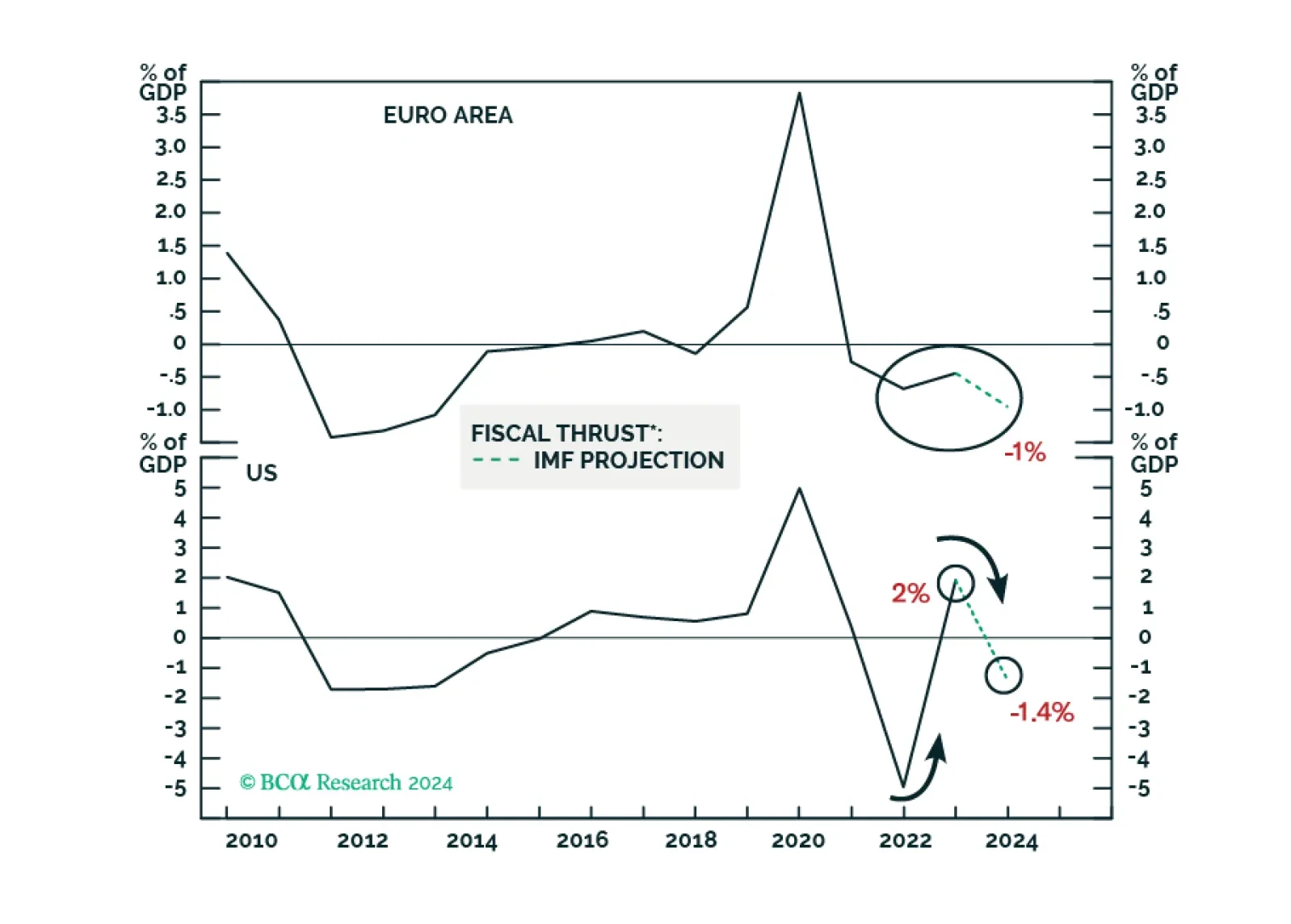

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

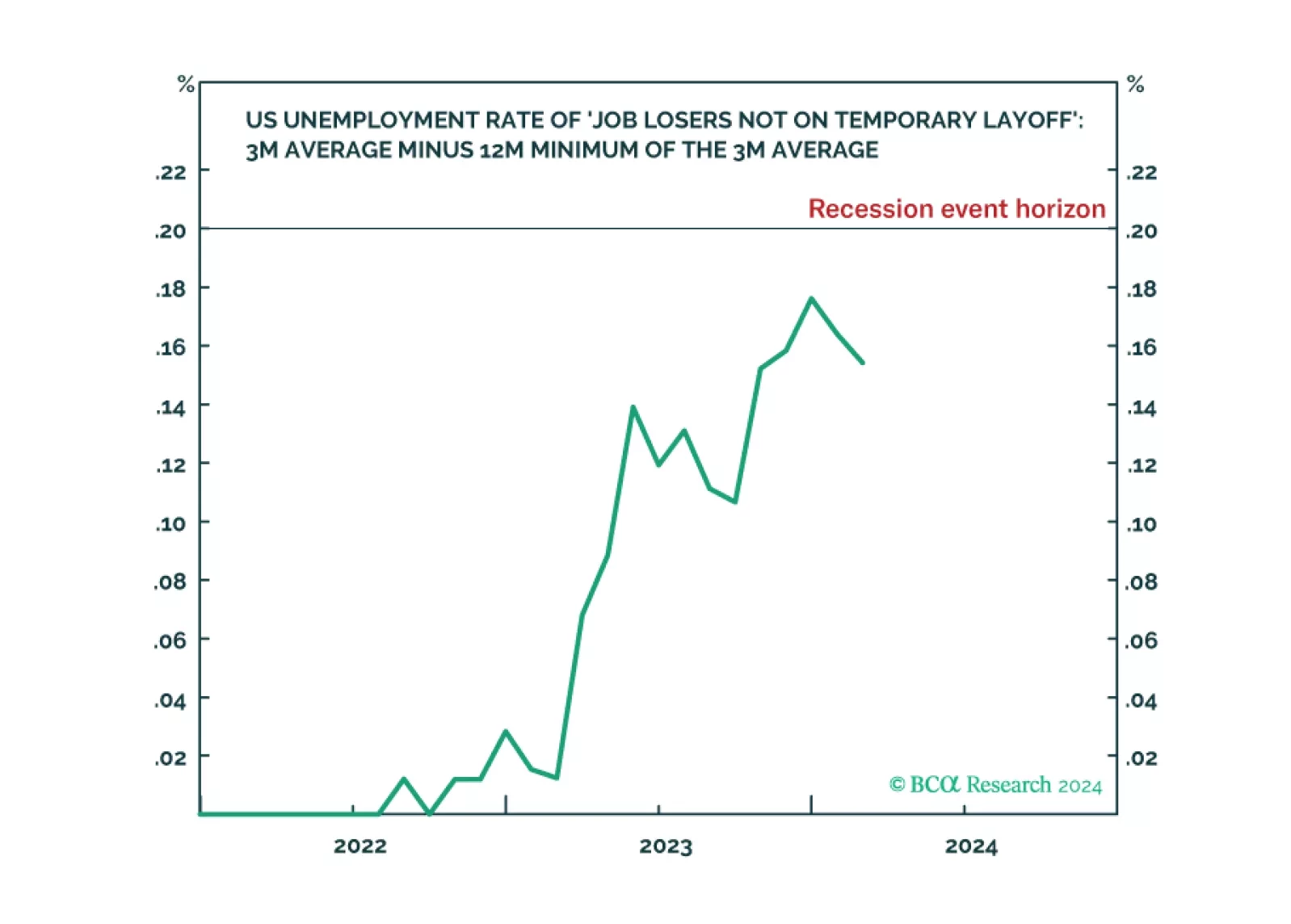

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

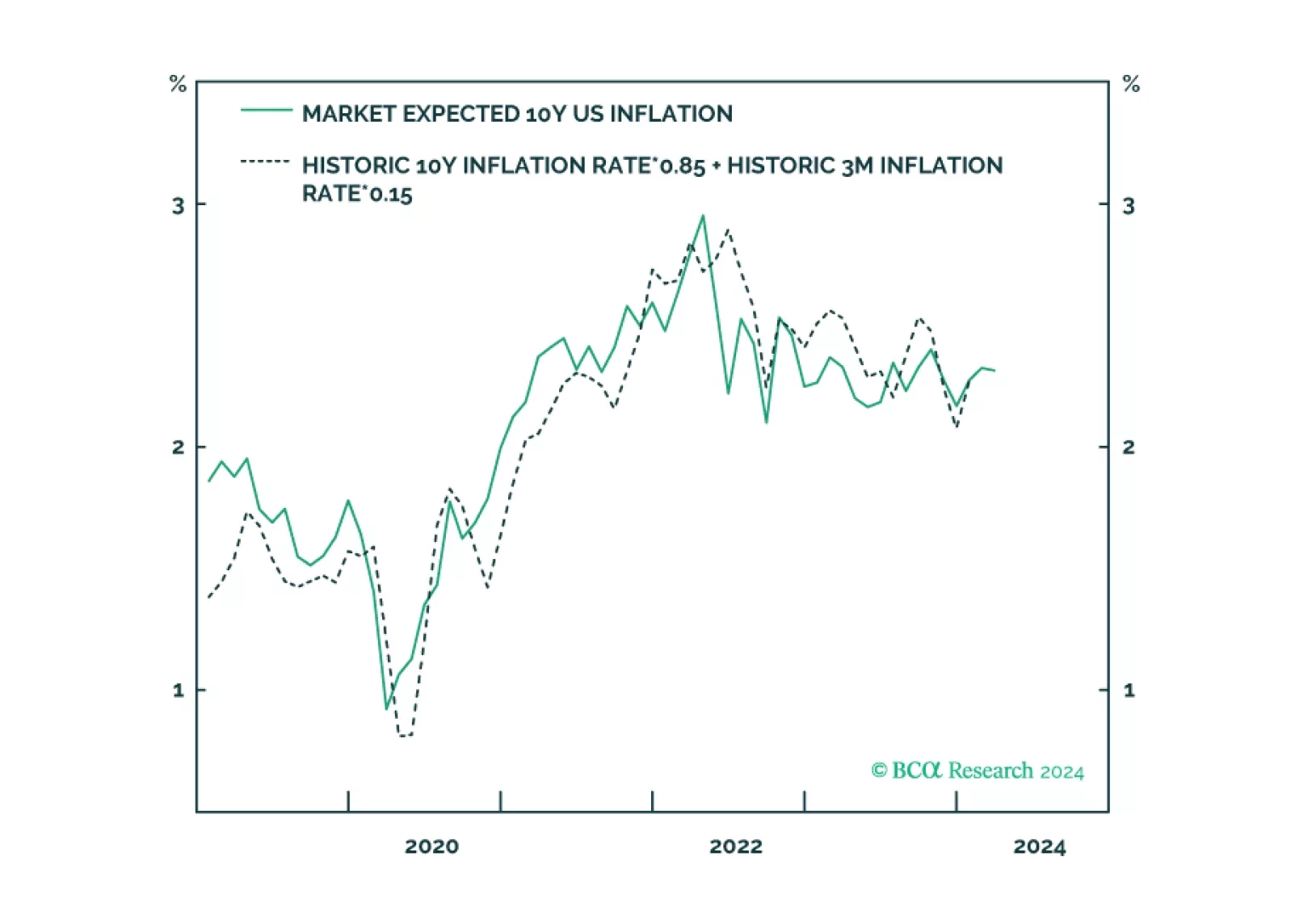

Expected inflation has surged to its highest level in a year. This has surprised many people, but expected inflation is behaving just as expected. Expected inflation is not a prophecy, it is just a mathematical function of delivered inflation. We discuss what this means for central banks in the US, UK, euro area, and Japan. Plus: bitcoin’s structural uptrend to $100,000+ is still intact.

The US ‘immaculate disinflation’ has run its course, given that labour force participation is topping out. This leaves the Fed with a dilemma. Settle for price inflation stabilising at 3 percent, and cut rates early to avoid higher unemployment. Or, not cut rates early and go the final mile to 2 percent price inflation, at the risk of higher unemployment. We discuss which way the Fed is likely to tilt, and the investment implications. Plus: China is oversold while Japan is overbought.

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.

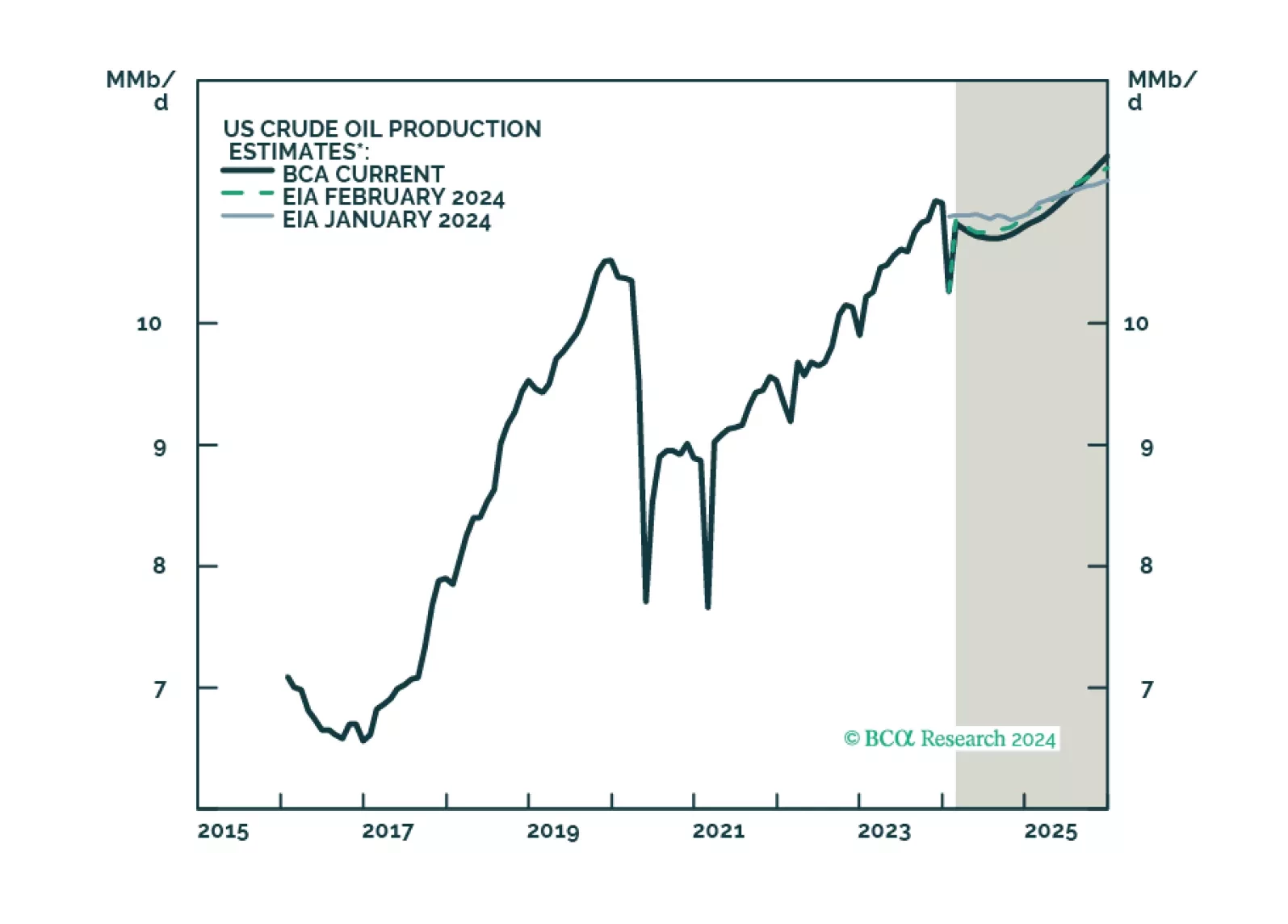

Energy markets are balanced in the short run, which keeps our Brent price forecasts at $95/bbl and $105/bbl in 2024 and 2025. Structurally, we see an upward bias to inflation, as geoeconomic fragmentation fundamentally alters supply chains; higher costs follow. Military access to oil will be prioritized. Renewables are the future, but war will be fought with hydrocarbons. We remain long the COMT, XOP and PPA ETFs.

The disinflation to date has been benign because it has come almost entirely from improving supply. But the supply-side tailwind has exhausted, so the last mile of the journey to 2 percent inflation will be the hardest, especially in the US and the UK. We discuss the investment implications. Plus, we highlight an interesting sector pair-trade.