Inflation

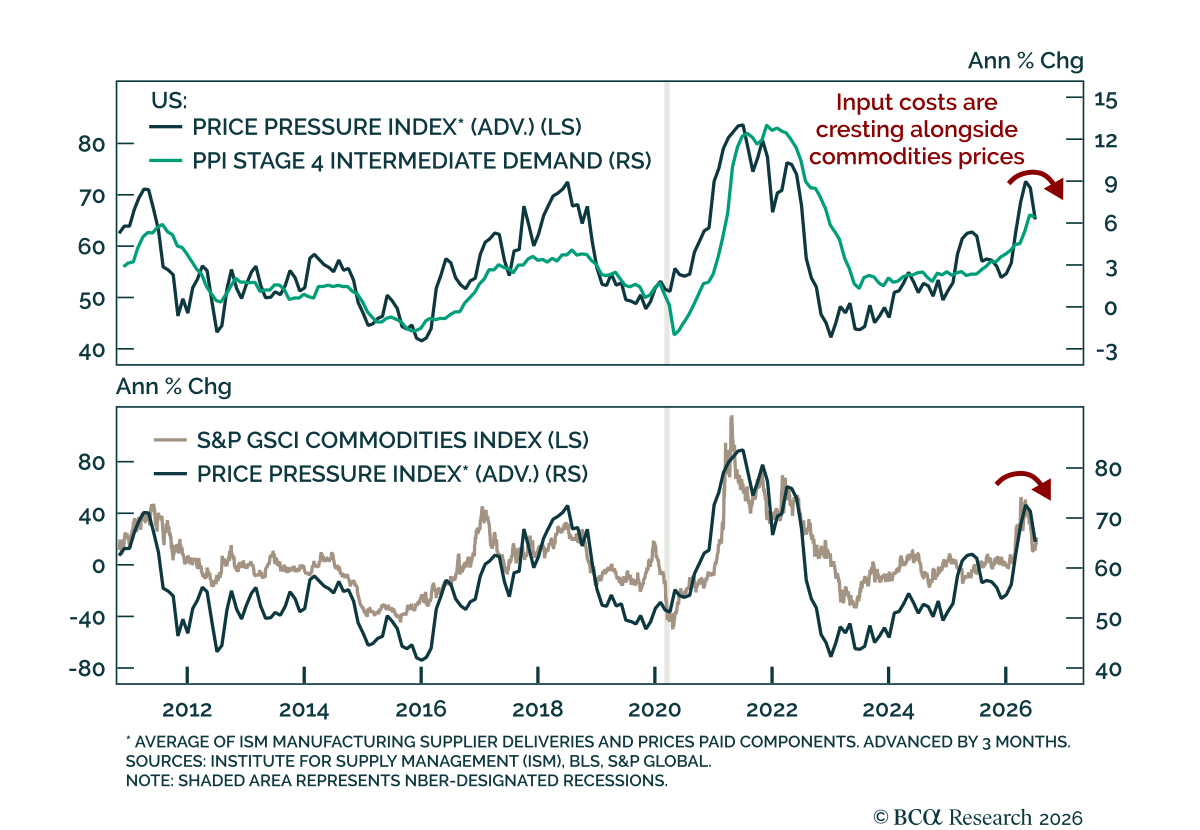

The June PPI report came in cooler than estimates, reinforcing the view that pipeline inflation pressures are easing and the Fed can stay on hold for now. Headline PPI contracted 0.3% m/m, lowering the annual rate to 5.5% y/y from 6.5%. The core measure,…

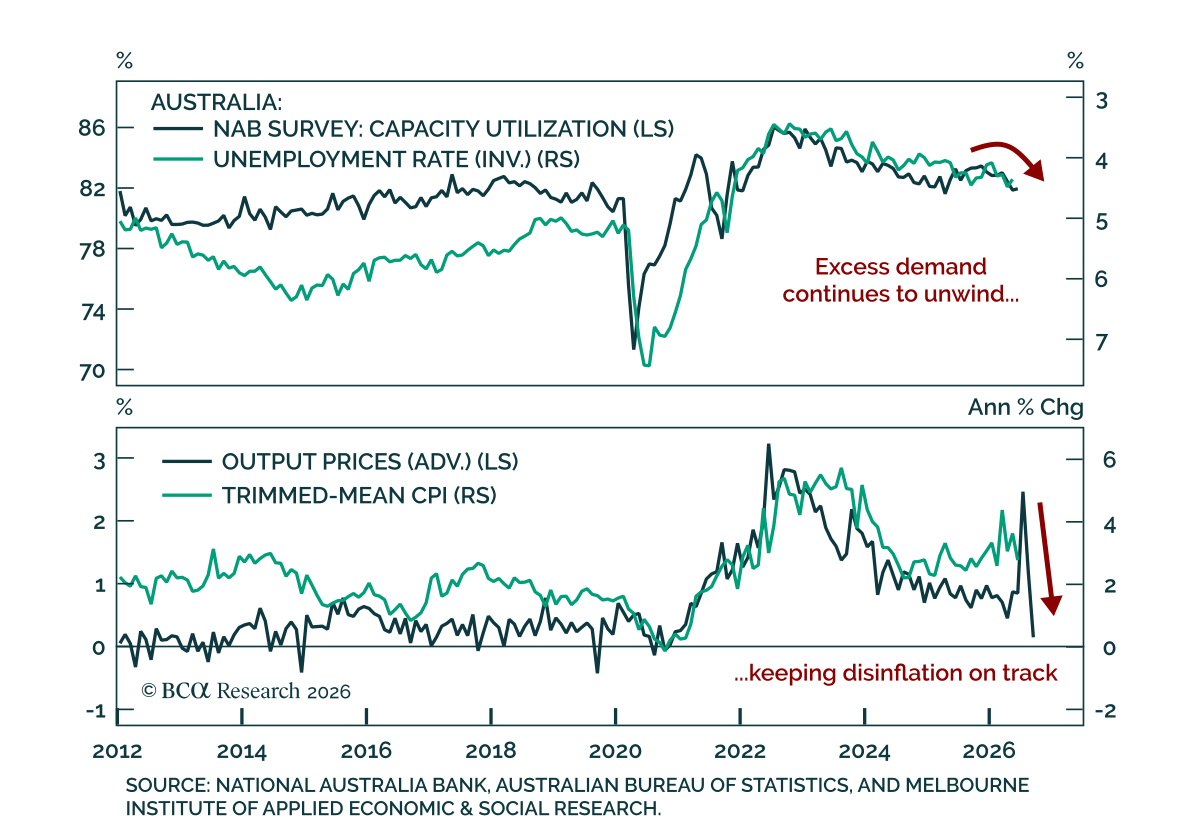

Australia's June NAB Business Survey points to a cooling economy, reinforcing the case for an extended RBA pause. Business conditions held at +3 for a third consecutive month, while business confidence, the more forward-looking measure, rebounded from -14 to…

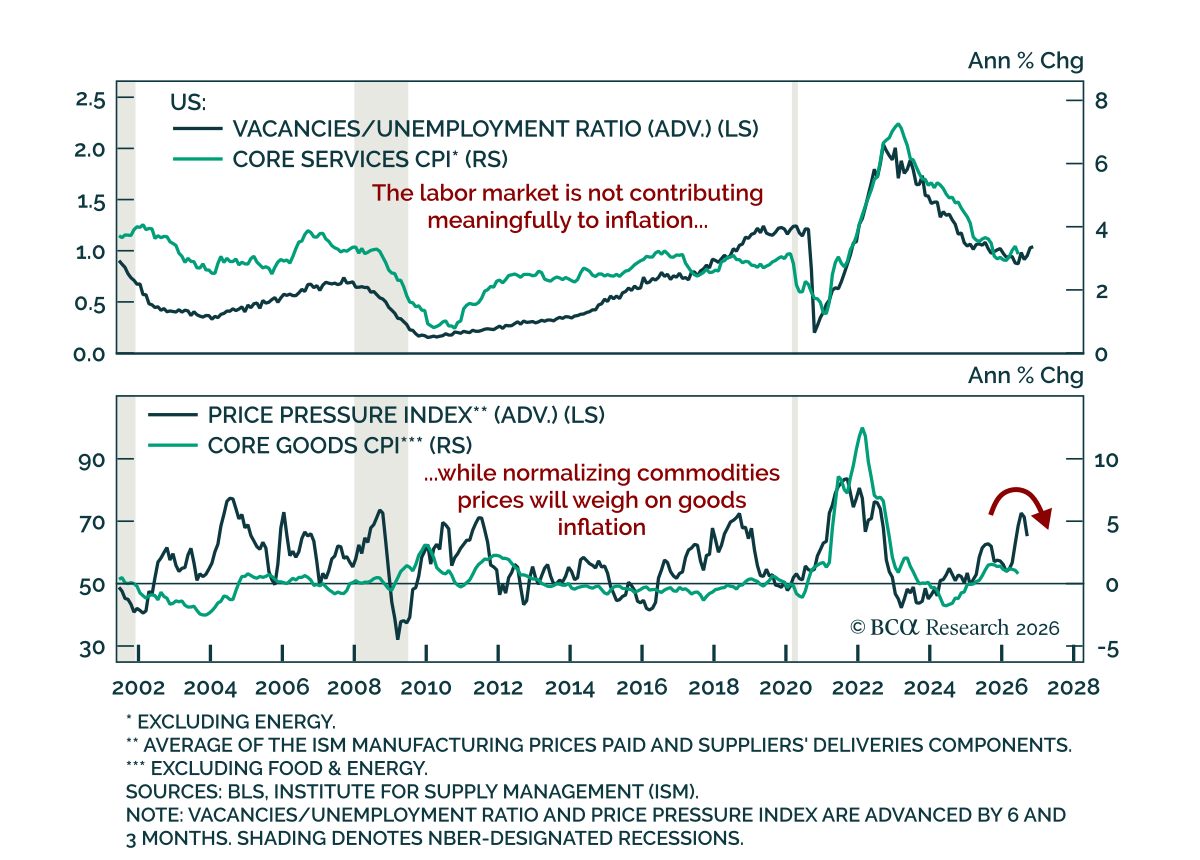

The June US CPI report was cooler than expected, reinforcing the case for the Fed to stay on hold in July. Headline CPI contracted 0.4% m/m, the first monthly decline since June 2024 and the most severe since April 2020, cooling the annual rate to 3.5% y/y…

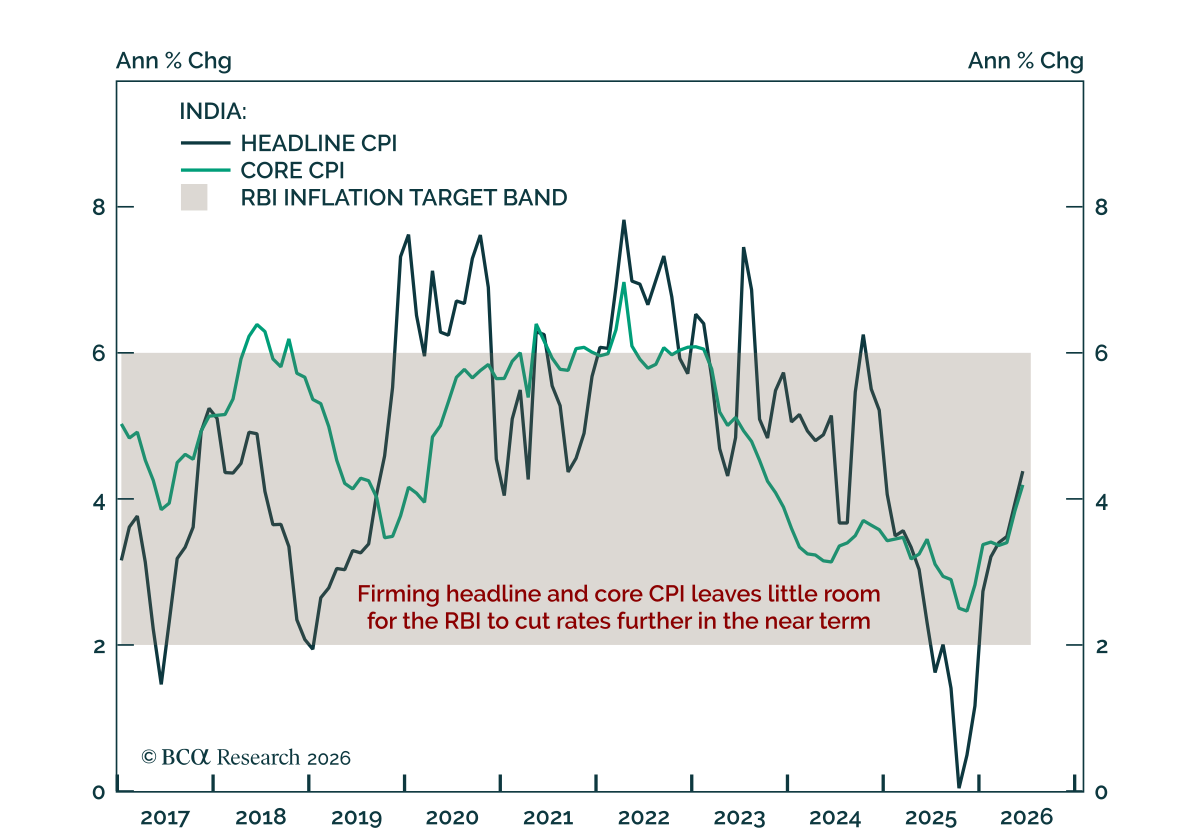

Indian headline CPI rose to 4.4%, limiting the RBI’s scope to ease and creating a less supportive backdrop for Indian assets. The increase pushed inflation above the RBI’s 4% target, though it remains within the tolerance band. Higher fuel and food prices…

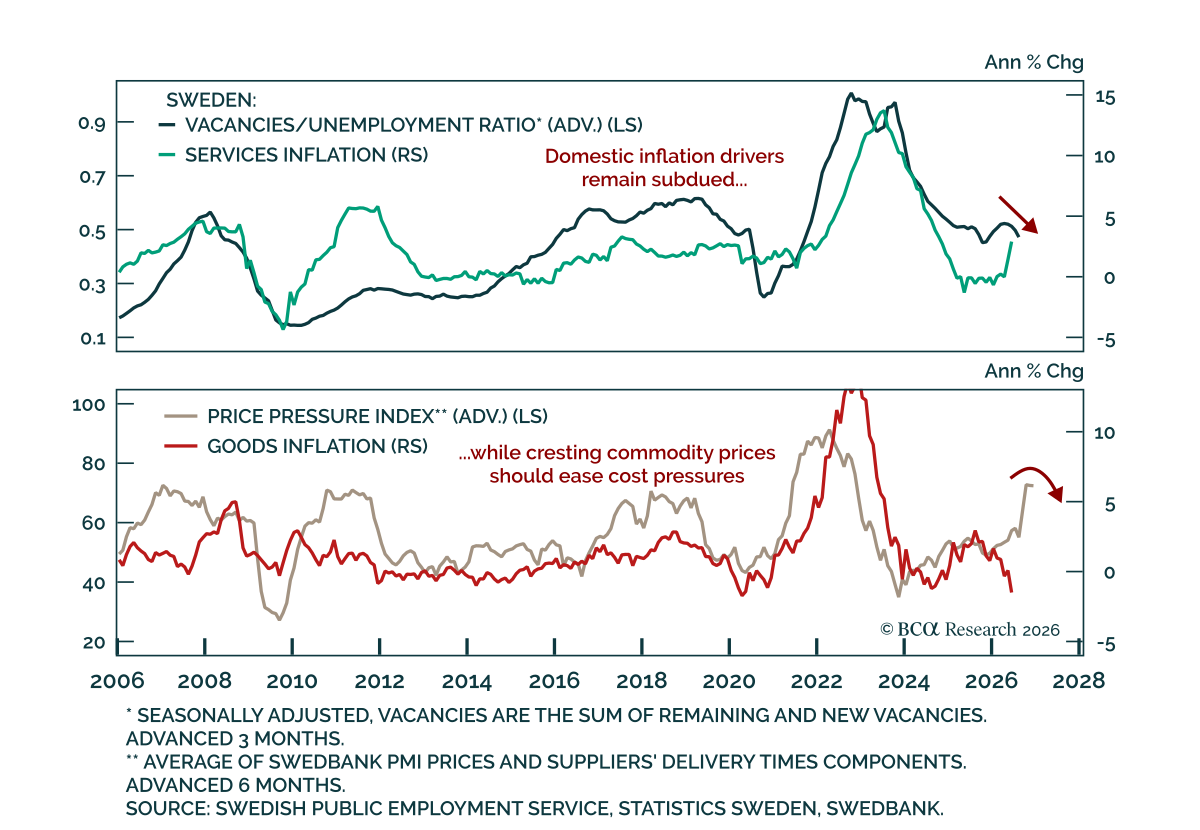

Subdued Swedish inflation should keep the Riksbank on hold. June headline CPIF eased to 1.3% y/y (0.3% m/m) from 1.5% (0.9%), and CPIF excluding energy slowed to 0.4% y/y (0.6% m/m) from 0.5% (0.7%). Both were marginally above estimates, but disinflation has…

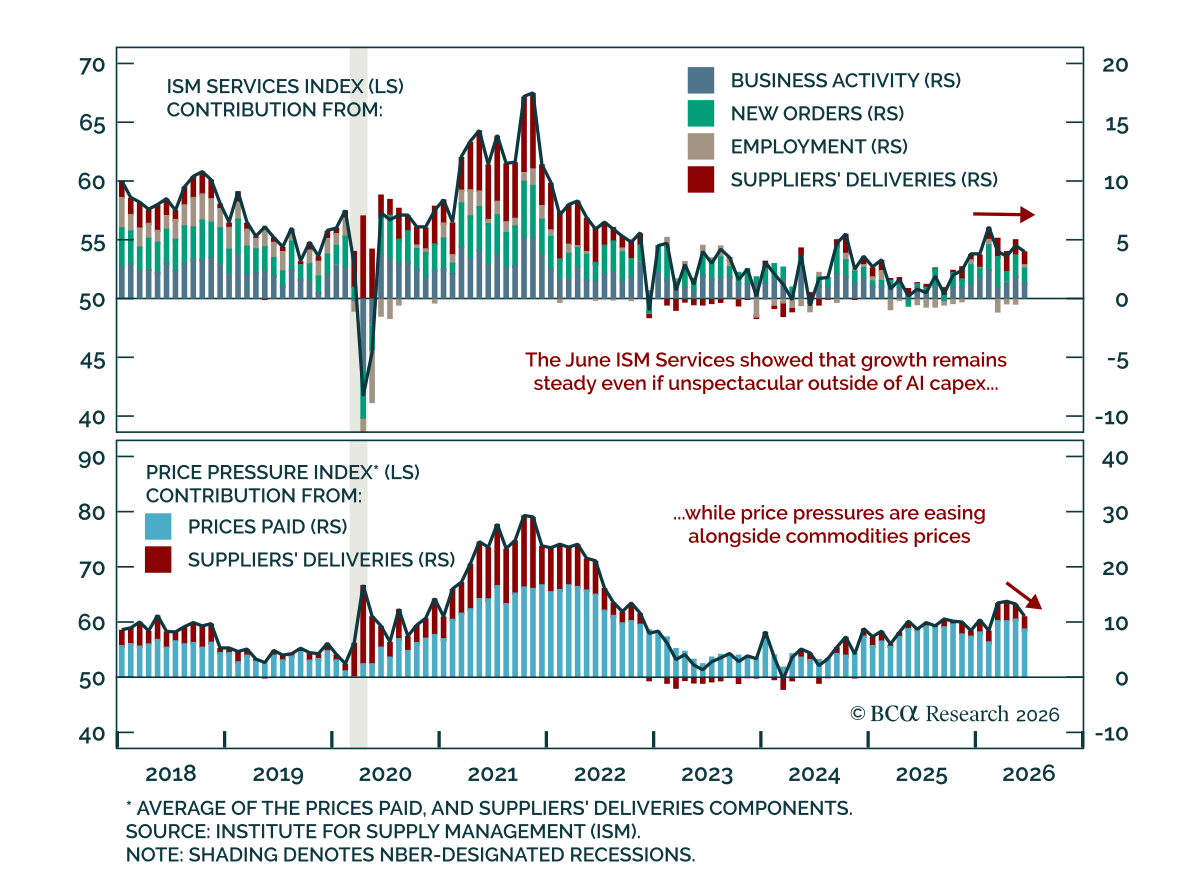

The June ISM Services survey was in line with consensus and reinforced the picture of a US economy that is neither overheating nor cooling significantly. The headline index ticked down to 54.0 from 54.5. The underlying picture was somewhat mixed, with new…

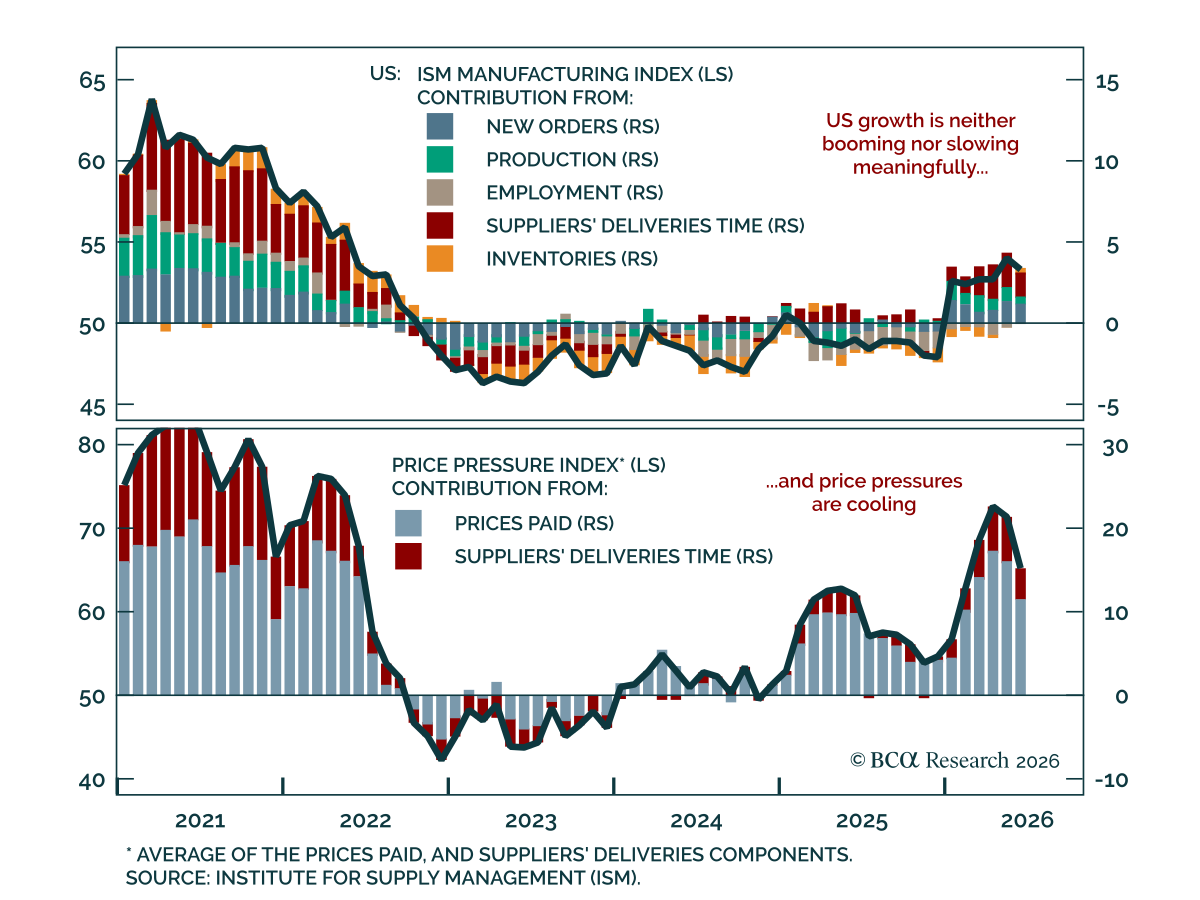

The June ISM Manufacturing index came in below estimates, but the broader US growth backdrop remains in a sweet spot. The headline index ticked down to 53.3 from 54.0. The slowdown was broad, with new orders easing to 56.0 from 56.8. Employment, however,…

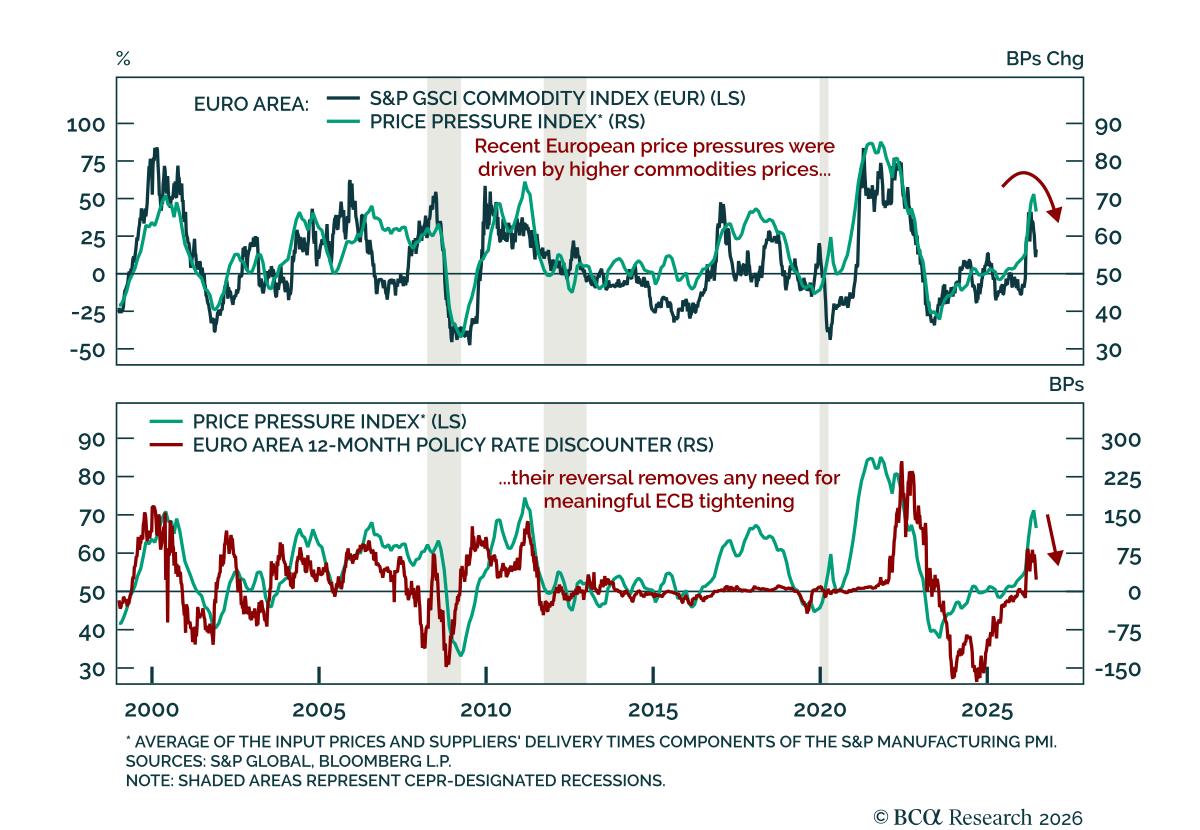

June inflation prints came in softer than expected across most major eurozone economies, reinforcing the case against further ECB tightening. Inflation undershot consensus in Germany, France, and Italy, while Spain was slightly above forecast but unchanged;…

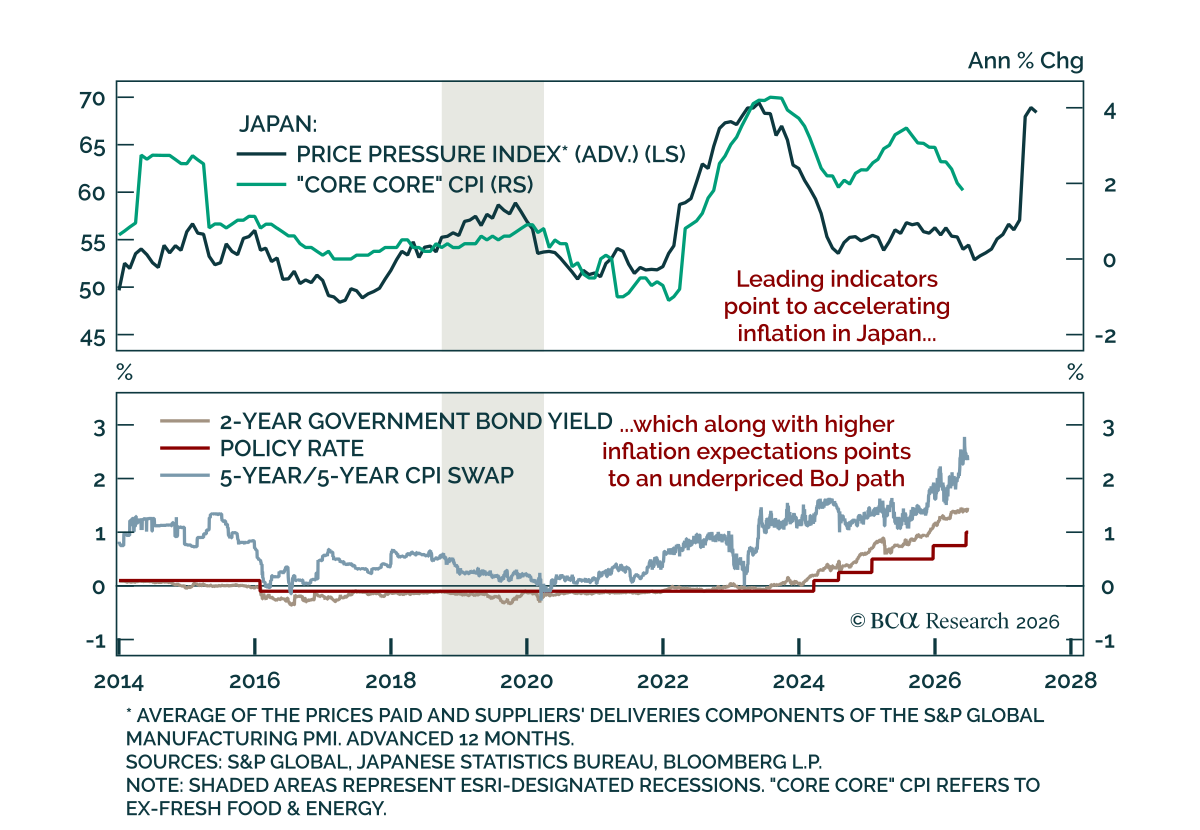

The June Tokyo CPI came in hotter than consensus, pointing to rising price pressures and further policy tightening. The headline index rose to 1.7% y/y from 1.4%. Core measures were also hot, with CPI ex-fresh food rising to 1.6% from 1.3%, and “core core”…

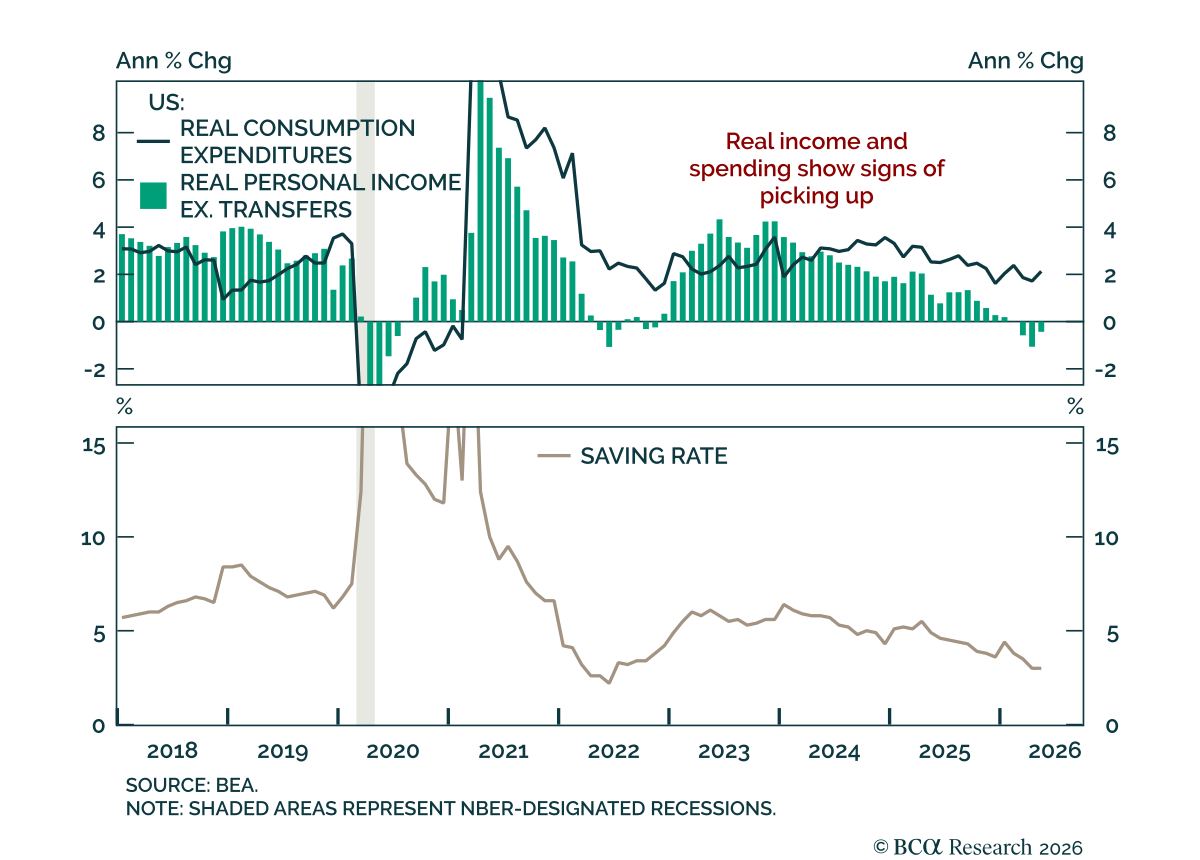

The May Personal Income and Outlays report beat estimates, showing firmer consumer momentum but still-sticky inflation. Both nominal and real spending beat estimates, rising 0.7% m/m and 0.3%, respectively. Personal income was also strong at 0.7%, while real…