Inflation/Deflation

Commentators often use notions like debt deflation, balance sheet recession, and liquidity trap interchangeably. Yet, these are different concepts. This report develops a framework and provides a diagnosis of China’s economic malaise. A follow-up report will deal with what kind of treatment is needed for a recovery. As a trade, we recommend shorting the EM equity index.

In this special report, we discuss whether the economic conditions necessary for a stronger yen (and higher JGB yields) will materialize over the next 12-to-18 months.

Inspired by a client’s questions, we examine the rationale behind the implementation of the trailing stop governing our near-term asset allocation recommendations.

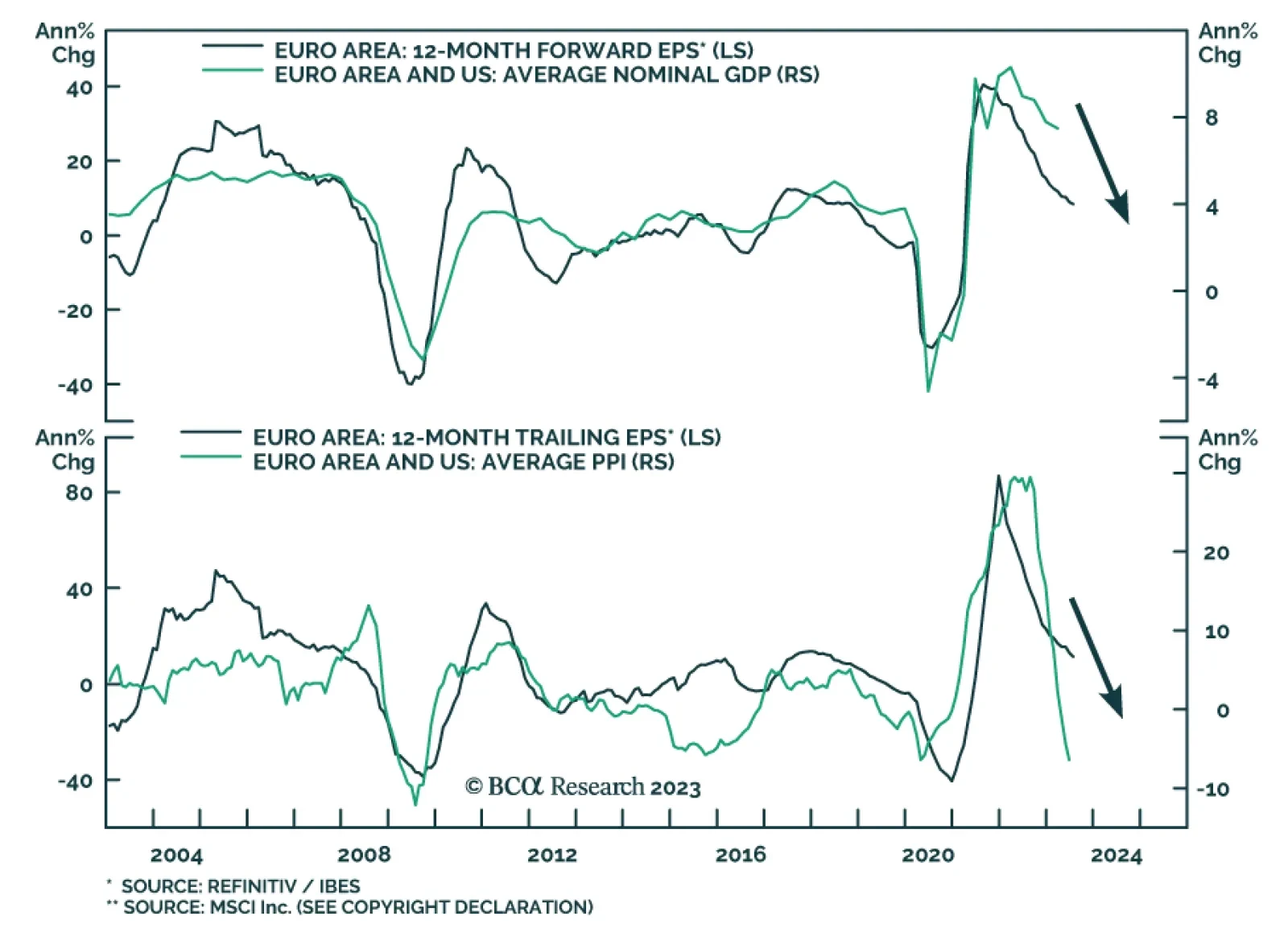

European real GDP growth is stabilizing, so why would European equities continue to trade sideways for the remainder of the year? The answer lies with nominal growth and its impact on earnings.