Inflation/Deflation

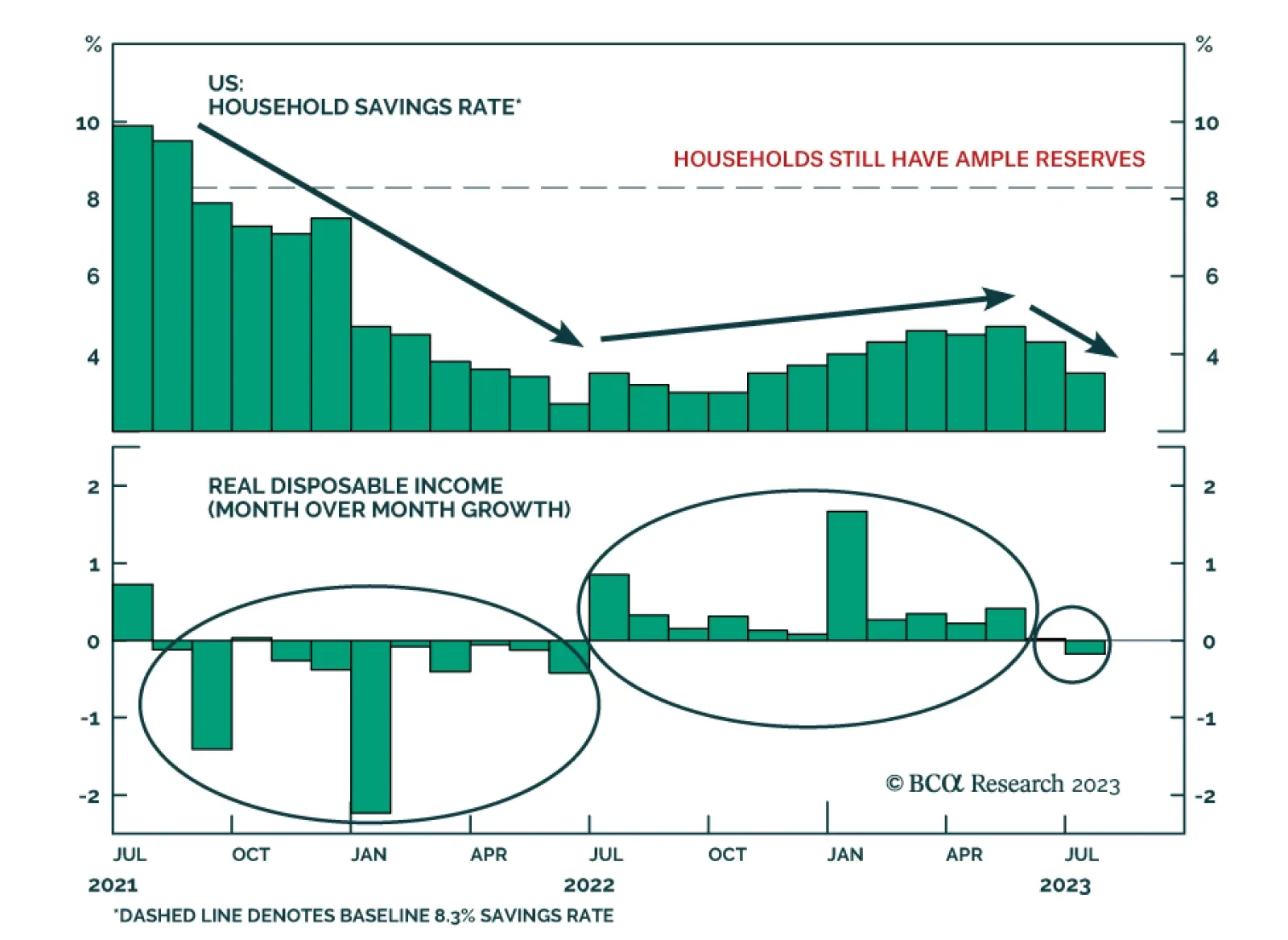

Our colleagues at BCA’s US Investment Strategy service have been excess savings bulls since cash began silting up on household balance sheets as transfer payments flowed from the Capitol to Main Street while High Street businesses were shuttered. Excess…

Stocks perform worse in presidential election years than average years, especially in the first half of the year, and especially if the ruling party ends up falling from power. Investors should take risk off the table until the unemployment rate peaks.

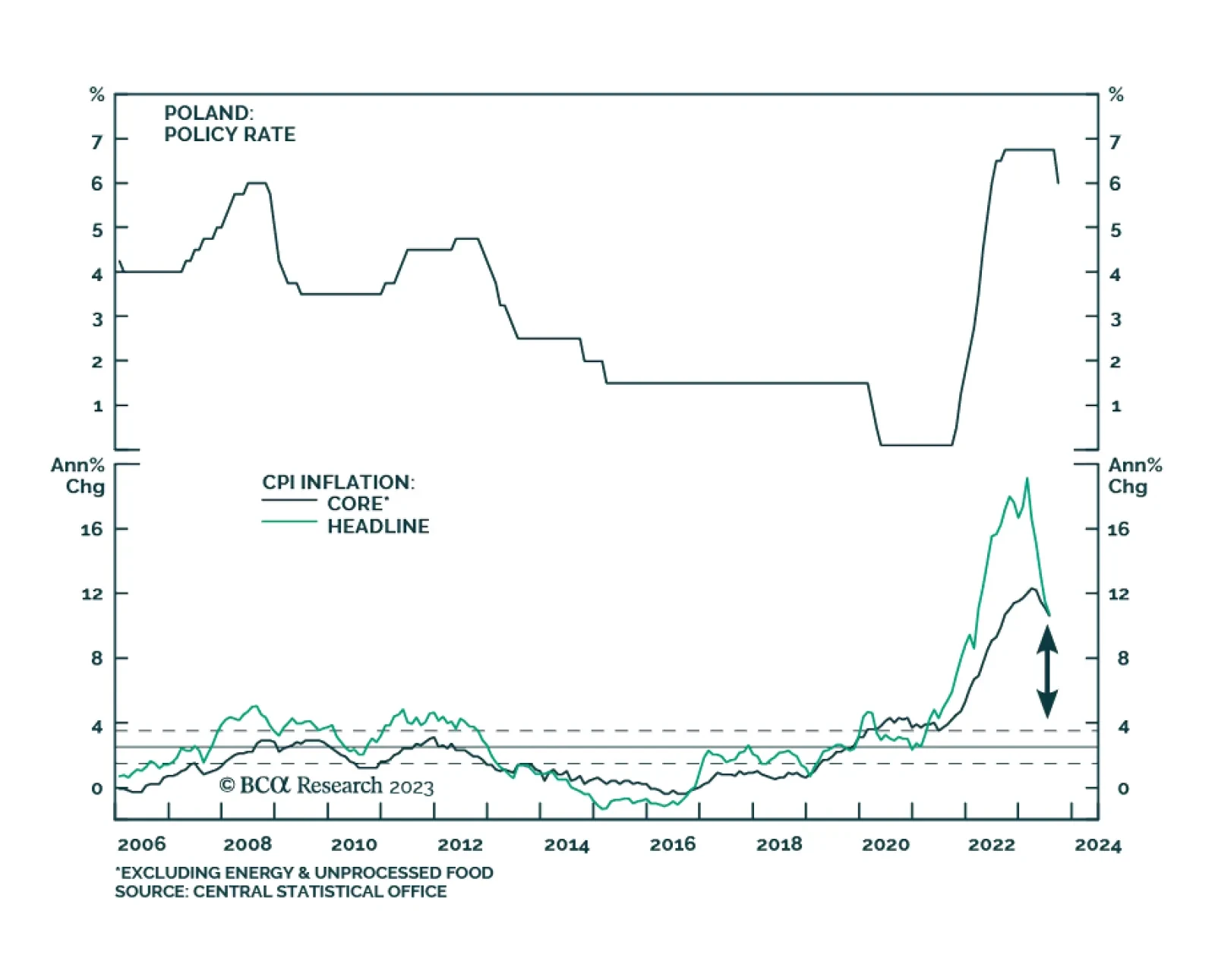

The Polish central bank delivered a larger-than-anticipated 75 basis point rate cut on Wednesday – slashing the policy rate to 6%, versus expectations of 6.5%. The aggressive move marks the first rate cut following a 11-month-long pause after the NBP lifted…

Carbon credits as an asset class are becoming increasingly investable. Given that the structural bull case for this asset class is compelling, strategic investors should long carbon credits. However tactical investors should book profits or consider merits of a short position, since prices are likely to correct over the next 12-24 months.

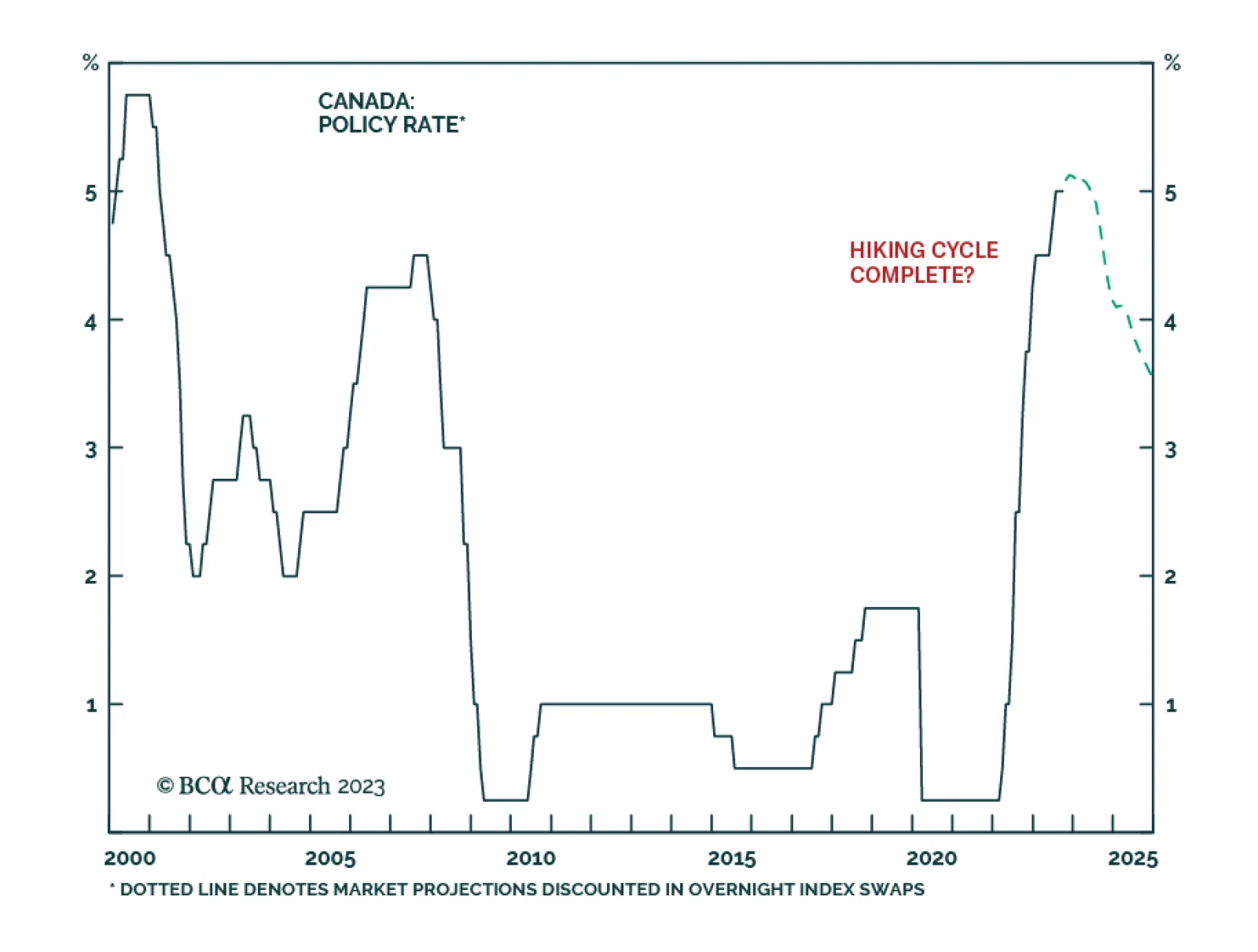

As expected, the Bank of Canada kept its policy rate unchanged at 5% on Wednesday. In particular, the central bank highlighted that domestic economic growth deteriorated. Indeed, last week’s GDP release showed the Canadian economy unexpectedly contracted…

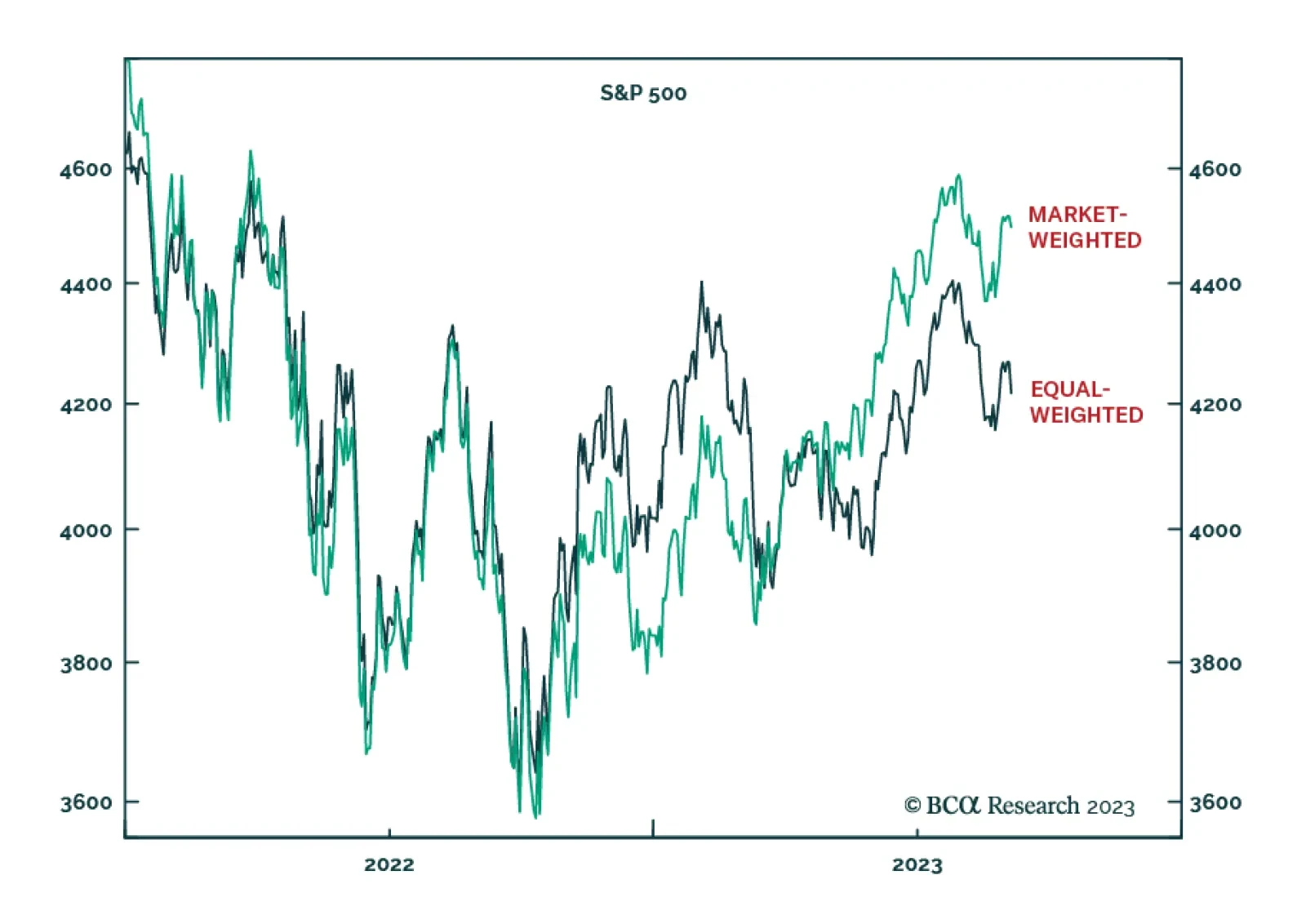

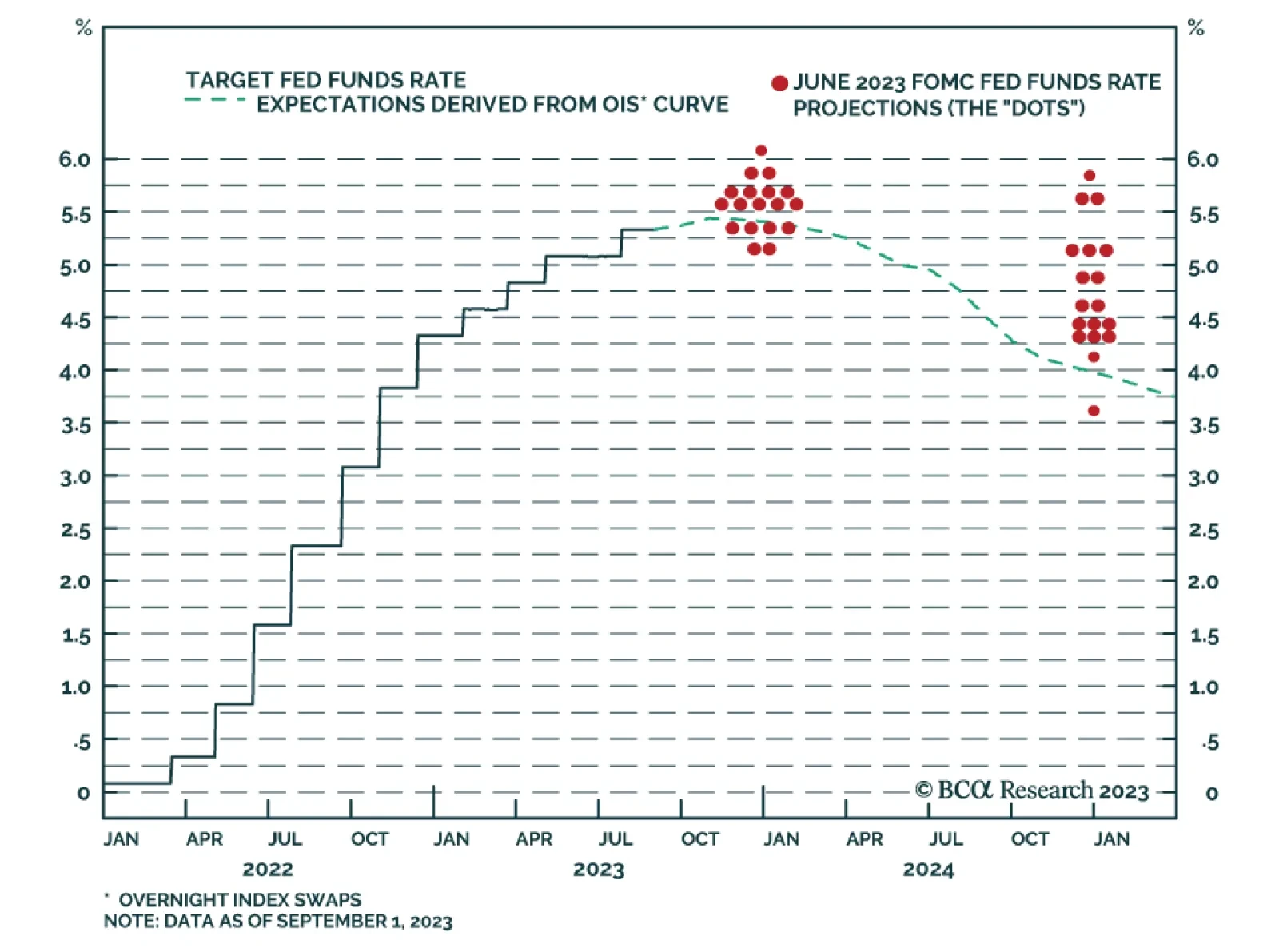

According to BCA Research’s Counterpoint service, Goldilocks is just a fairy tale. In the near-term, this will be negative for stocks, neutral for bonds, and positive for the dollar. The Fed can win the war against inflation, but not without much higher…

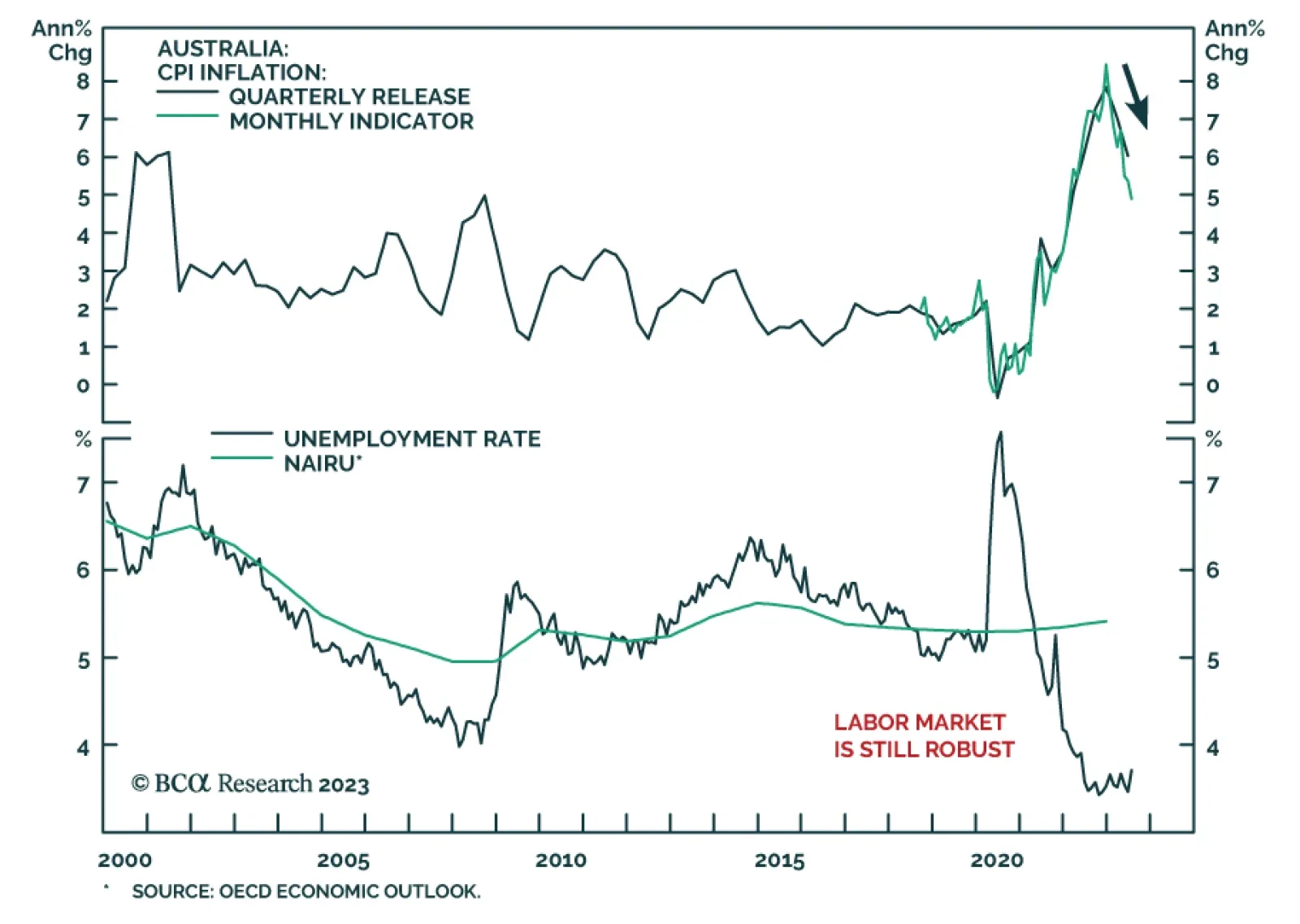

The AUD was the worst performing currency on Tuesday after the Reserve Bank of Australia kept its cash rate target unchanged at 4.1% for the third consecutive month. In particular, outgoing Governor Philip Lowe underscored that the uncertain economic outlook…

In a Tuesday morning television interview, Fed Governor Christopher Waller signaled that the Fed will not lift rates when it meets later this month. Specifically, Waller echoed language used by Chair Powell at the Jackson Hole conference by saying that recent…

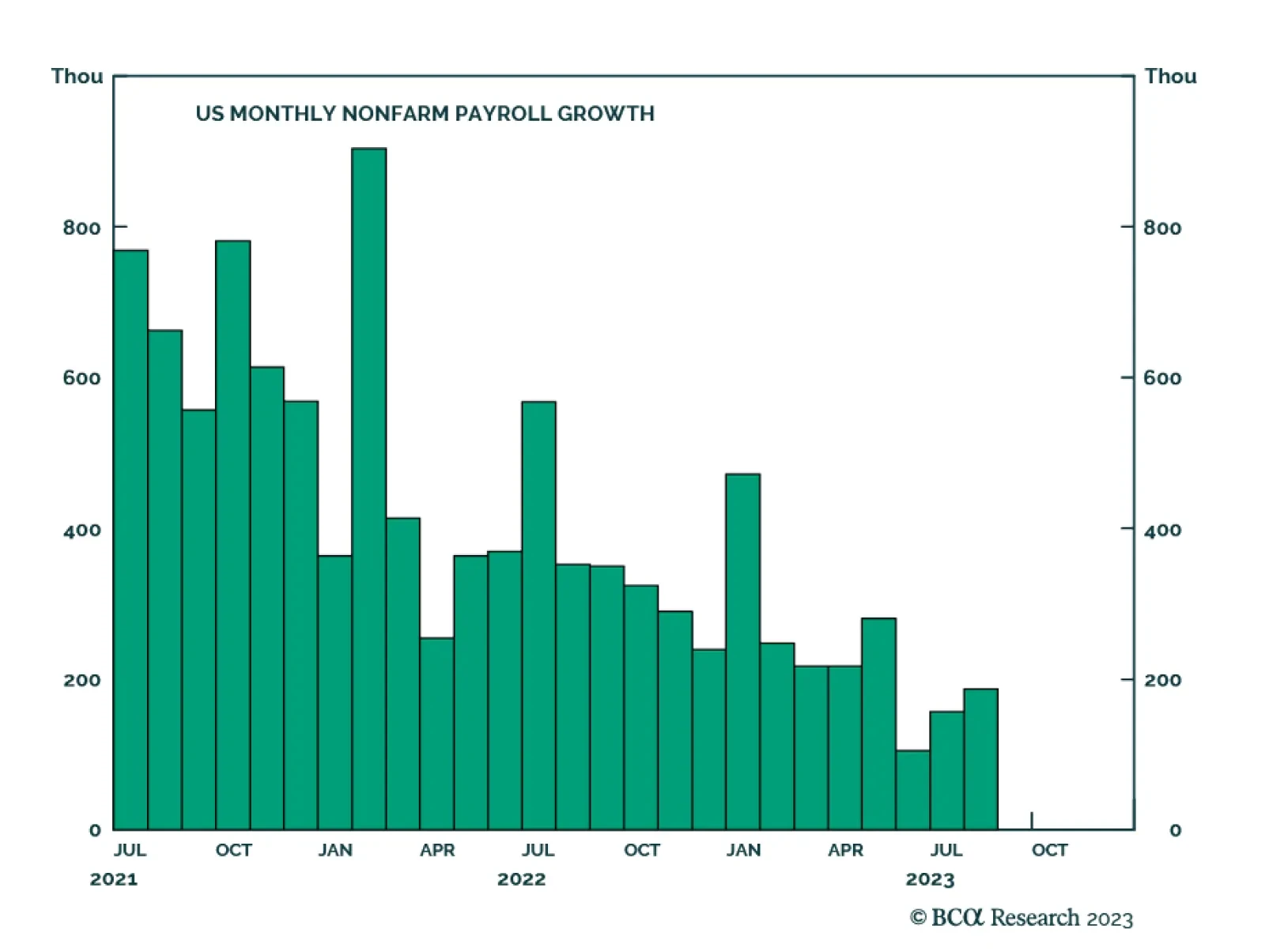

Friday’s US employment report suggests that the softening of the labor market is continuing at a steady pace. Although nonfarm payroll employment in June and July was revised down by 110 thousand, the 187 thousand increase in August came in above expectations…

US bond investment takeaways from this week’s PCE and employment releases.