Inflation/Deflation

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

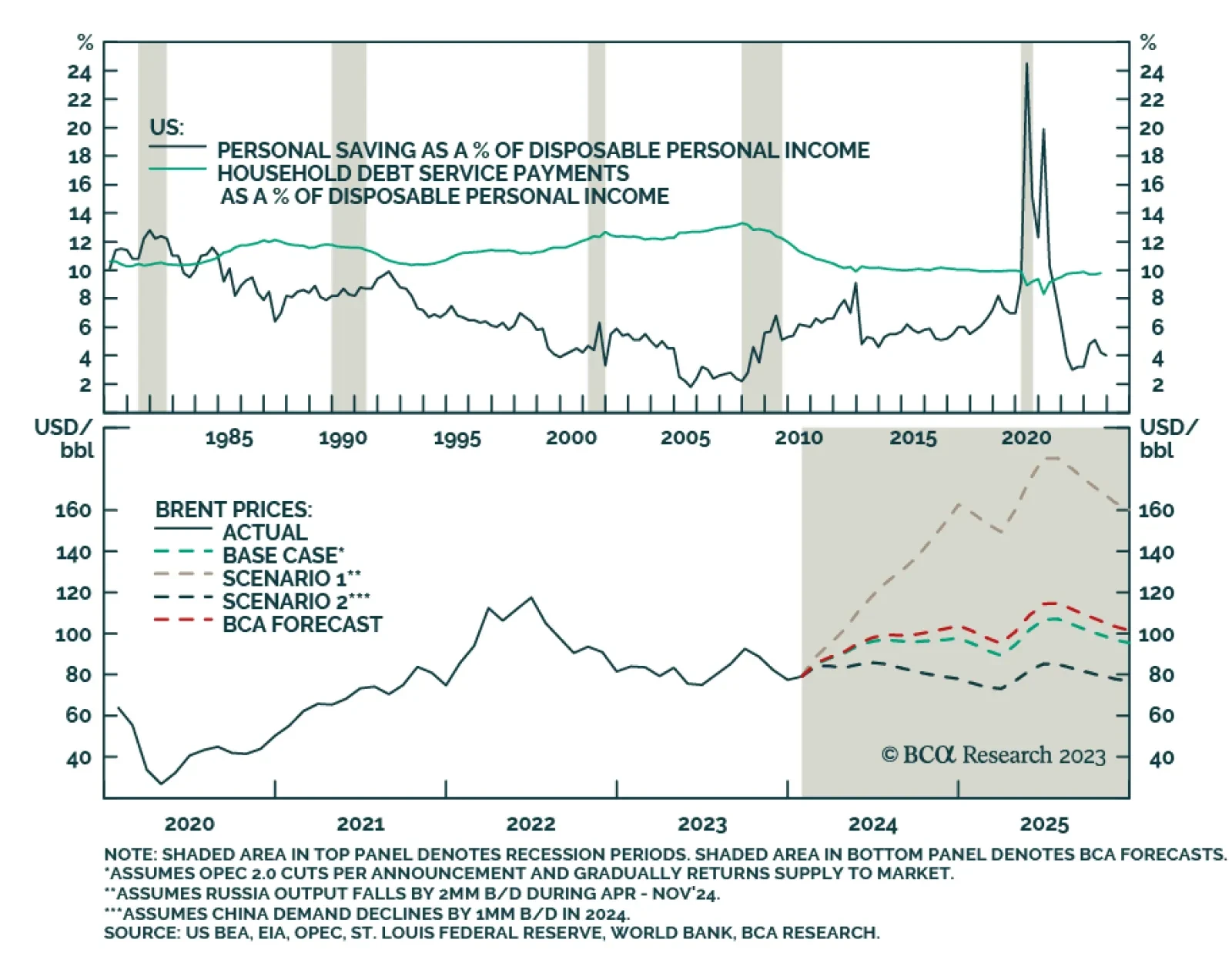

Our Commodity & Energy colleagues see oil markets balanced in the short run, which keeps their Brent price forecasts at $95/bbl and $105/bbl for 2024 and 2025. That said, they note the odds are increasing demand growth could surprise to the…

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.

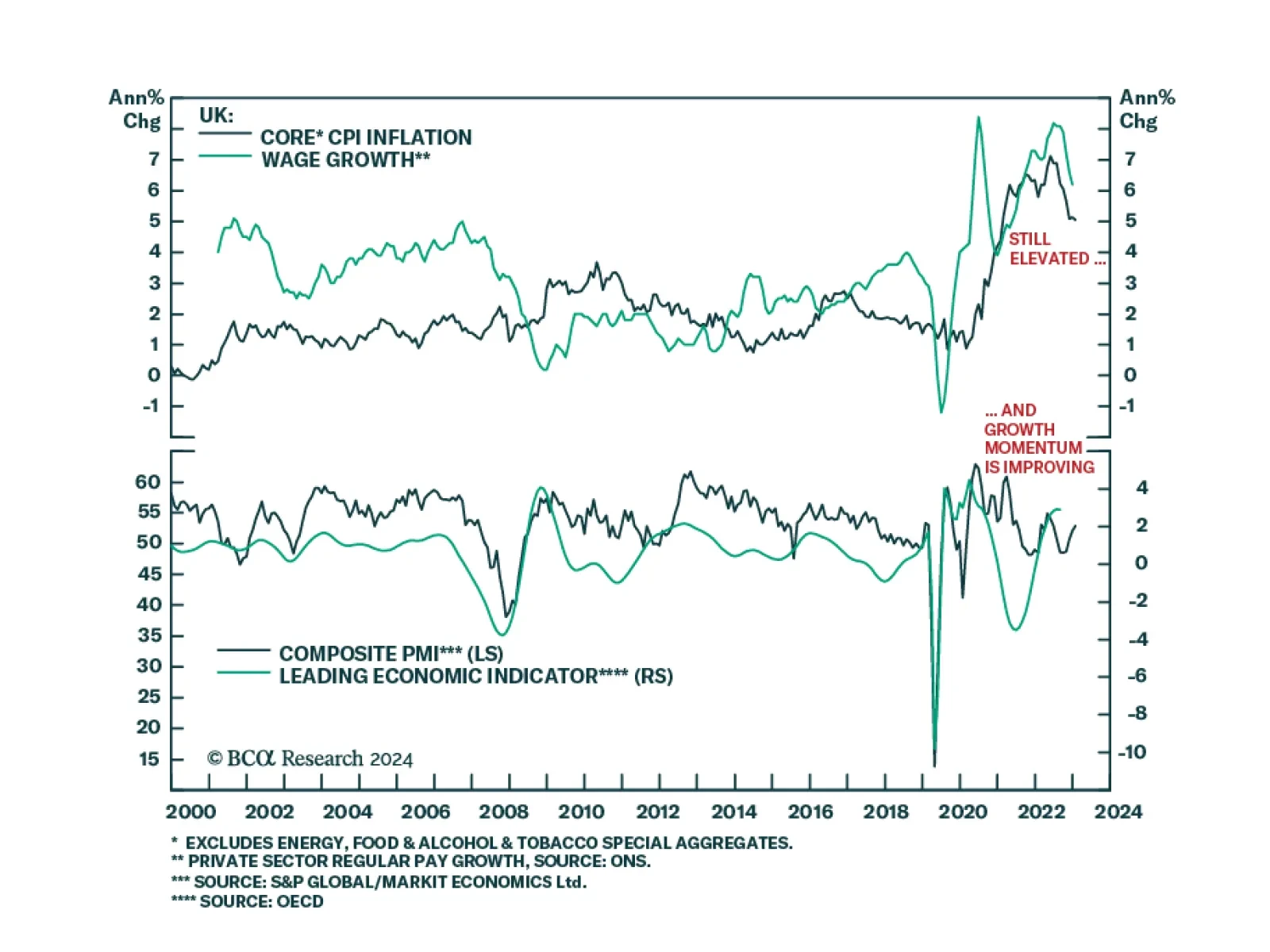

The UK inflation release for January came in slightly softer than anticipated. Both headline and core CPI were unchanged on year-over-year basis at 4.0% and 5.1%, respectively – below expectations of slight accelerations. The 0.6% m/m decline in the headline…

Prices of agricultural commodities have come under intensified downward pressure this year. Corn, soybean, and wheat prices have fallen by 8.6%, 8.3%, and 4.9% respectively so far this year. Multiple factors are behind the selloff. First, ag prices…

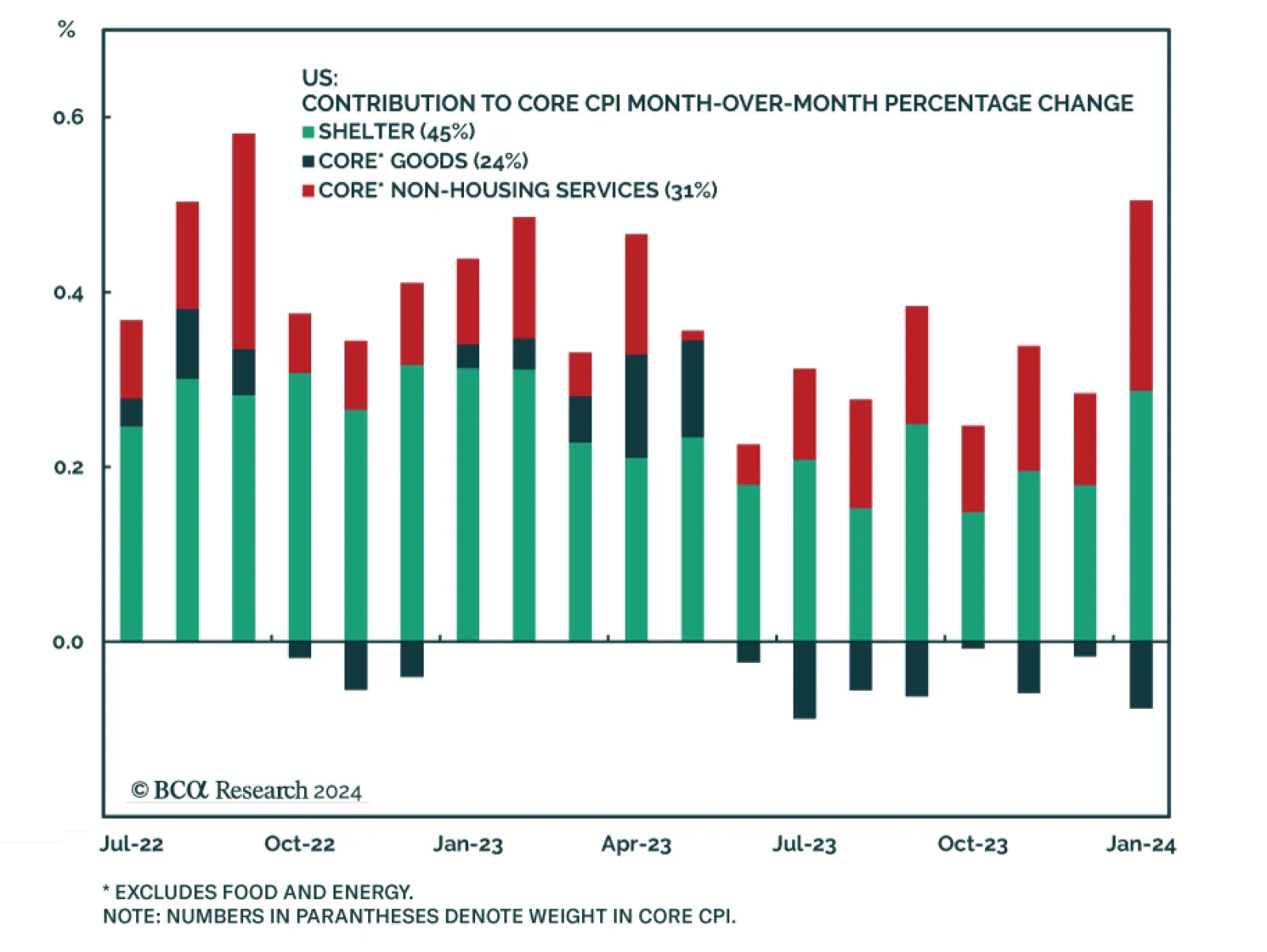

Comments on yesterday’s CPI report and yield moves.

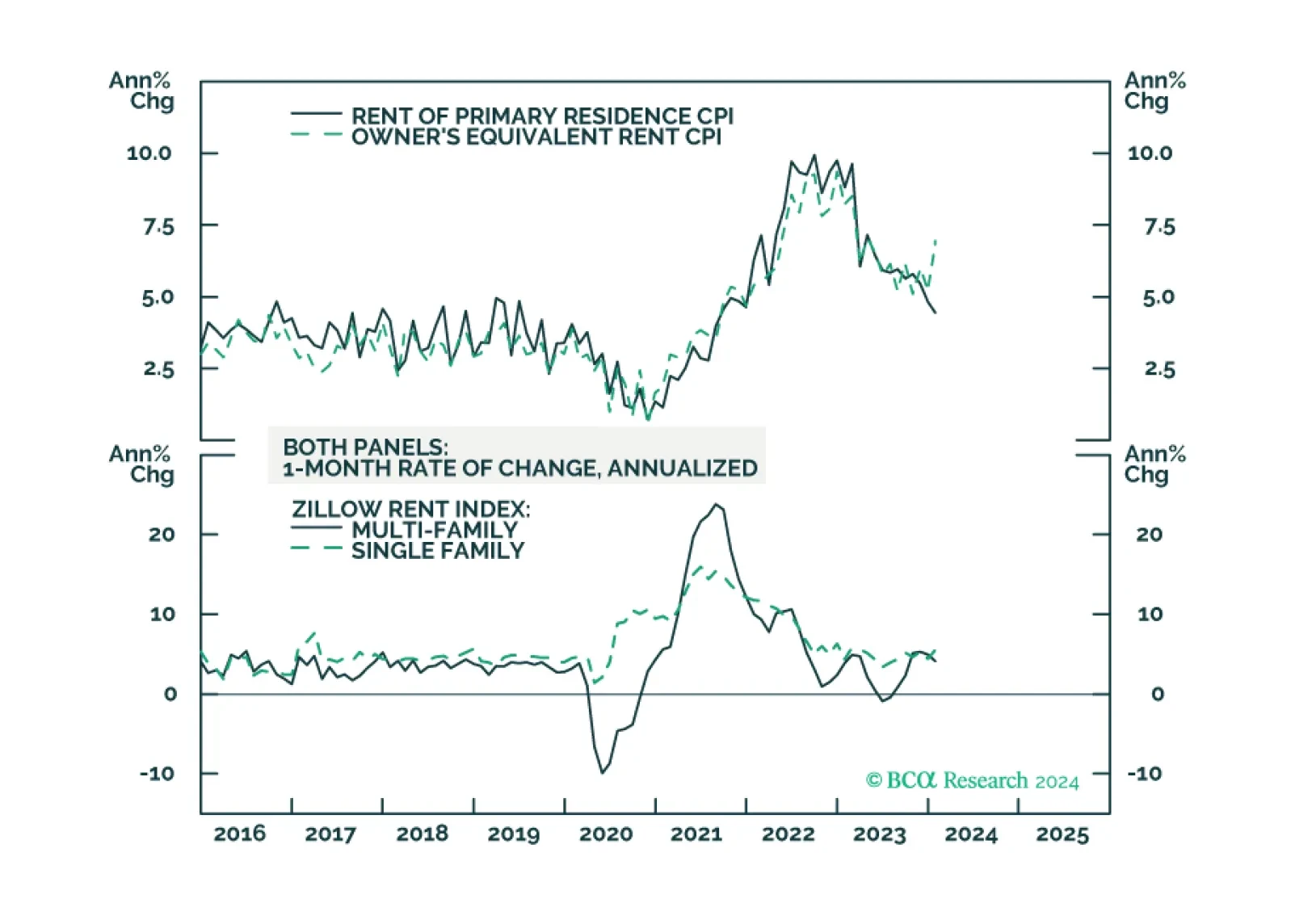

The US CPI report for January showed inflation did not cool as much as anticipated. Headline inflation accelerated from 0.23% to 0.31% on a month-over-month basis, higher than anticipations of 0.2% m/m. It fell from 3.4% to 3.1% on a year-over-year basis,…

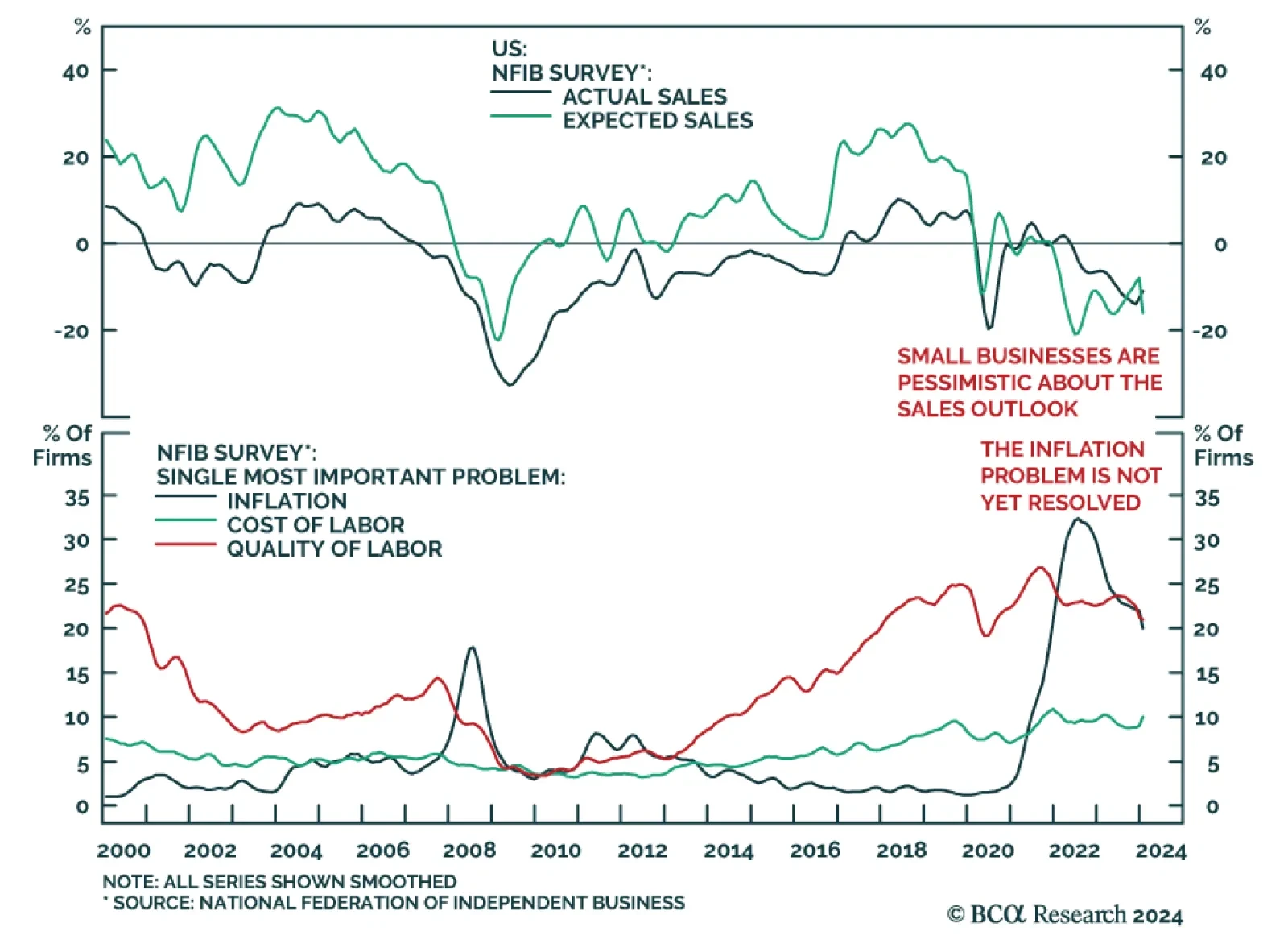

We highlighted in a recent Insight that positive economic surprises are prompting economists to revise up their US economic growth expectations. The Goldilocks narrative is supporting the rally in risk assets. However, results of the January NFIB survey…

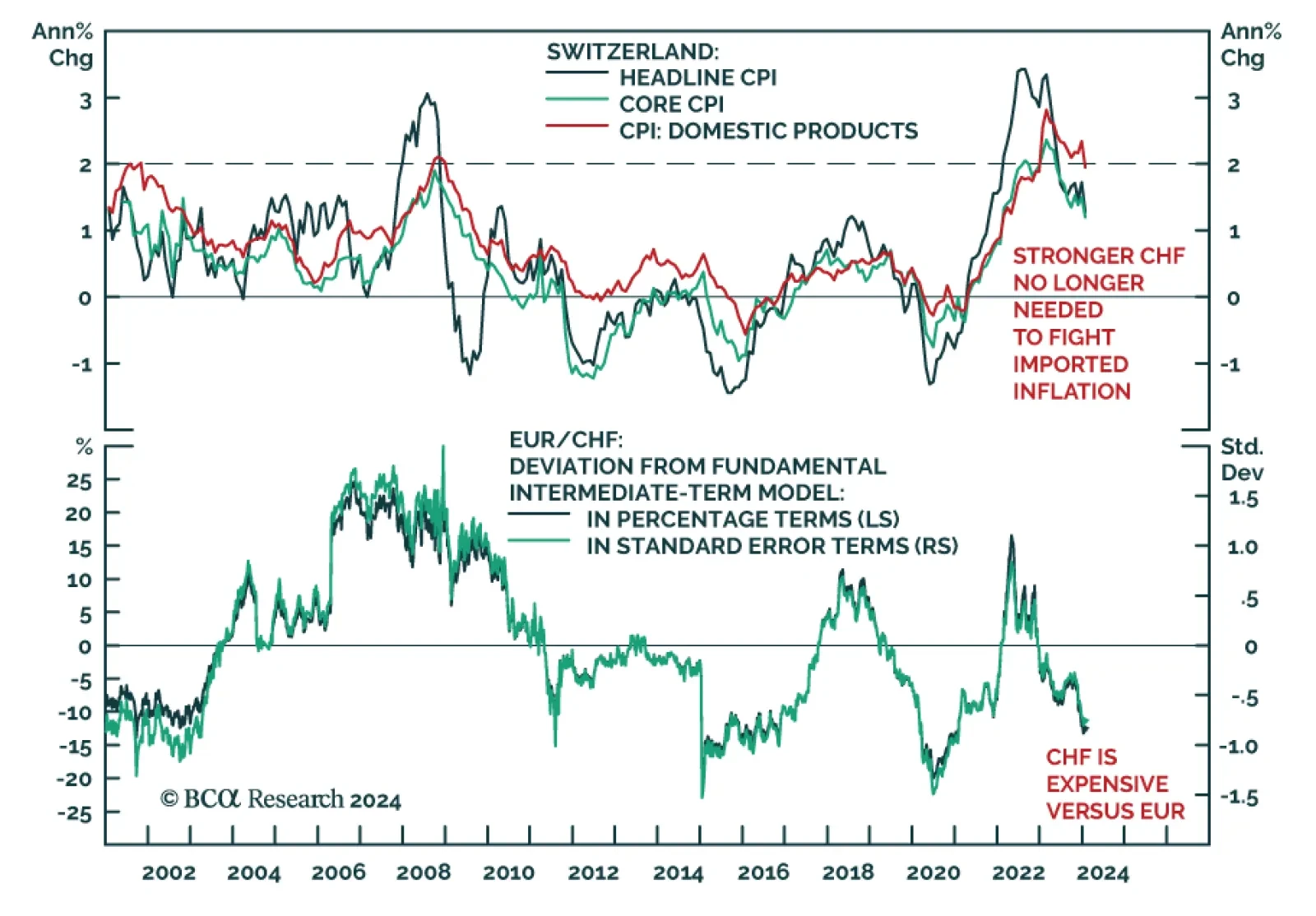

The Swiss franc is among the worst performing major currencies so far this year. This marks a reversal following its stellar performance last year. The Swiss National Bank’s (SNB) support for the domestic currency is behind last year’s strength.…

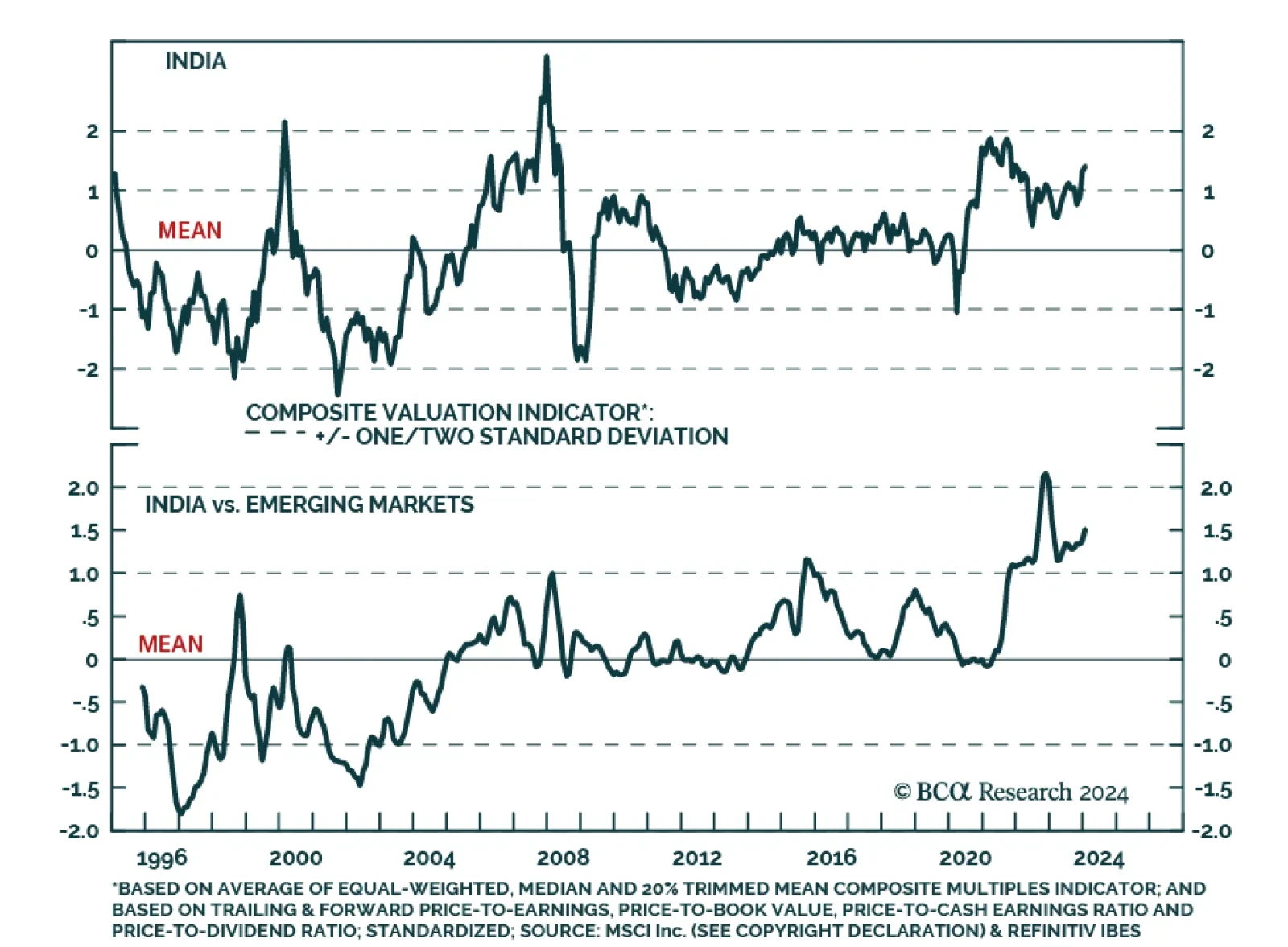

Indian economic data releases delivered a positive signal on Monday. CPI inflation slowed from 5.7% y/y to 5.1% y/y in January – within the Reserve Bank of India’s (RBI) 2-6% target range. Meanwhile, industrial production growth accelerated from 2.4% y/y to…