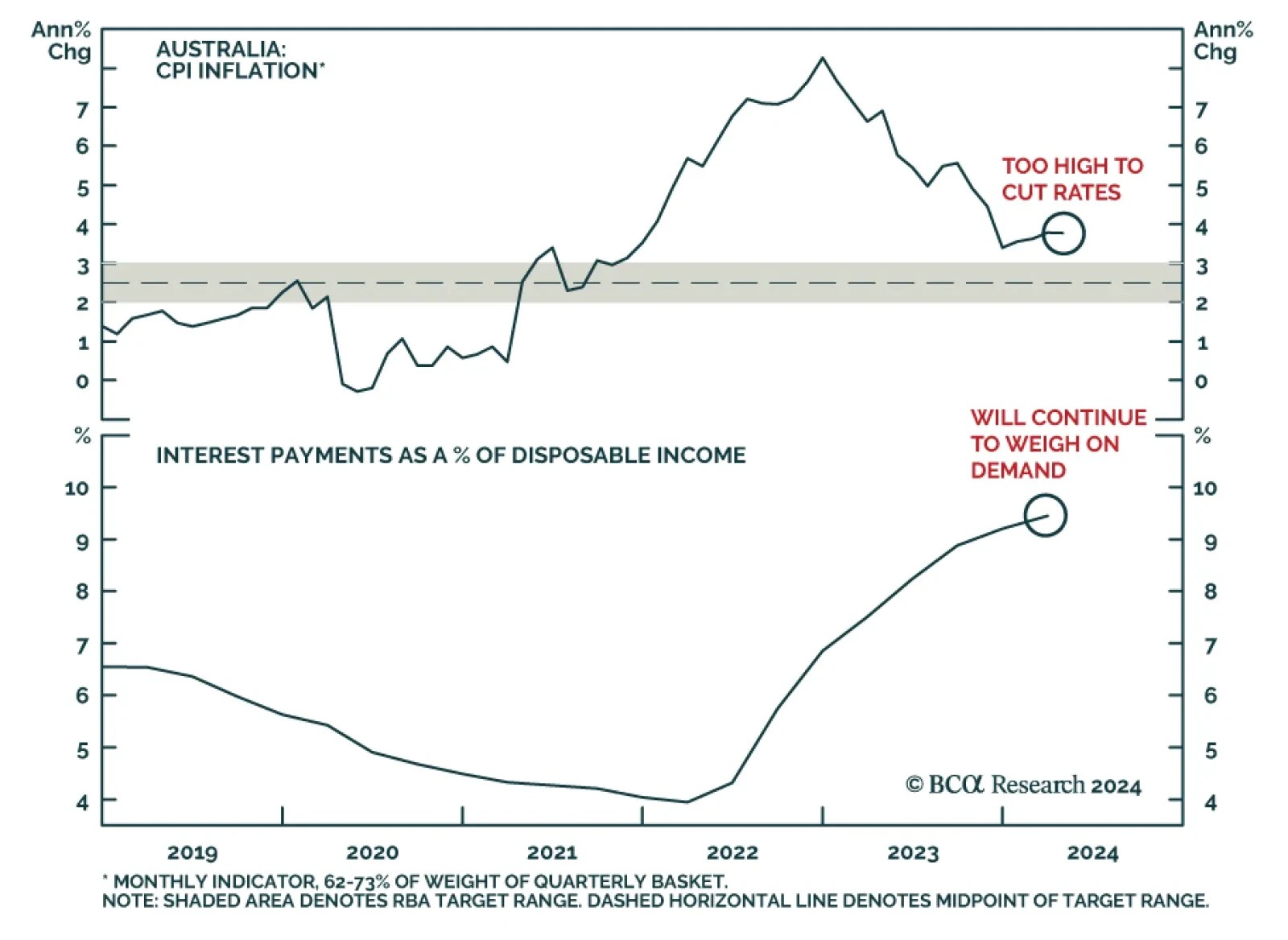

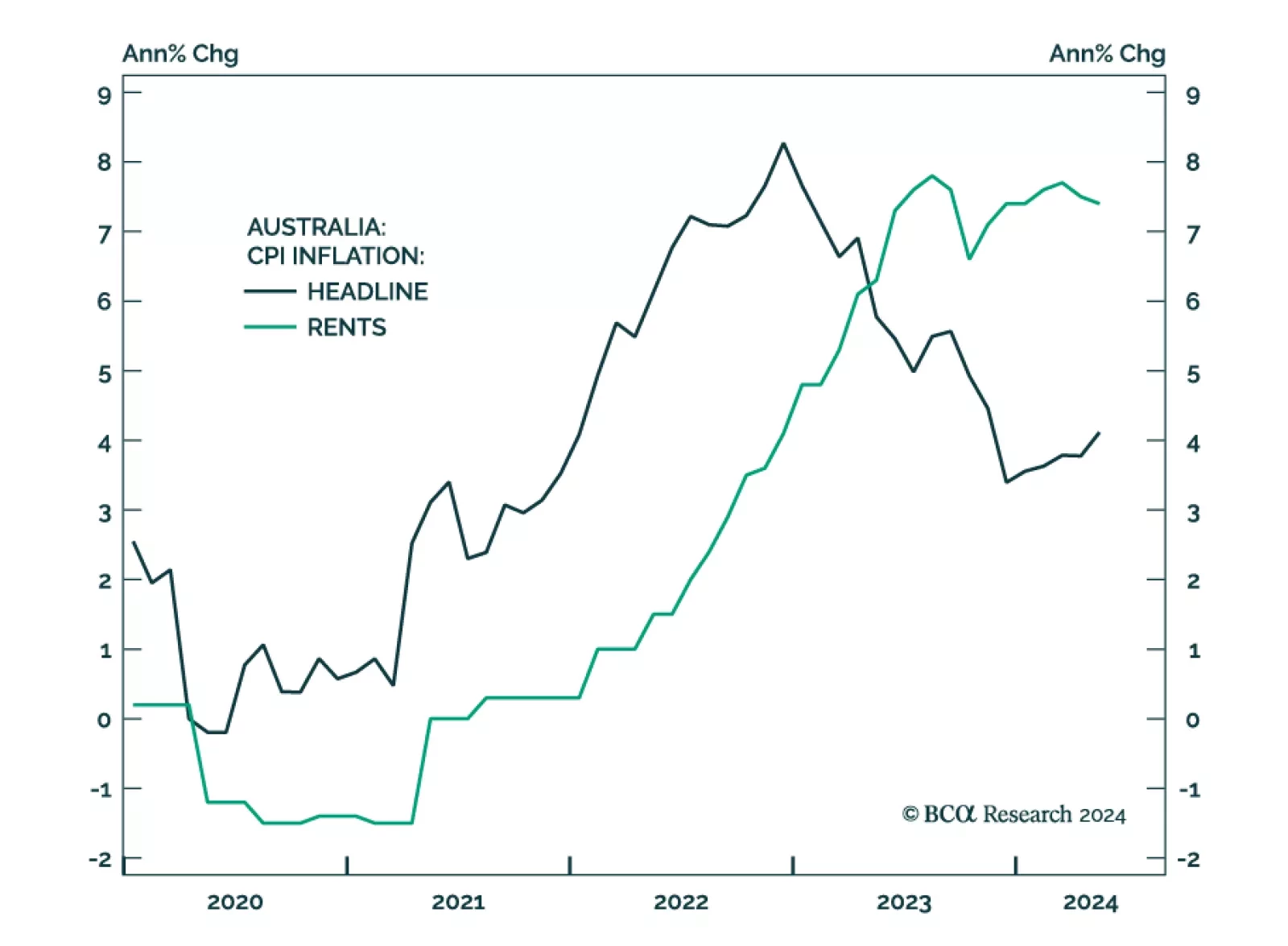

Inflation/Deflation

In Section I, we examine some concerning signs of US economic weakness that emerged in June. We also discuss portfolio positioning in the face of falling interest rates and cross-check our recommended US equity overweight in the face of extremely optimistic expectations about AI’s impact on growth. We conclude that defensive positioning continues to be warranted. In Section II, we dig into those optimistic expectations for AI. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. We doubt that AI will end up truly boosting economic activity by this magnitude.

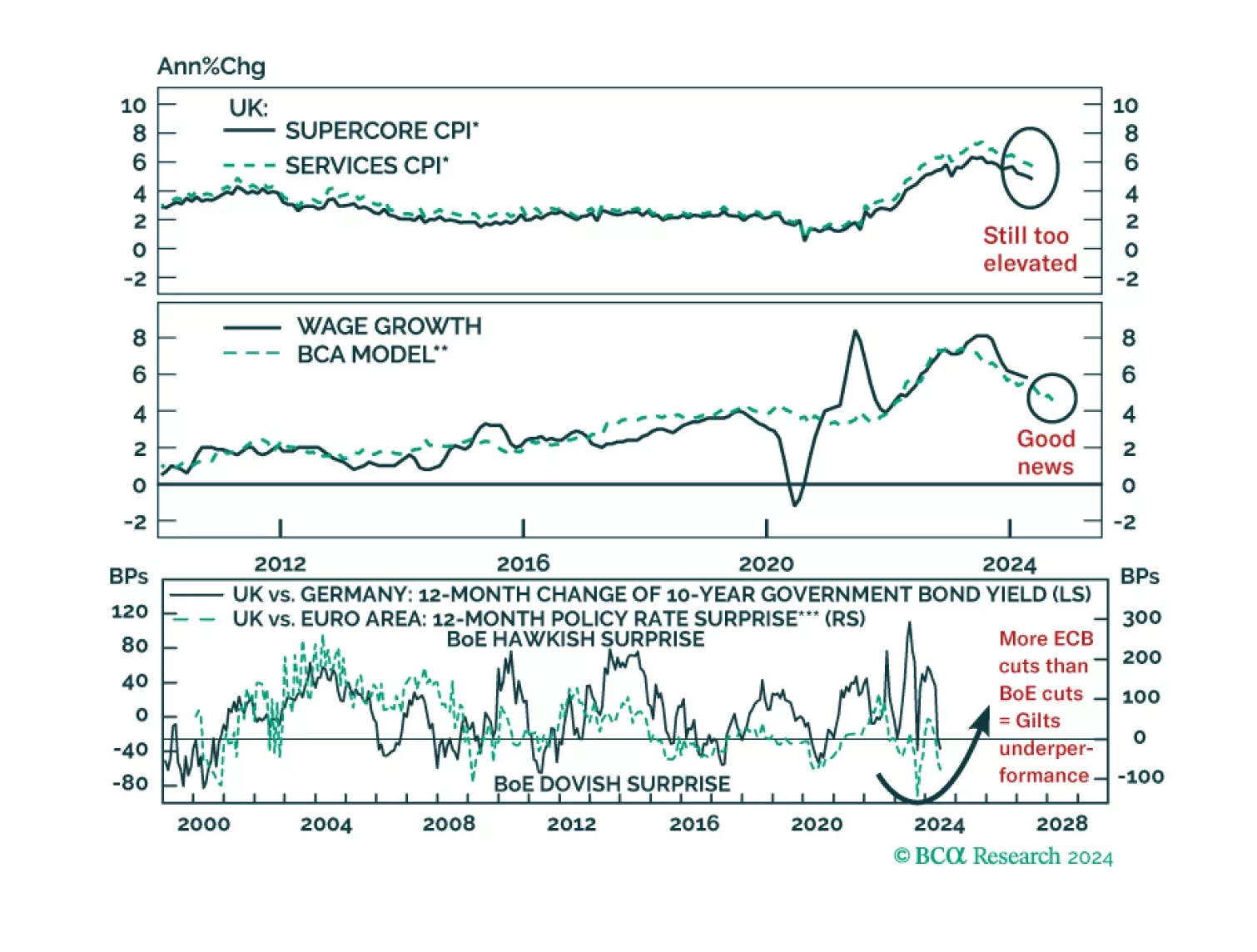

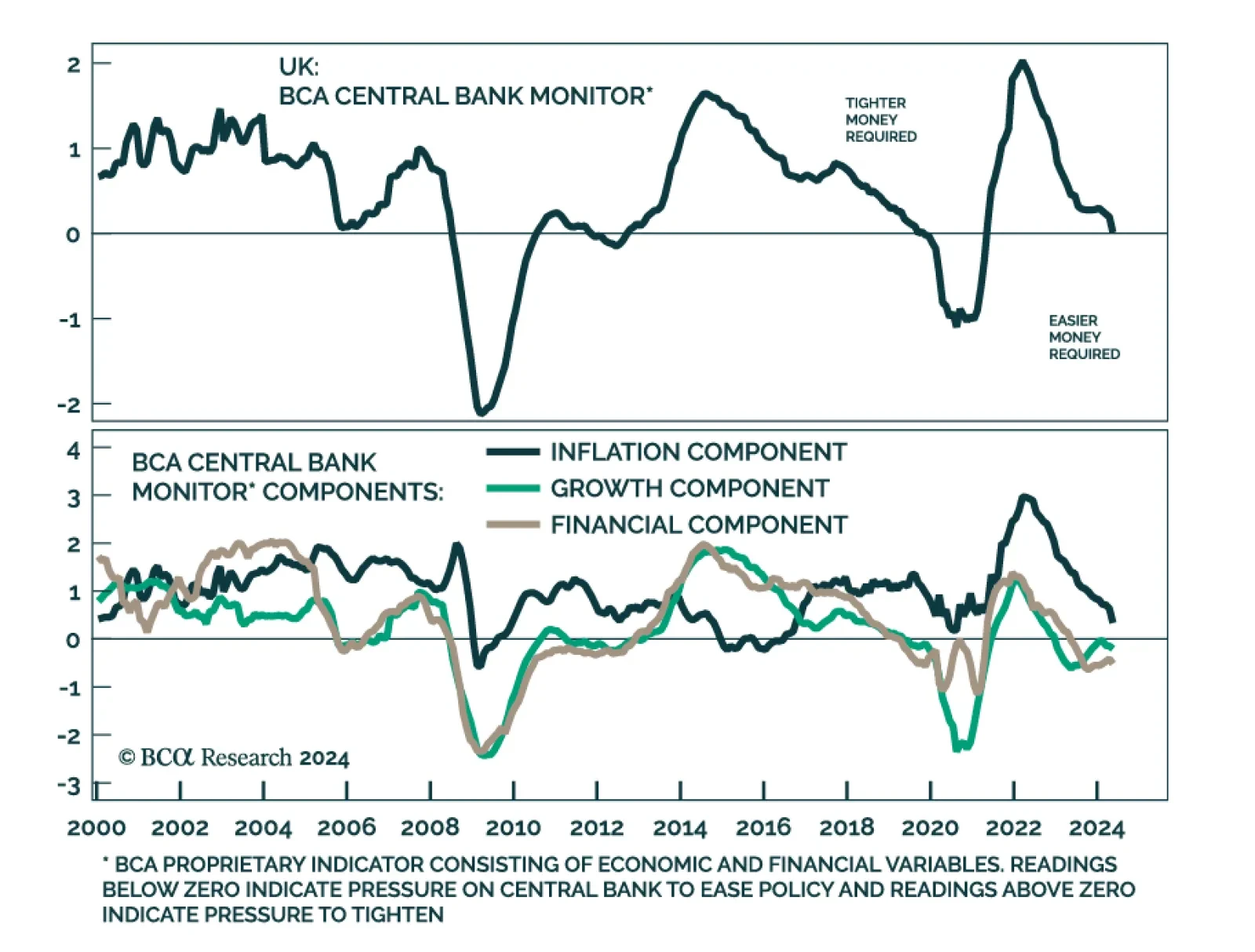

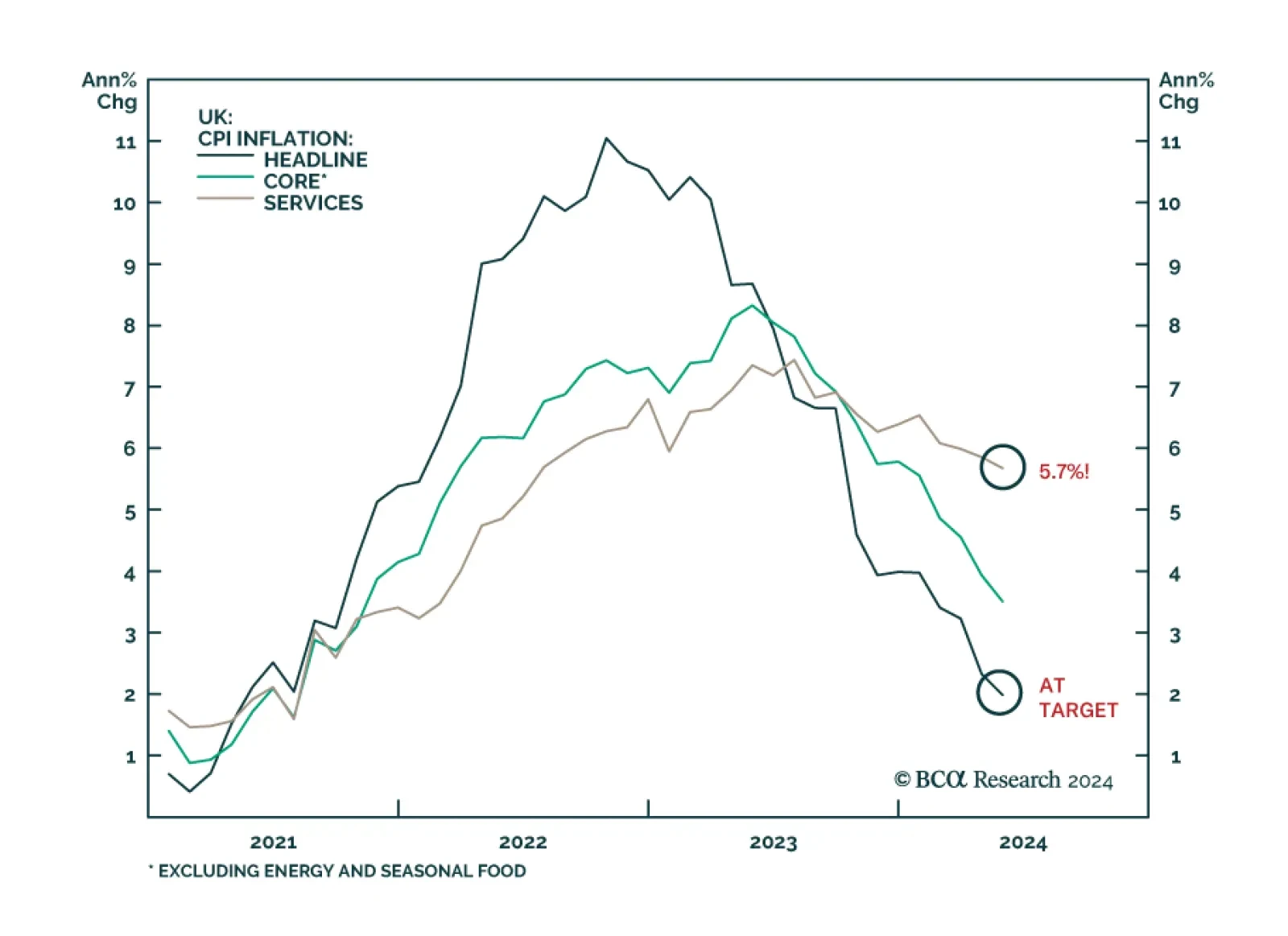

Is the BoE making a mistake moving toward rate cuts before the end of the summer? What would such a move mean for UK asset prices?

Today’s report recaps last week’s webcast and elaborates on its themes, delving into the empirical evidence underpinning our conviction that asset allocators should underweight equities sparingly and fleetingly. We remain tactically neutral and cyclically bearish.

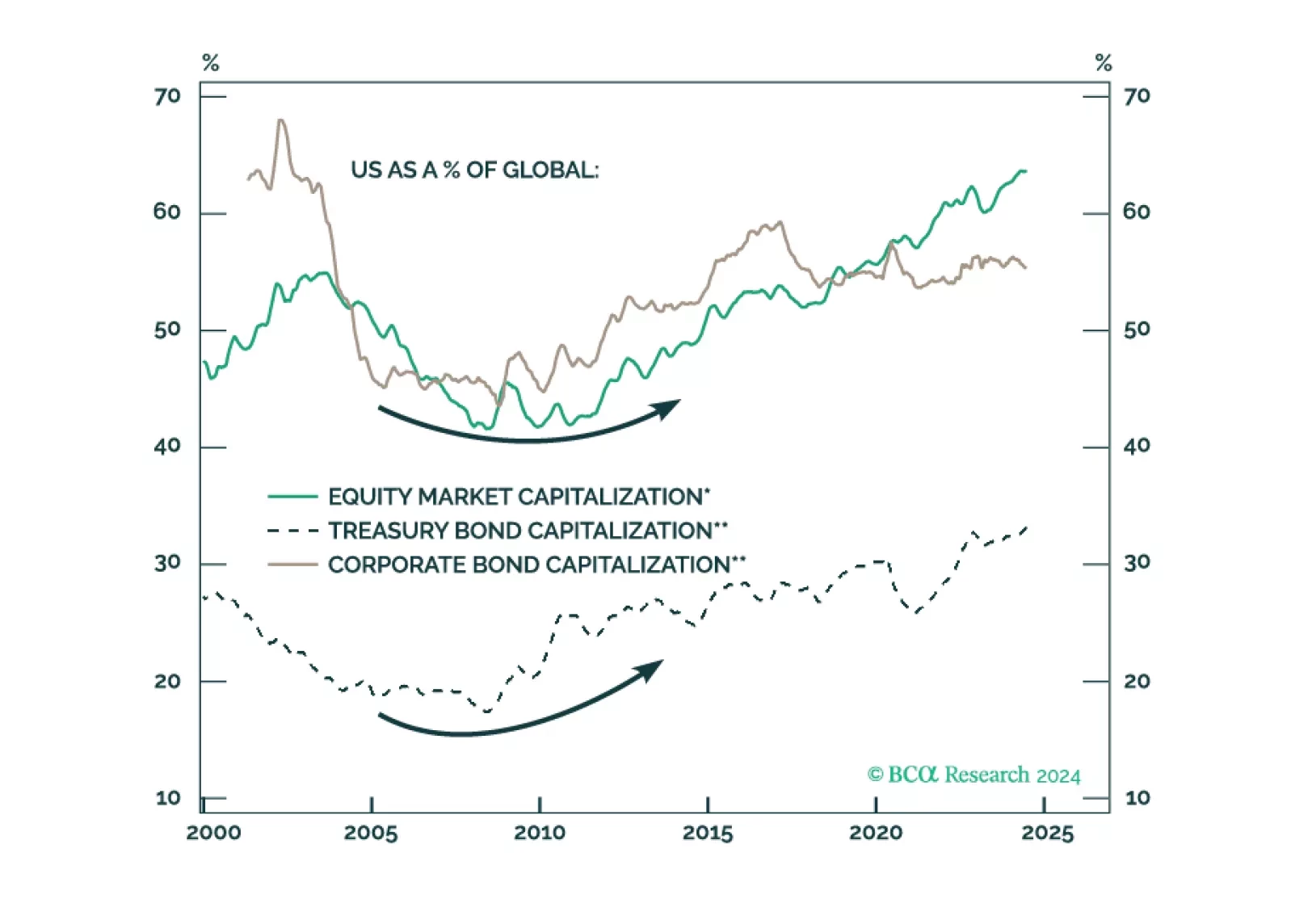

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.