Inflation/Deflation

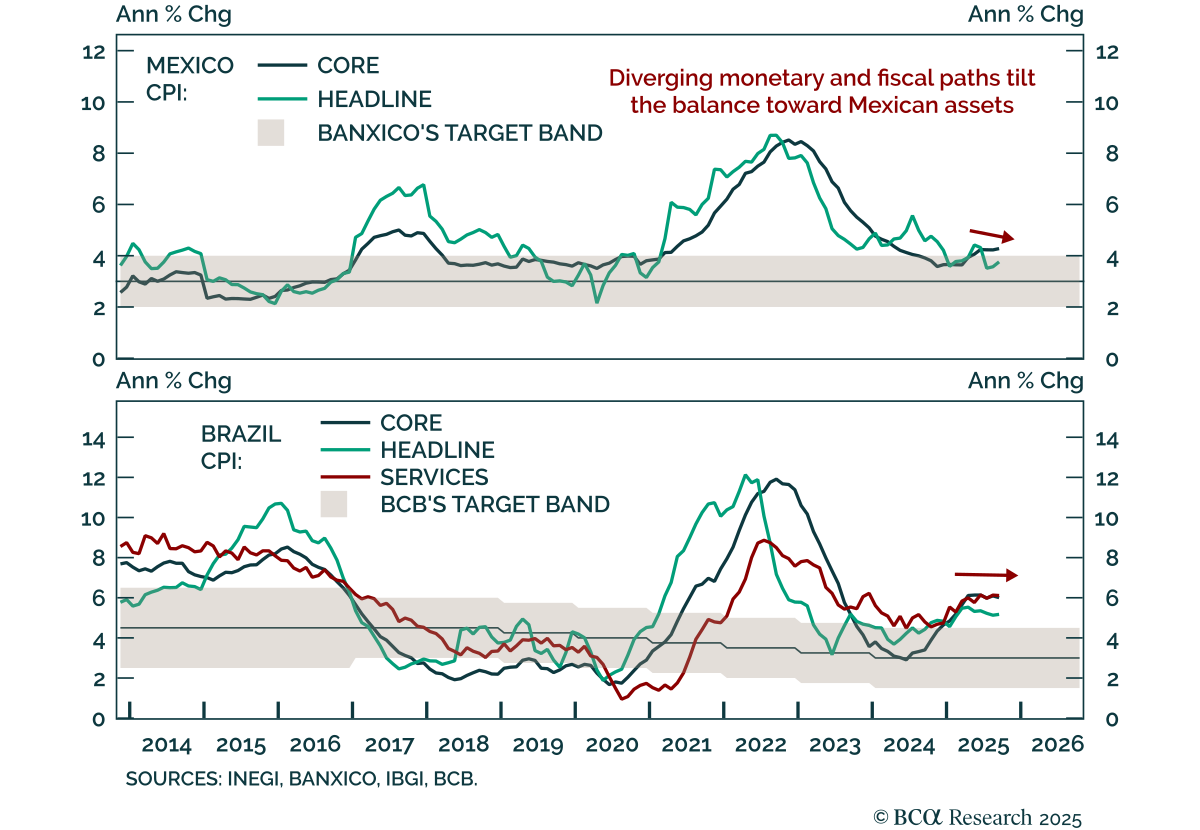

September CPI releases in Brazil and Mexico reinforce a divergent inflation and policy outlook that supports an overweight stance in Mexican local bonds and currency relative to Brazilian assets. Brazil’s headline CPI at 5.2% was slightly higher than in…

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

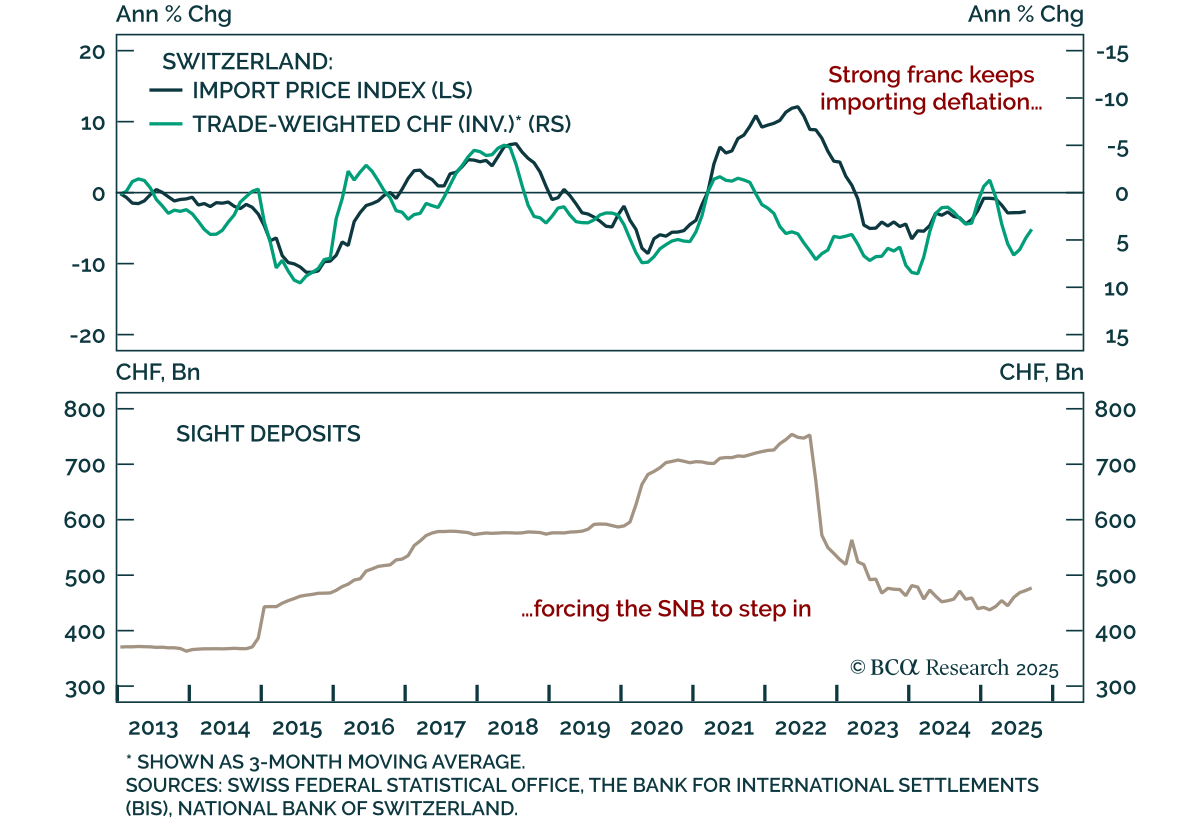

Expect greater currency interventions and negative policy rates from the Swiss National Bank (SNB), reinforcing a neutral stance on CHF and Swiss sovereign debt over the next 12 months. In recent joint statement on foreign exchange practices, the…

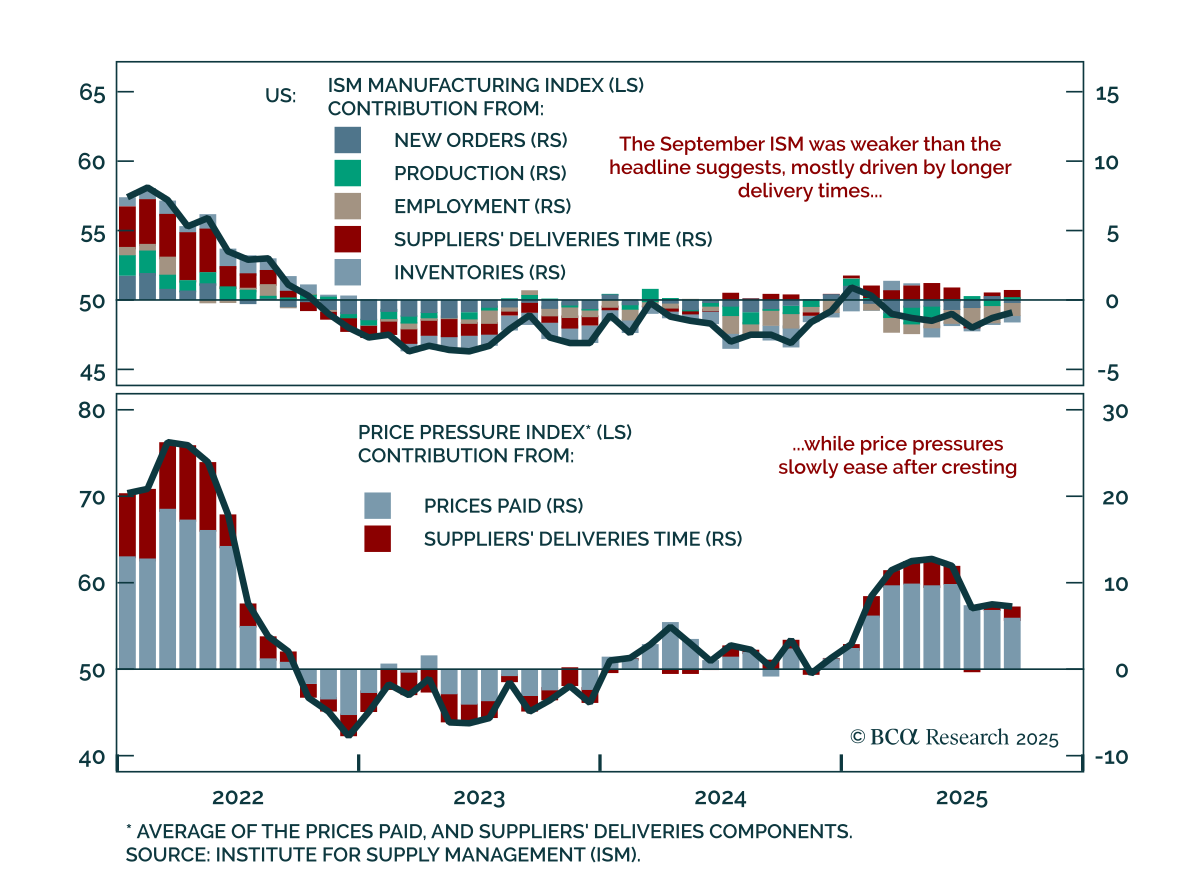

The September ISM Manufacturing index beat expectations at 49.1, but details confirm weak momentum and tariff-driven pressures. The headline improved from 48.7 in August, its second consecutive monthly gain, but the uptick came mainly from longer supplier…

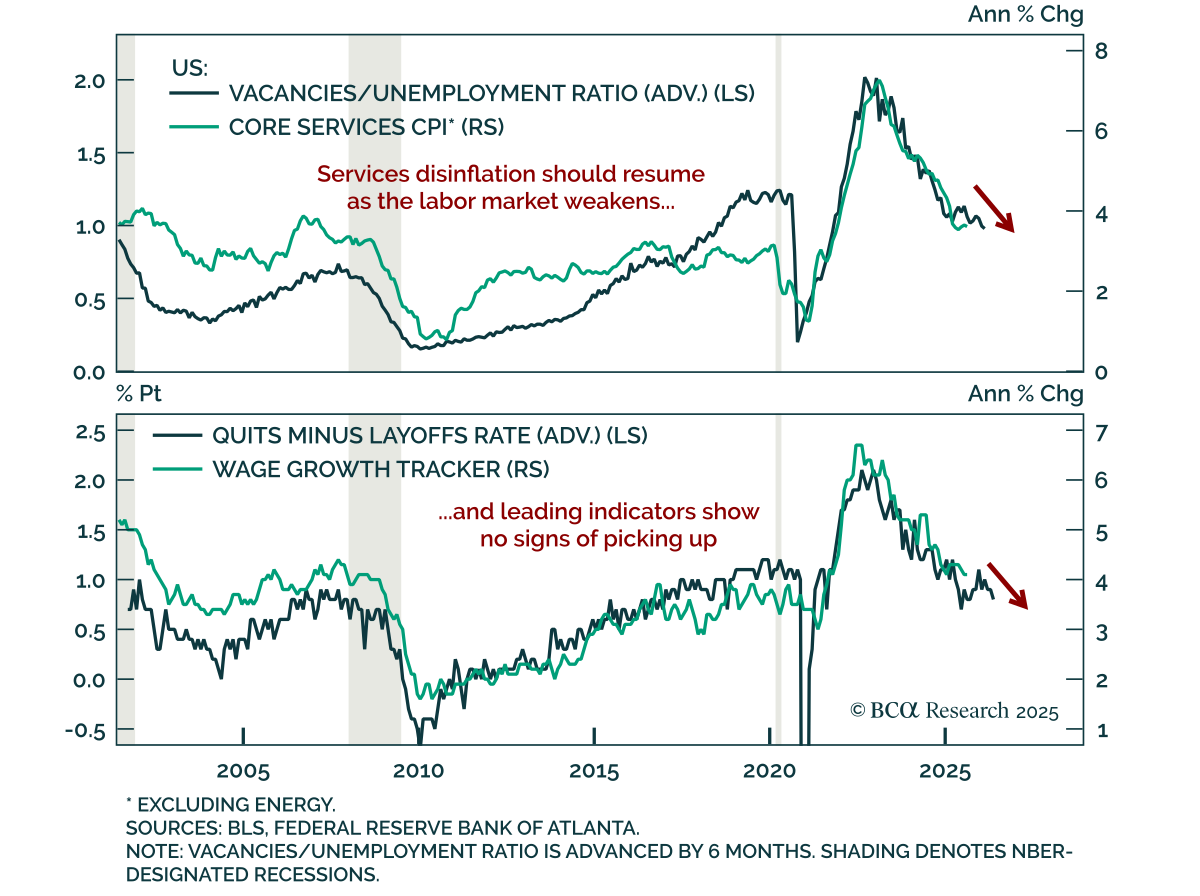

August JOLTS data confirm a loosening labor market, reinforcing a modestly defensive allocation stance. Job openings ticked up to 7.23m from 7.21m, yet gains came from non-cyclical sectors. Quits fell to 3.09m from 3.17m, pushing the quits rate down to 1.9%…

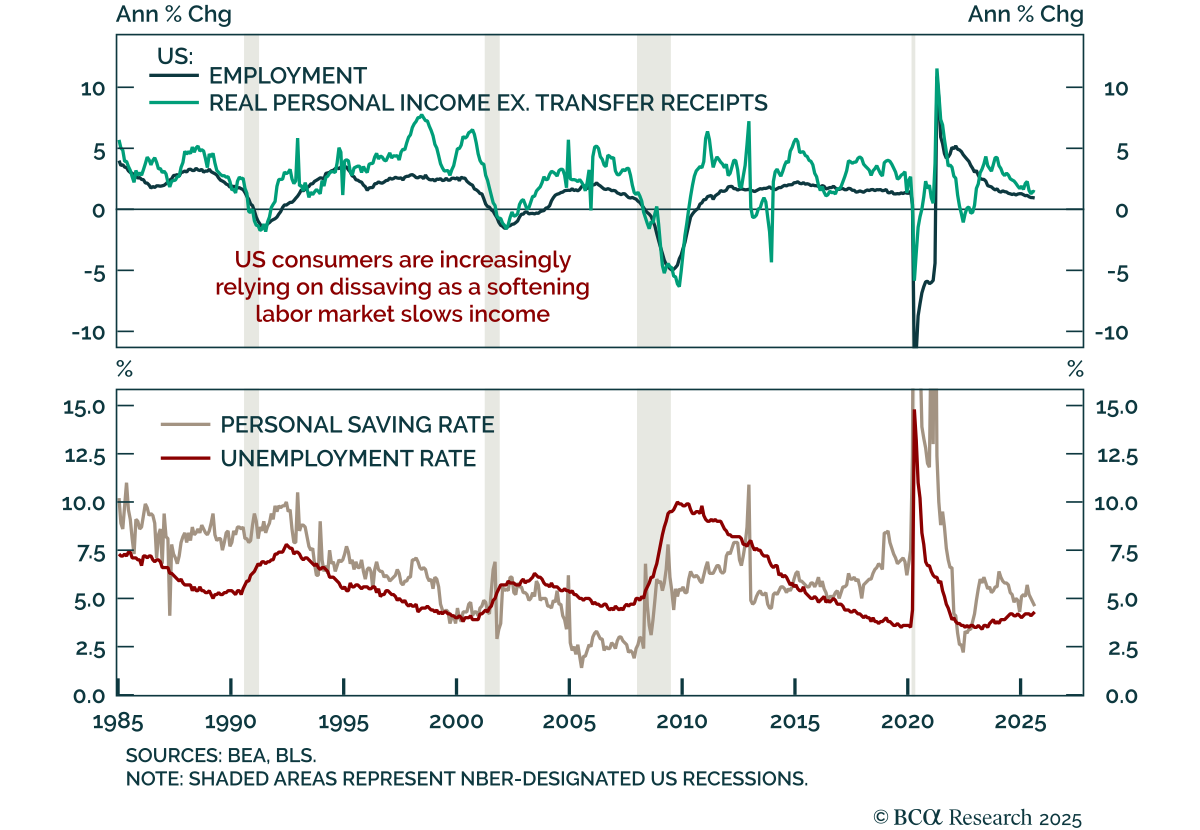

September consumption and income data beat estimates, showing a resilient US consumer but leaving the outlook fragile. Personal spending rose 0.6% m/m, outpacing income at 0.4%, pushing the saving rate down to 4.6%, its lowest level this year. Adjusted for…

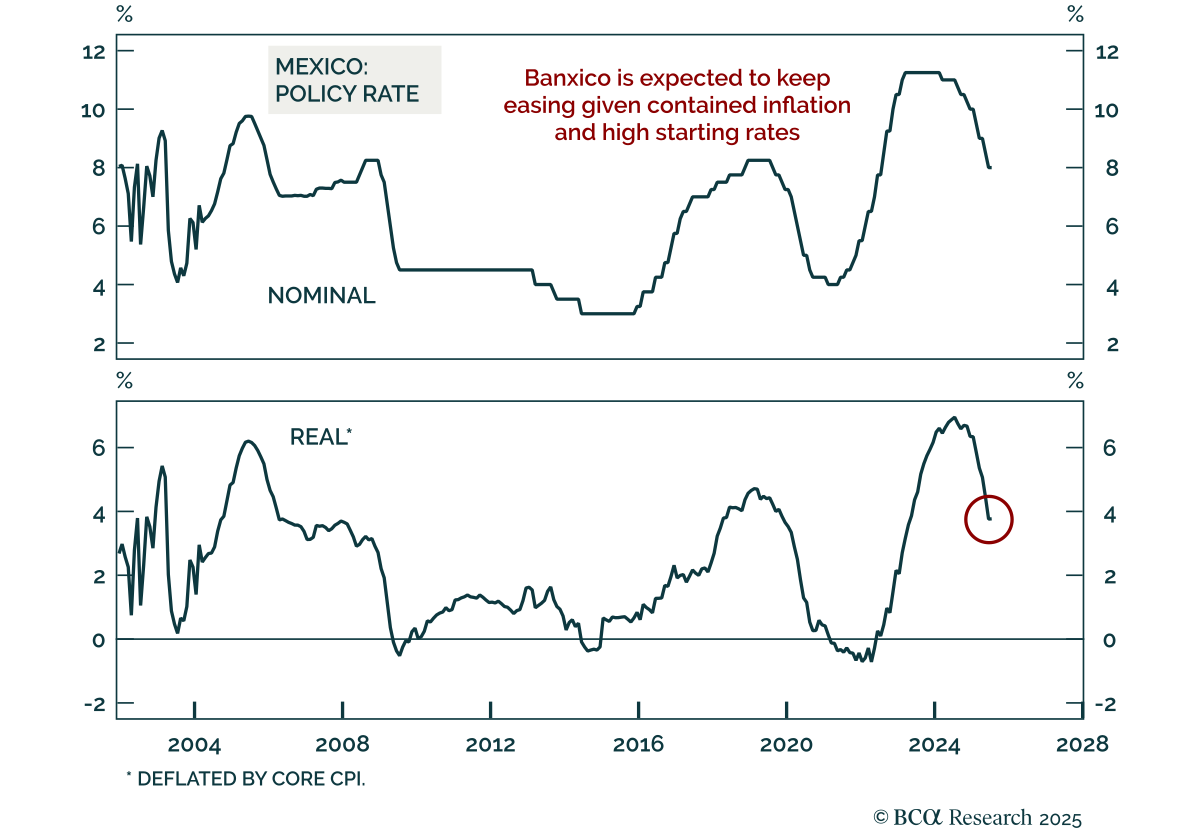

Banxico cut rates to 7.5%, reinforcing our call to go long Mexican local bonds and overweight Mexico across EM portfolios. Inflation is within target, giving policymakers space to ease. Sound fiscal management and strong external accounts continue to support…

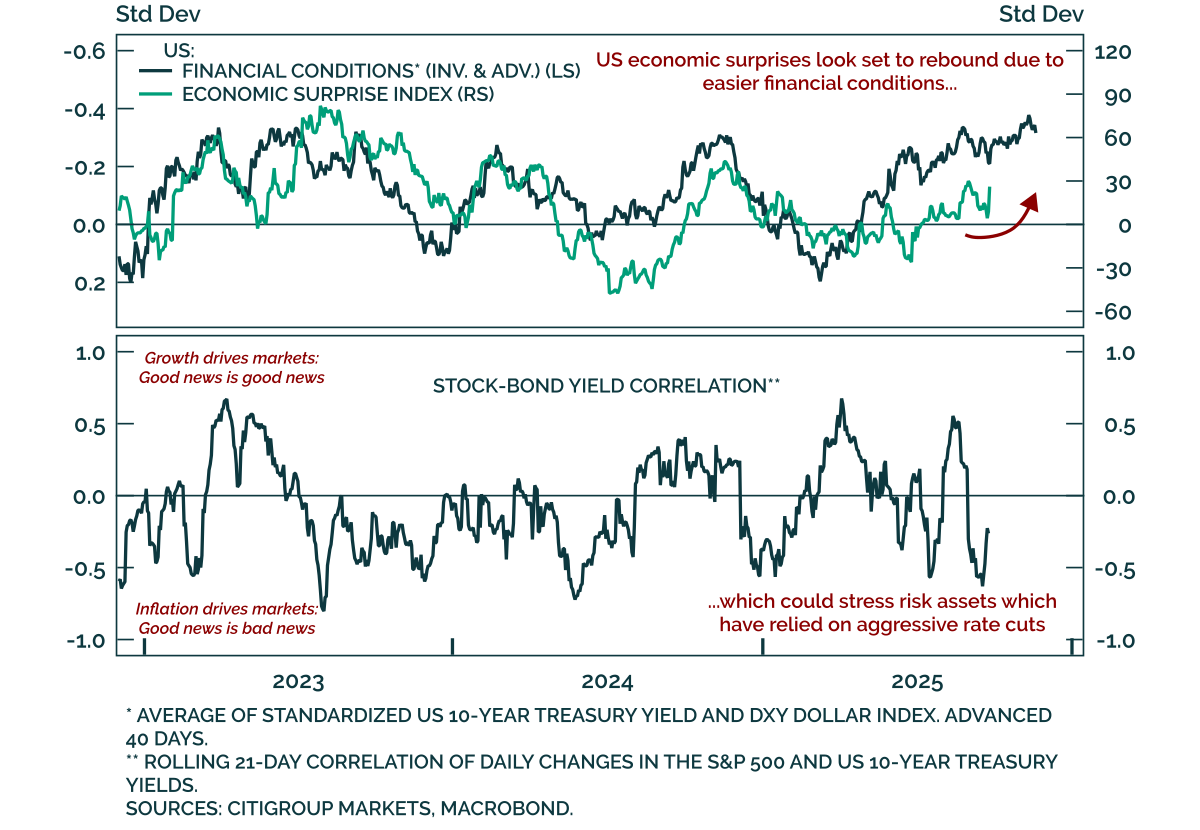

Our tactical framework, which tracks the reflexive loop between financial conditions and economic surprises, points to stronger near-term growth, leaving equities vulnerable if inflation re-accelerates. Data surprises move markets, while bond yields and the…

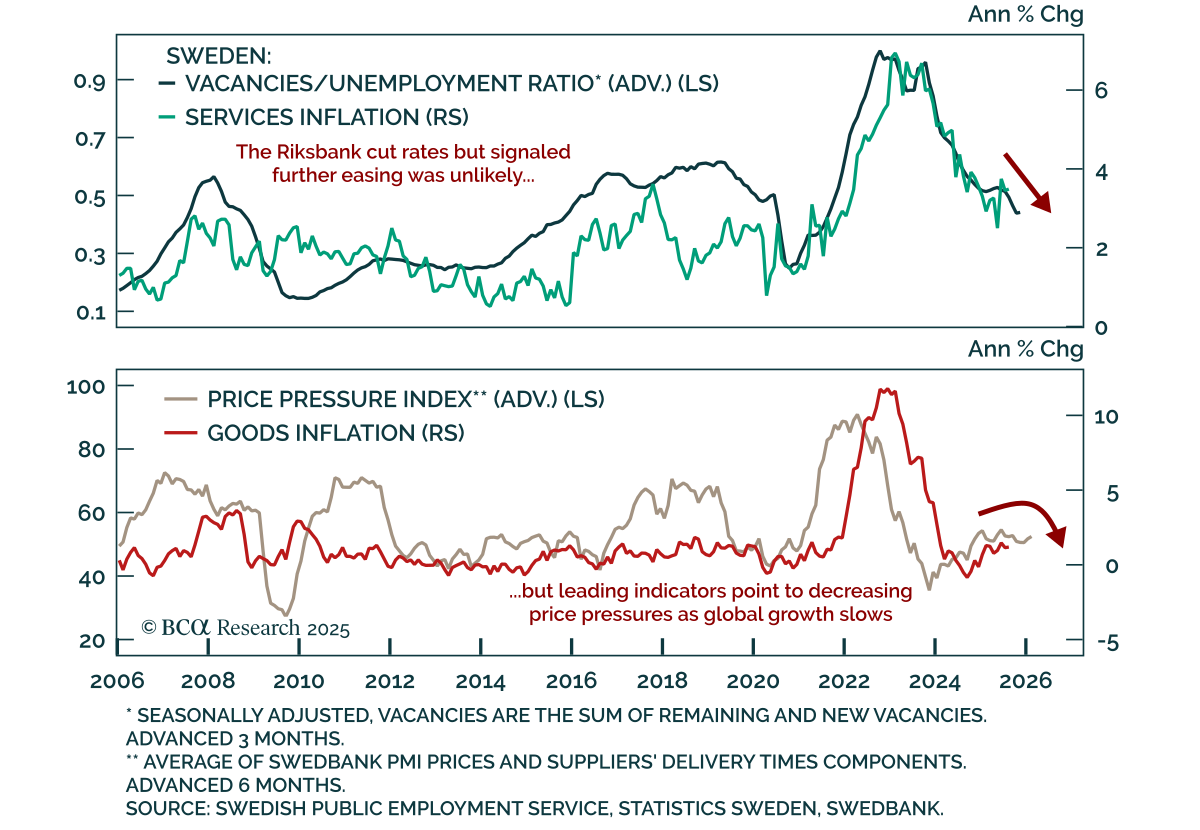

The Riksbank surprised with a 25 bps cut to 1.75%, signaling no further easing for now but keeping the door open to additional cuts as growth weakens. The move came despite recent inflation prints above the central bank’s forecasts. Leading indicators,…