Inflation/Deflation

The Fed cut rates by 25 bps to 3.75%–4.00% and announced QT will end December 1, signaling modest easing but no December cut commitment. The decision matched expectations, with dovish (Gov. Miran, for a 50 bps cut) and hawkish (Pres. Schmid, for no cut)…

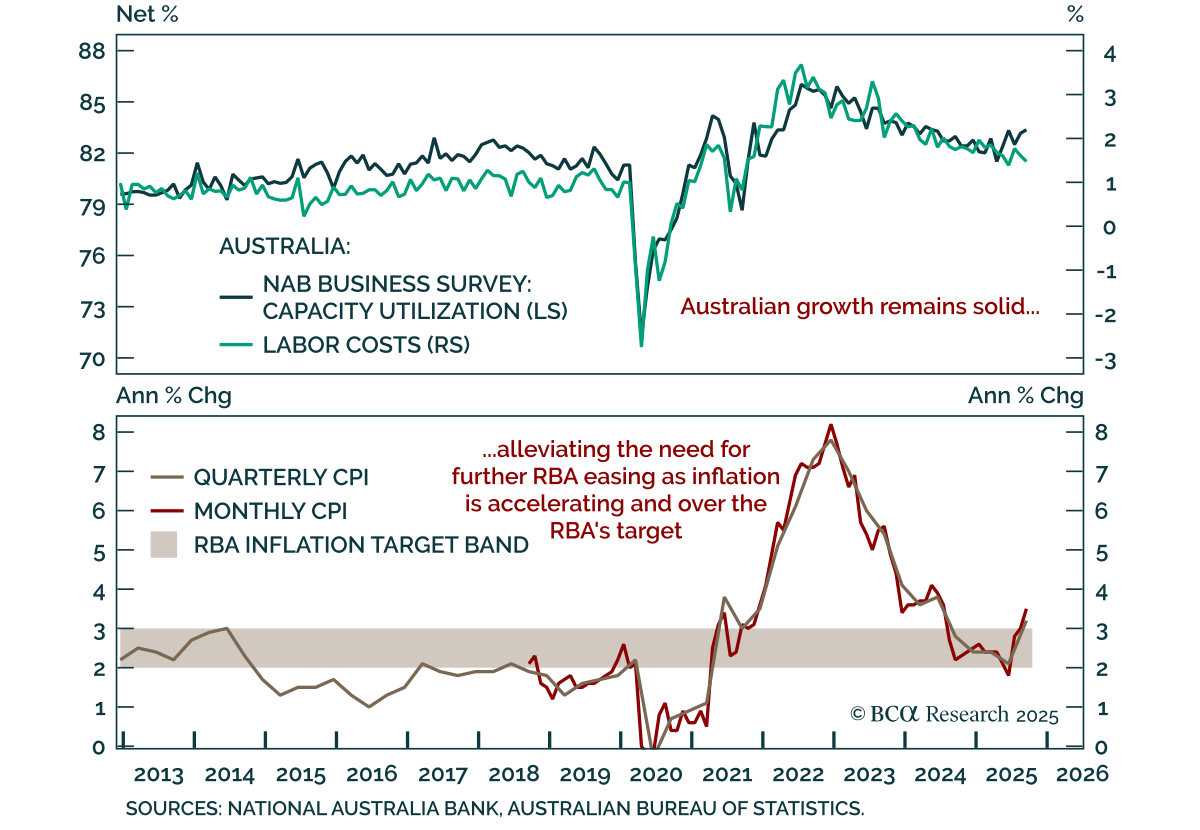

Australian September and Q3 inflation surprised to the upside, reinforcing the RBA’s cautious stance on easing. Headline CPI rose to 3.5% y/y from 3.0%, above the RBA’s 2–3% target range, while trimmed mean CPI increased to 2.8% from 2.6%. The September data…

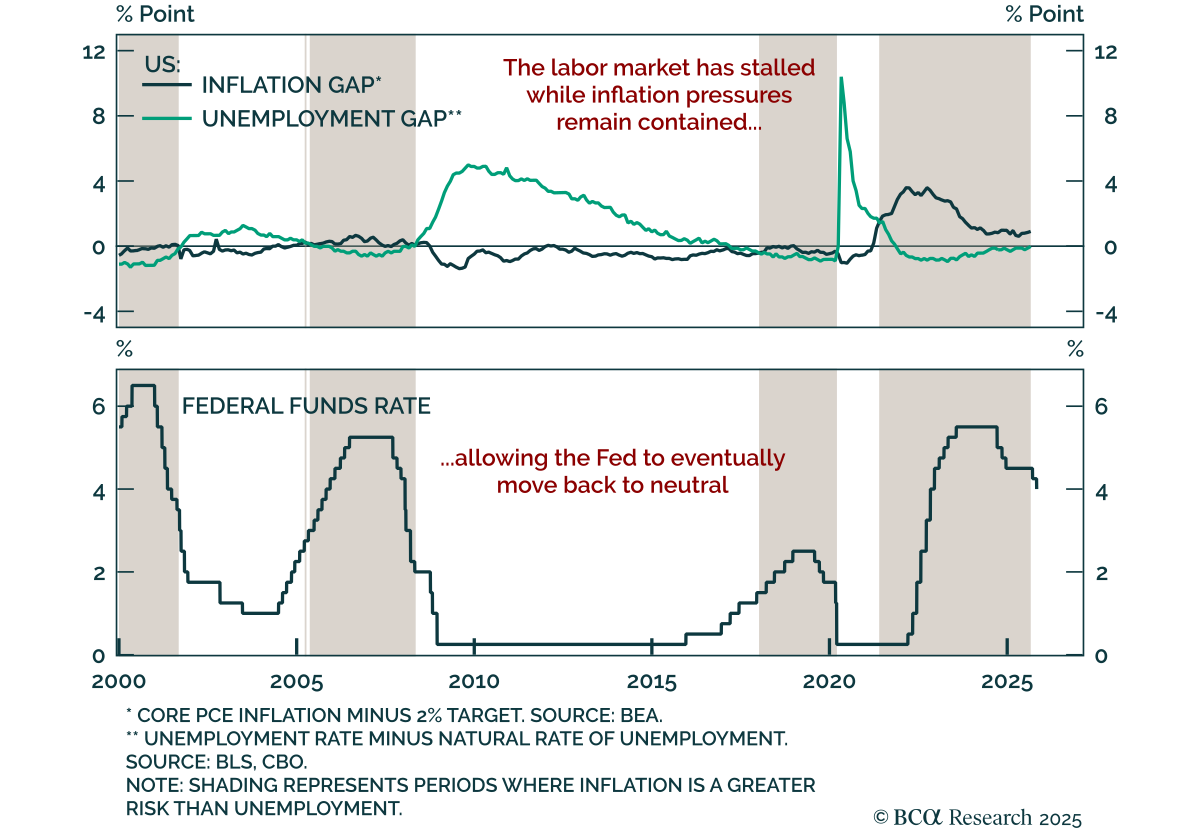

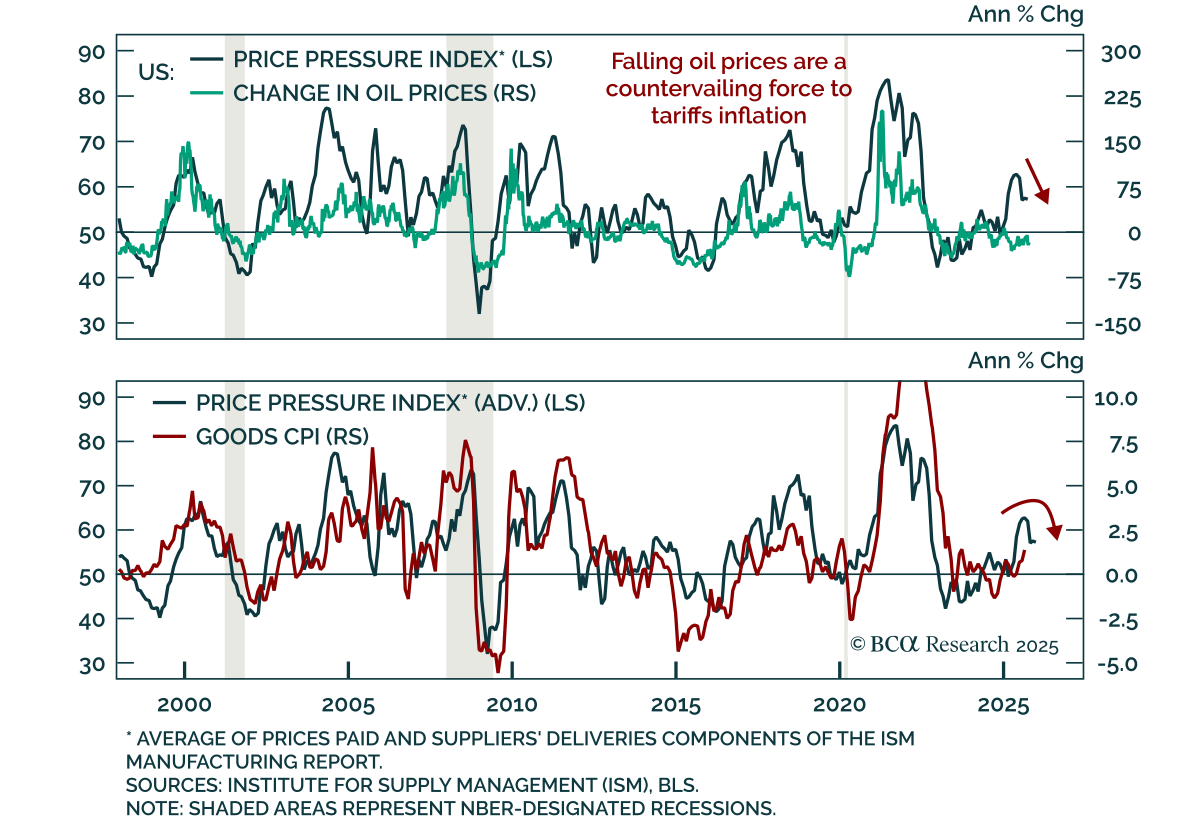

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

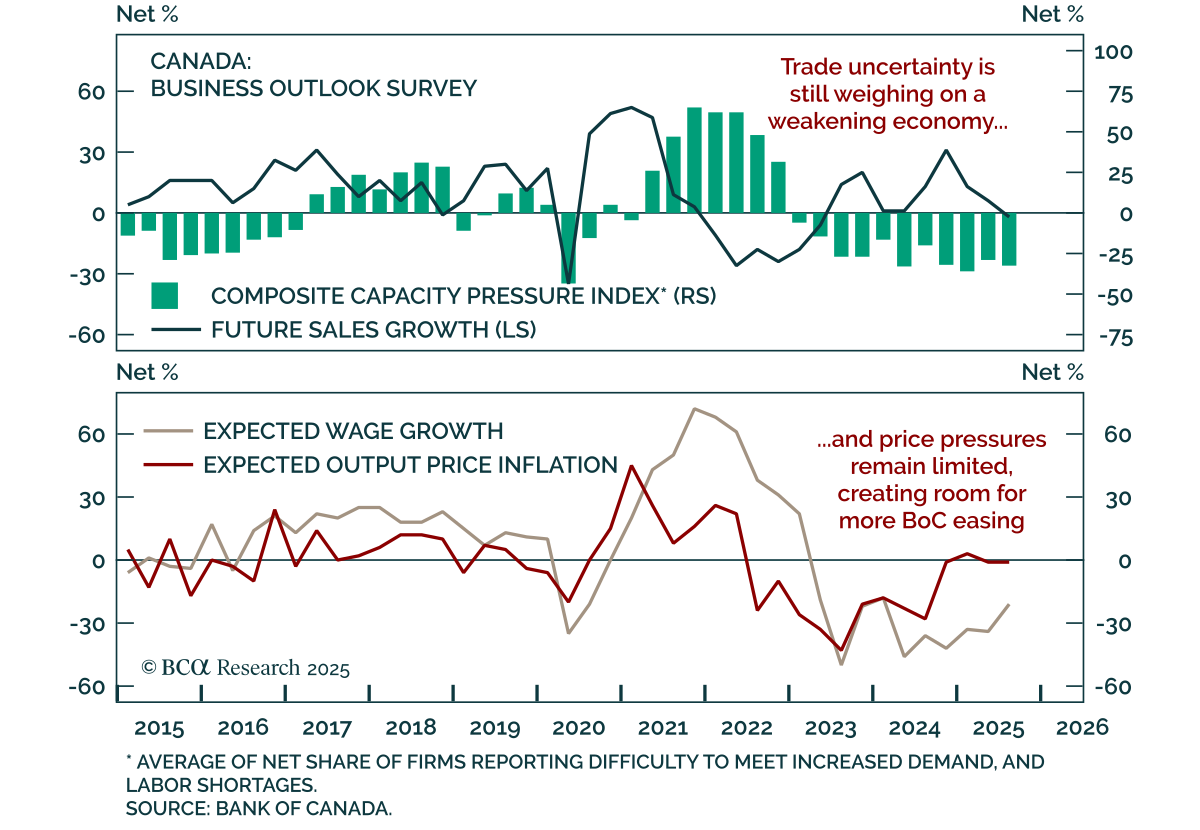

Canada’s Q3 Business Outlook Survey paints a weak macro picture with limited price pressures, supporting an overweight on CGBs and CAD 5s10s steepeners. The BOS Indicator ticked up marginally to -2.3 from -2.4, as low capacity utilization and business…

Falling oil prices are countering tariff-driven inflation which, along with a weakening labor market, is reinforcing a long duration stance. Brent crude broke below the $65/bbl support level held since June and WTI is now down 16% from a year ago. Falling oil…

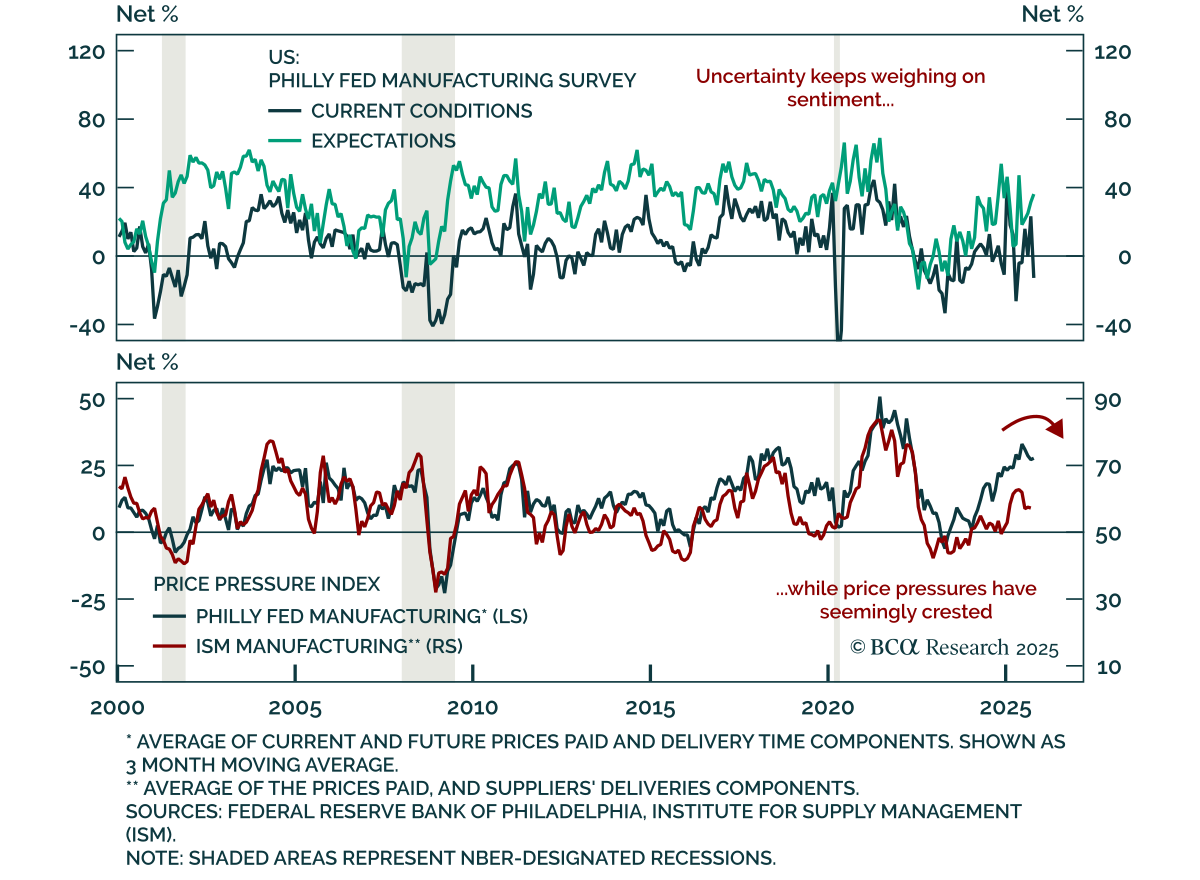

The October Philadelphia Fed manufacturing survey was mixed, showing weak headline data but steadier underlying components. The headline index fell to -12.8 from 23.2, the lowest level since April 2025. Underlying details were not as dire: shipments moderated…

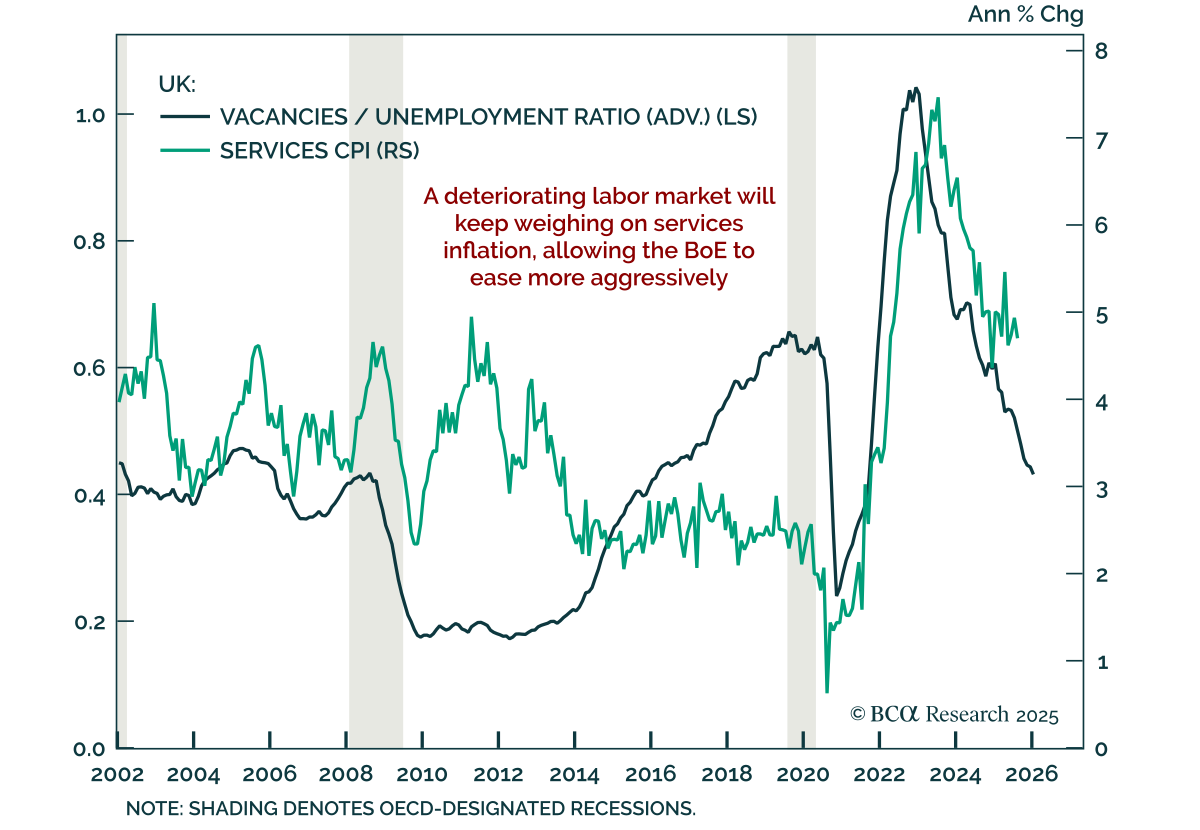

UK labor data weakened in August and September, reinforcing downside inflation risks and supporting overweight Gilts with 2s10s steepeners. Payrolls fell by 10k in September, while job vacancies continued to slide to cyclical lows as unemployment reached…

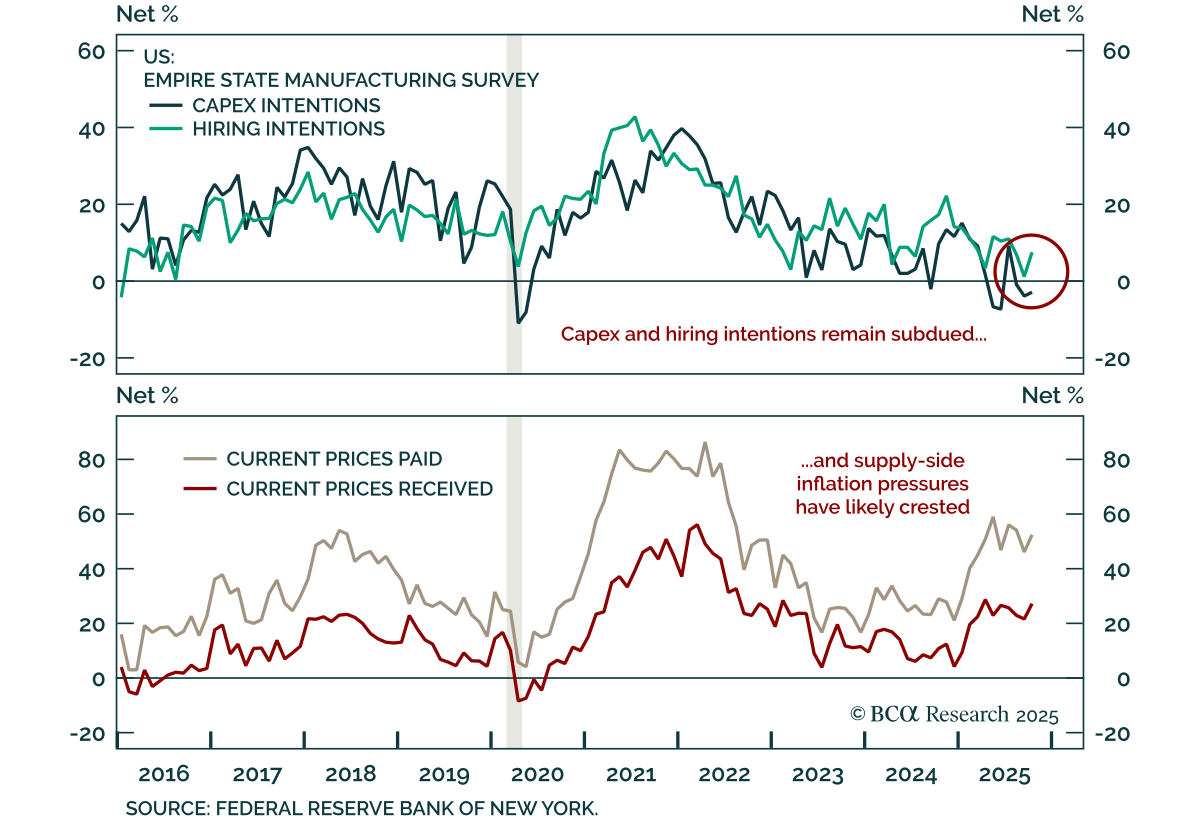

The October Empire Manufacturing survey beat estimates, but weak investment and hiring intentions temper its positive signal. The index rose to 10.7 from -8.7, indicating modest activity growth. New orders ticked up, and shipments increased after plunging…

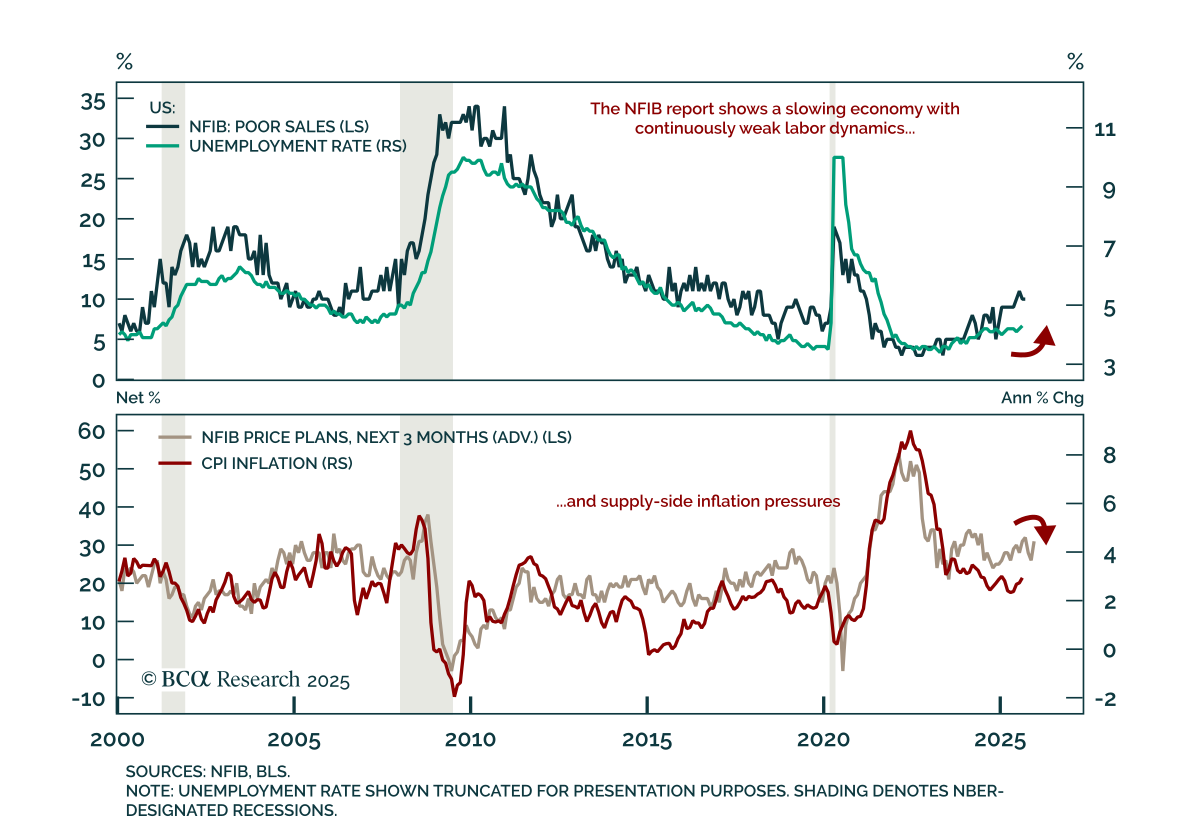

The September NFIB Small Business Optimism Index missed estimates, falling to 98.8 from 100.8. The decrease was driven by expectations, as fewer small businesses expect the economy to improve or real sales to rise. Firms also reported inventories as too high,…

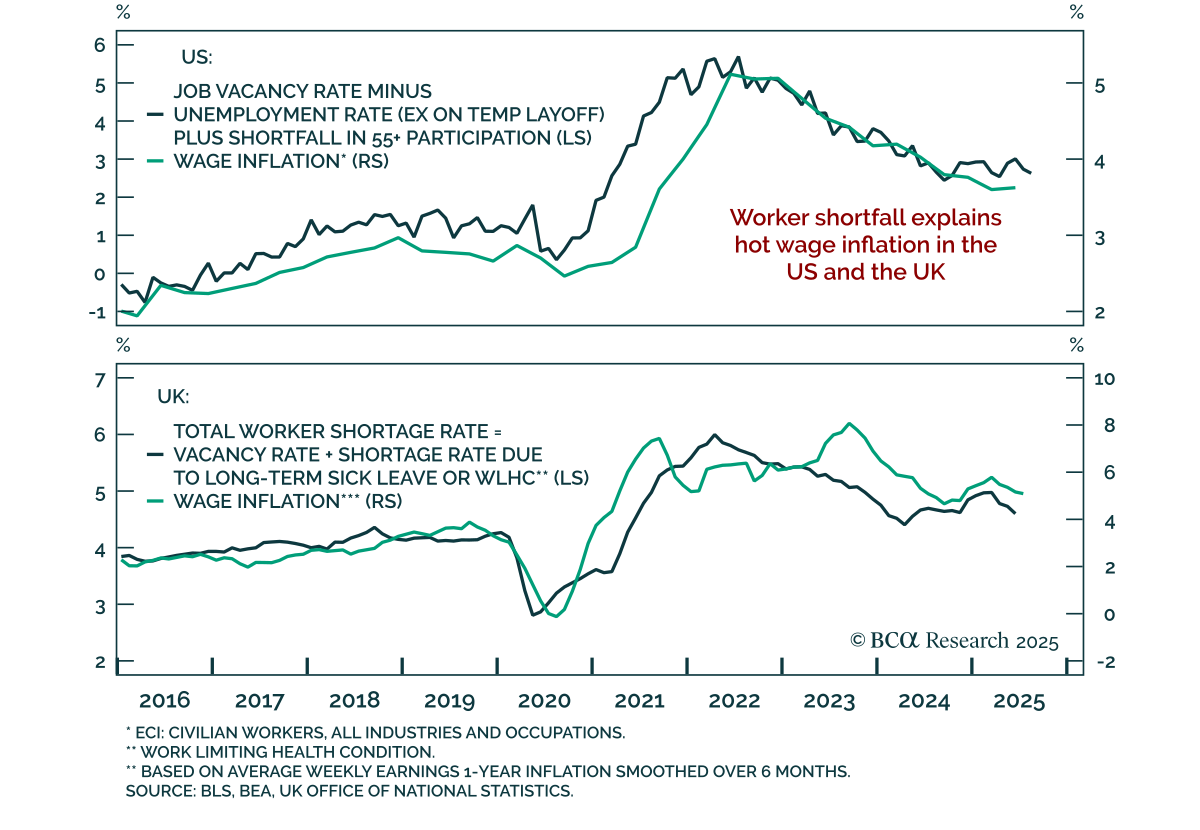

Persistent wage pressures in the US and the UK stem from similar structural worker shortfalls, according to BCA’s Counterpoint Strategy. In both economies, headline labor data mask hidden deficits created by early retirements in the US and long-term illness…