Inflation/Deflation

BCA Research’s Global Asset Allocation service continues to recommend an overweight on government bonds, neutral on cash, and underweight on equities and credit. Market technicals do not suggest this is a robust broad-based equity rally. The US stock…

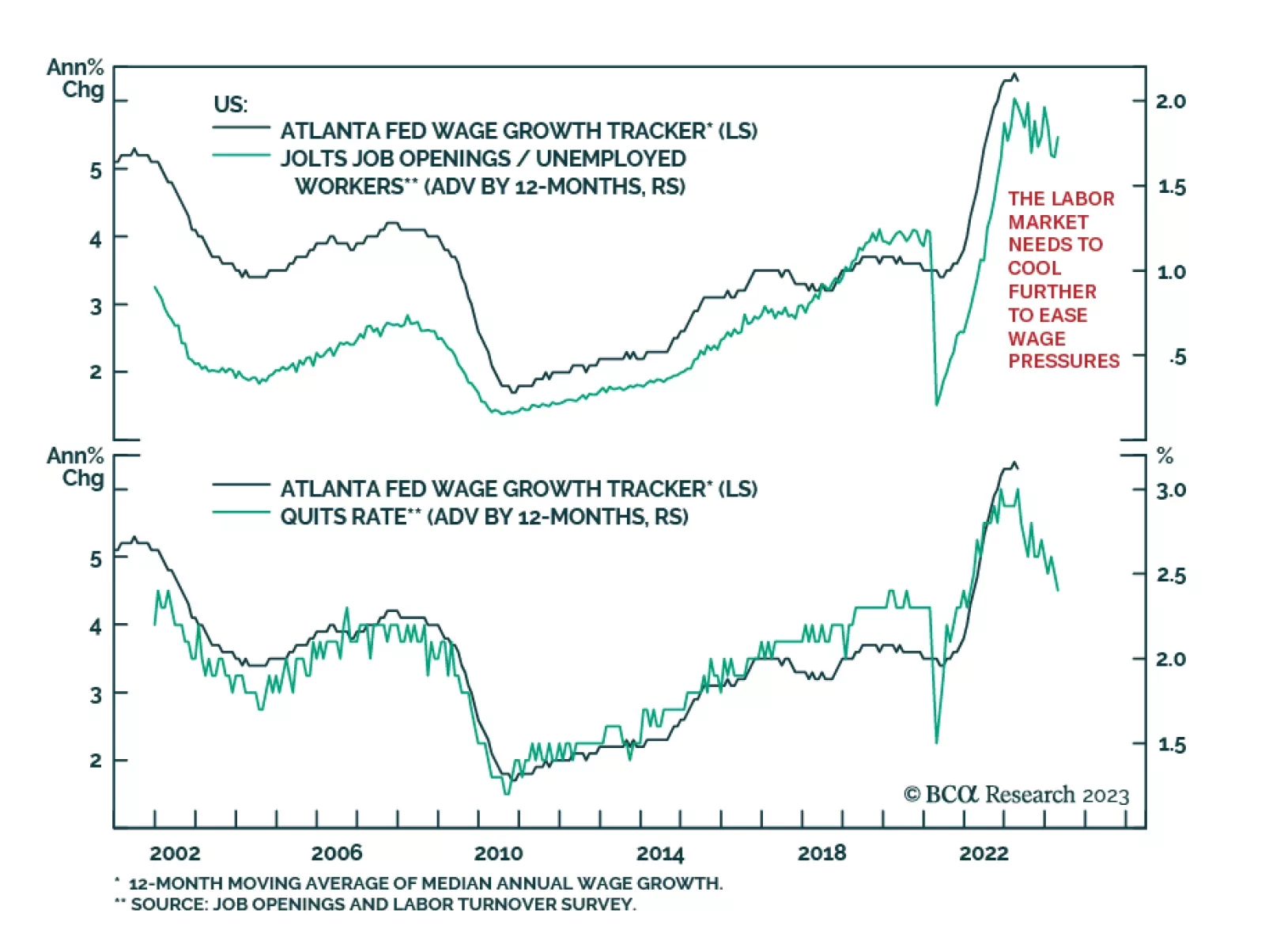

The JOLTS survey for April shows job openings unexpectedly rising from an upwardly revised 9.7 million to 10.1 million – above expectations of a decline to 9.4 million. The job openings rate inched up to 6.1% from 5.9% while the ratio of job openings to…

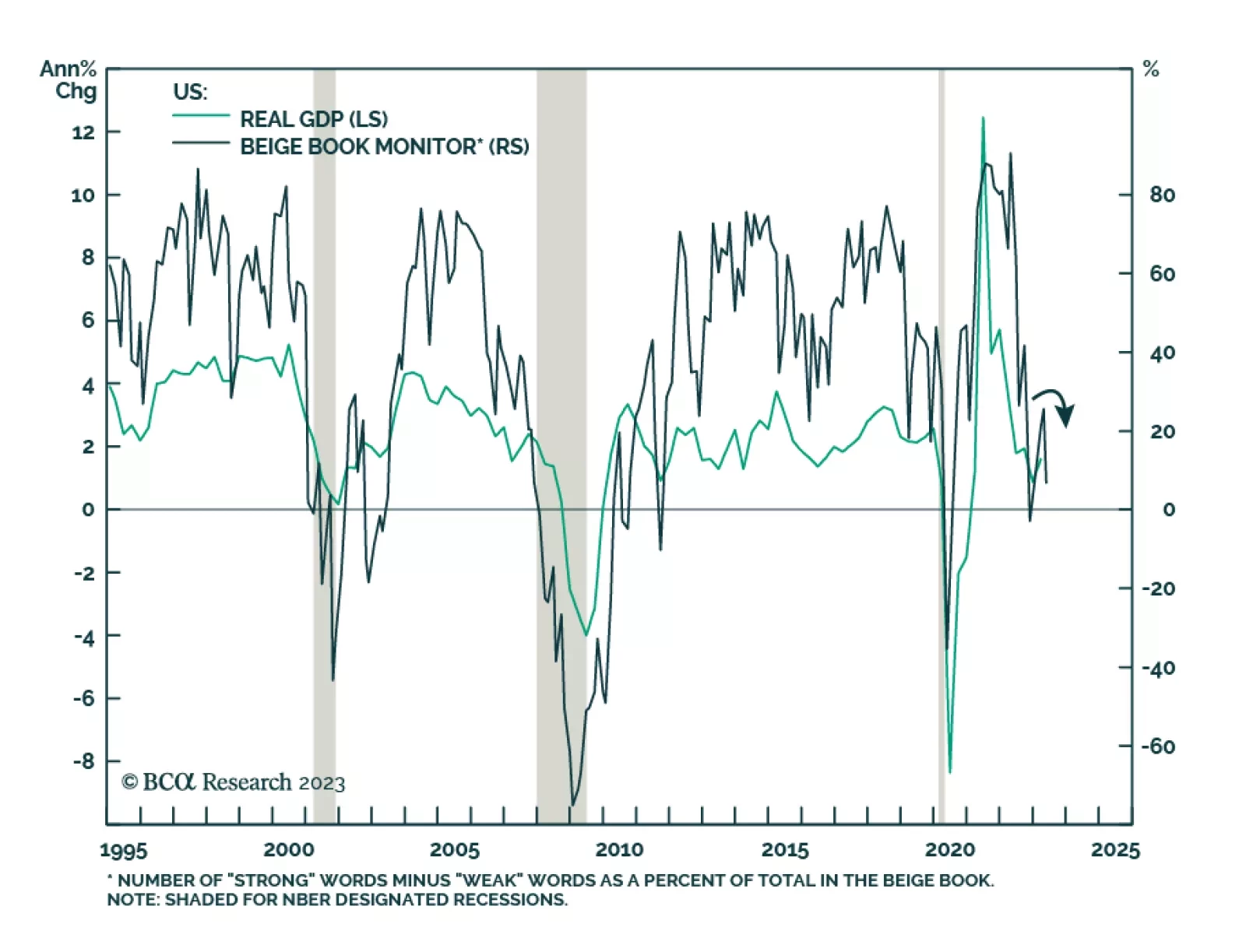

The Fed’s Beige Book is signaling that the US economy is losing steam following an improvement in momentum earlier this year. The release revealed that future growth expectations deteriorated. In particular, manufacturing activity was weak across most of the…

Expectations for oil demand growth through 2023-24 are way too optimistic. Until these expectations fall to -0.5-1 percent, the oil price has further downside. Plus: collapsed complexity confirms that AI is in a mania, while basic materials stocks and ZAR/EUR are rebound candidates.

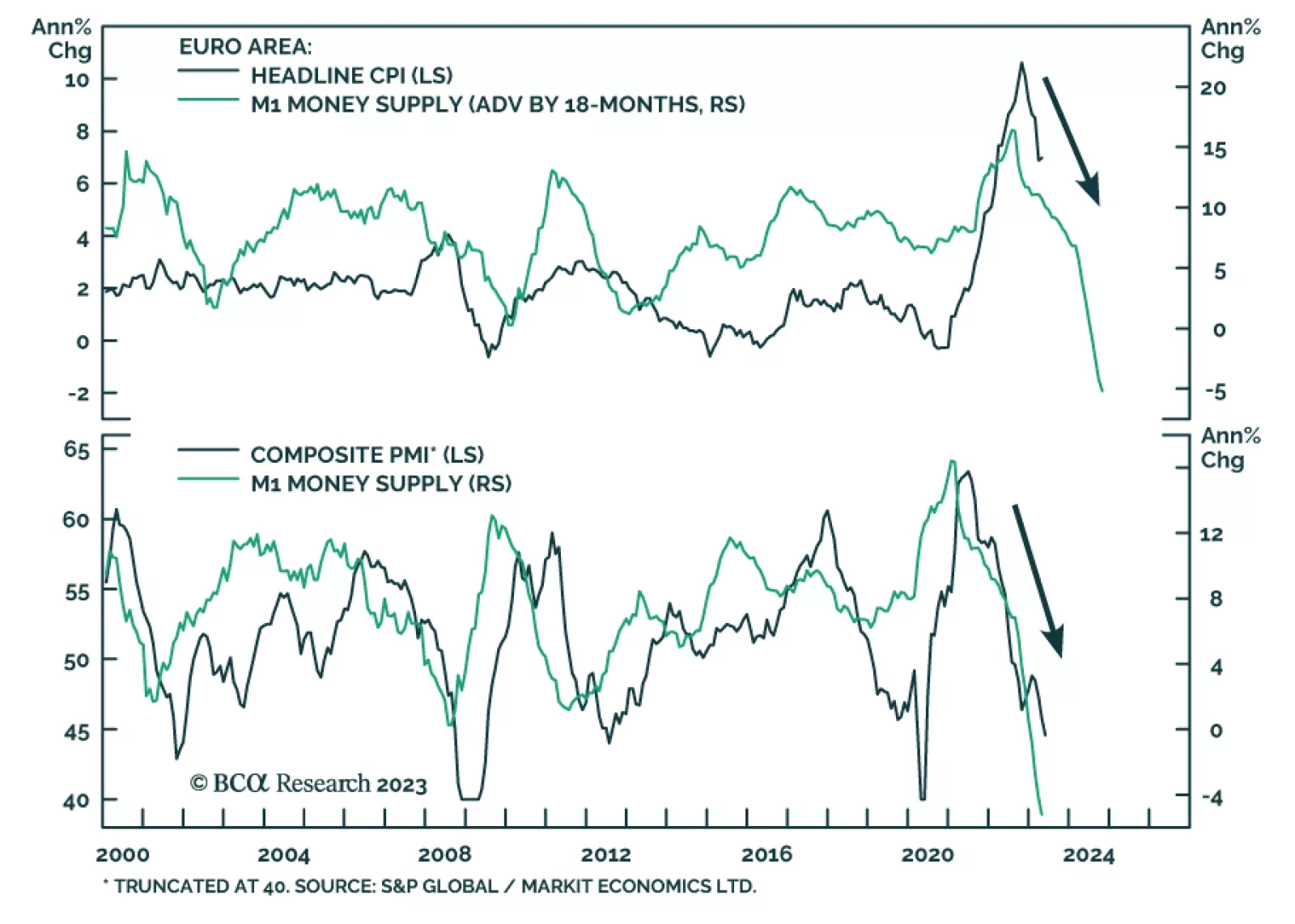

The latest Eurozone data releases show the impact of the ECB’s aggressive monetary tightening cycle. The contraction in M1 money supply – which includes currency in circulation and overnight deposits – deepened to -5.2% y/y in April while the broader M3…

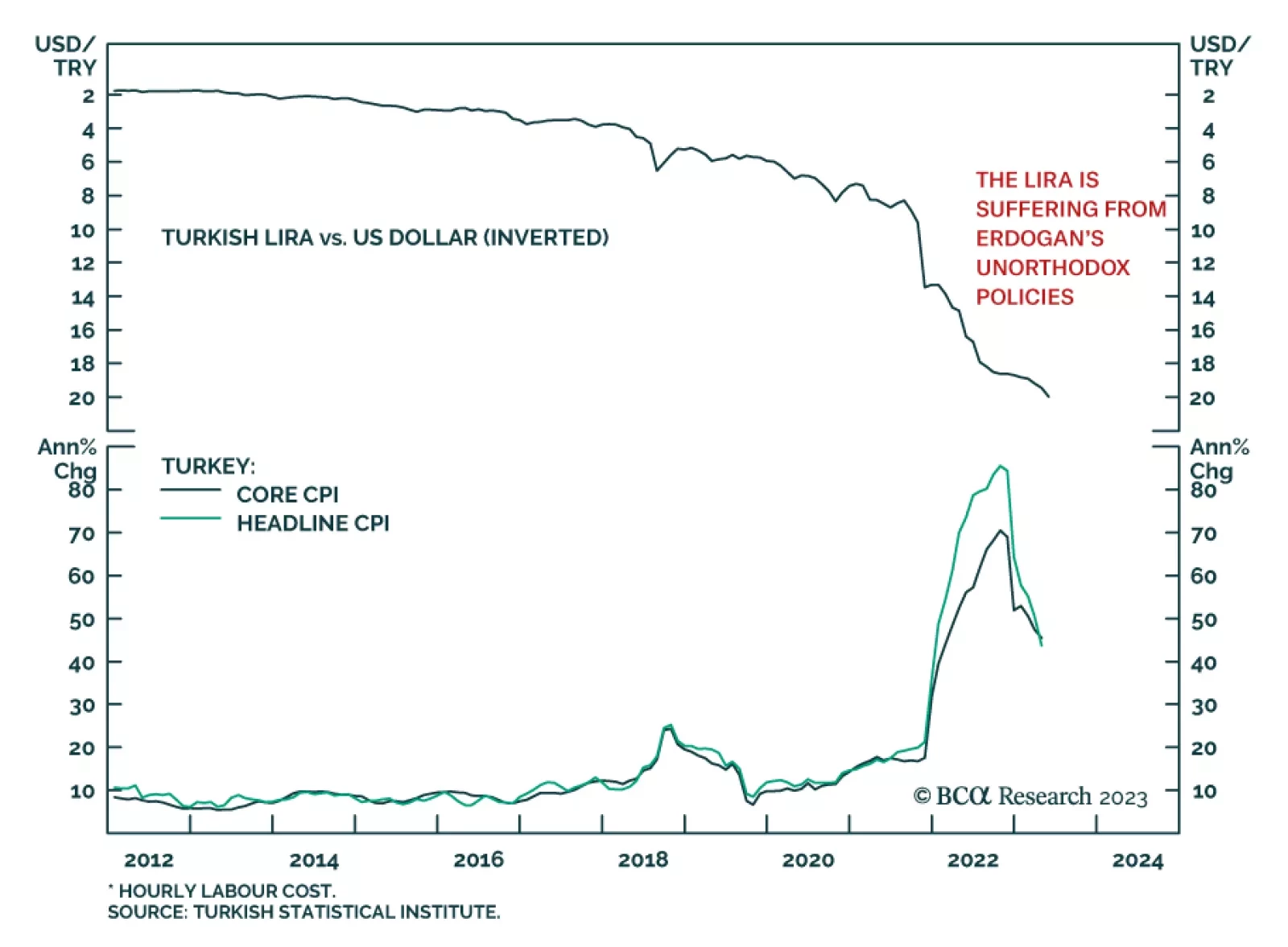

The Turkish lira hit a fresh record low on news that President Recep Tayyip Erdogan secured another five-year term following Sunday’s run-off election. Notably, despite an economic crisis (including headline CPI inflation which peaked at 86% in October) and…

A major divergence has emerged between the performance of the S&P500 and the US equal-weighted stock index. Even though the S&P500 index has been grinding higher, the US equal-weighted index has failed to rally. Such a pronounced decoupling…

According to BCA Research’s US Bond Strategy service Treasury yields will remain rangebound until the unemployment rate starts to rise. However, yields are now near the top-end of that trading range, making this a good entry point to initiate long duration…

Now that the French pension reforms have been passed, President Macron’s focus will be on the international stage. Where are the risks and opportunities for French assets created by this pivot?

The Reserve Bank of New Zealand hiked rates this week to 5.5%. There are many reasons to expect that to be the last rate hike for this cycle – a development that is positive for New Zealand bonds but bearish for the New Zealand dollar.