Inflation/Deflation

A look at how US bond yields responded to yesterday’s strong economic data and this morning’s soft inflation print.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

In Section I, we reiterate why a soft economic landing remains improbable in the US. Some reasonable estimates of the level of excess savings point to their depletion in a year’s time, but other estimates indicate a much earlier end point. We interpret this evidence, as well as other indicators, as pointing to an earlier rather than later US recession if the current stance of monetary policy is maintained or tightened further. In Section II, we provide an update on the US housing market. We acknowledge that permanent site residential structures investment may begin to contribute positively to US real GDP growth if the recent pickup in housing starts is sustained. But the recent housing market data is symptomatic of a negative housing supply shock that is far more consistent with the “no landing” economic scenario than the “soft landing” scenario that stocks are betting on. We continue to recommend that investors position their portfolios conservatively.

The combination of a global manufacturing recession and tight/tightening policy is raising a red flag for global non-TMT stocks. In China, households are entering a liquidity trap, and deflationary pressures are heightening. Authorities need to reduce interest rates considerably and allow the currency to depreciate. By doing so, China will export its deflation to the rest of the world.

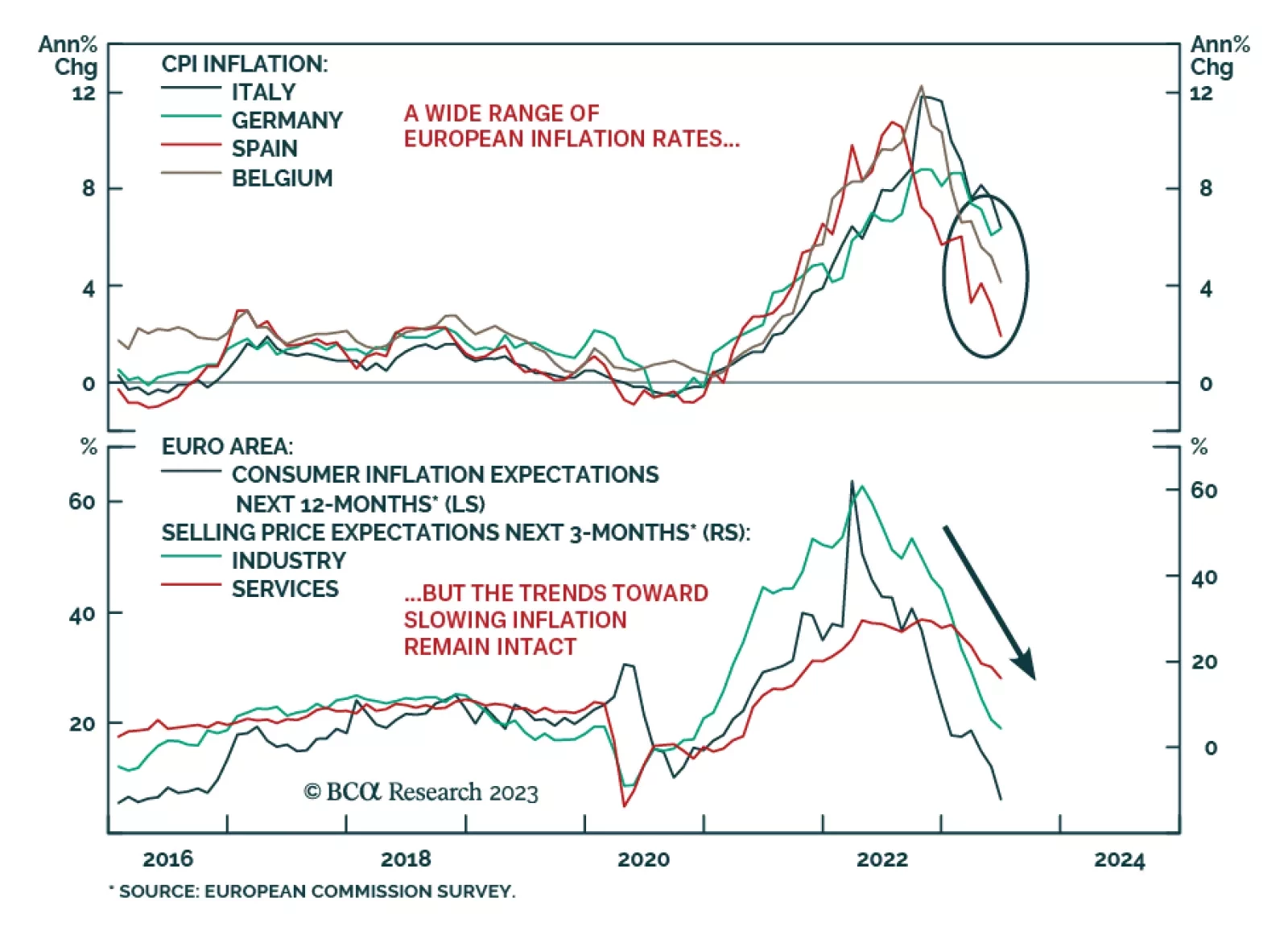

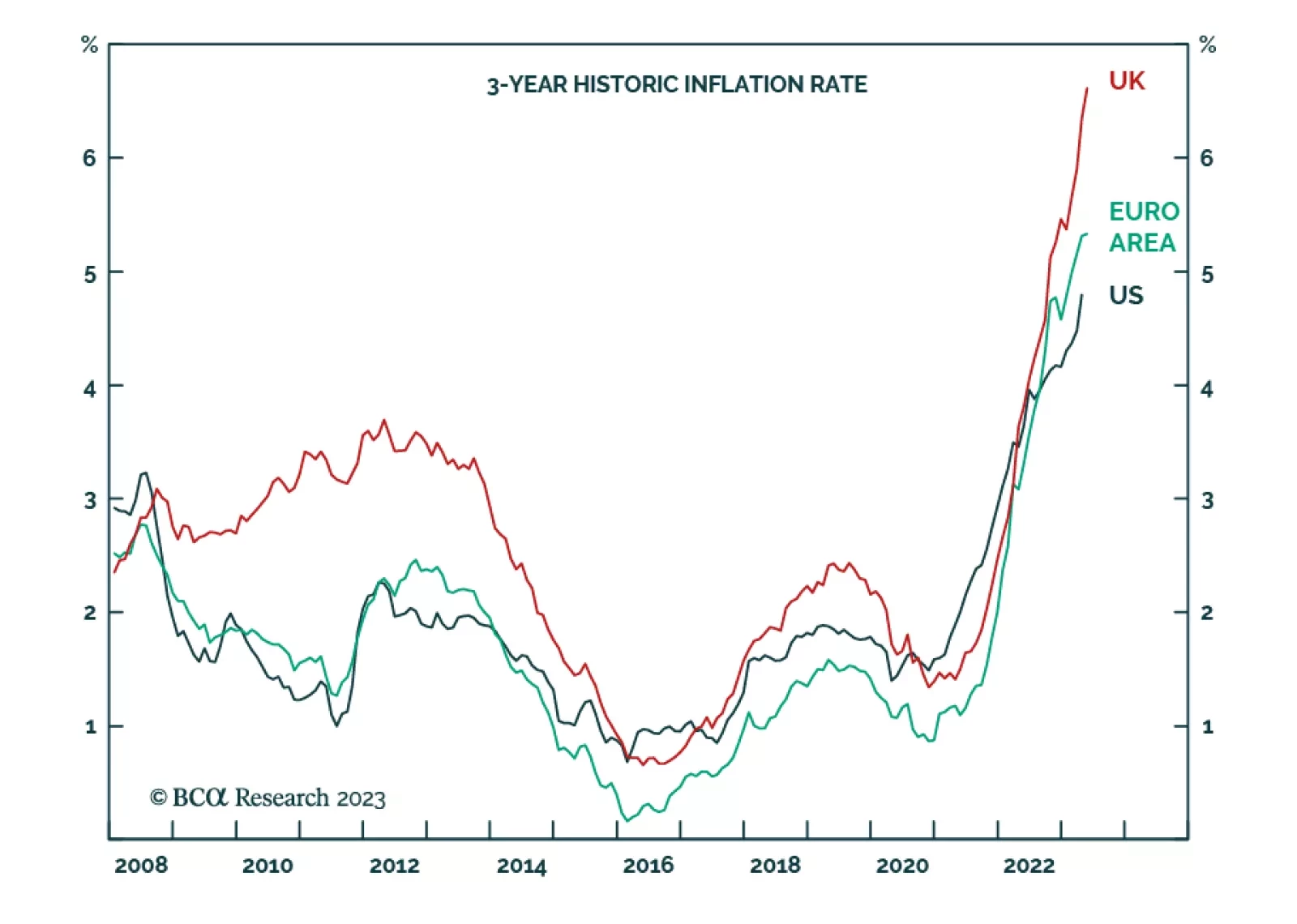

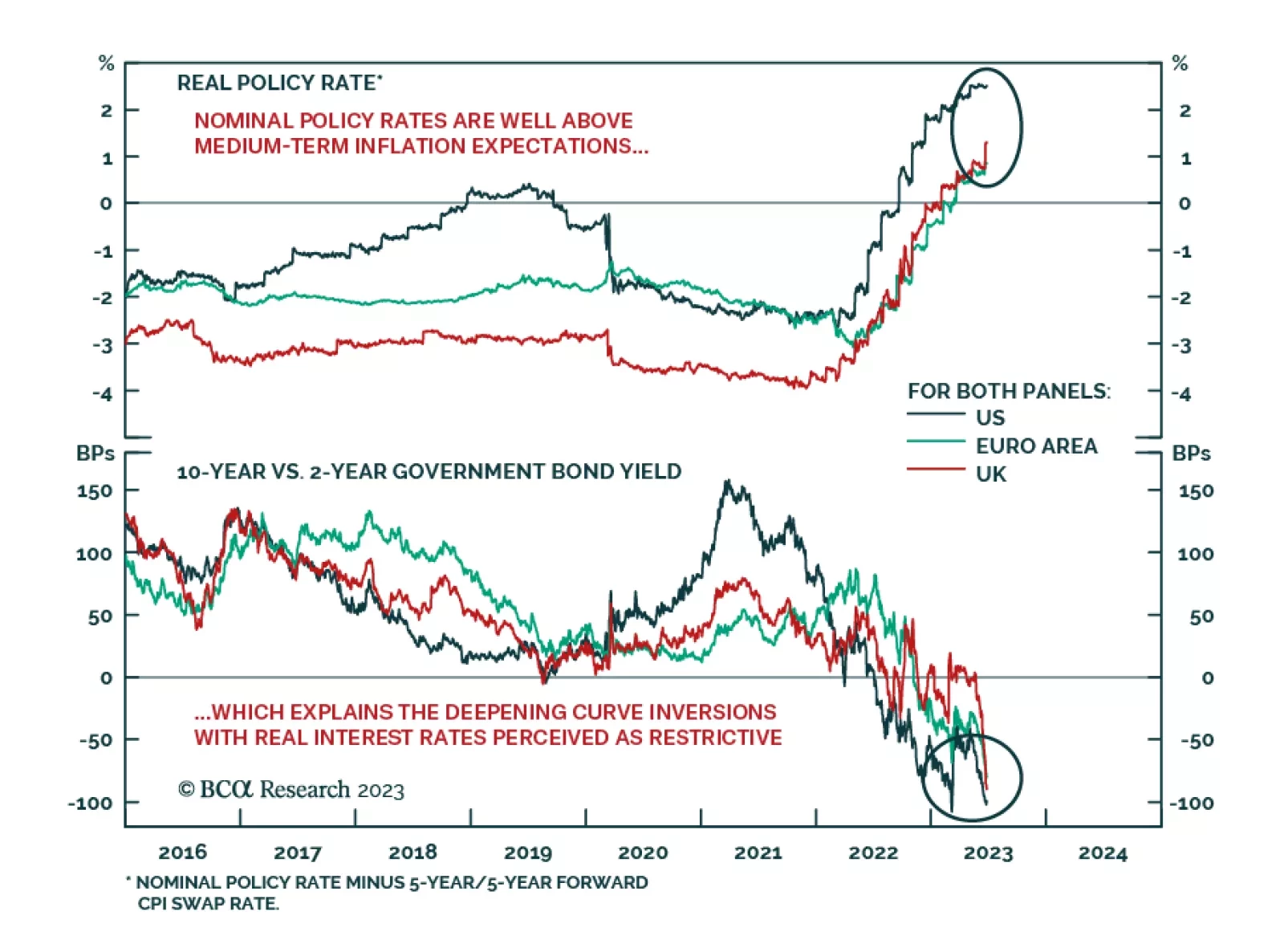

The market does not grasp the implied depths of recessions that will be needed to prevent inflation expectations from un-anchoring. Among the major economies, the most vulnerable to a deep recession is the UK. We explain why, and some investment implications. Plus: the yen is a rebound candidate, while Japanese equities are a reversal candidate.