Inflation/Deflation

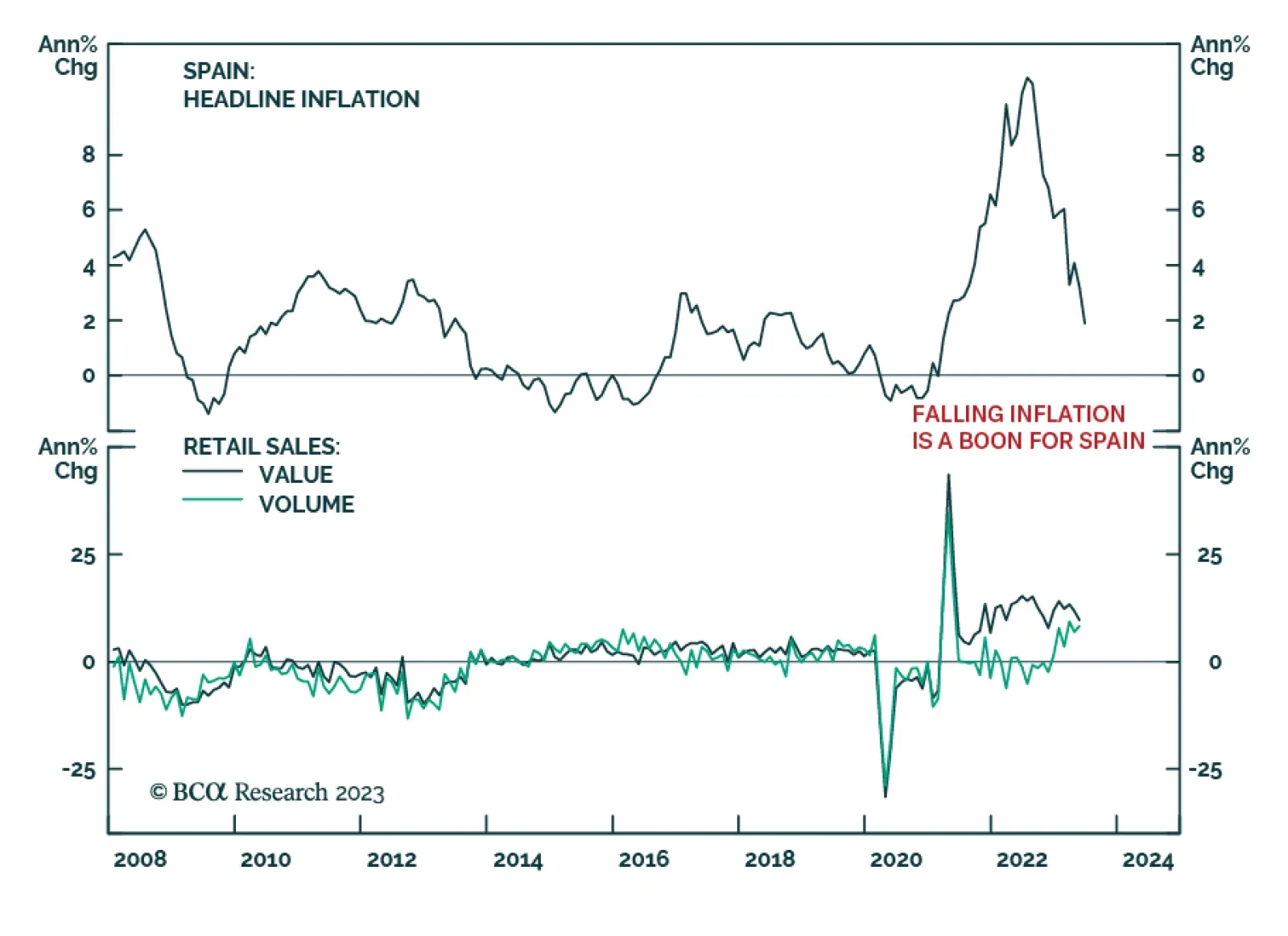

Spain is holding a general election this Sunday and the country is likely to veer to the right. Will this shift threaten European unity and herald a new period of tensions in the Eurozone?

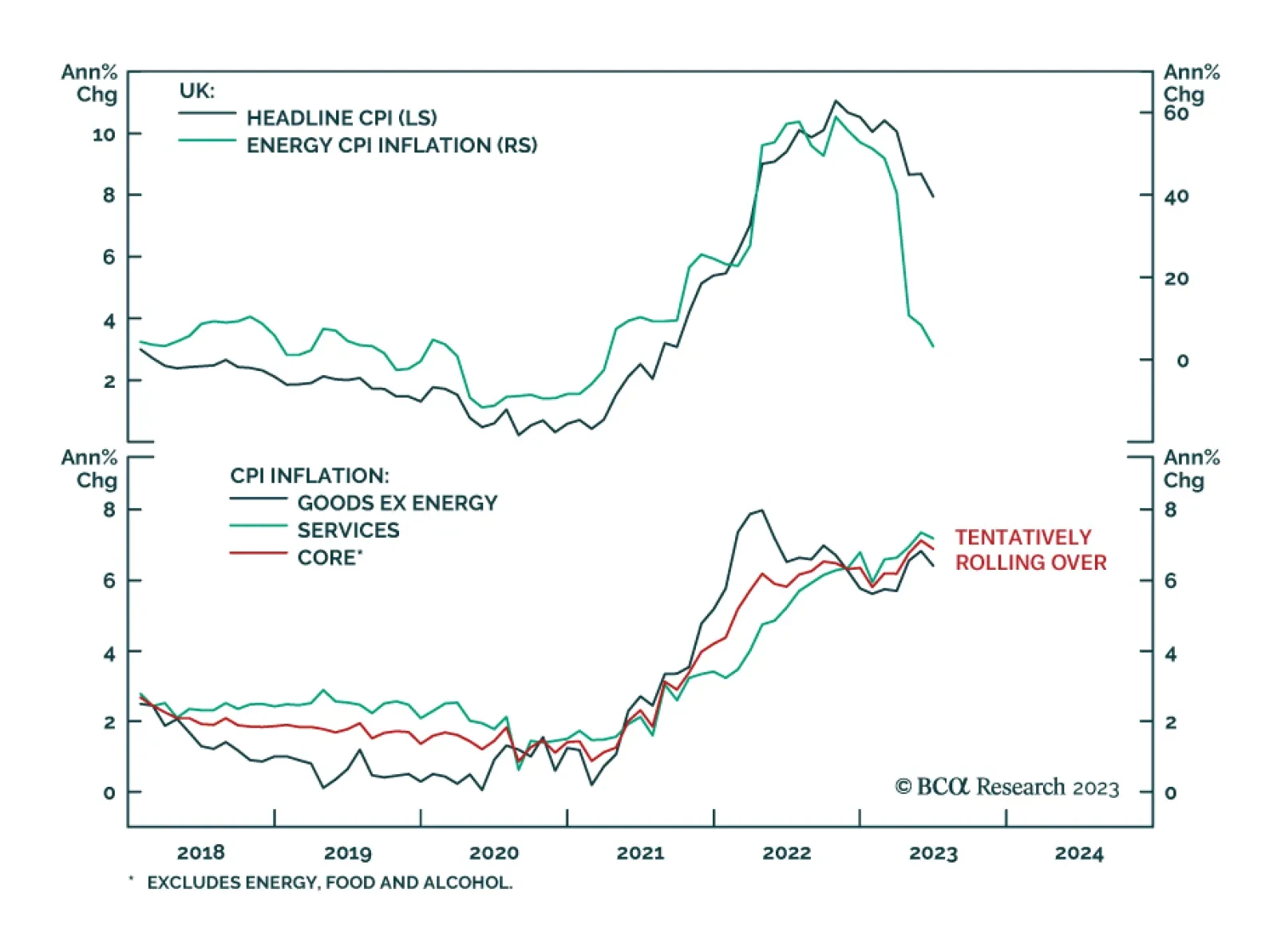

In this report, we dissect which markets have broken out and which ones have not, and reflect what this entails for our global macro view. Also, we analyze how the S&P 500 has been taking its cues from a change in the inflation trend. Yet, inflation dynamics are complex, and a falling inflation rate does not mean that the inflation menace has been eliminated.

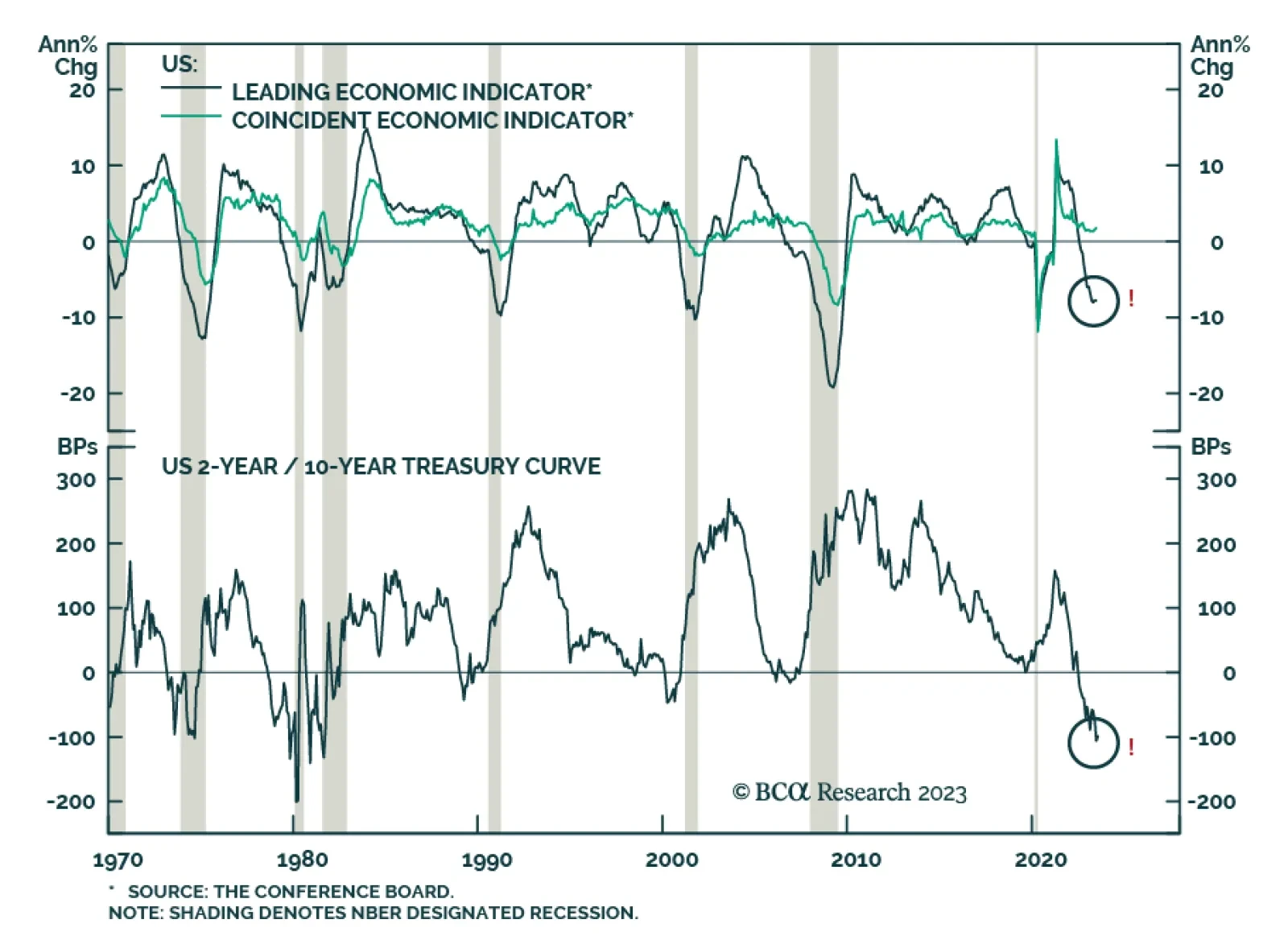

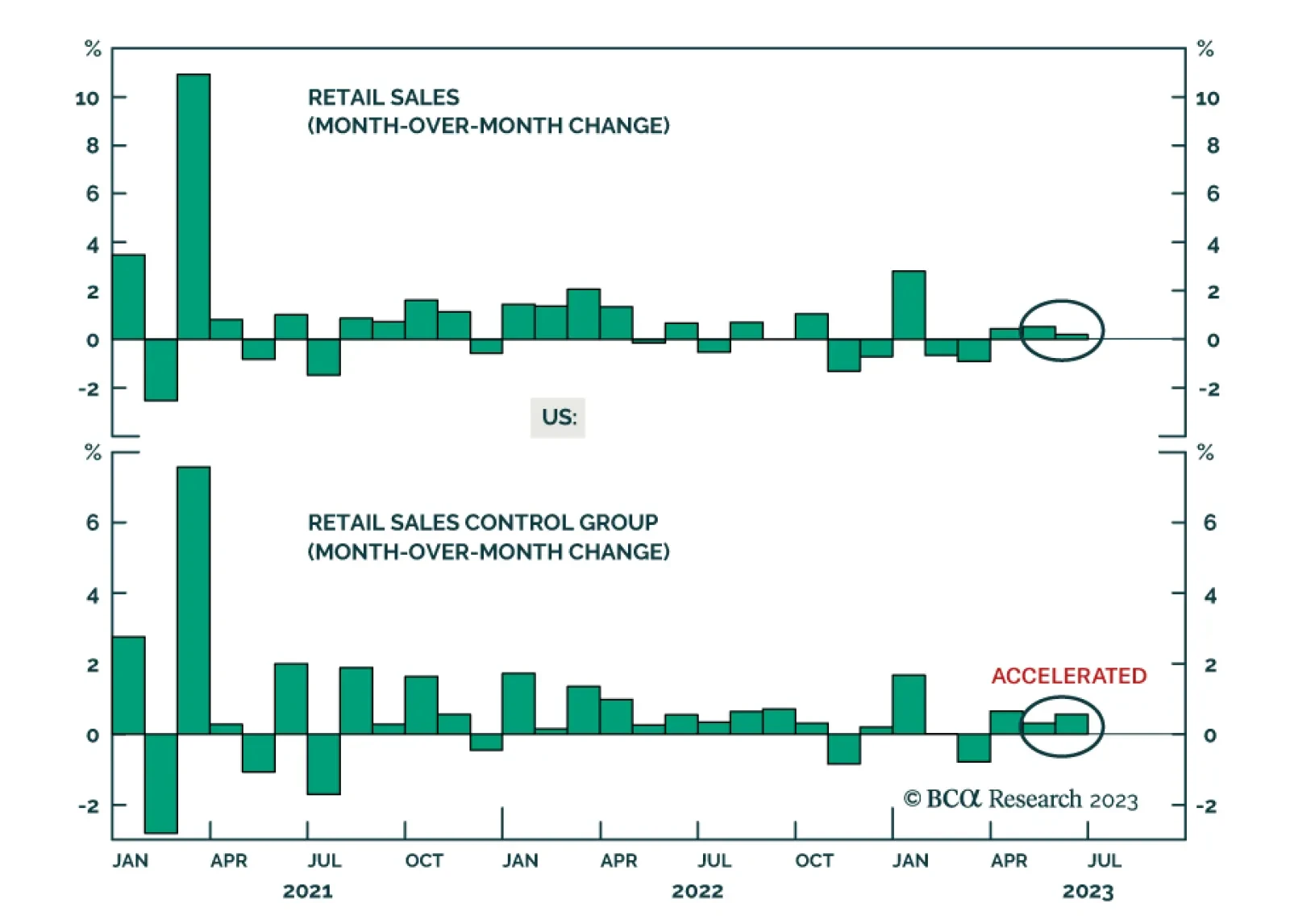

In recent months, the European and US economies have greatly diverged, with the Euro Area massively disappointing while the US has surprised to the upside. Can this dichotomy continue or is it Europe’s turn to shine?