Inflation/Deflation

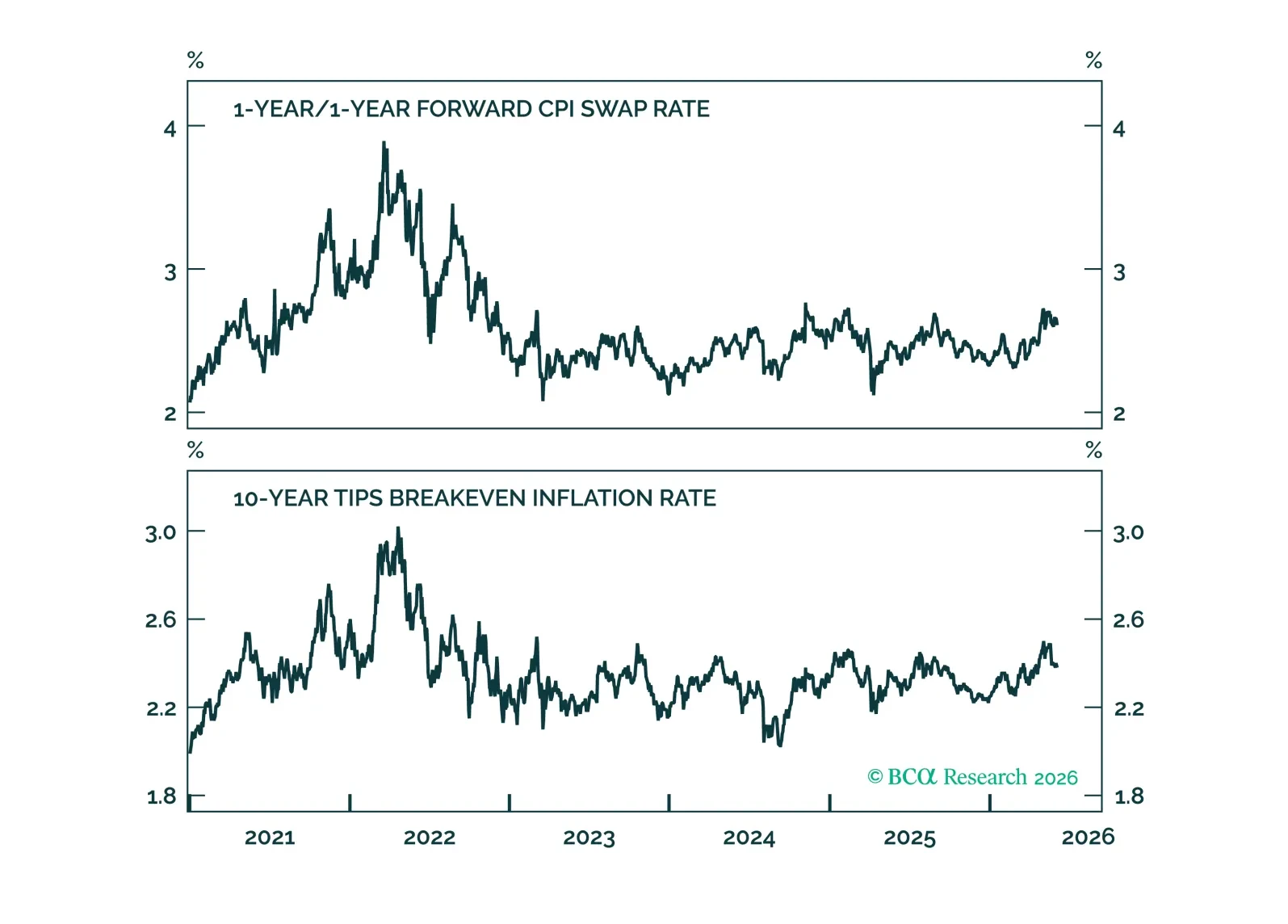

Most Fed and pundit assessments of inflation expectations are overly narrow, focusing too much on long-term market-based measures. We favor a more qualitative approach that asks whether the inflation outlook is influencing household and business decision making.

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

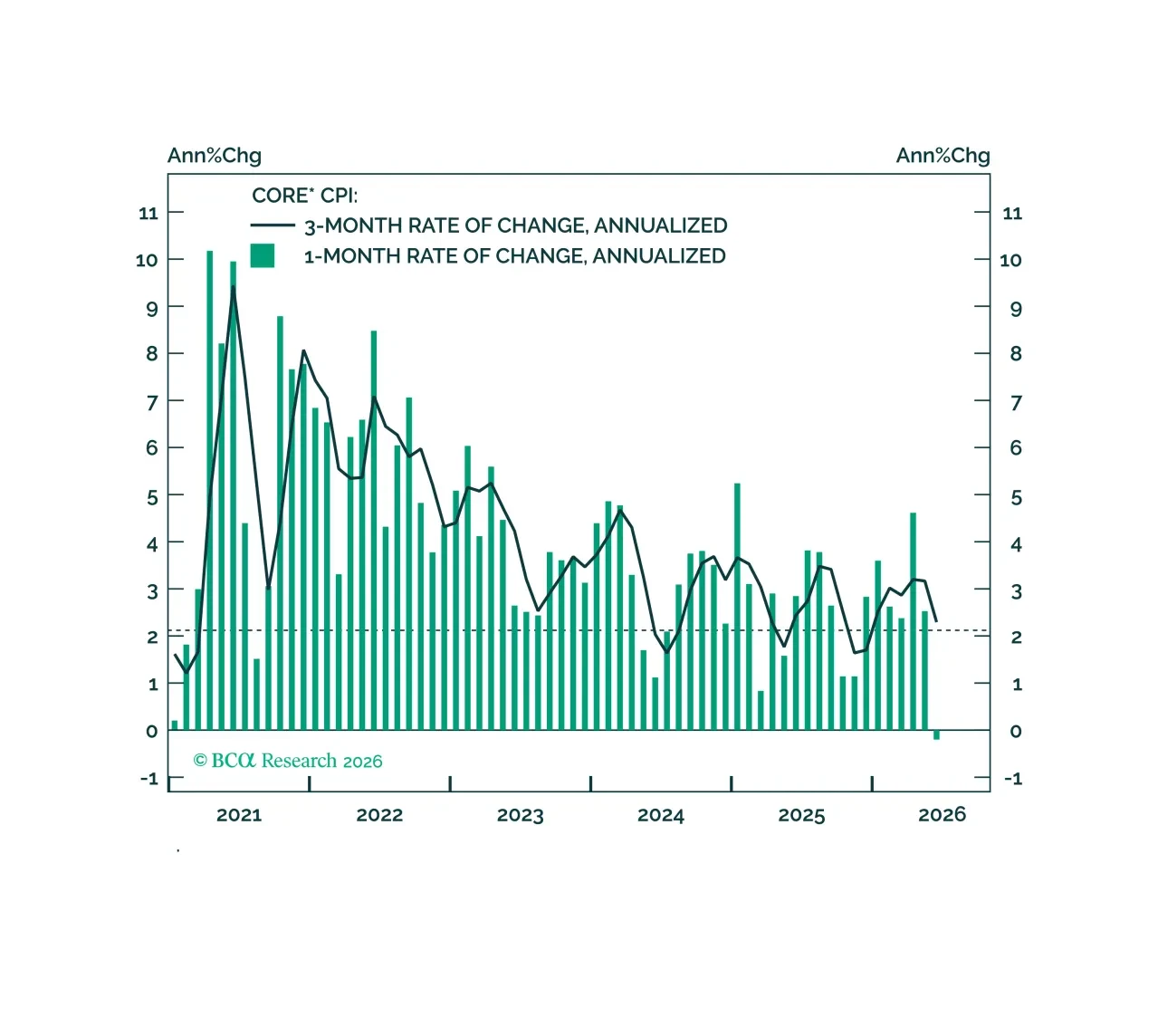

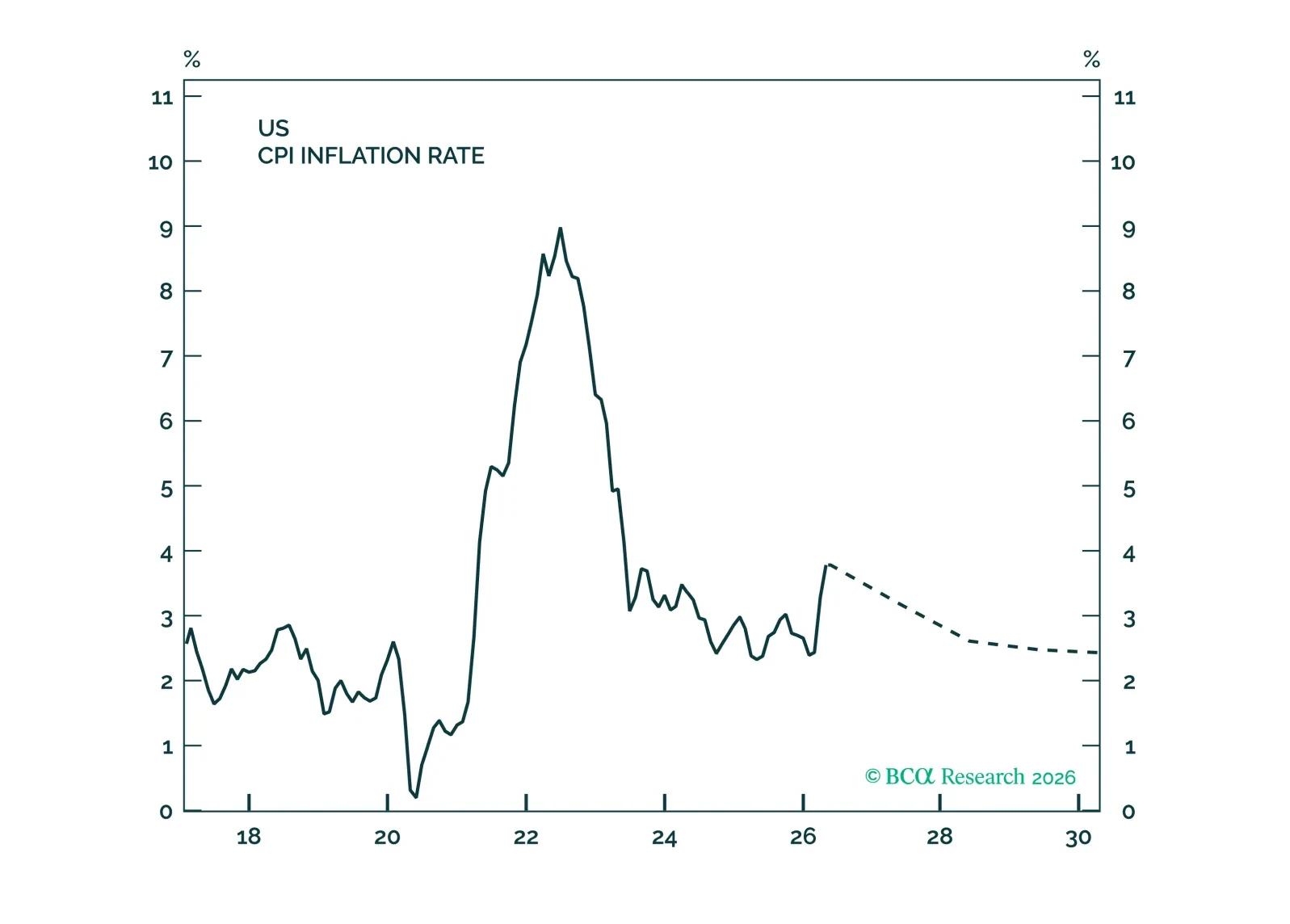

June’s low CPI reading rules out a July rate hike, but September is still on the table.

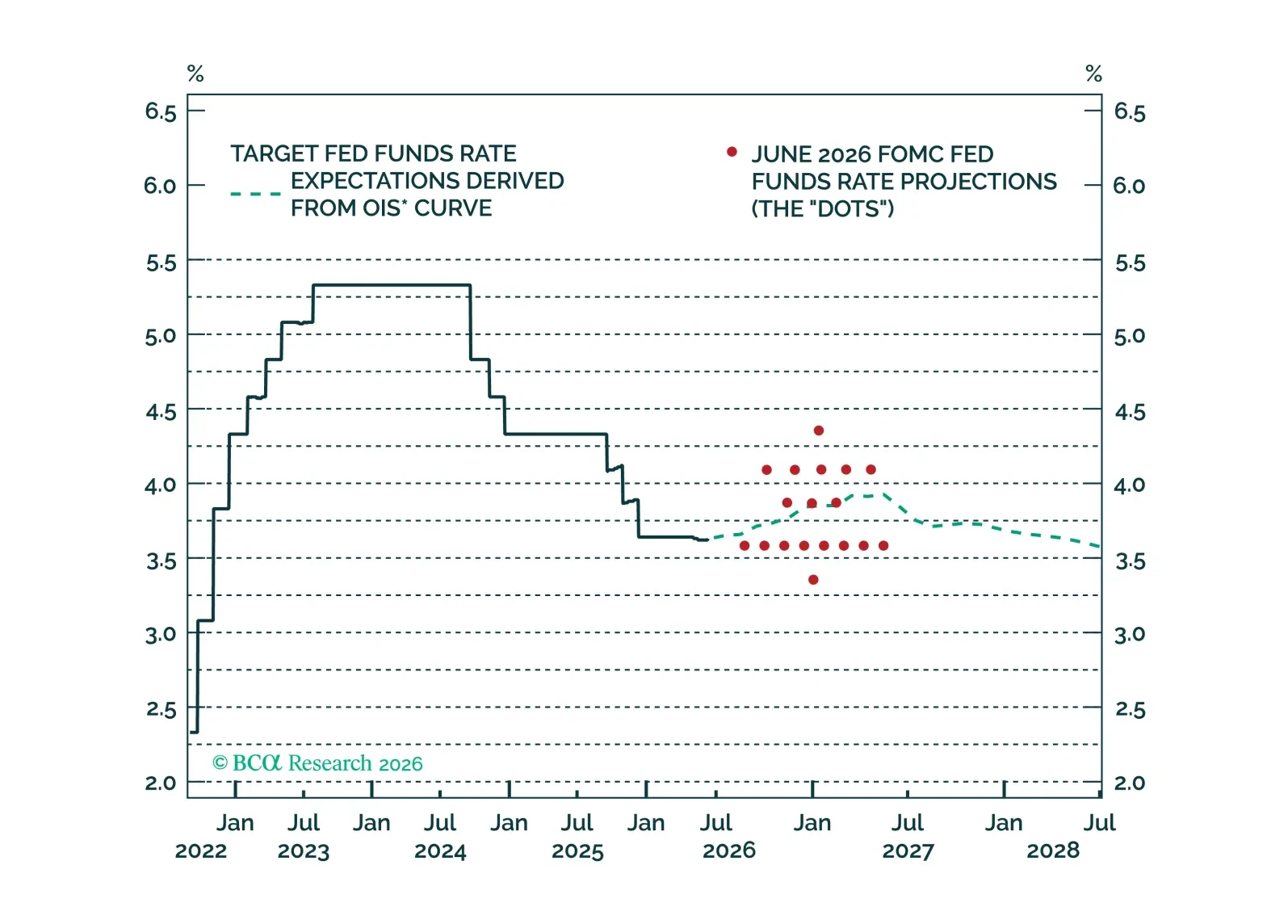

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.

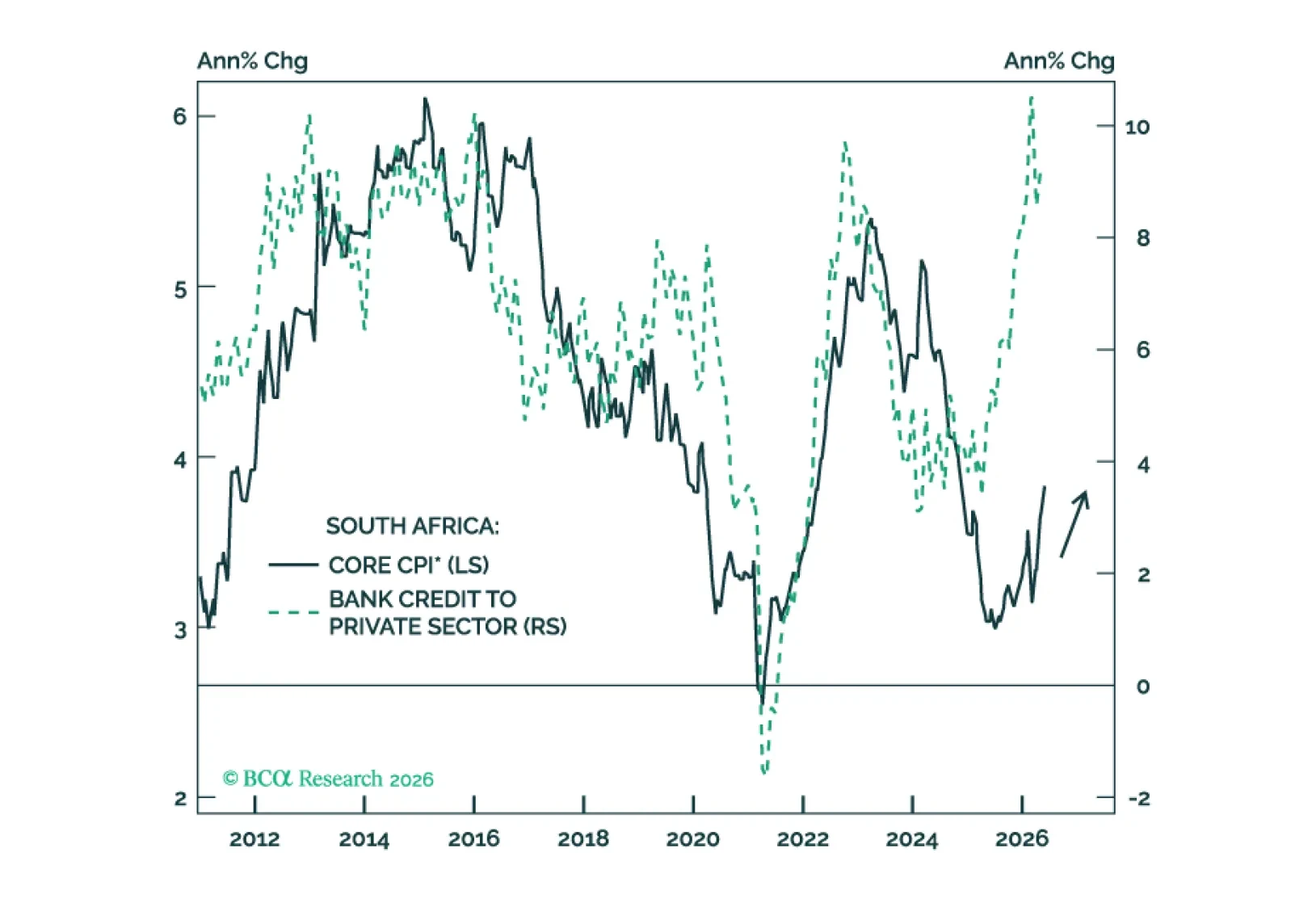

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

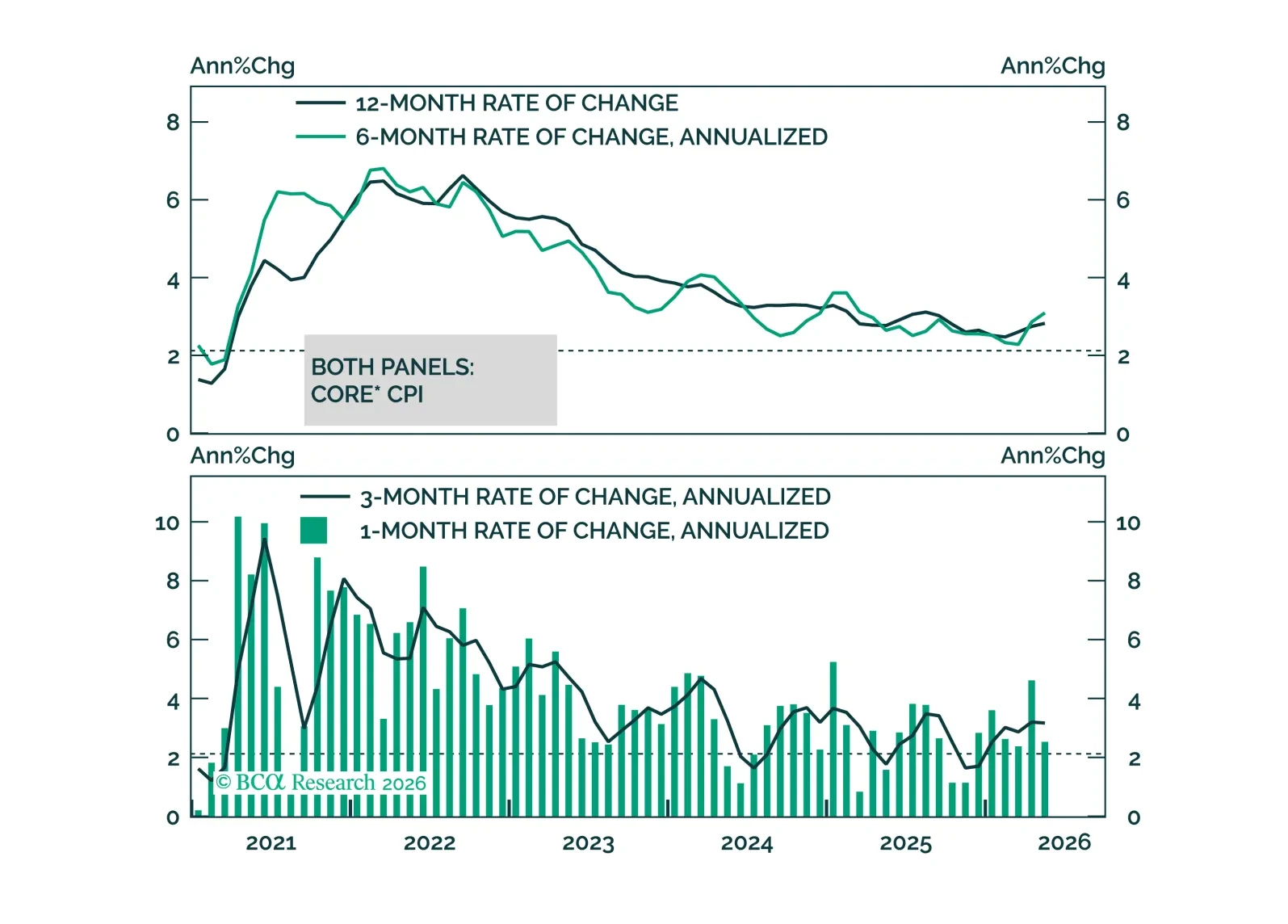

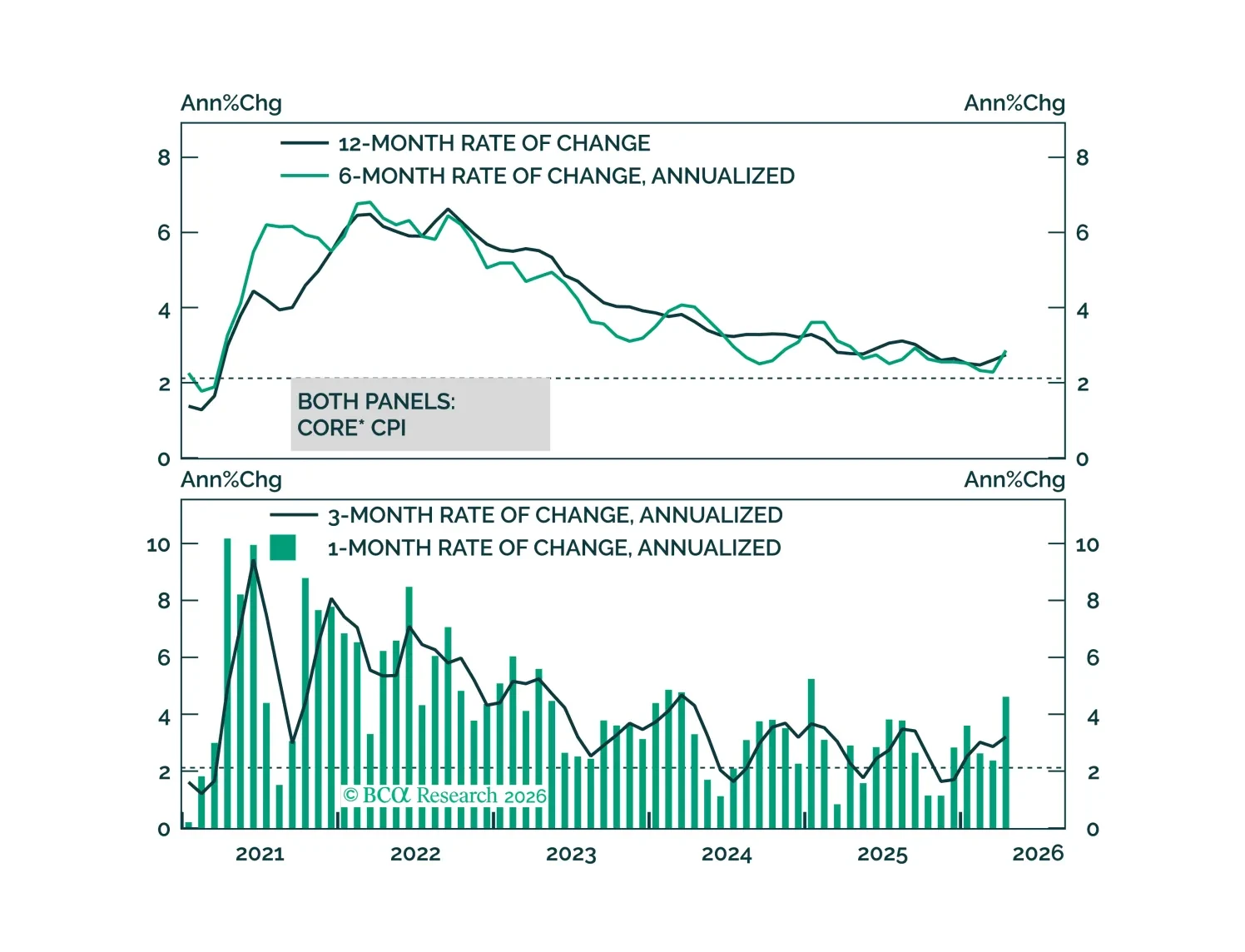

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

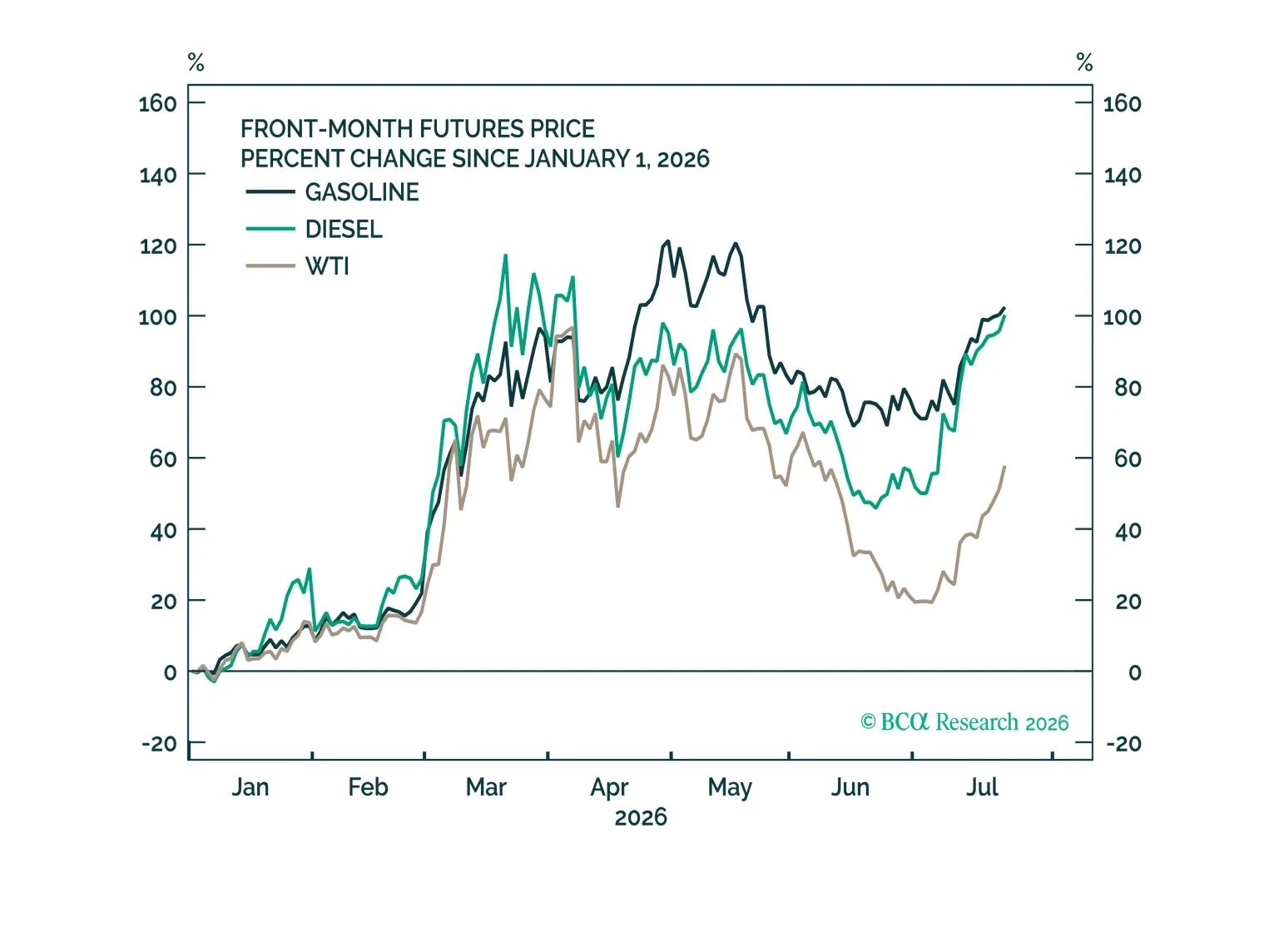

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.