Industrials

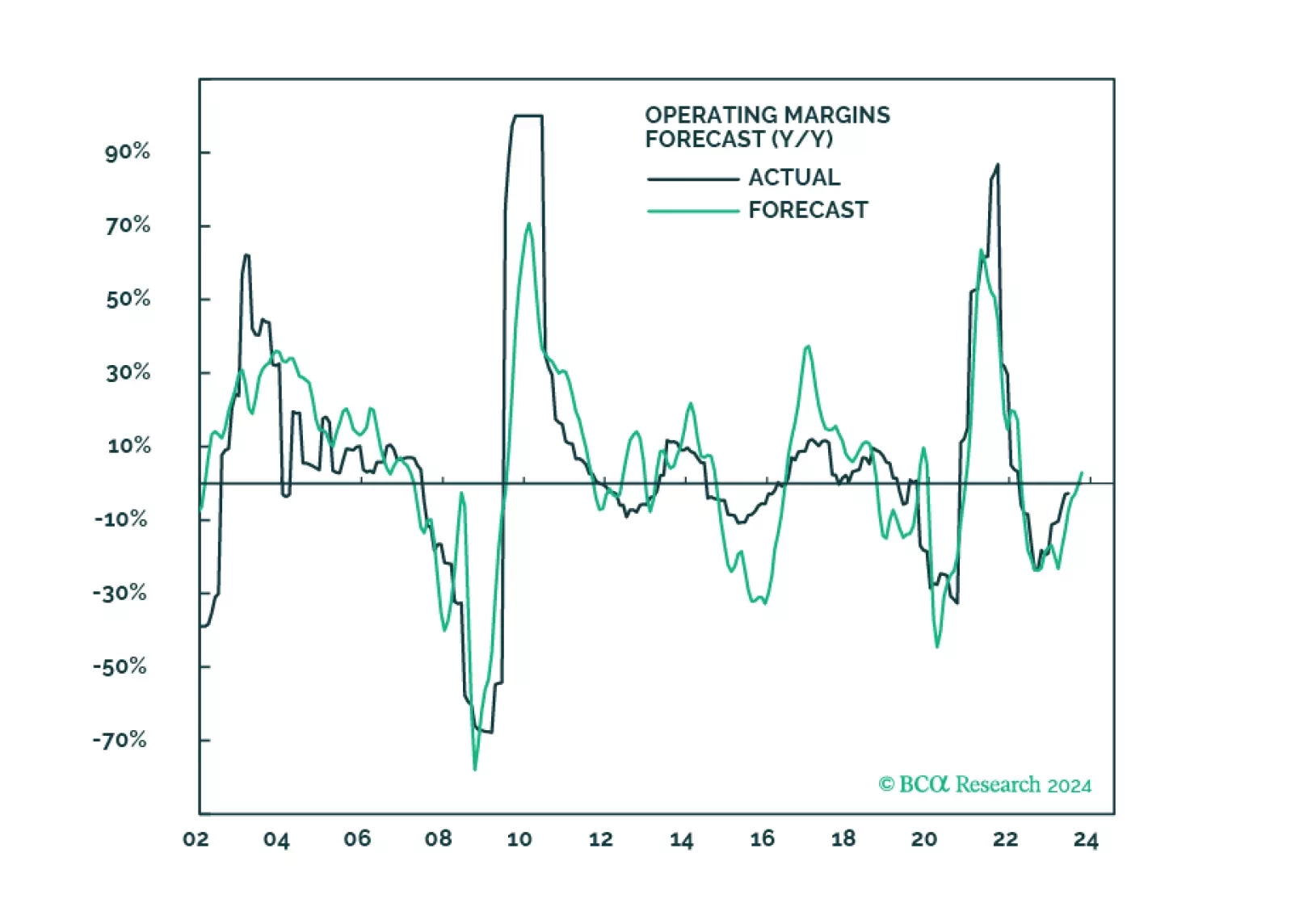

Reported earnings for Q4-2023 were rather underwhelming and prone to issues that we have identified over the past few months: Growth is concentrated in just a few sectors and companies, while the profitability of a broad swath of the equity market is under pressure from disinflation and sticky wages. Consumers are still spending, but less enthusiastically than before, while a switch from spending on services to spending on goods is in its very early innings. Downgrade Consumer Staples to neutral.

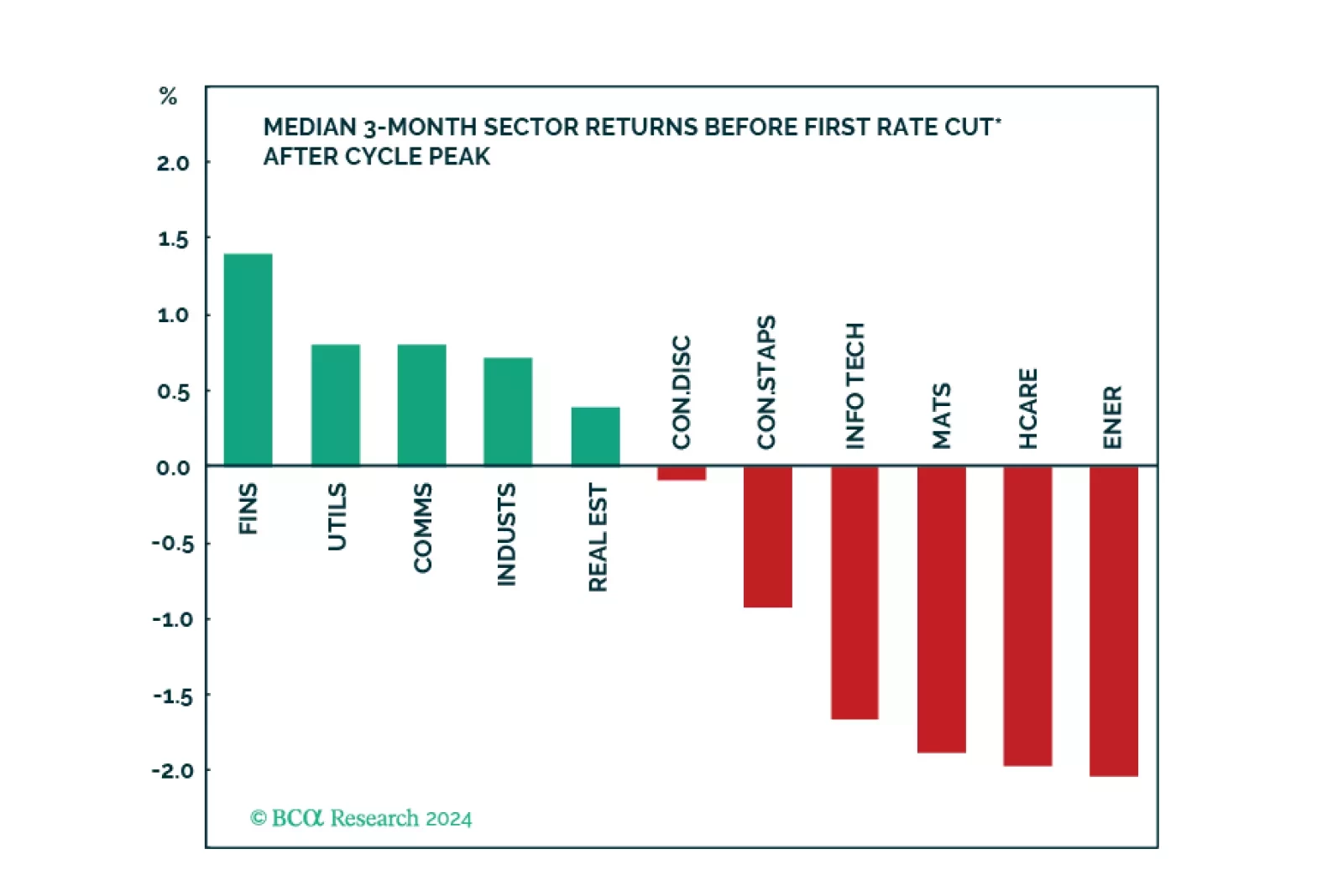

We created a sector selection scorecard based on performance of sectors under various macroeconomic regimes while taking into consideration revisions to expected earnings growth and valuations in a historical context. Our total sector selection scorecard suggests overweighting defensives such as Utilities, and Consumer Staples, and underweighting cyclicals such as Consumer Discretionary, Industrials, and Financials. Considering this analysis, we have adjusted our sector positioning accordingly.

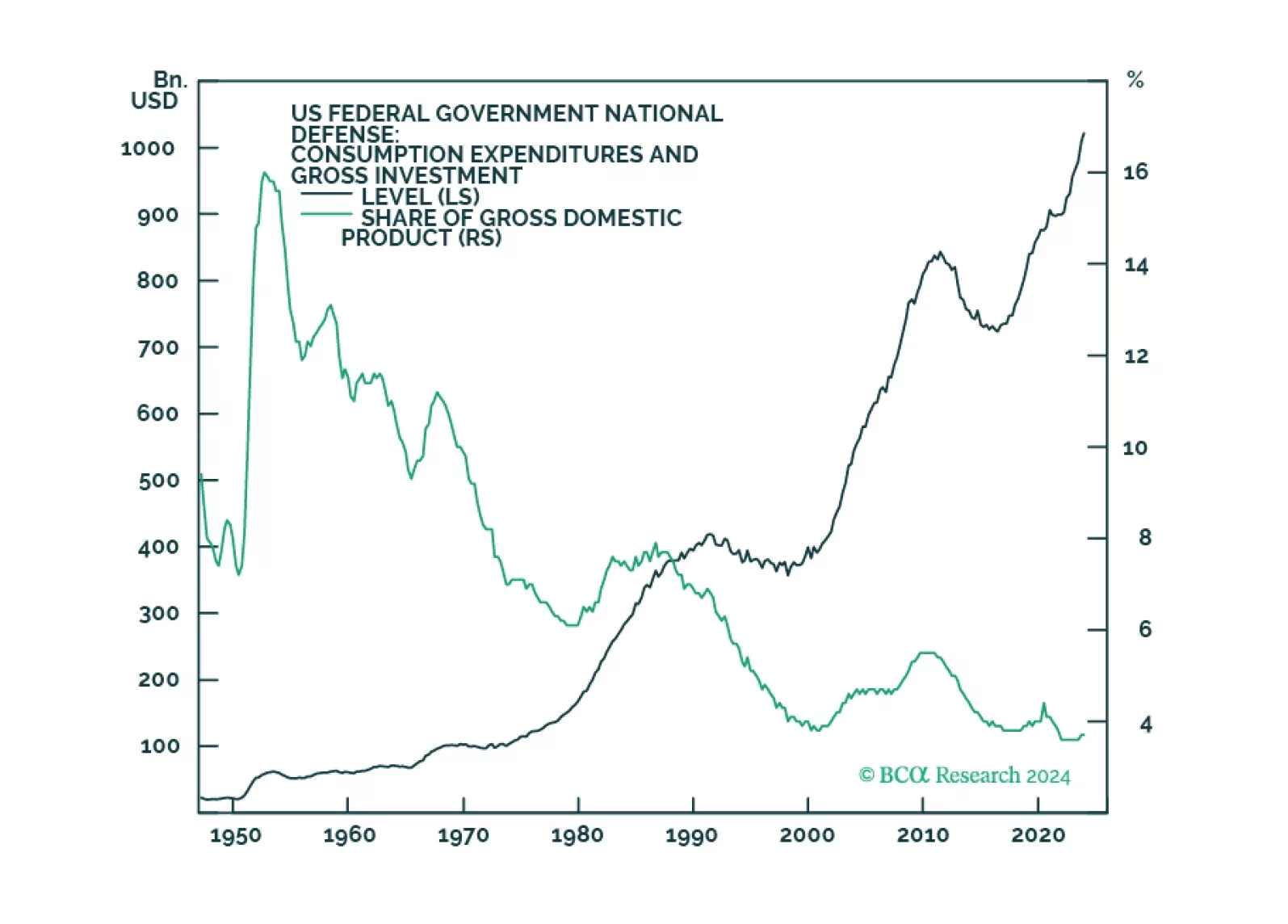

The US DoD rolled out its first-ever industrial policy designed to reverse decades of atrophy in its military-industrial complex. This left the US with diminished access to CMM commodities and supply chains, which are now dominated by China, and an industrial ecosystem to support its war-fighting mission that risks become uncompetitive. We remain long the XME and COMT ETFs to retain exposure to CMM producers and refiners. At tonight’s close, we will get long the Invesco Aerospace & Defense ETF (PPA), anticipating increased defense spending.

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Disinflation coupled with sticky wage growth is likely to result in either a second wave of inflation or layoffs and a recession. In the meantime, market expectations for sales, growth, and margins are overly optimistic and are inconsistent with macroeconomic headwinds. We recommend gradually realigning the portfolio to a more defensive stance.

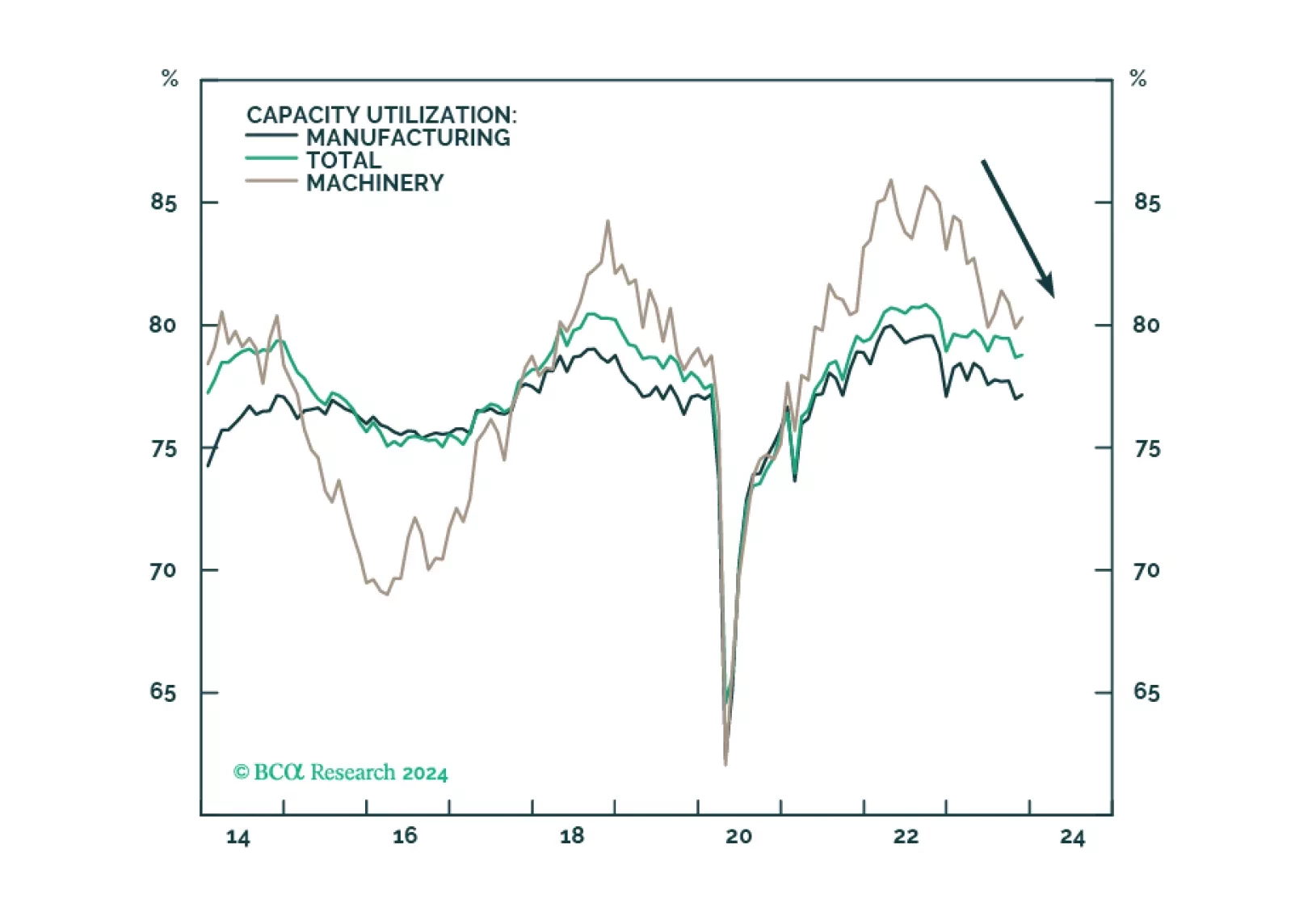

The US manufacturing renaissance, spurred on by reshoring, automation, and government spending, is running its course but progress has slowed on the back of tight monetary conditions and the manufacturing recession. The deceleration of these positive trends weighs on the outlook for the Capital Goods industry group, impeding its performance over the short term. However, we reiterate that positive long-term trends for the industry remain intact. We downgrade Capital Goods to a tactical underweight. It remains a strategic overweight.

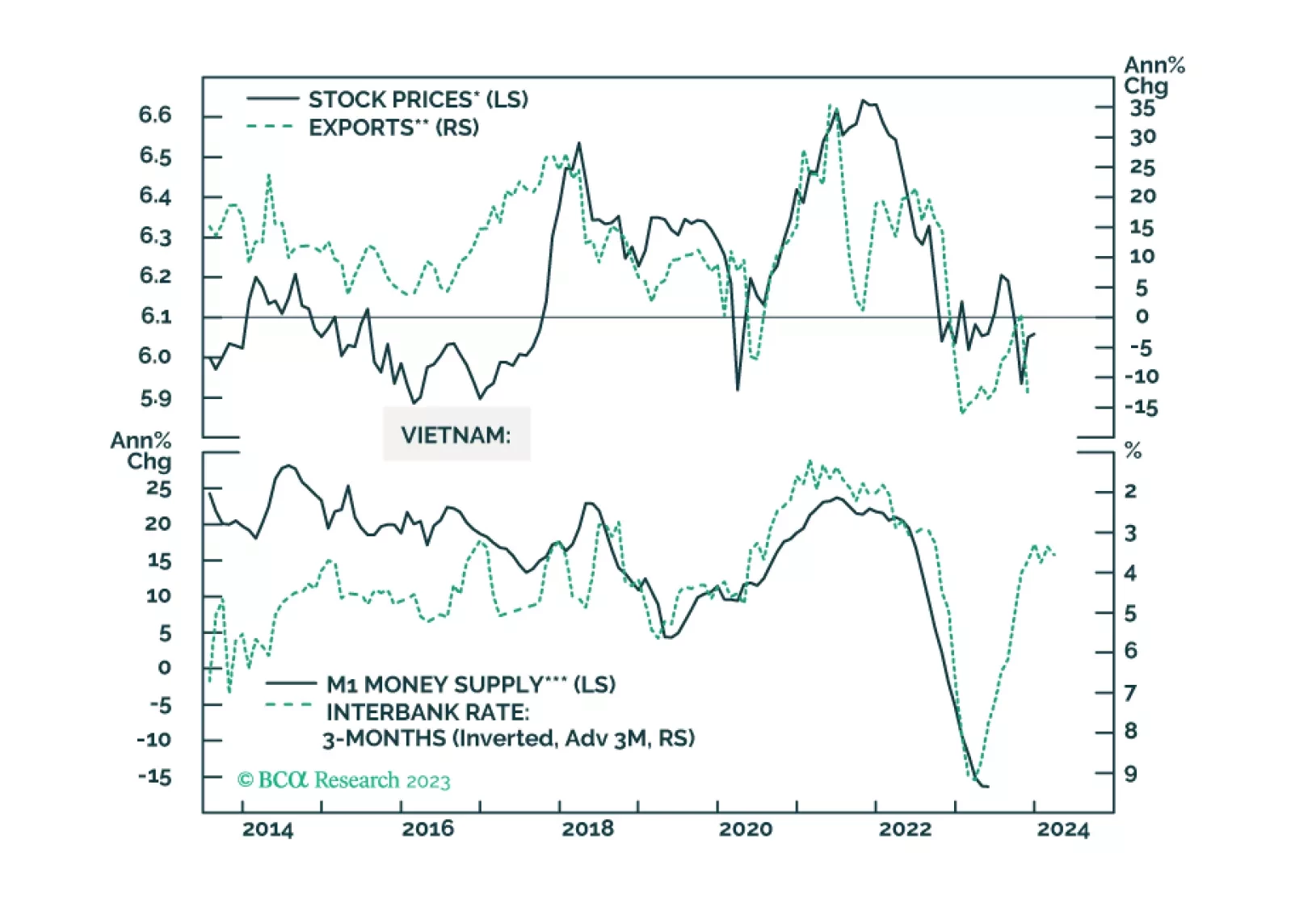

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.