Hot Topic

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

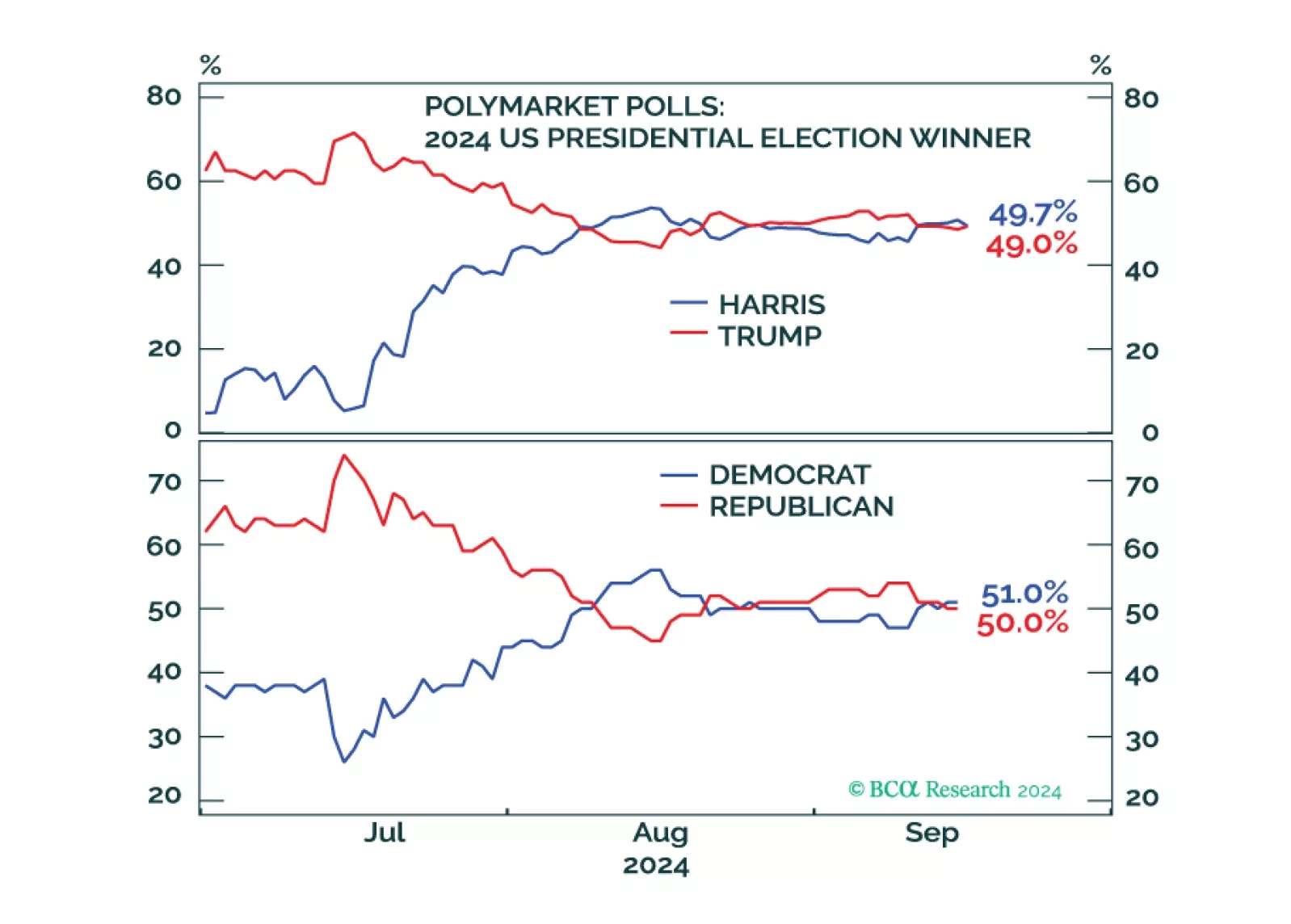

Trump may be slightly favored for the White House but the US election is still extremely close. Odds of a contested or contingent election are rising, which should cause stock market volatility. A Republican sweep should cause more volatility. Democratic gridlock is next most likely but benign for stocks in the short run.

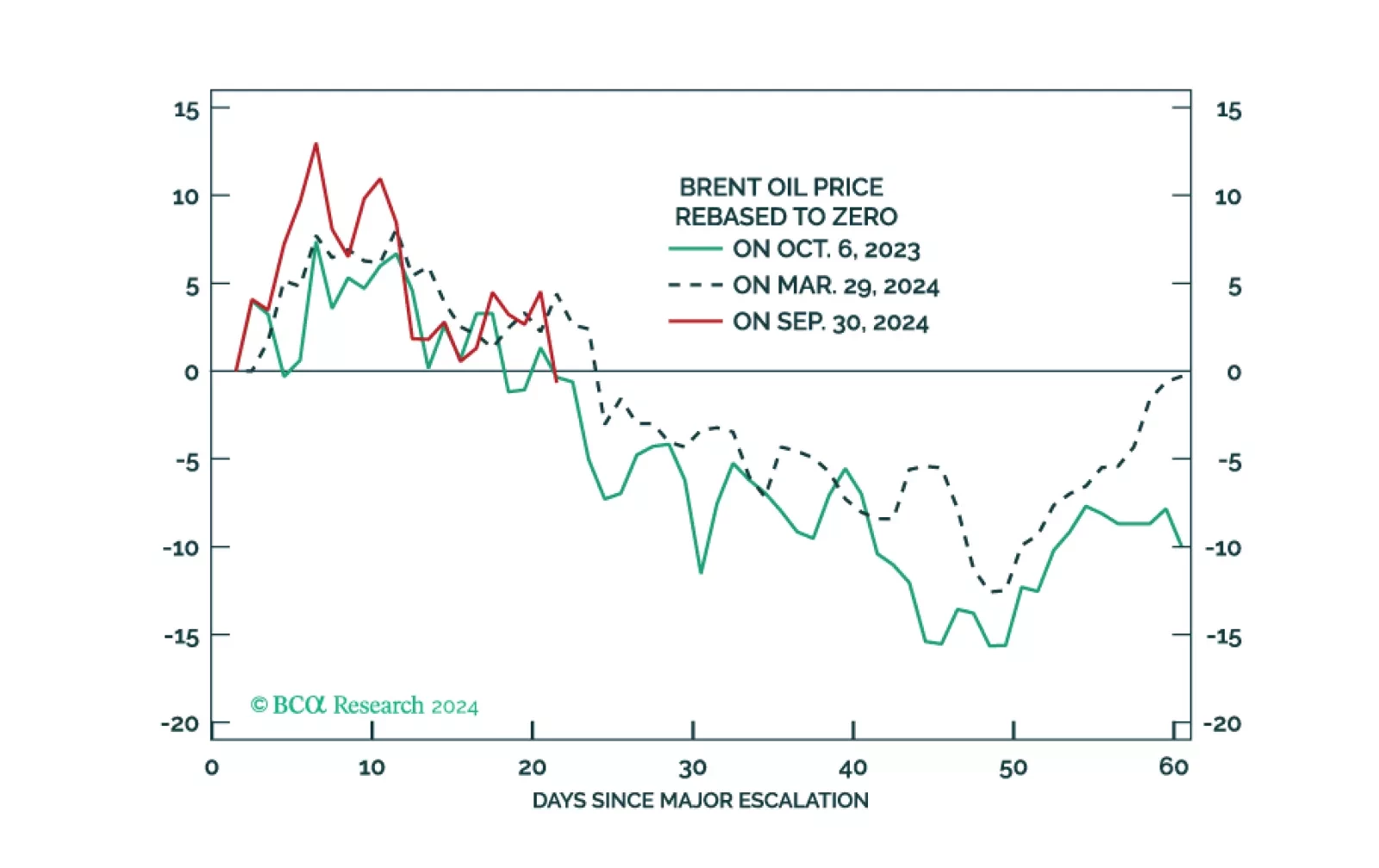

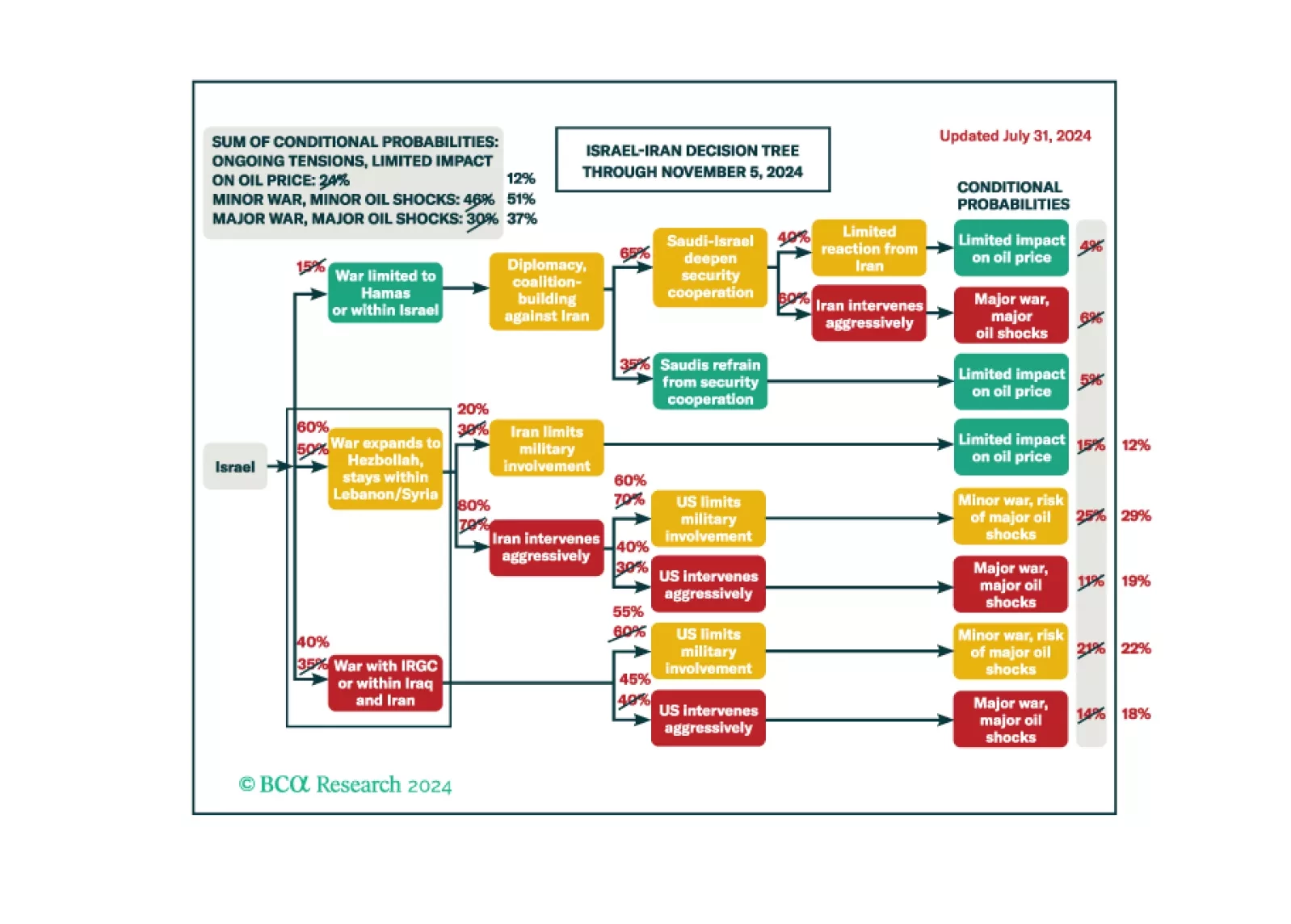

We maintain 37% odds of a major recessionary oil shock, 51% odds of minor shocks, and 12% odds of no shocks.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.

The Nifty Fifty bull market of the early seventies was a mania in which investors got carried away chasing after a subset of prized growth stocks. While we do not think the Magnificent Seven stocks are in a bubble, they do have some parallels with the growth stars of 50 years ago.

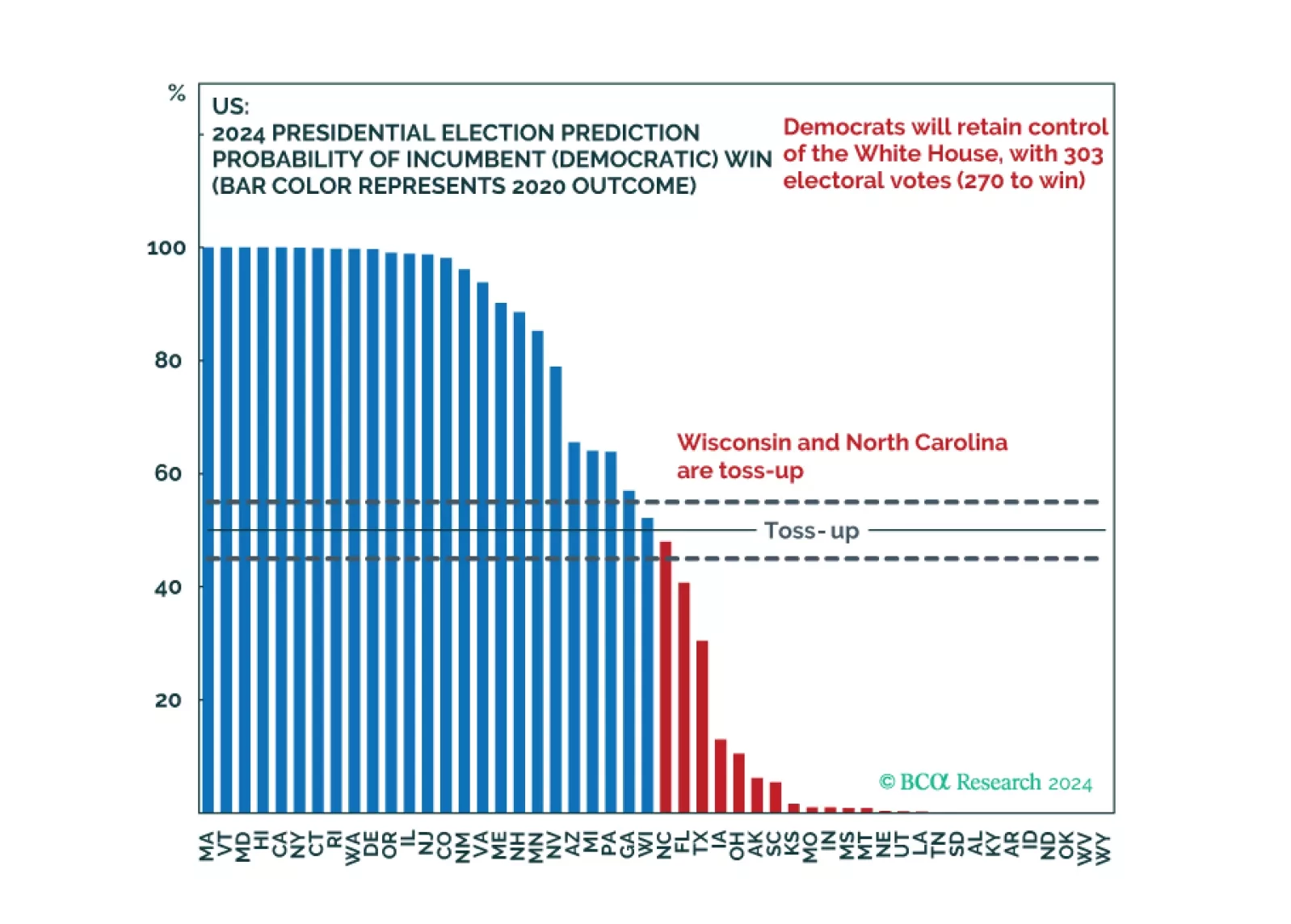

Our quant model shows Democrats winning the election at a 56% probability, with 303 electoral college votes. But swing state economies are slowing and Democrats’ odds in Michigan fell. Trump can win with Georgia, Michigan, plus one other state. Neither the Fed nor China’s stimulus should reduce one’s odds of a Republican upset.

Markets are rallying on Fed rate cuts and China stimulus but there will also be October surprises ahead of the US election, which Trump could still win. Russia’s conflict with the West is escalating and the Middle East is destabilizing further. Investors should favor US bonds but they should add some risk in emerging markets in response to China’s policy turn.

As we head into a more turbulent macroeconomic and geopolitical period, investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable region, and not so dependent on the US or China. Hence, we are introducing the Global Political Capital Index as a way to integrate these factors into a score that can help narrow down the countries with the best and worst abilities to deal with the incoming challenges.

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.