Hot Topic

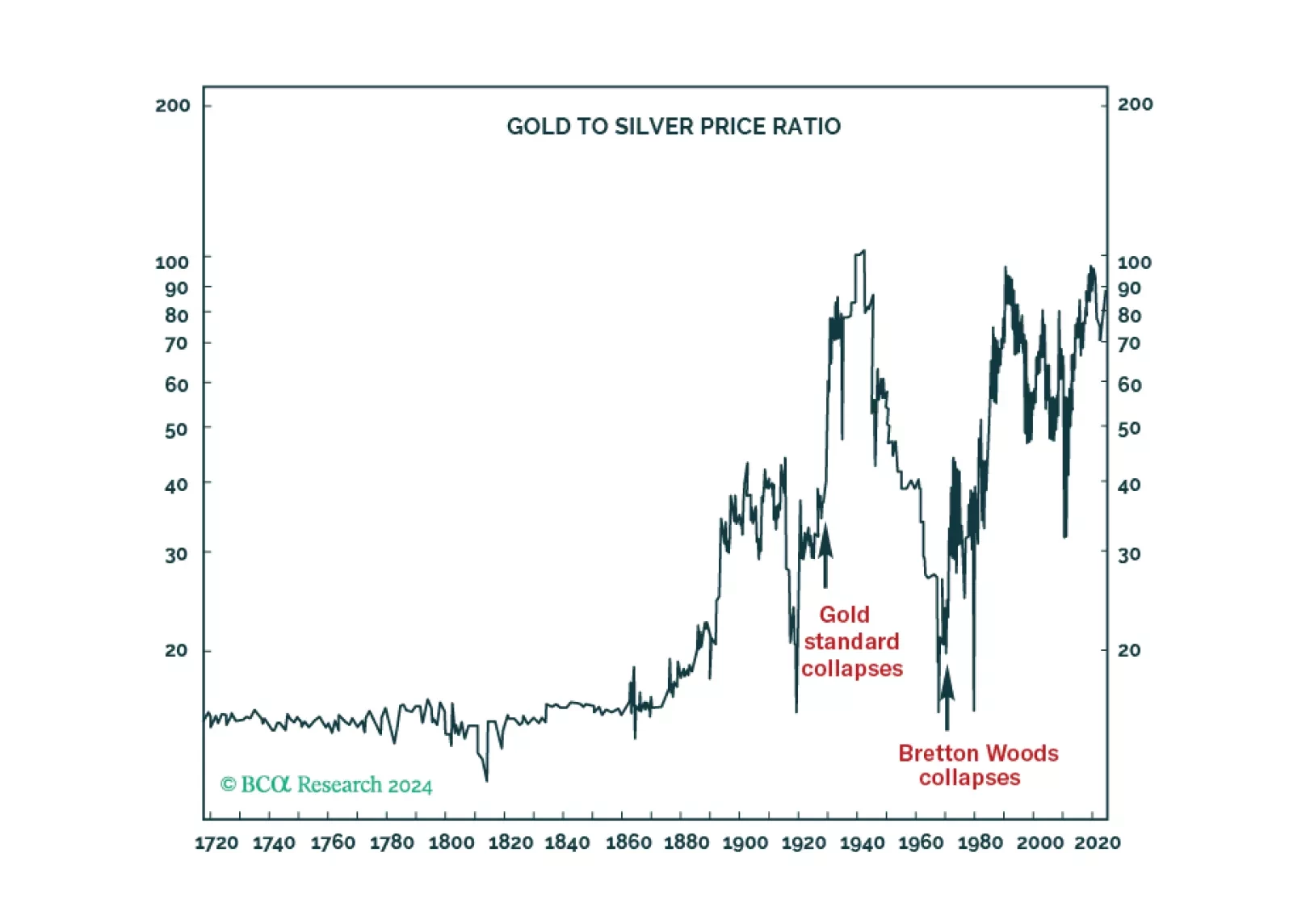

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

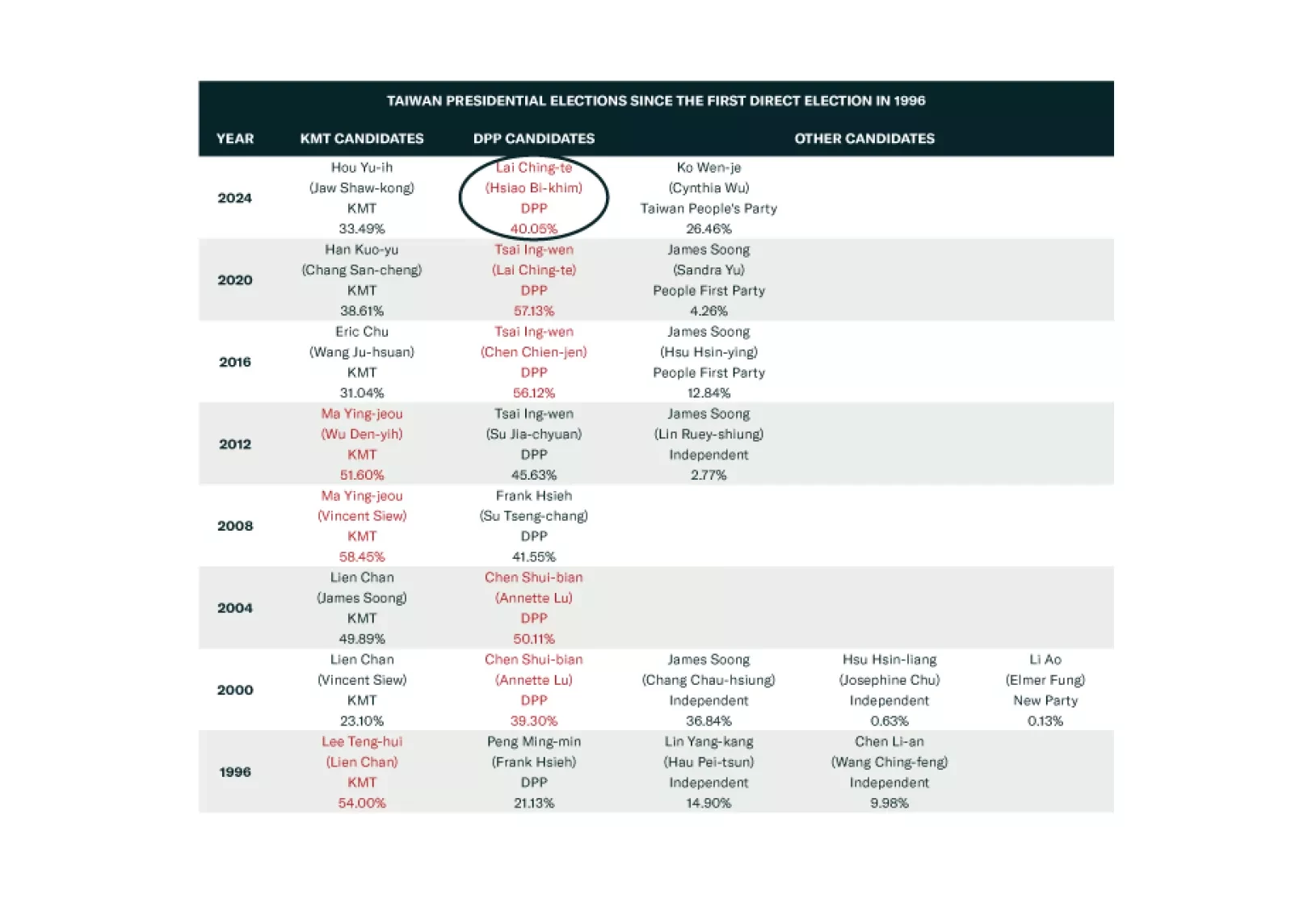

Taiwan’s election will lead to serious Chinese military and economic pressure but not full-scale war. War is a long-term concern. Investors should short TWD-USD.

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

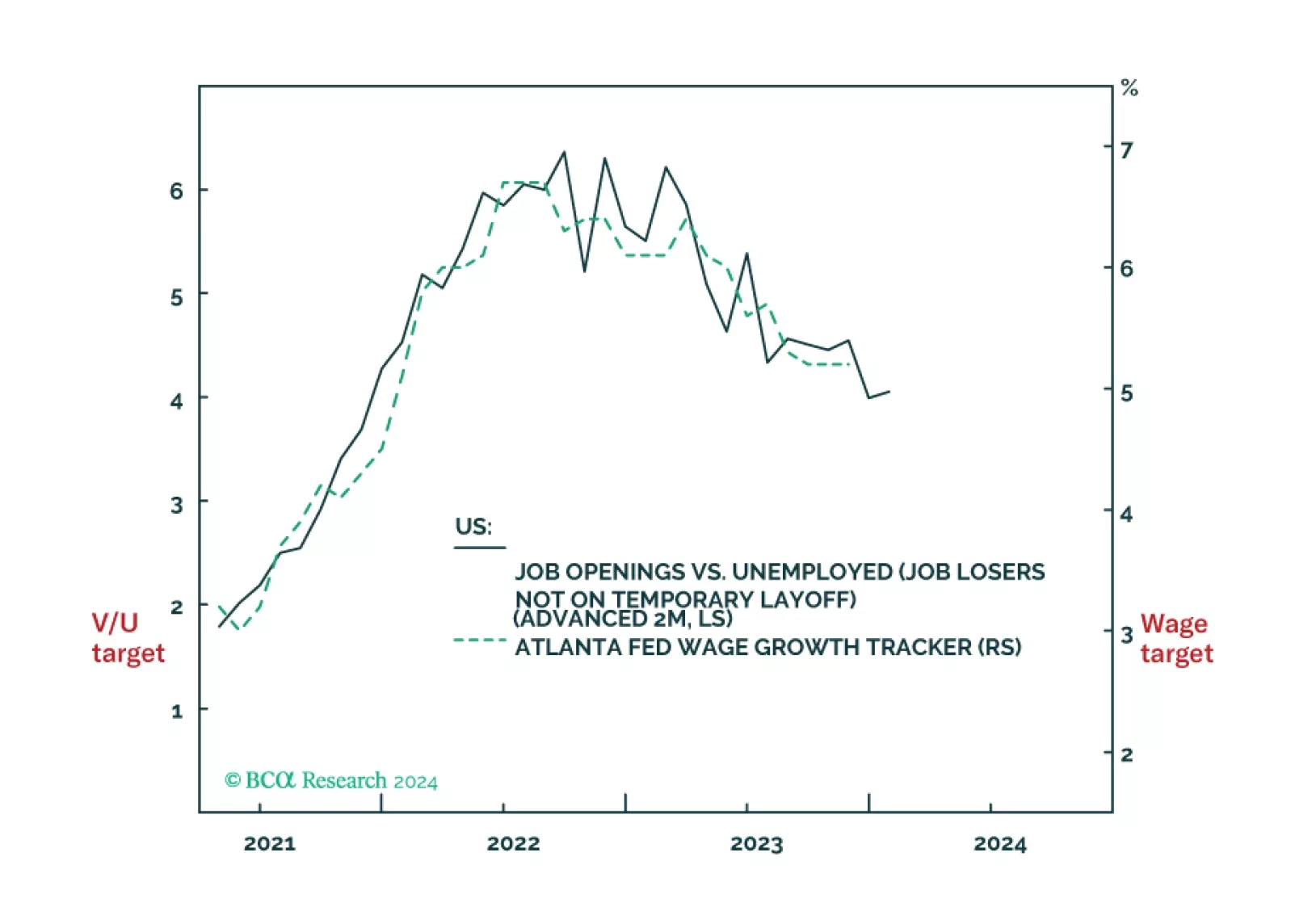

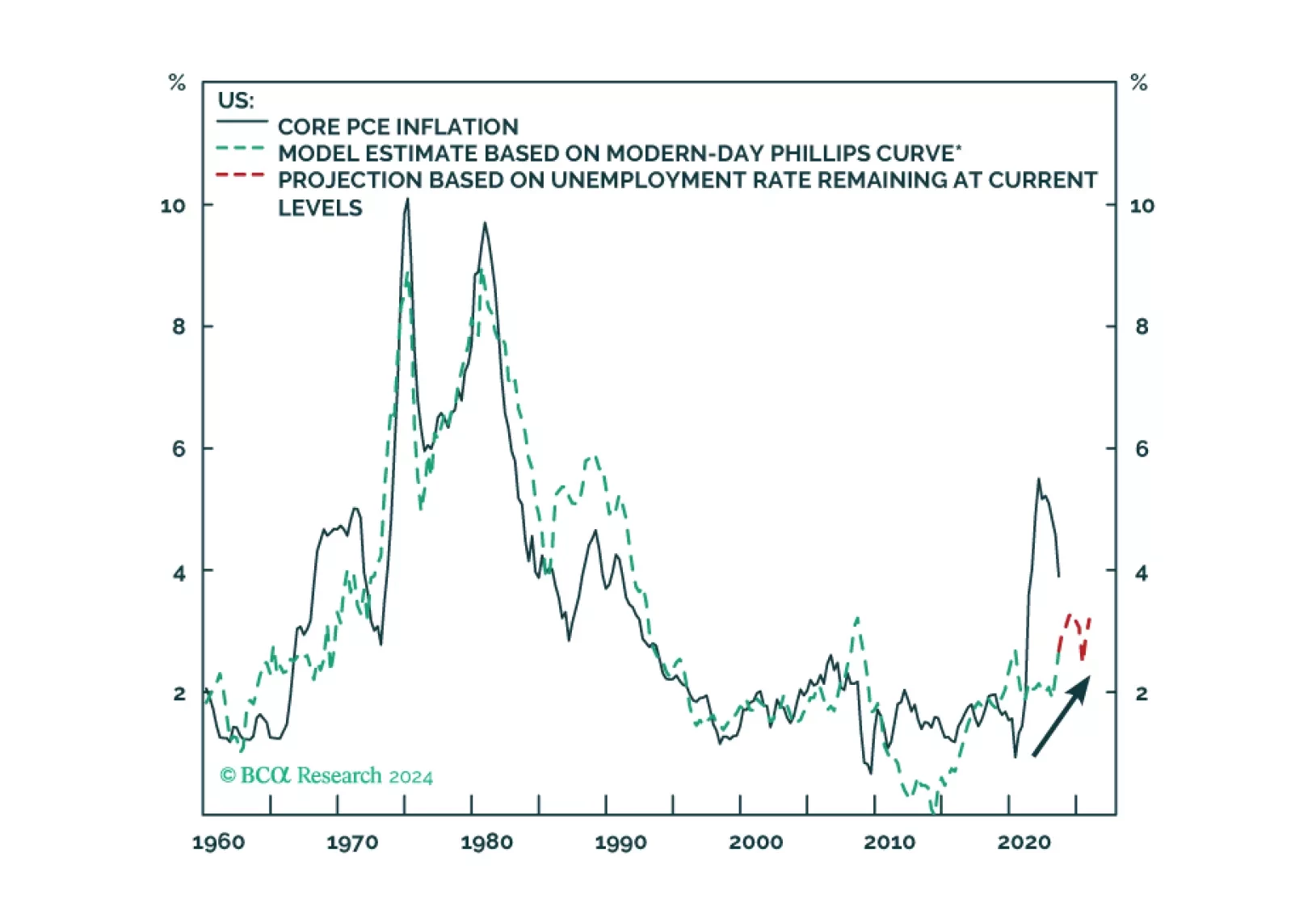

The Fed faces a dilemma. Cut rates early to avoid a recession, but at the risk of not slaying wage inflation. Or, not cut rates early to ensure that wage inflation is slayed, but at the risk of a downturn. Faced with such a dilemma, the lesser evil is to slay wage inflation even at the risk of a downturn. Meaning that the market has overpriced early rate cuts. We discuss some other investment implications, and identify two rebound candidates.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

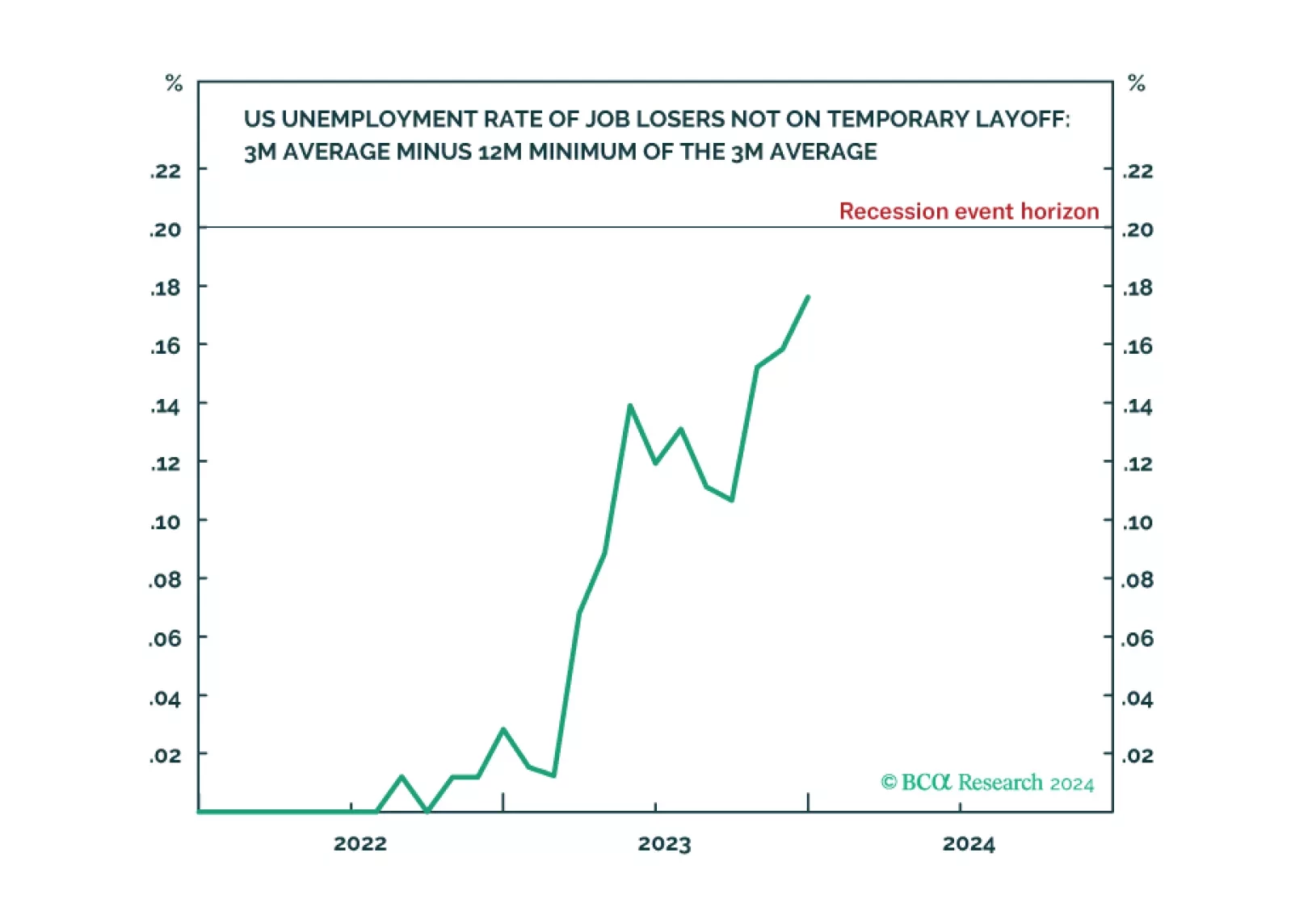

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

In Section I, we discuss the implications and potential risks of the Fed’s recent pivot. The near-term implications of the Fed's dovish pivot are likely to continue to be bullish for risky asset prices, and a new high in global stock prices cannot be ruled out. The Fed has not effectively countered market expectations that monetary policy will cease to be tight in a year’s time, which has eased financial conditions and will work counter to the Fed’s economic forecasts. However, we would expect this, at most, to delay rather than to prevent a recession. Developed economies remain on a recessionary path so long as monetary policy in the US and euro area remains actually tight. As such, we do not see the December meeting as a truly bullish catalyst for risky assets on a 12-month time horizon. In Section II, my colleague Ryan Swift of BCA’s US Bond Strategy service reviews the outlook for the Fed’s interest rate and balance sheet policies for next year.

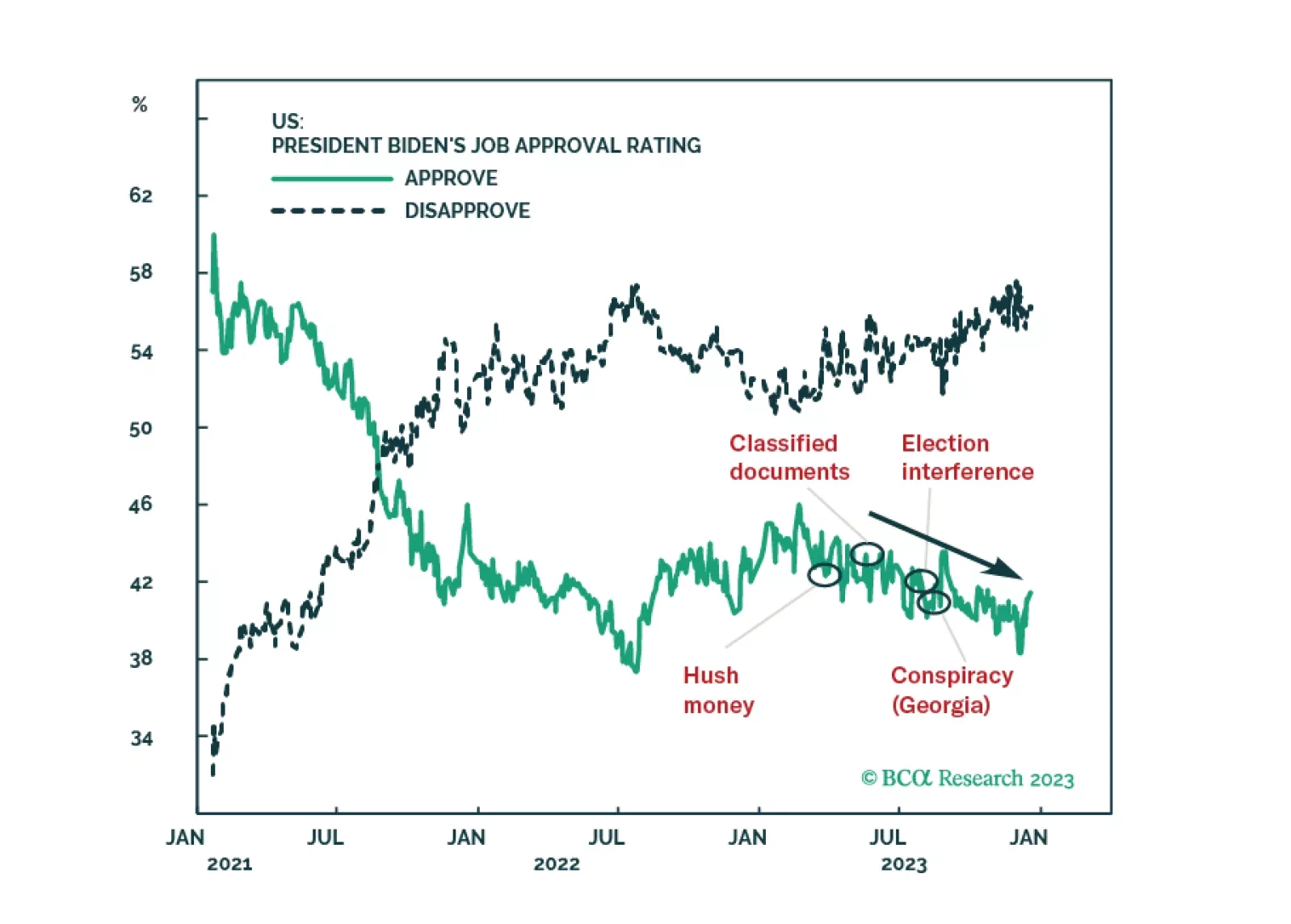

The Republican Party’s odds of winning the 2024 election will benefit, if anything, from state courts’ attempts to exclude President Trump from primary or general election ballots. Higher odds of a change of ruling party will increase stock and bond market volatility.

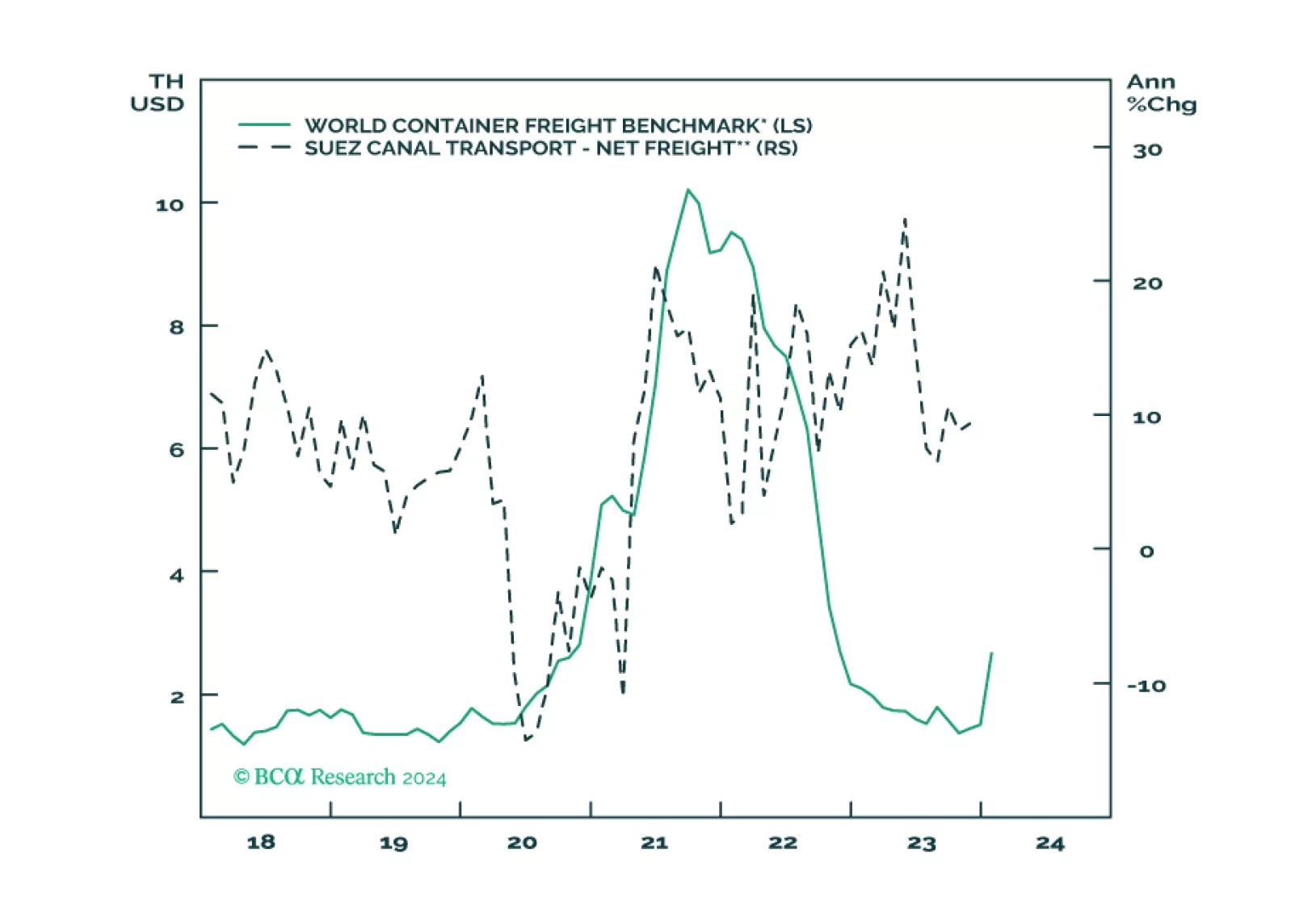

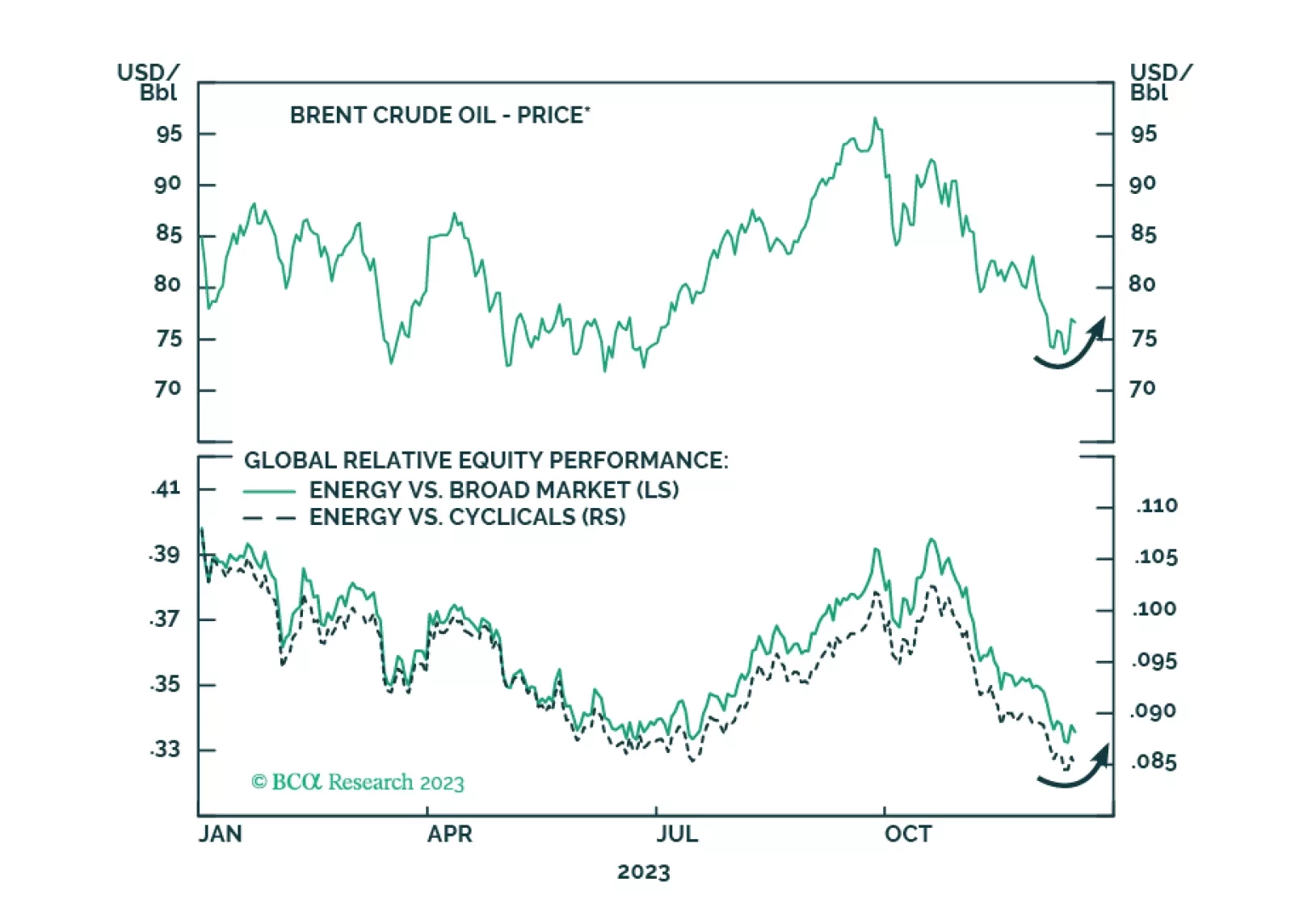

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

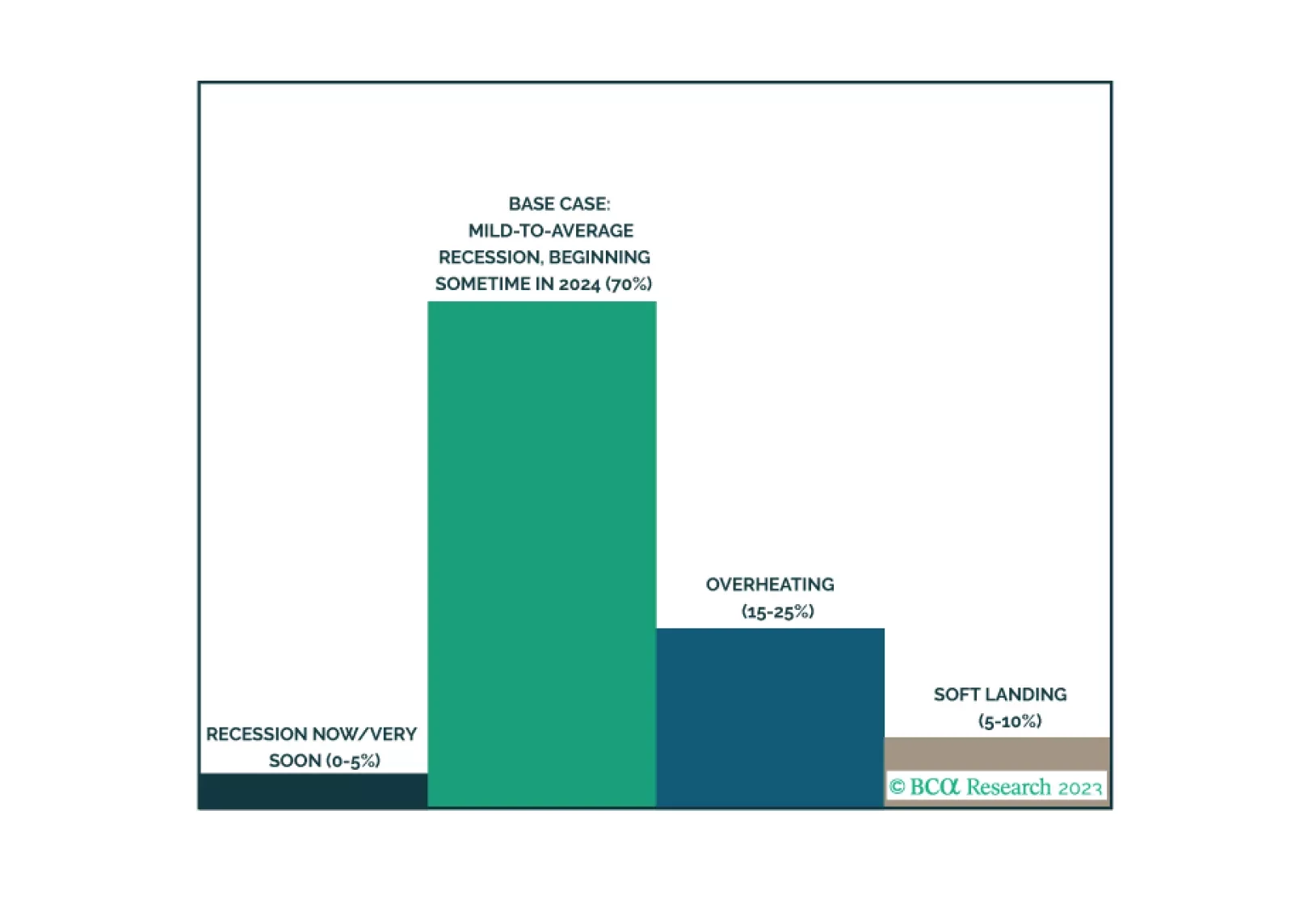

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.