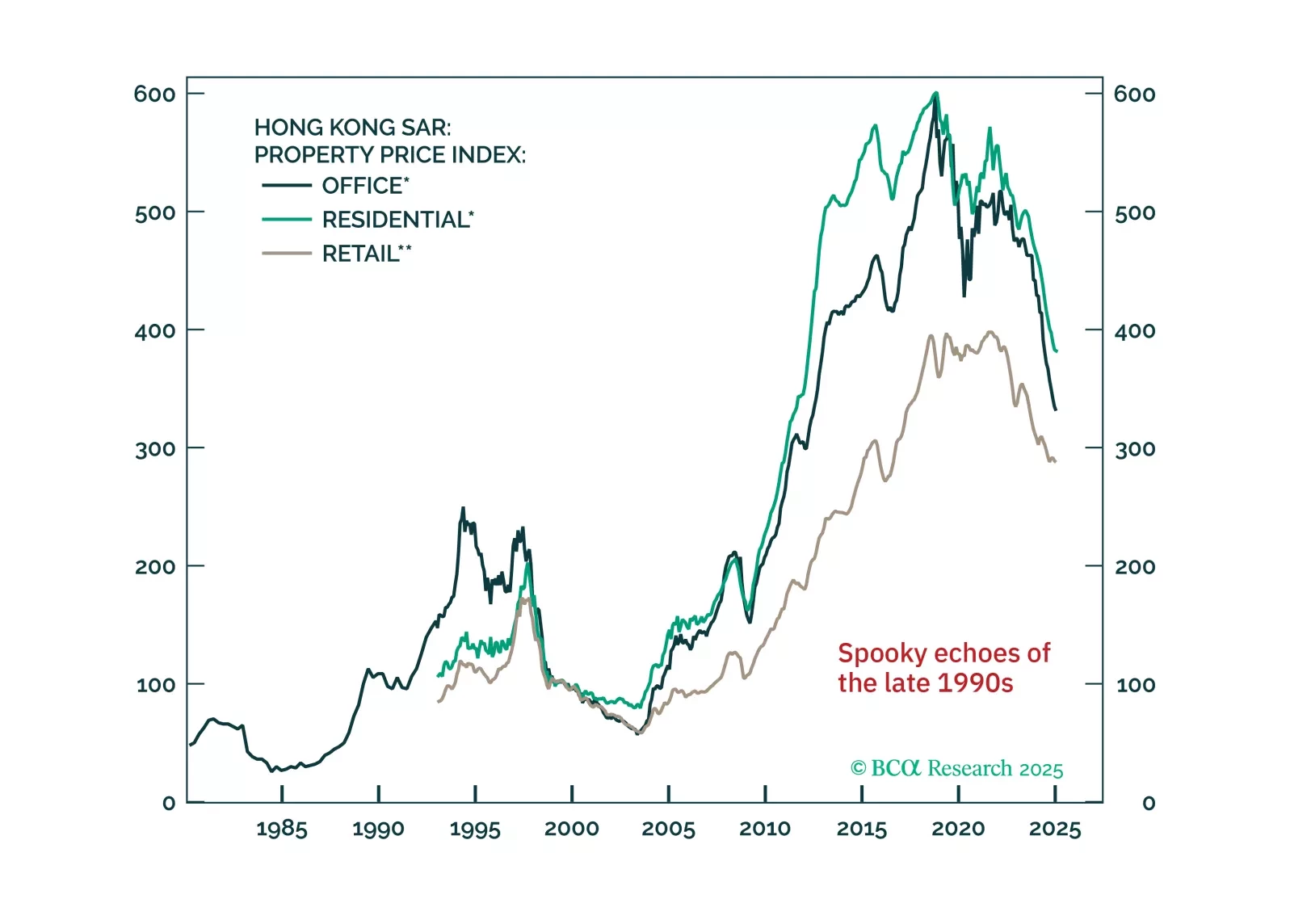

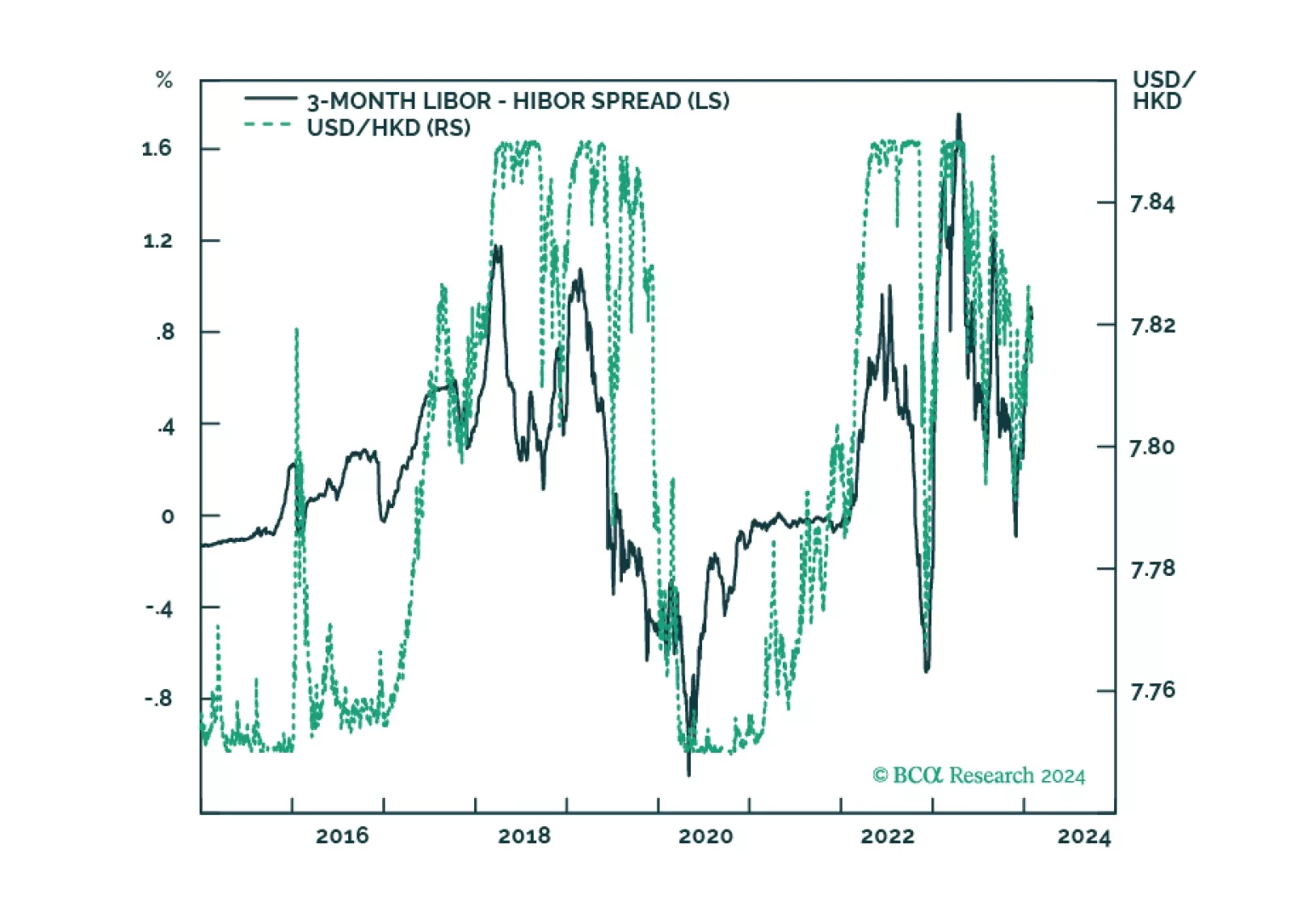

Dear clients, The Foreign Exchange Strategy will take a summer break next week. We will resume our publication on September 4th. Best regards, Chester Ntonifor, Vice President Foreign Exchange Strategy Feature The economy of Hong Kong SAR1 has been held under siege by two tectonic forces. With the highest share of exports-to-GDP in the world, and at very close proximity to China, the epicenter of the pandemic shock, economic growth has been knocked down hard. The second shock to Hong Kong’s economy has been political instability. The extradition bill that was proposed in February 2019, followed by the enactment of the national security law this past June, has been accompanied by cascading street-wide protests and social unrest. The spirit of the bill is that crimes committed in Hong Kong can be trialed in China. The US has moved to impose sanctions on Hong Kong, as it no longer sees the city-state as autonomous, the latest of which is revoking its extradition treaty with the former colony. Some commentators have defined this as the end of the one country, two systems socio-economic model that has been in place since the handover from British rule in 1997. From a currency perspective, these shocks put in question the sustainability of the Hong Kong dollar (HKD) peg. Historically, currency pegs more often than not fail, especially in the midst of both geopolitical and economic turmoil. This was the story of the Asian Financial crisis in the late 1990s, and the Mexican peso crisis earlier that decade. Is the Hong Kong dollar destined for the same fate? If so, what are the potential adjustments in the exchange rate? Finally, what indicators can investors look to as a guide for any pending adjustment? A Historical Perspective Chart 137 Years Of Stability The HKD is no stranger to shifting exchange-rate regimes. Over the last 170 years, it has been linked to the Chinese yuan, backed by silver, pegged to the British pound, free-floating, and, since 1983, tied to the US dollar. Therefore, a bet on the unsustainability of the peg is historically justified. That said, the stability of the peg to the US dollar has survived 37 years of economic volatility, suggesting the Hong Kong Monetary Authority (HKMA) has been able to successfully navigate a post-Bretton Woods currency era (Chart 1). Beginning as a bi-metallic monetary regime in the early 19th century, the HKD was initially linked to gold and silver prices, akin to the commodity–monetary standard that dominated that era. When Britain colonized Hong Kong in 1841, and as new trade alliances developed, the drawbacks of the bi-metallic monetary standard became apparent. As bilateral trade boomed, adjustments to imbalances (surpluses or deficits) could not occur through the exchange rate since it was fixed. Therefore, they had to occur through the real economy. This led to very volatile and destabilizing domestic prices. The stability of the peg to the US dollar has survived 37 years of economic volatility. Most Anglo-Saxon countries finally converted from bi-metallic exchange rates to the gold standard in the late 1800s, and strong ties to China dictated that Hong Kong naturally adopted the silver dollar in 1863. However, the silver system had the same drawbacks as the bi-metallic standard. Specifically, when your money supply is fixed, any increase in output leads to “few dollars chasing many goods.” This is synonymous with falling prices, just as “many dollars chasing few goods” is synonymous with rising inflation. The petri dish for this phenomenon was the post-World War I construction boom. A fixed money supply under the gold (and silver) standard meant rapidly falling prices globally. By the late 1920s, most countries had overvalued exchange rates relative to gold (and silver), that exerted powerful deflationary forces on their domestic economies. This forced most Western governments to debase fiat money vis-à-vis gold to stop price deflation. Correspondingly, China had to abandon the silver standard in November 1935, with Hong Kong shortly following suit. At the time of debasement, the United Kingdom was the leading economic power. As a colony, it made sense for the Hong Kong government to link the HKD to the British pound. The established rate was GBP/HKD 16, giving birth to the currency board system (Chart 2). Meanwhile, as a trading hub, a peg with an international currency made sense. The problems there were two-fold. First, the pound was still gold-linked. And second, Britain’s subsequent decline in economic power was accompanied by a series of sudden and dramatic devaluations in the pound, which was hugely disruptive to Hong Kong’s financial system. By 1972, the British government decided to float the pound, which effectively ended the GBP/HKD peg. Chart 2A History Of The HKD Peg In July 1972, the authorities made the decision to peg the Hong Kong dollar to the US dollar at USD/HKD 5.65, which was another policy mistake. The switch made sense given the rising economic power of the US, as well as rising trade links (Chart 3). However, the dollar was also under a crisis of confidence following the Nixon devaluation in 1971. In February 1973, the HKD was freely floated. Chart 3The Peg Is Usually Against The Dominant Economic Power Counter-intuitively, the free-floating era for HKD was arguably the most volatile for its domestic economy. For one, discipline in monetary policy was gone. Money and credit growth exploded, inflation hit double-digits, home prices soared and the trade balance massively deteriorated. Political instability was also rife, given the uncertainty surrounding the end of British claims on the island. As the dialogue included China’s reclaim of political control over Hong Kong, there was uncertainty over the rule of law. This cocktail of political and economic uncertainty led to a 33% depreciation in the HKD between mid-1980 and October 1983. Panicked policymakers returned to the US dollar peg. Paul Volcker, then Federal Reserve chairperson, was establishing himself as the world’s most credible central banker, having dropped US inflation from almost 15% in 1980 to below 3% by 1983. Economic and financial links with the US also justified a peg. In August of 1983, the authorities announced a USD/HKD fixed rate of 7.80, which has remained in place since. The Current Peg: Advantages And Disadvantages Chart 4Fiscal Prudence In Hong Kong The advantage of the HKD peg is that the choice of the nominal anchor, the US dollar, renders it credible. First, the US dollar is an international reserve currency dominating international trade, which helps to facilitate settlements while instilling confidence among transacting participants. As a financial hub, this is crucial for Hong Kong. Meanwhile, such an anchor imposes fiscal discipline, since government deficits cannot be monetized by money printing. In the case where the government tries to be profligate, the rise in inflation will lower real rates and lead to capital outflows. This will force the HKMA to sell US dollars and absorb local currency. In the extreme case, the central bank can run out of reserves, causing the peg to collapse. Indeed, over the past several years, government debt in Hong Kong has been close to nil (Chart 4). The drawback of a fixed exchange rate regime is that a country or a region relinquishes control over independent monetary policy. In the case of Hong Kong, this means that interest rates are determined by the actions of the US Fed. Such a marriage was justified when the business cycles between the two economies were in sync, but in times of economic divergences, the fixed exchange rate leads to economic volatility. Chart 5Currency Peg And Internal Devaluation Chart 6Hong Kong Interest Rates In The Late 90's This divergence was clearly evident in the 1990s, as falling interest rates in the US supercharged a housing and stock market bubble in Hong Kong. When the Asian crisis finally came around in 1997, the lack of exchange-rate flexibility led to a vicious internal devaluation (Chart 5). A prolonged period of high unemployment and stagnant wages was needed for Hong Kong to finally improve its competitiveness. Most importantly, in 1998, in the depths of the Asian financial crisis, the peg attracted a concerted attack from speculators who believed a devaluation of the Hong Kong dollar alongside other regional currencies was inevitable. Their assault inflicted considerable pain, driving short-term HKD interest rates (Chart 6) and wiping out over a quarter of the local stock market in a matter of weeks. At the time, the Hong Kong government was successful in fending off the speculative attacks by intervening massively in both the foreign exchange and equity markets. Is An Adjustment Pending? If So, When? Chart 7USD/HKD And Interest Rate Spreads As the above narrative suggests, the HKD is no stranger to socio-economic shocks and speculative attacks, and it has, more recently, weathered them pretty well. The more immediate question is whether the shift in the political landscape could be potent enough to crack the peg this time around. While plausible, it is unlikely for a few reasons. First, the HKD continues to trade on the stronger side of the peg as US interest rates have collapsed, wiping off any positive carry that would have catalyzed outflows. Fluctuations in the USD/HKD within the 7.75-7.85-band track the Libor-Hibor spread pretty closely (Chart 7). A currency board has unlimited ability to defend the strong side of the peg, since it can print currency and absorb foreign reserves (print HKDs and use these to buy USDs in this case). On the weak side, these foreign exchange reserves are drawn down. Therefore, any threat to the peg should be preceded by consistent trading on the weaker side, questioning the HKMA’s ability to keep selling FX reserves to defend the peg. Fluctuations in the USD/HKD within the 7.75-7.85-band track the Libor-Hibor spread pretty closely. Second, the Hong Kong peg remains extremely credible, since the entire monetary base is backed over two times by FX reserves (Chart 8). Even as a percentage of broad money supply, Hong Kong reserves are ample and very high by historical standards (Chart 8, bottom panel). Meanwhile, since 1983, the currency board system has undergone a number of reforms and modifications, allowing it to adapt to the changing macro environment. This represents a powerful insurance policy for the HKMA’s ability to defend the currency peg, significantly enhancing the system’s credibility. Chart 8Ample Foreign Exchange Reserves Chart 9Hong Kong Runs Recurring Surpluses Third, ever since the peg was instituted, Hong Kong has mostly run budget surpluses. As a result, government debt in Hong Kong is almost non-existent, as we illustrate above. This has removed any incentive to monetize spending, which remains an open argument in the US, Japan or even the euro area. One of our favored metrics on the health of a currency is the basic balance, and on this basis, Hong Kong scores much more favorably than the US. While Hong Kong has transitioned from being a goods exporter to that of services, it remains extremely competitive, with a healthy current account surplus of 5% of GDP (Chart 9). These recurring surpluses have propelled Hong Kong to one of the biggest creditors in the world, with a net international investment position that is a whopping 430% of GDP and rising (Chart 10). Chart 10Hong Kong Is A Net Creditor To The World Fourth, over the past few years, productivity in Hong Kong has outpaced that of the US and most of its trading partners (Chart 11). This has lifted the fair value of the currency tremendously. This means it is more like that when the peg adjusts, the outcome will be HKD appreciation. On a real effective exchange rate basis, the HKD is not that overvalued compared to the US dollar, after accounting for the massive increase in relative productivity (Chart 12). It is notable that during the Asian financial crisis, currencies like the Thai bhat were massively overvalued, which is why the adjustment was back down toward fair value. Chart 11Hong Kong Is Highly Productive Chart 12Trade-Weighted HKD Is Slightly Expensive Fifth, there is a strong incentive for both Beijing and Hong Kong to defend the peg, because the relevance of Hong Kong is no longer as a shipping port, but as a financial center. The peg reduces volatility, as transactions are essentially dollarized. The relevance of Hong Kong in Asia can be seen by looking at the market capitalization of the Hang Seng index compared to that of the Topix index in Tokyo or the Shanghai Composite index. Any escalation in the US-China trade war, especially in the technology sphere, will only lead to more listings on the Hong Kong stock exchange. Equity flows through the HK-Shanghai and HK-Shenzhen stock connect program are rising, suggesting the market still considers Hong Kong an important intermediary in doing business with China (Chart 13). On the political front, the most potent risk is that the US Treasury moves to unilaterally limit access to US dollars by Hong Kong banks. While this was discussed by President Trump’s top advisers, it was also dismissed as unwise due to the potential shock to the global financial system. Meanwhile, with massive swap lines with the Fed, Hong Kong’s international banks can always draw on US liquidity. Tariffs on Hong Kong goods are another option, but this again will not really deal a severe blow to the peg, since Hong Kong mainly re-exports, with very little in the way of domestic goods exports (Chart 14). Chart 13Hong Kong Is An Important Financial Center Chart 14Hong Kong Is Partially Insulated From Tariffs Property Market Blues The property market is the one area in Hong Kong where a sanguine view is difficult to paint. Hong Kong is one of the most unaffordable cities on the planet, and high income inequality has been a reason behind resident angst. The gini coefficient, a measure of inequality in a society, is more elevated in Hong Kong compared to Singapore, China or even South Africa. After years of loose monetary policy, property prices in Hong Kong have completely decoupled from fundamentals. Housing is even more unaffordable now than it was back in 1997, and domestic leverage is very high. With such a high debt stock, even a gradual uptick in interest rates will have a significant impact on the debt service burden (Chart 15). Stocks and real estate prices are positively correlated, suggesting deleveraging pressures will likely be quite high if both unravel (Chart 16). Chart 15High Debt Service Burden##br## In Hong Kong Chart 16Hong Kong Stocks Are Tied To The Property Market However, there are offsetting factors. First, it is unlikely that interest rates in Hong Kong (or anywhere in the developed world for that matter) will rise anytime soon. COVID-19 has provided “carte blanche” in terms of global stimulus. More importantly, the US is at the forefront of this campaign, meaning interest rates in Hong Kong will remain low for a while. Second, in recent history, Hong Kong has proven that it has the resilience to handle volatility in the property markets. During the Asian crisis, property prices fell by 60%, yet no bank went bust. Share prices also collapsed but are much higher today, suggesting the drop was a buying opportunity. And with such a low government debt burden, any systemic threat to banks will nudge the authorities to bail out important companies and sectors. In terms of asset markets, the performance of the Hang Seng index relative to the S&P 500 is purely a function of interest rates. The US stock market is dominated by technology and healthcare that do well when interest rates fall, while banks and real estate dominate the Hong Kong market. So rising rates hurt the US stock market much more than Hong Kong (Chart 17). Meanwhile, the recent turmoil has made Hong Kong assets very cheap relative to its sister-city, Singapore (Chart 18). This suggests that a lot of the potential equity outflows have already occurred, based on today’s situation. Chart 17Interest Rates And The Hong Kong Stock Market Chart 18Hong Kong Has Cheapened Relative To Singapore The Future Of The Peg A peg to the Chinese RMB makes sense. The Hong Kong economy is now heavily tied to the Chinese economy, with over 50% of exports going to China (previously mentioned Chart 3). However, that will sound the death knell for Hong Kong’s status as a financial center, since the US dollar remains very much a reserve currency. There is also a risk that if Beijing uses RMB depreciation as a weapon in a blown-out confrontation with the US in the coming years, it will threaten the sustainability of the HKD peg, since it could inflate asset bubbles. What is more likely is that the option of re-pegging to the RMB comes many years down the road, when the yuan has become a fully convertible currency. The recent turmoil has made Hong Kong assets very cheap relative to its sister-city, Singapore. There is the option to assume another currency board akin to Singapore. This option makes sense, since this would give the HKMA scope to link to cheaper currencies, such as the yen and euro. Such an overhaul will require significant technical expertise and political will from both Beijing and Hong Kong. It is not very clear what the cost/benefit outcome would be of this initiative, but it is worth considering since the RMB itself is managed against other currencies. Finally, there is always the option to fully float the peg, but this is likely to increase volatility. As well, for policymakers, it makes sense to continue pegging the exchange rate to the US dollar as it depreciates against major currencies, since it ends up easing financial conditions for Hong Kong concerns. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Special Administrative Region of the People's Republic of China Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades