Government

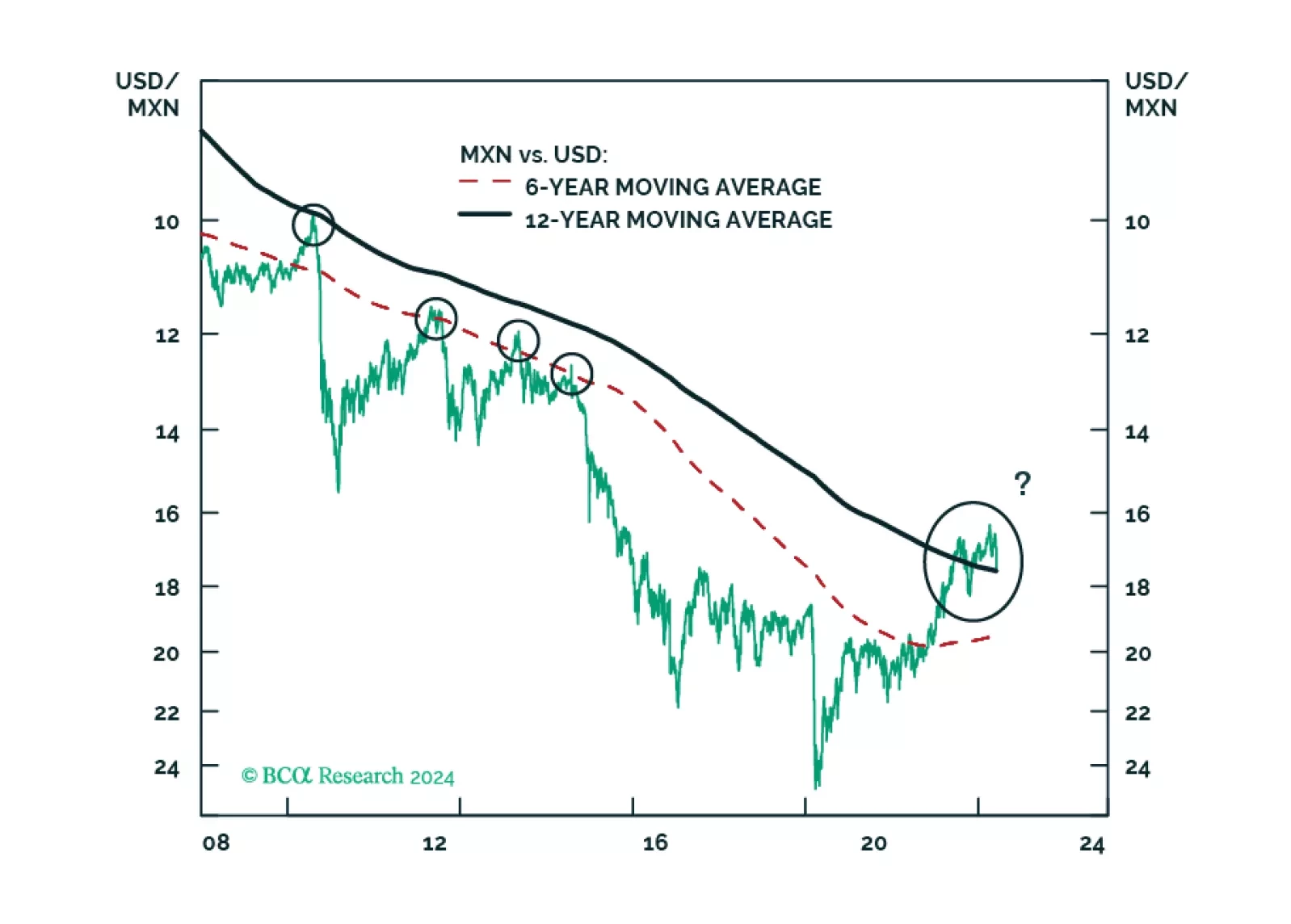

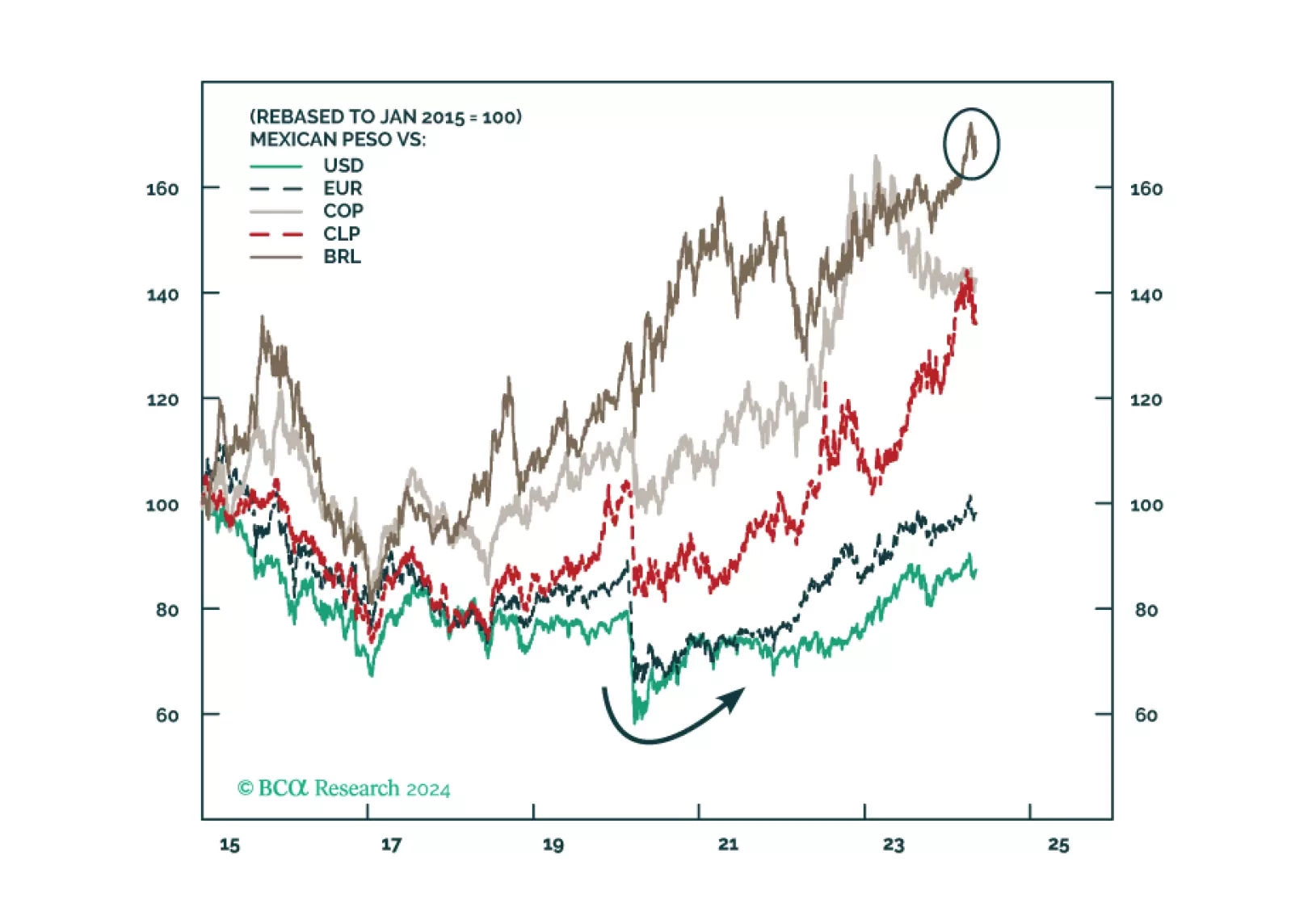

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

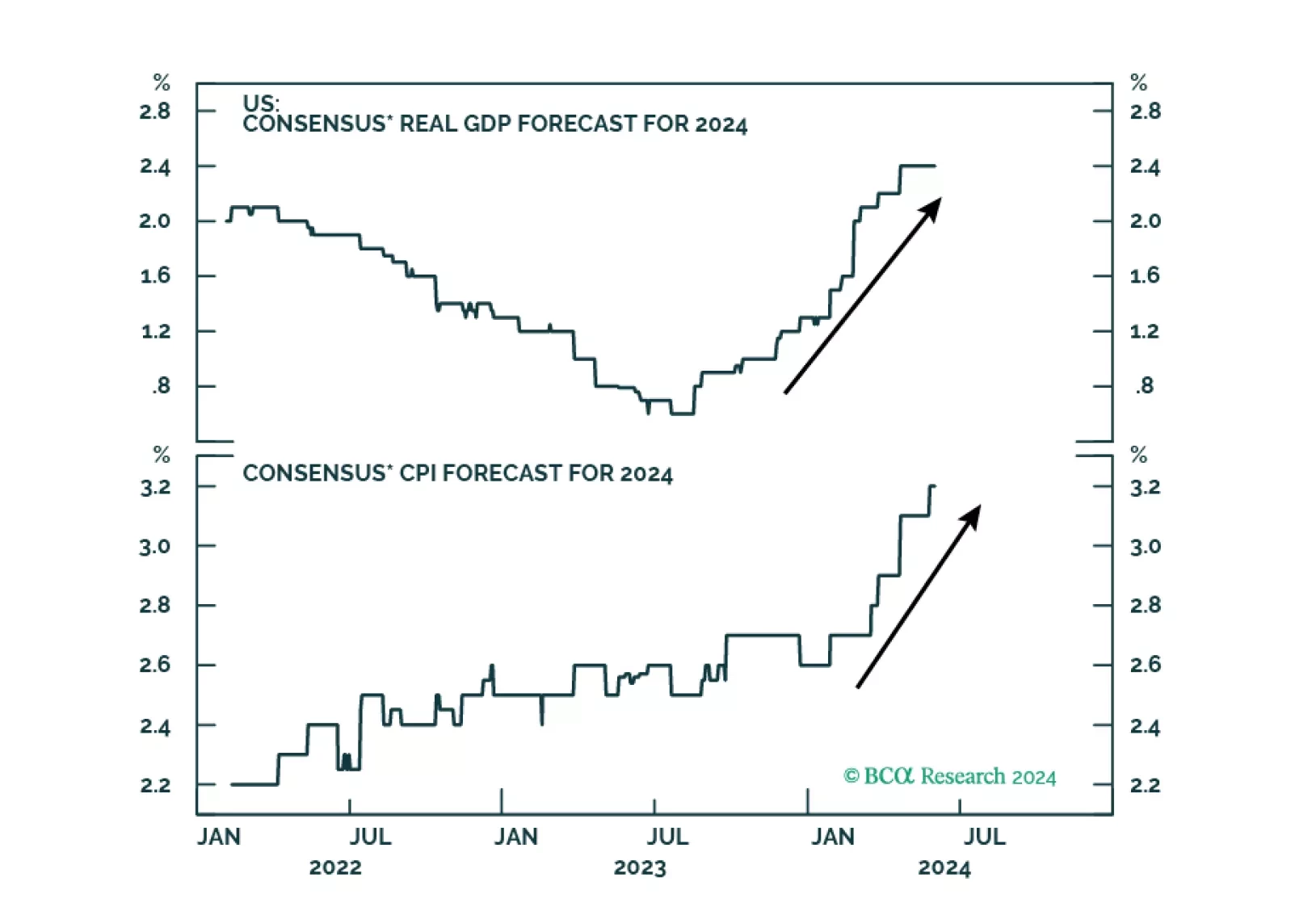

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

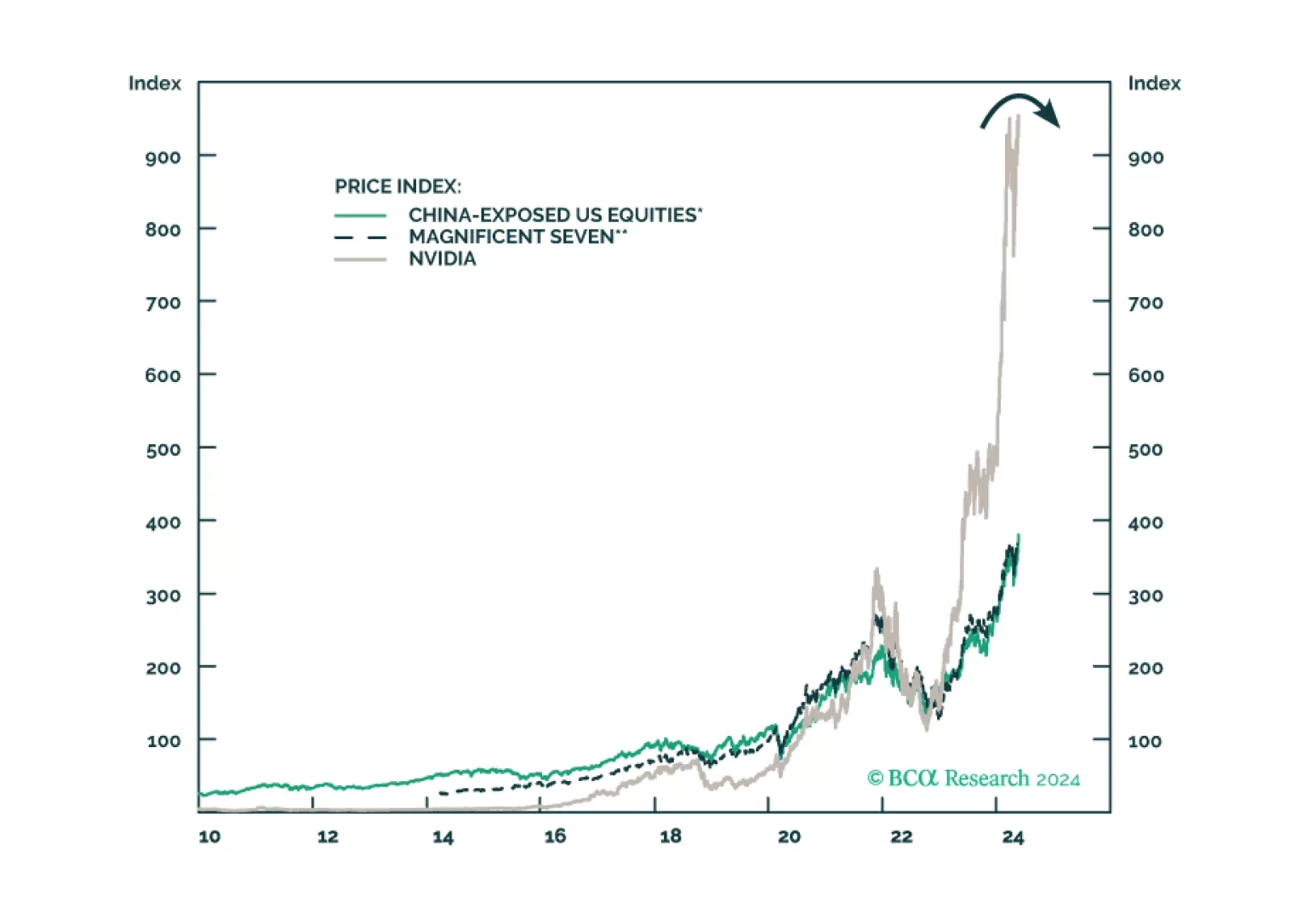

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

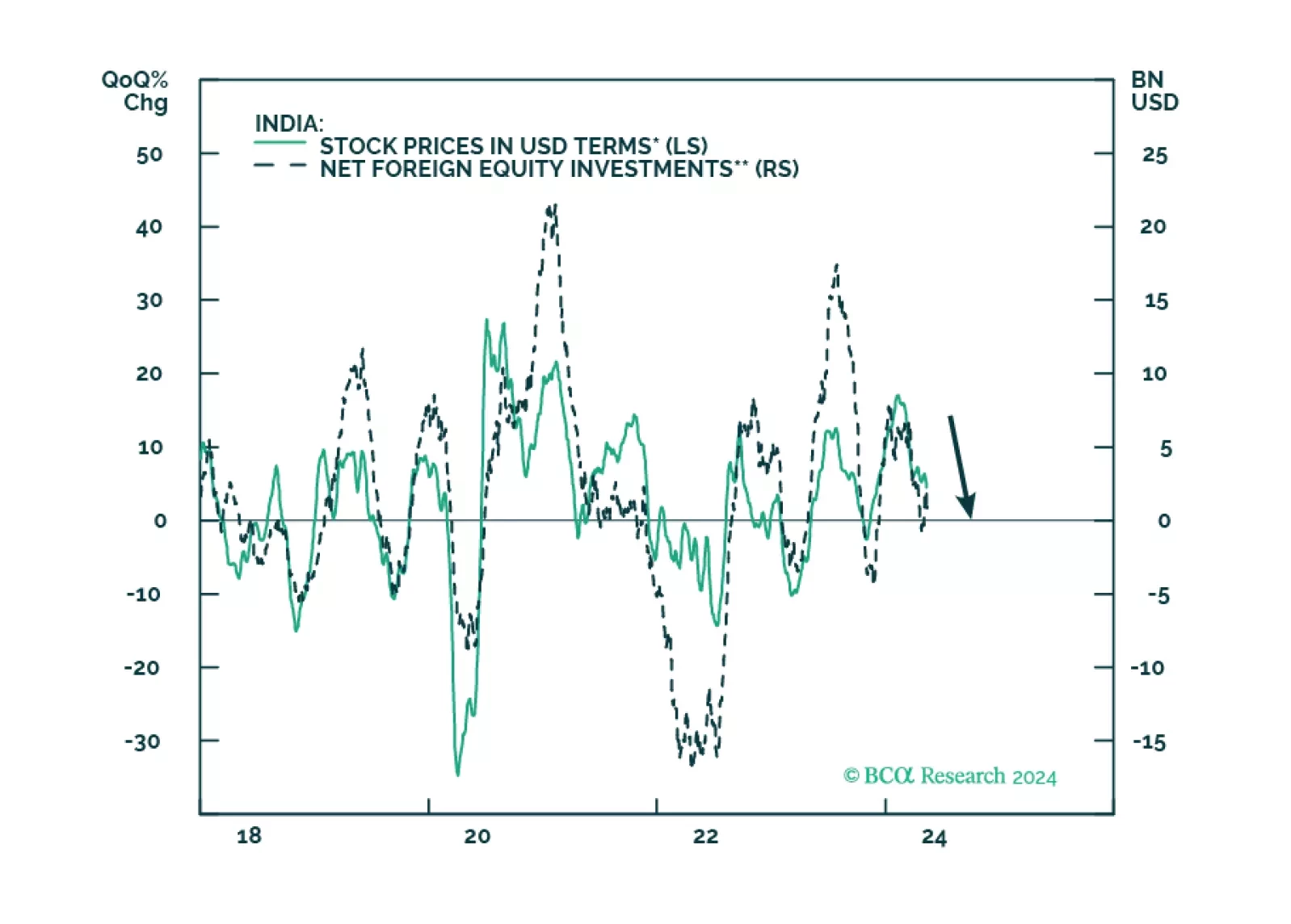

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.