Gov Sovereigns/Treasurys

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

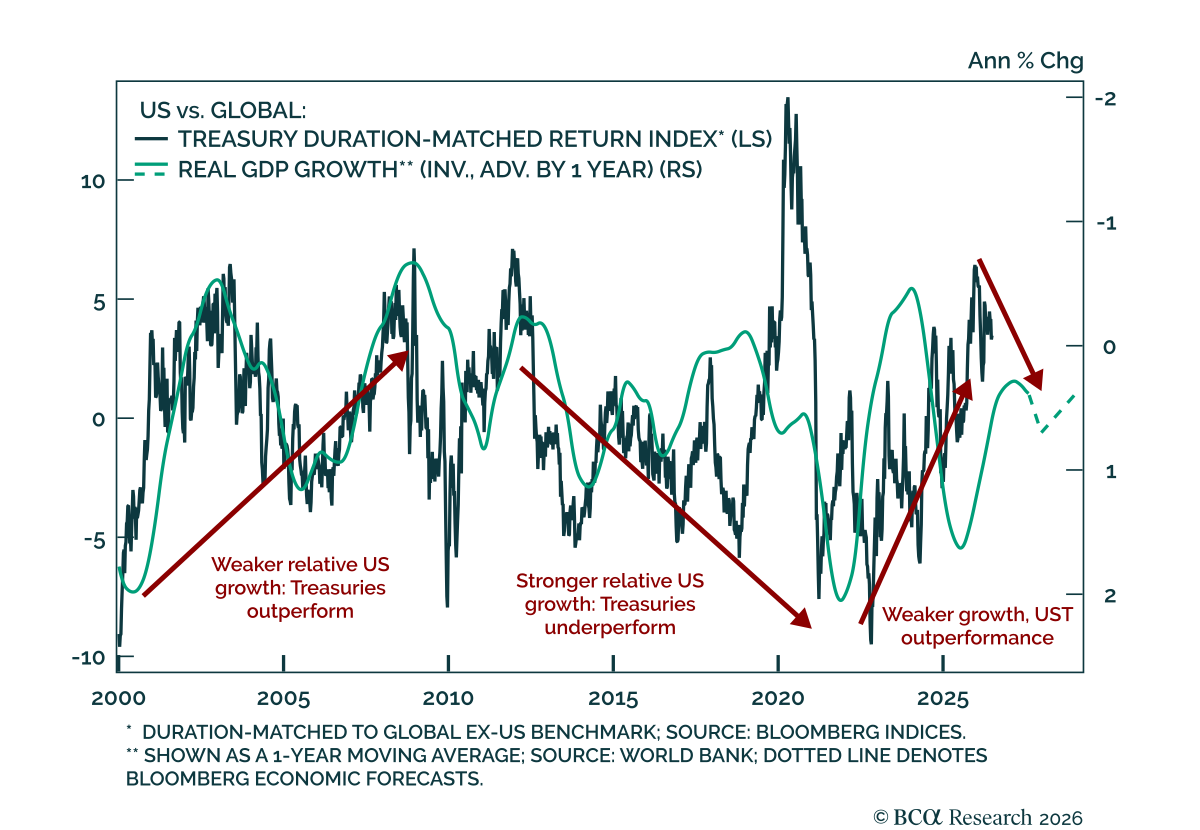

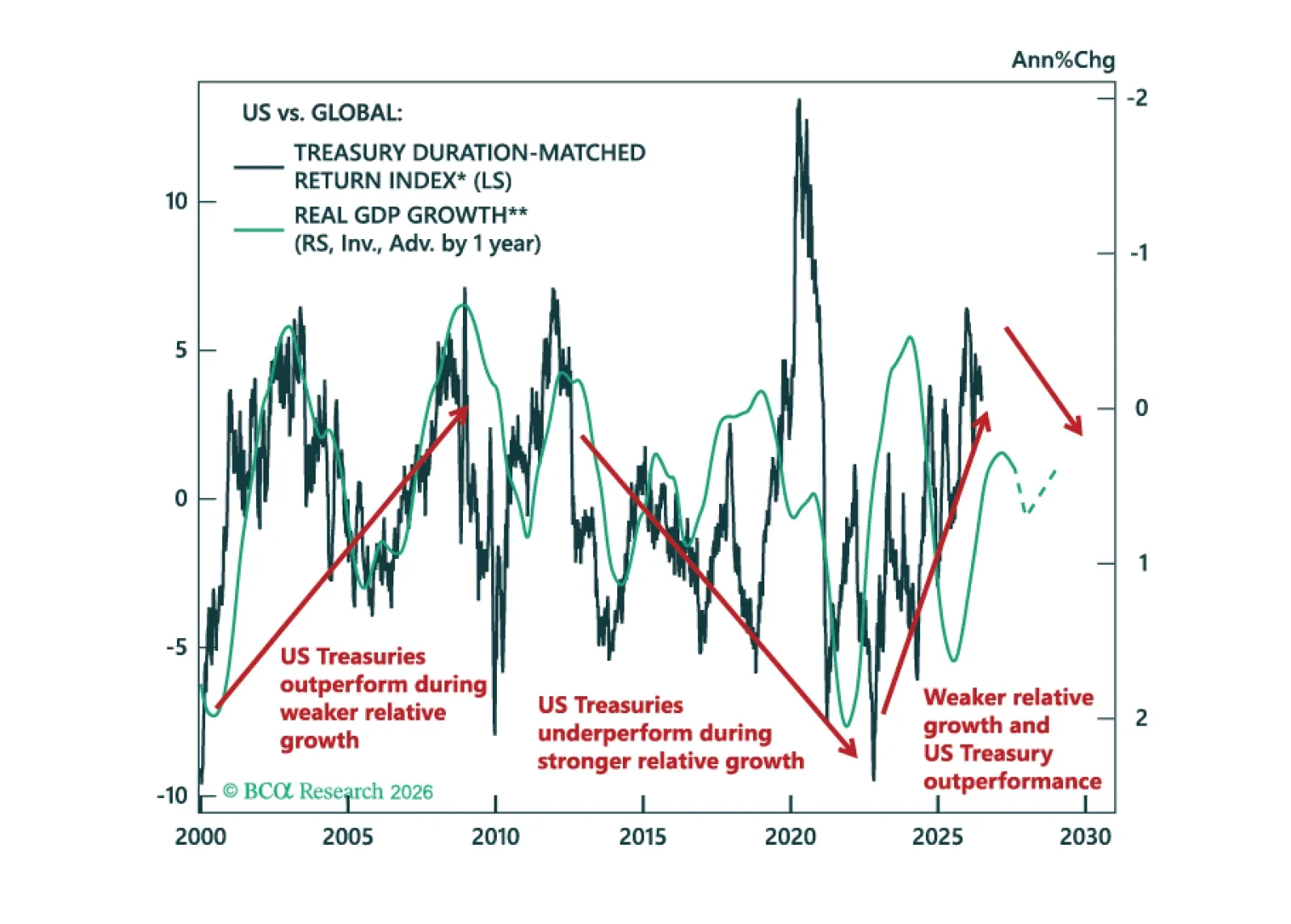

We review our Model Bond Portfolio performance for Q2 and look ahead as fixed income markets move beyond the US-Iran conflict, which is finding its kinetic equilibrium. Valuations and growth differentials are moving against continued US Treasury outperformance.

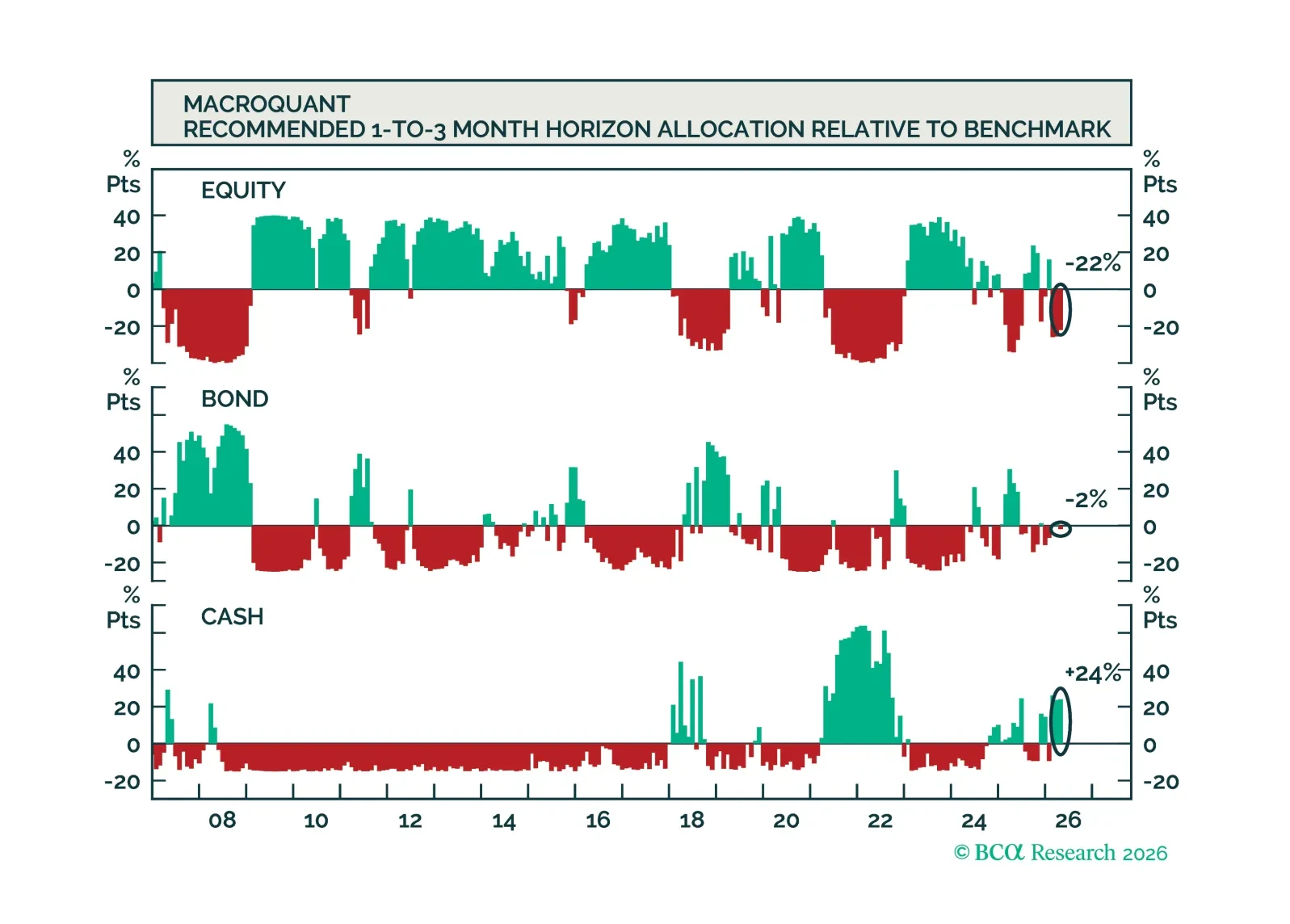

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

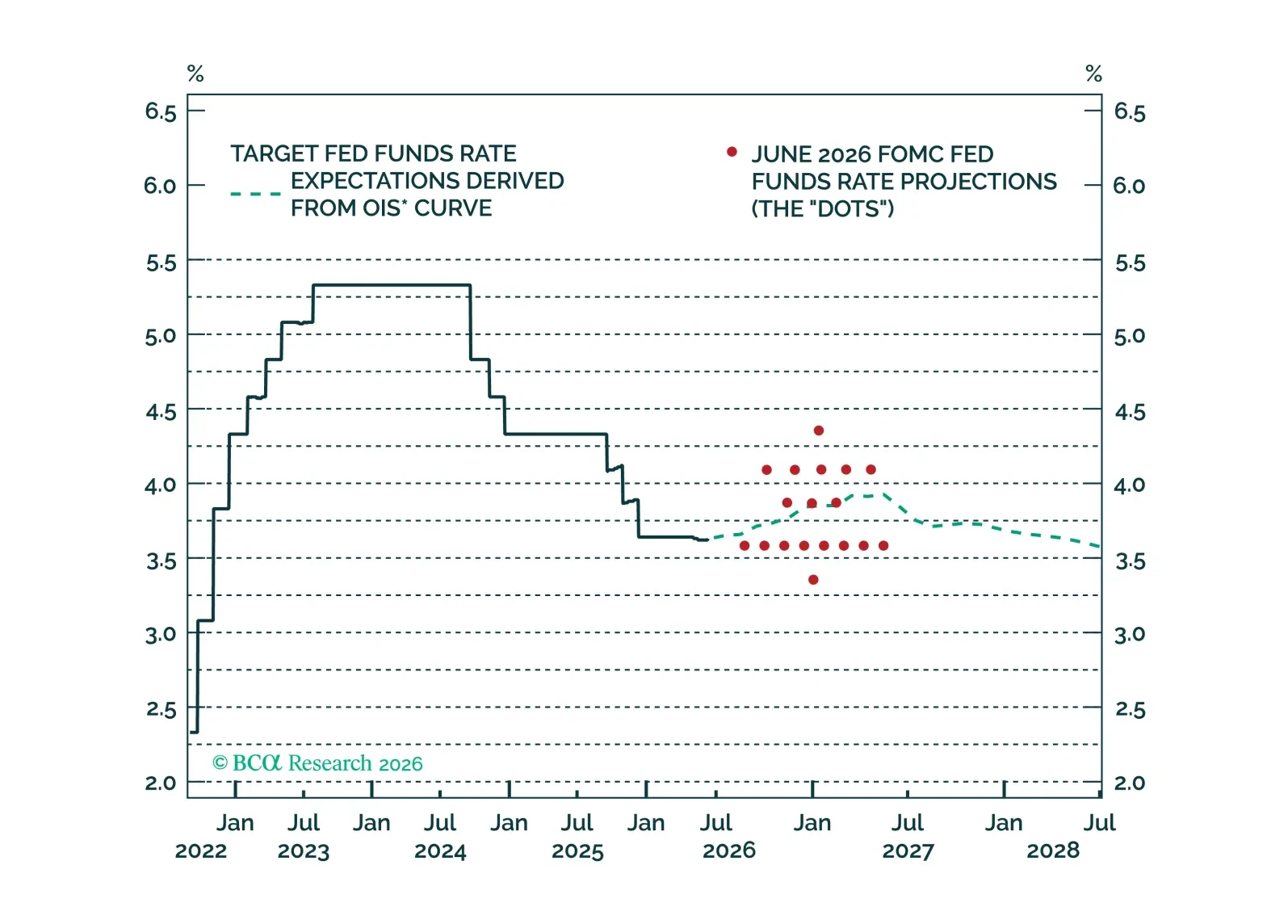

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.

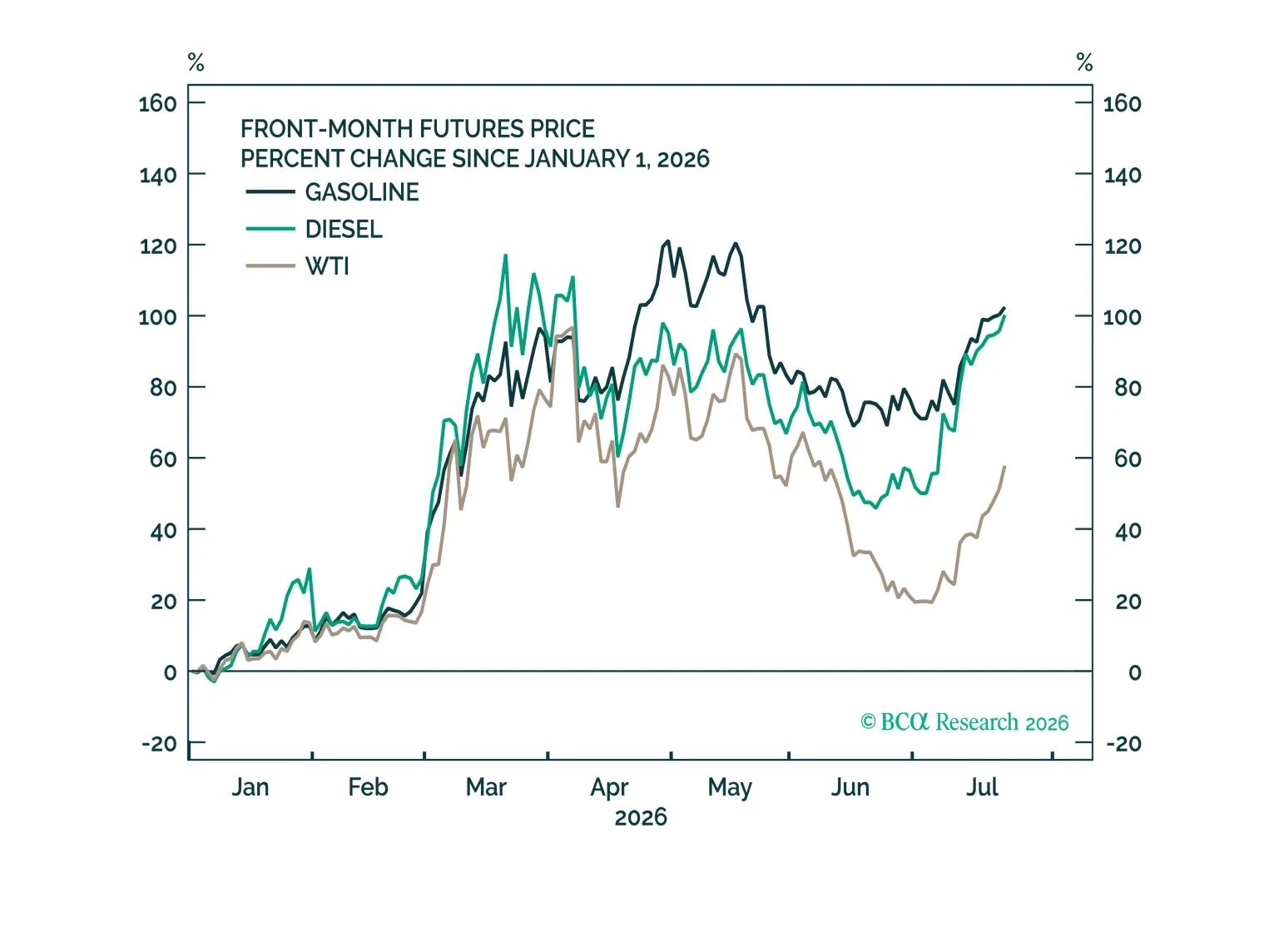

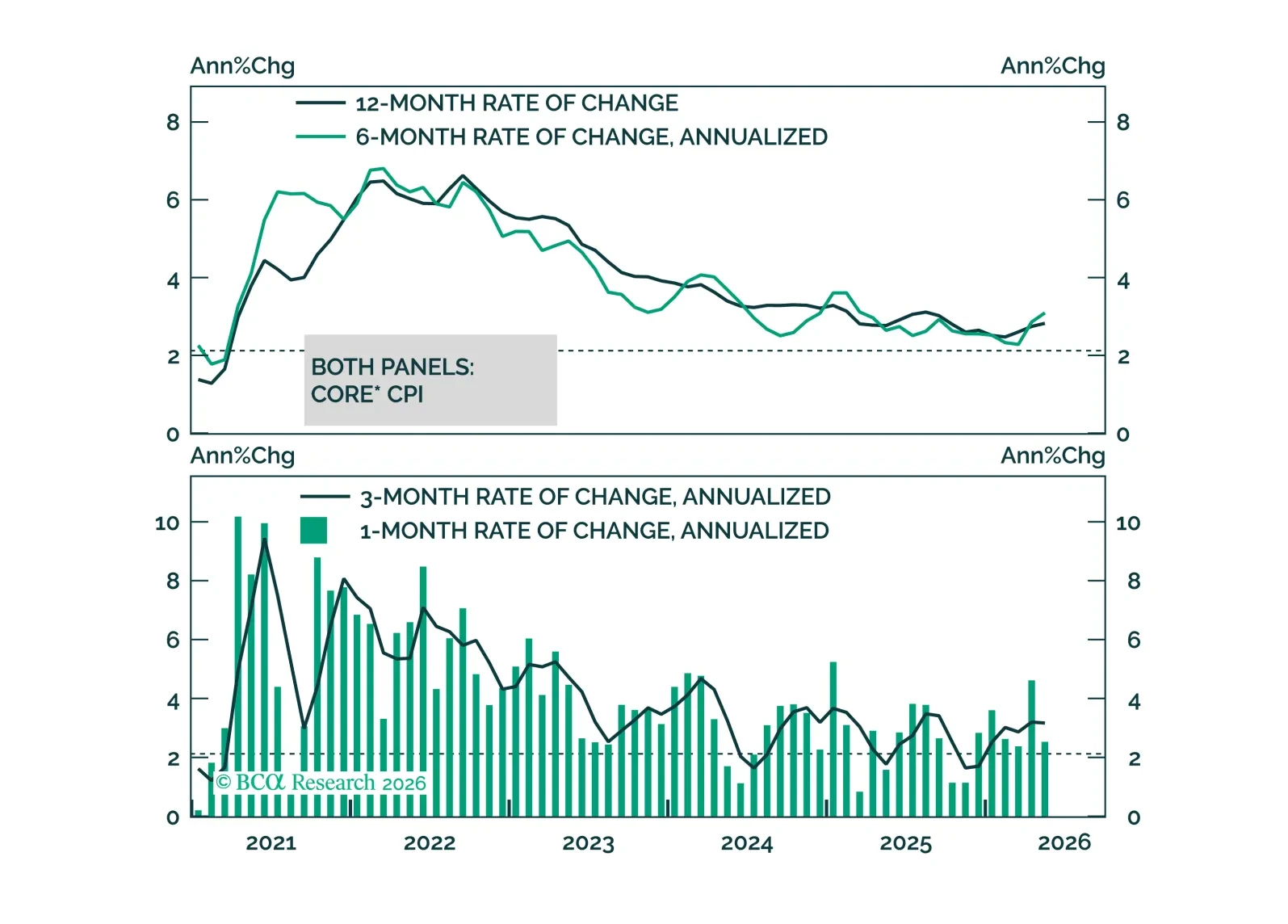

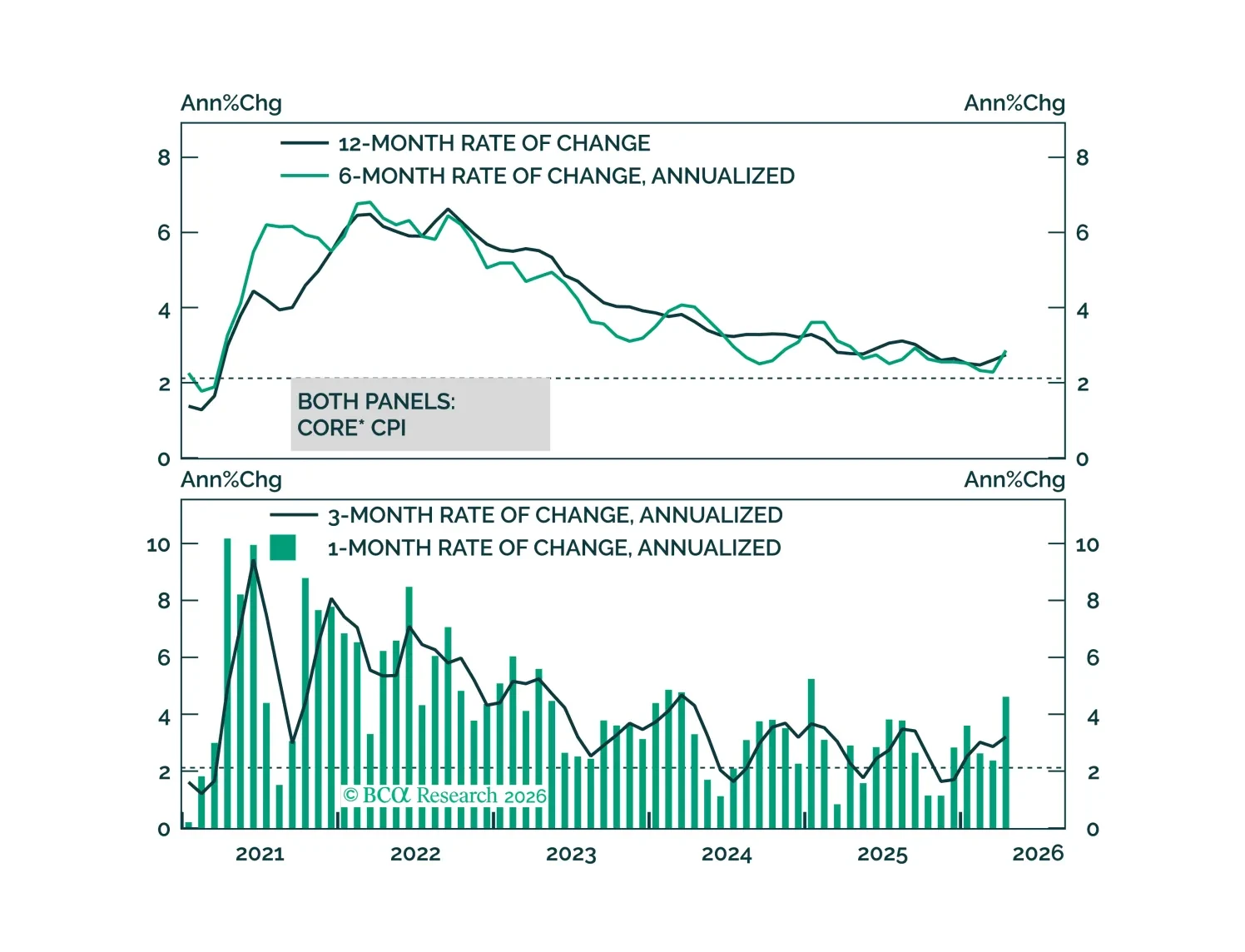

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.