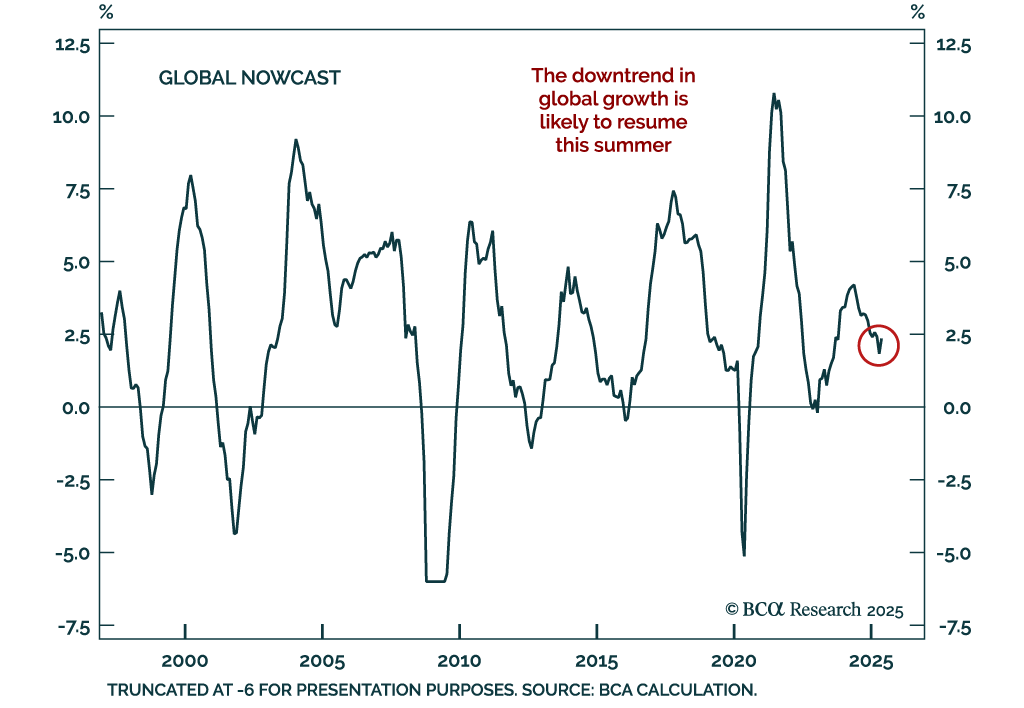

Global

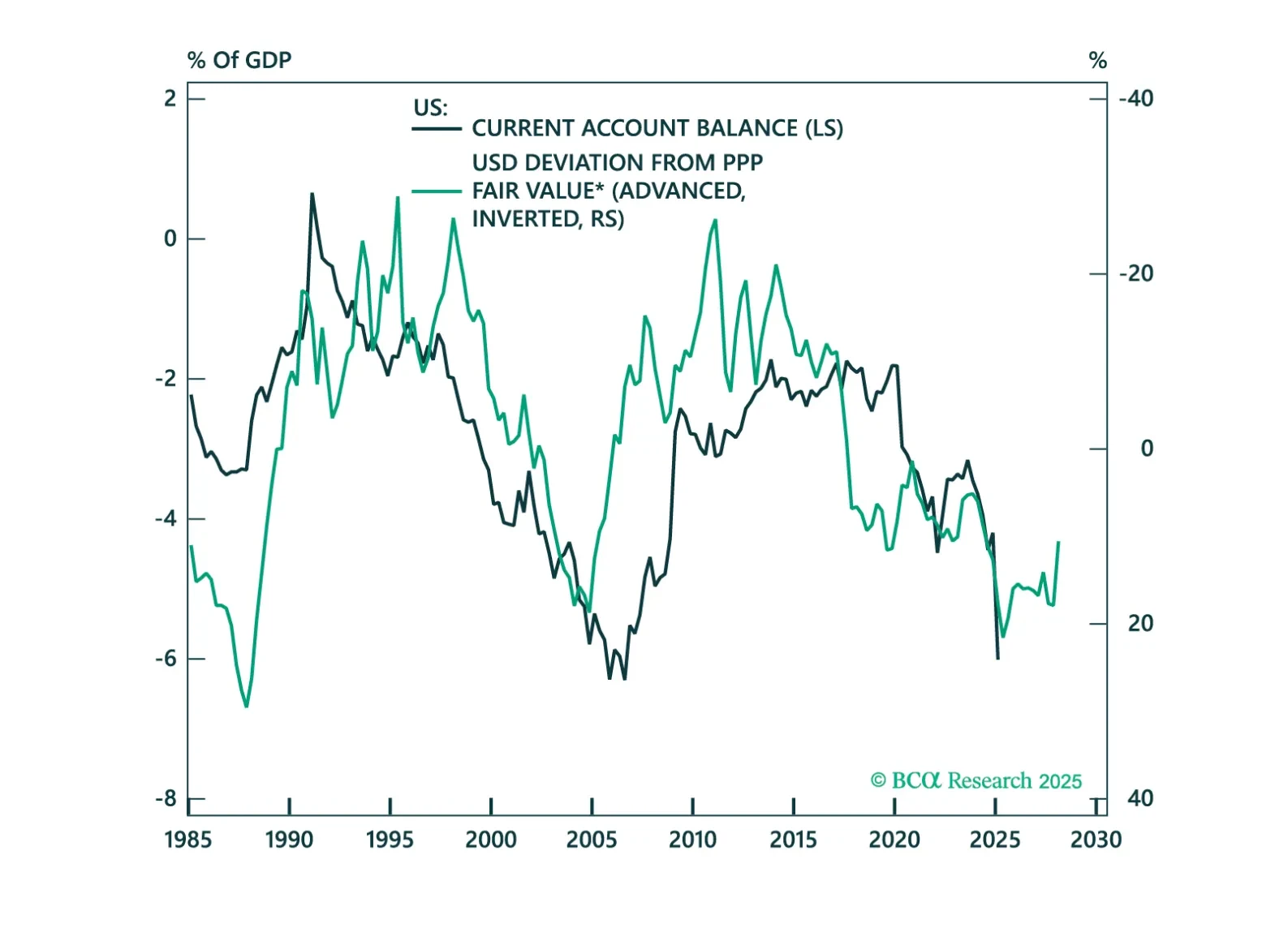

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

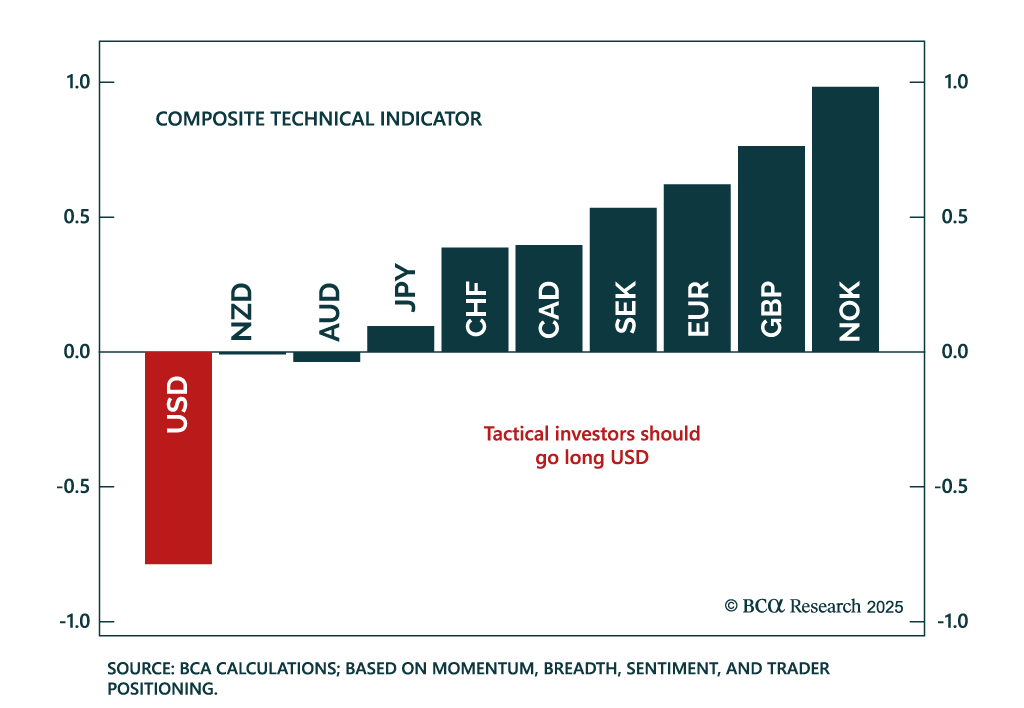

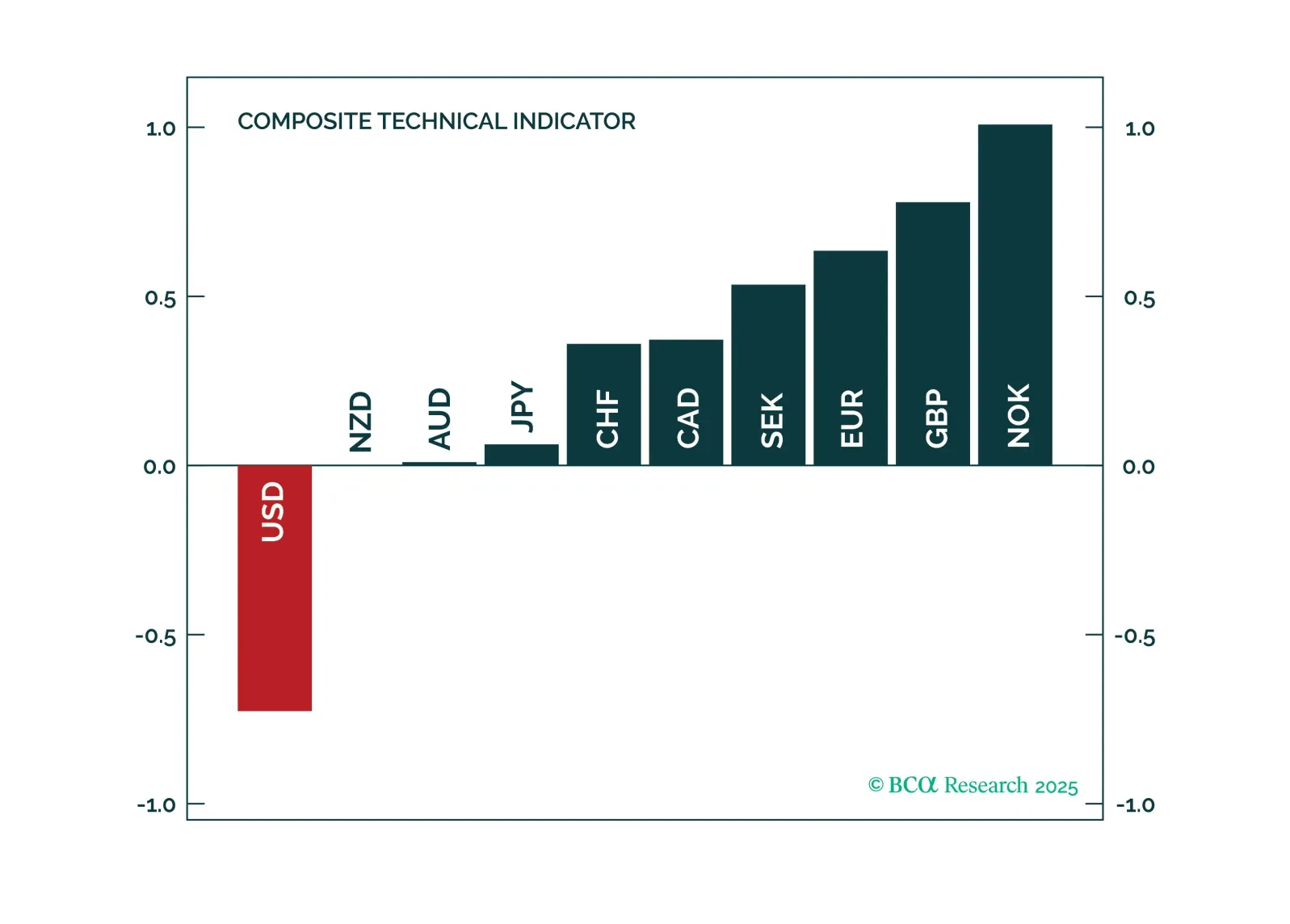

In this FX note, we provide a rationale for why it is important to pay attention to technical indicators, while still keeping your eyeball on the structural factors that drive currencies. This report answers the following questions: 1. Should you buy or sell the USD over a three-to-six month period from the pure lens of our proven technical indicators and 2. What are the best tactical cross trades among currencies.

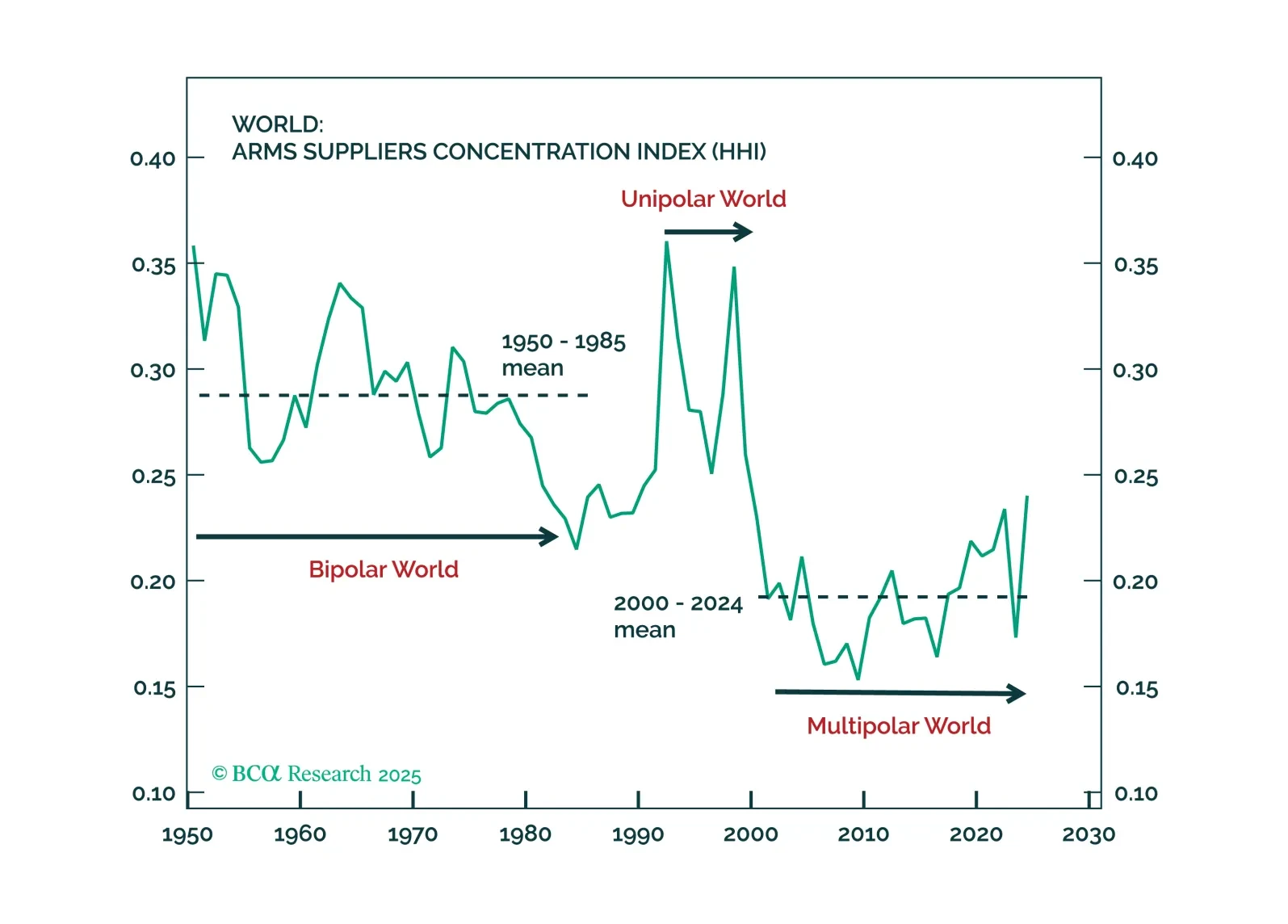

In our Beta report, we focus on our decade view. Many of our global allocator clients are scrambling to incorporate geopolitics into their strategic asset allocation. For most, this means thinking about war… or about future end-states. This is a mistake. We consider the next five years (maybe a decade) as the transition to the new era, a transition away from American unipolarity. And the transition itself is investment relevant. A transition to a multipolar world – which we think is occurring – will crush the USD and favor non-US assets. A transition to a bipolar world – not our base case, but still possible – would do the opposite.