Geopolitics

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.

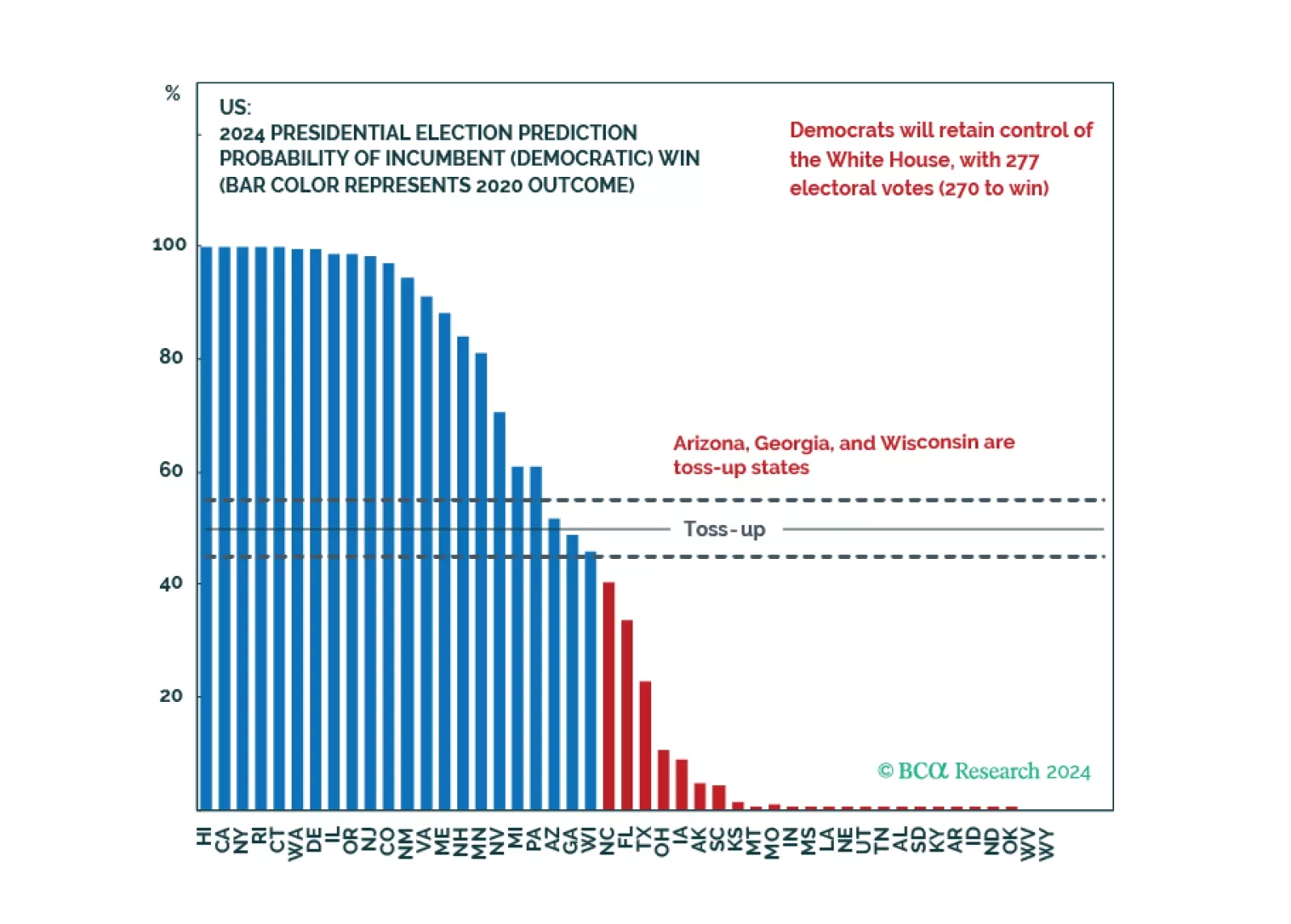

Though there are some positive signals recently for the Democrats, it is still hard for them to close the gap and turn things around. The Republicans are still favored to win the Senate as well as the House in the upcoming election.

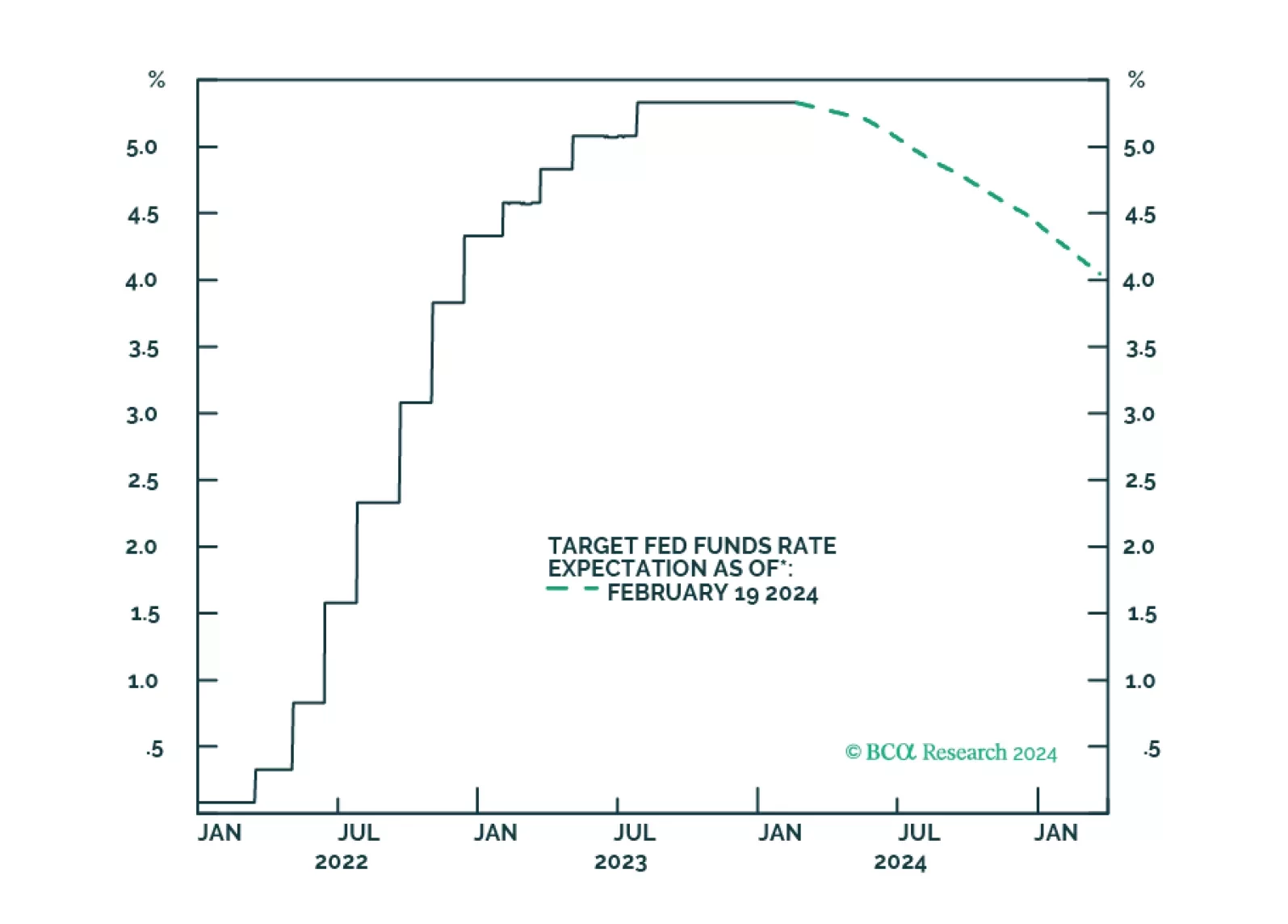

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.

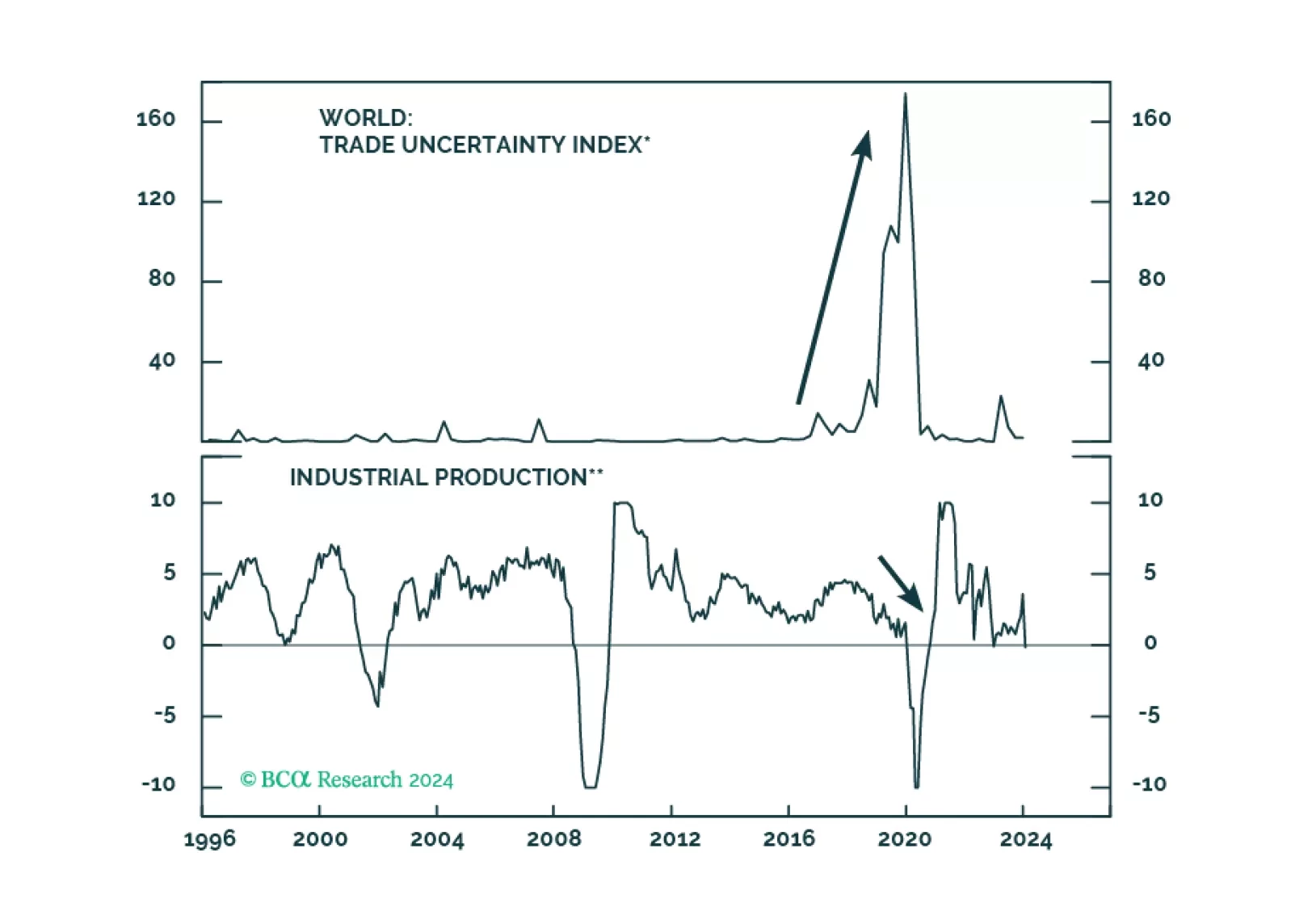

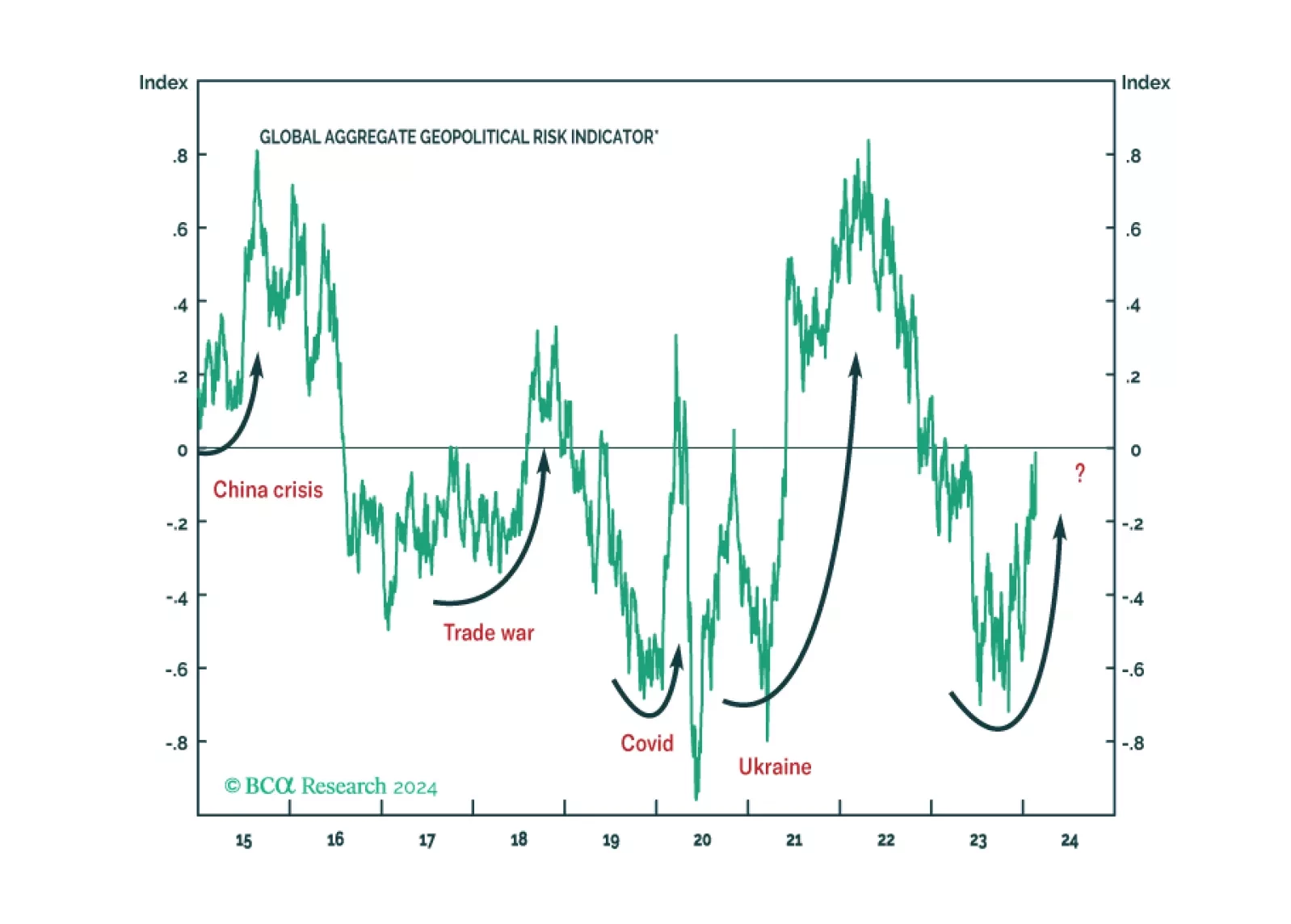

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

Democrats remain favored for reelection in 2024, which implies gridlock and policy status quo in 2025. That is not negative for stocks in the near term. However, economic, political, and geopolitical risks will escalate from here, causing volatility.