Fixed Income

The Thai economy has continued to underwhelm its ASEAN peers since the pandemic. It grew at a measly 1.5% in Q3 this year compared to the same period last year. Thai stocks and the currency have sold off as well. That said, the recently elected government…

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

The November US CPI release came in broadly in line with consensus expectations on Tuesday. On an annual basis, headline CPI inflation eased from 3.2% y/y to 3.1% y/y while core inflation was unchanged at 4.0% y/y. On a monthly basis, both headline and core…

According to BCA Research’s US Bond Strategy service, Treasury curve steepeners will pay off handsomely once the next recession hits. However, curve flatteners (aka barbelled Treasury portfolios) offer better value for the near term. A barbelled Treasury…

Our US fixed income team’s key investment views for 2024.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

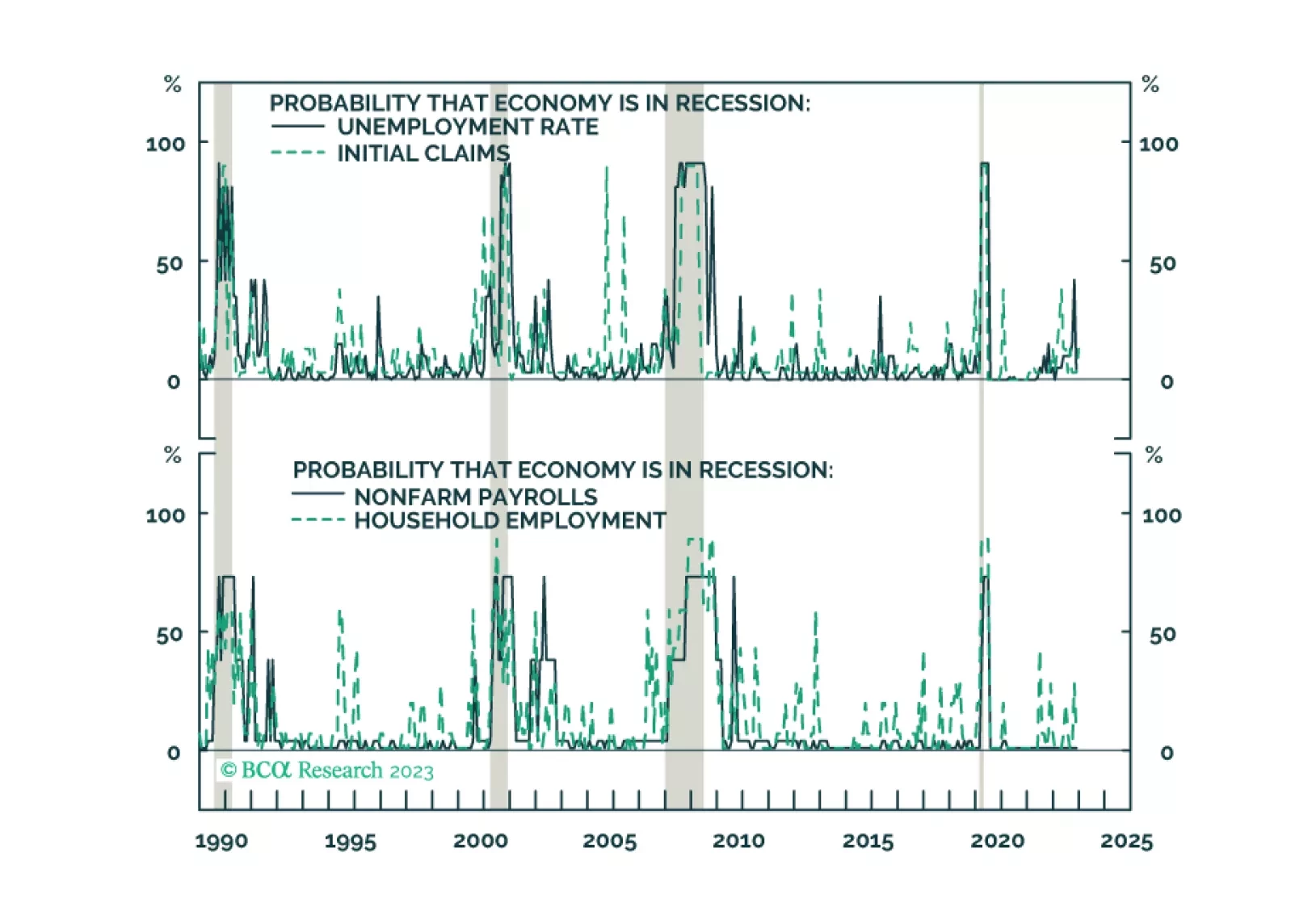

The US employment report delivered a positive surprise on Friday. Nonfarm payroll growth accelerated from 150 thousand to 199 thousand in November, beating expectations of 185 thousand. Importantly, the favorable result was corroborated by the unemployment…

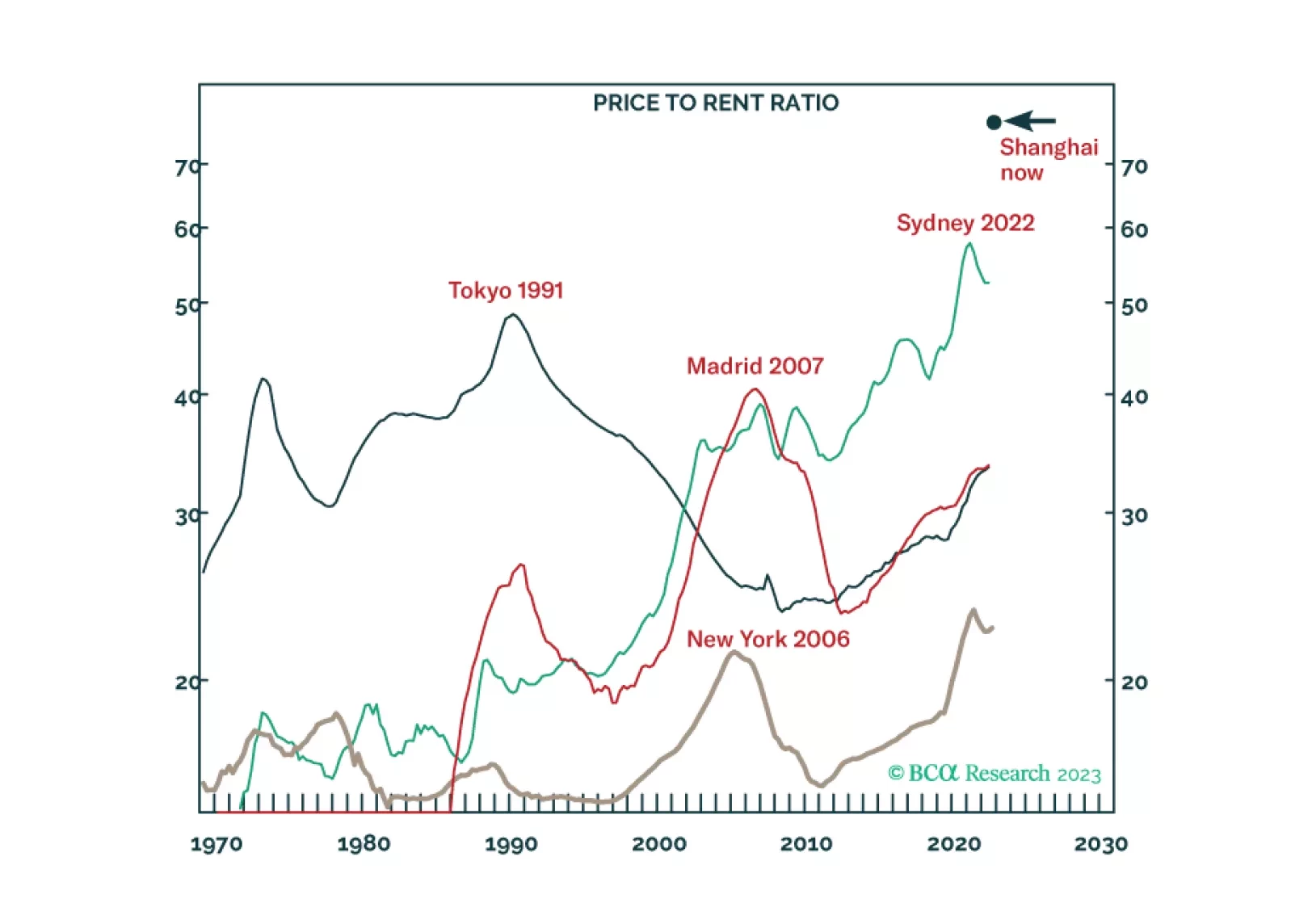

The global investment community has become well aware of many problems facing the Chinese economy including real estate excesses, policymakers’ reluctance to stimulate, as well as elevated debt levels among local governments, enterprises, and consumers. …

The Japanese yen strengthened considerably on Thursday after comments by Bank of Japan (BoJ) Governor Kazuo Ueda caused investors to bring forward their expectation of the timing of the end of negative rates. In particular, Ueda noted that monetary policy…