Fixed Income

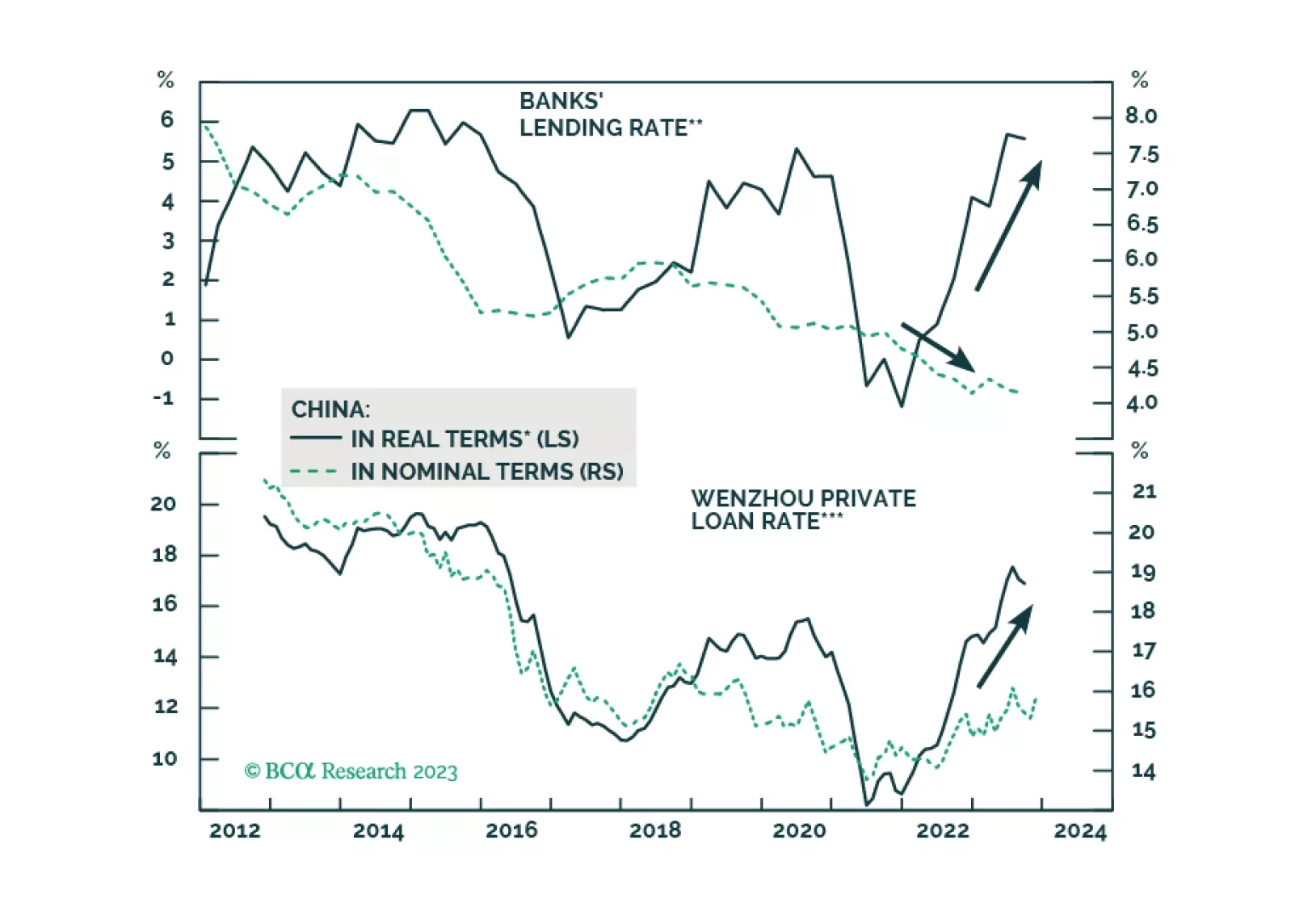

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

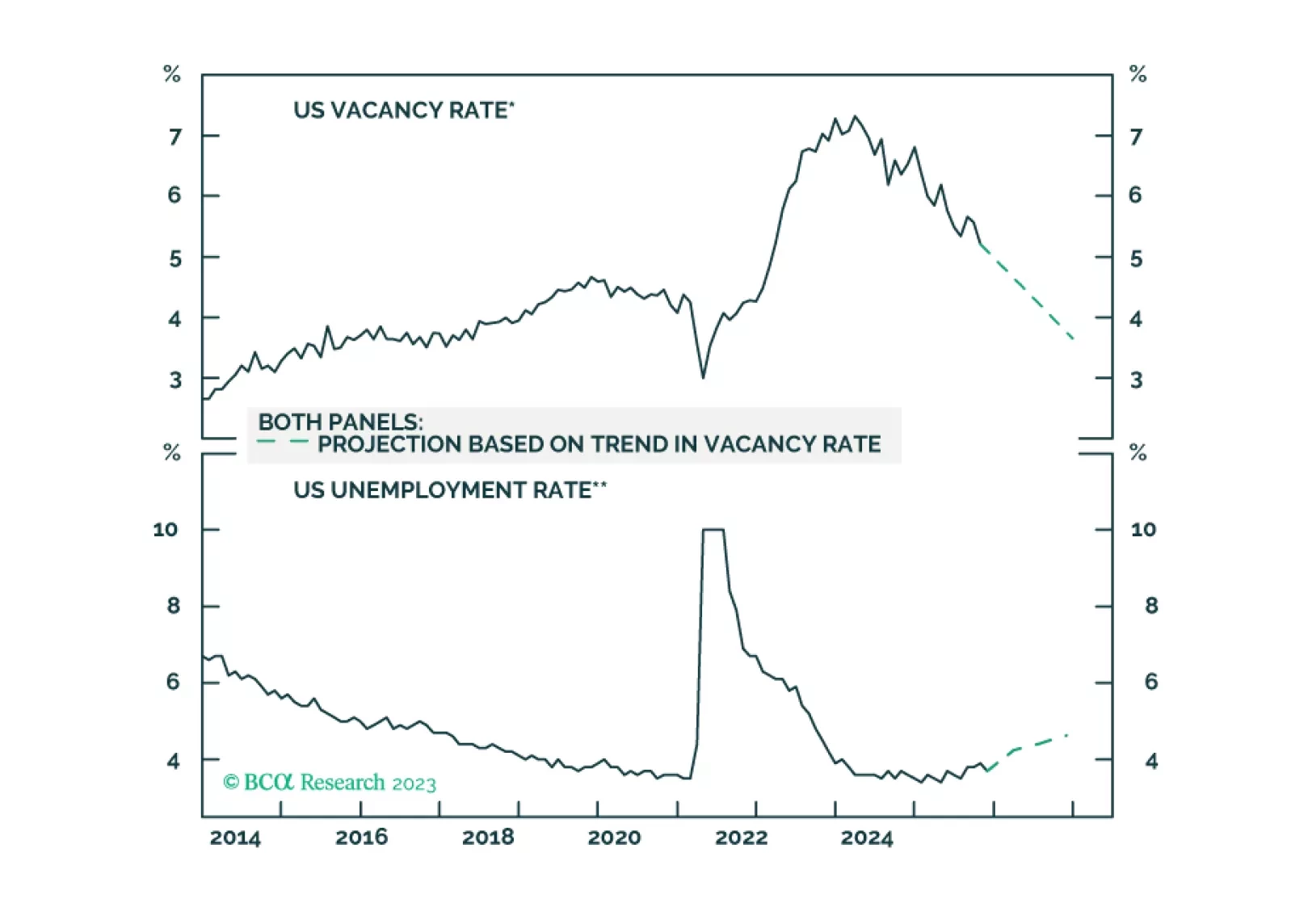

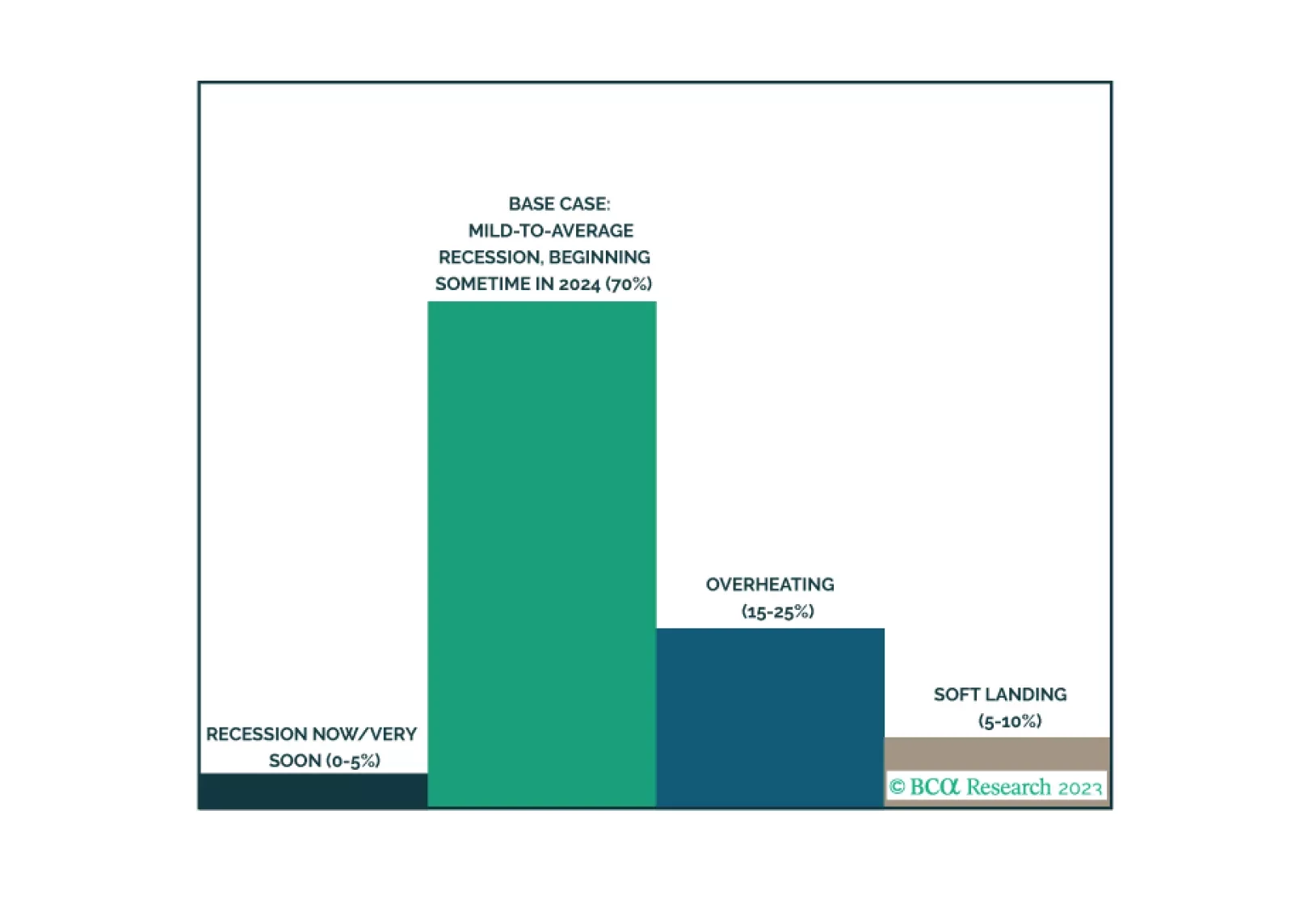

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

Explore the eight main themes that will drive the returns of European assets in 2024.

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.