Fixed Income

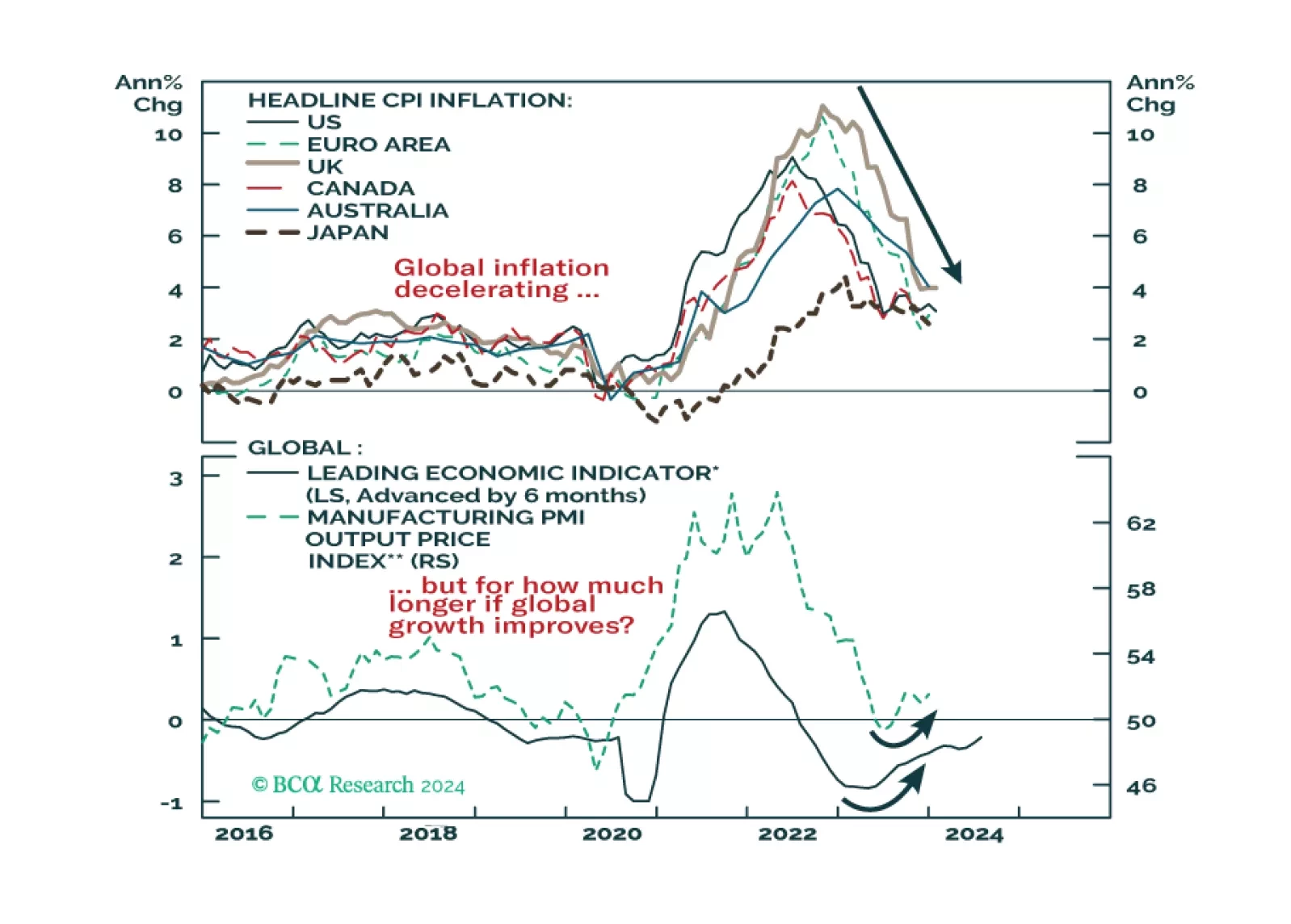

Could a second wave of global inflation be underway? The latest inflation prints in the US and UK showed upside surprises, while there is evidence of increased price pressures in global manufacturing. Combined with the improvements seen in economic sentiment measures and leading economic indicators in the US and Europe, and potential upside risks to oil prices, we see a strong case for owning more inflation protection in global bond portfolios. Inflation-linked bonds look attractive in this environment, especially in the US.

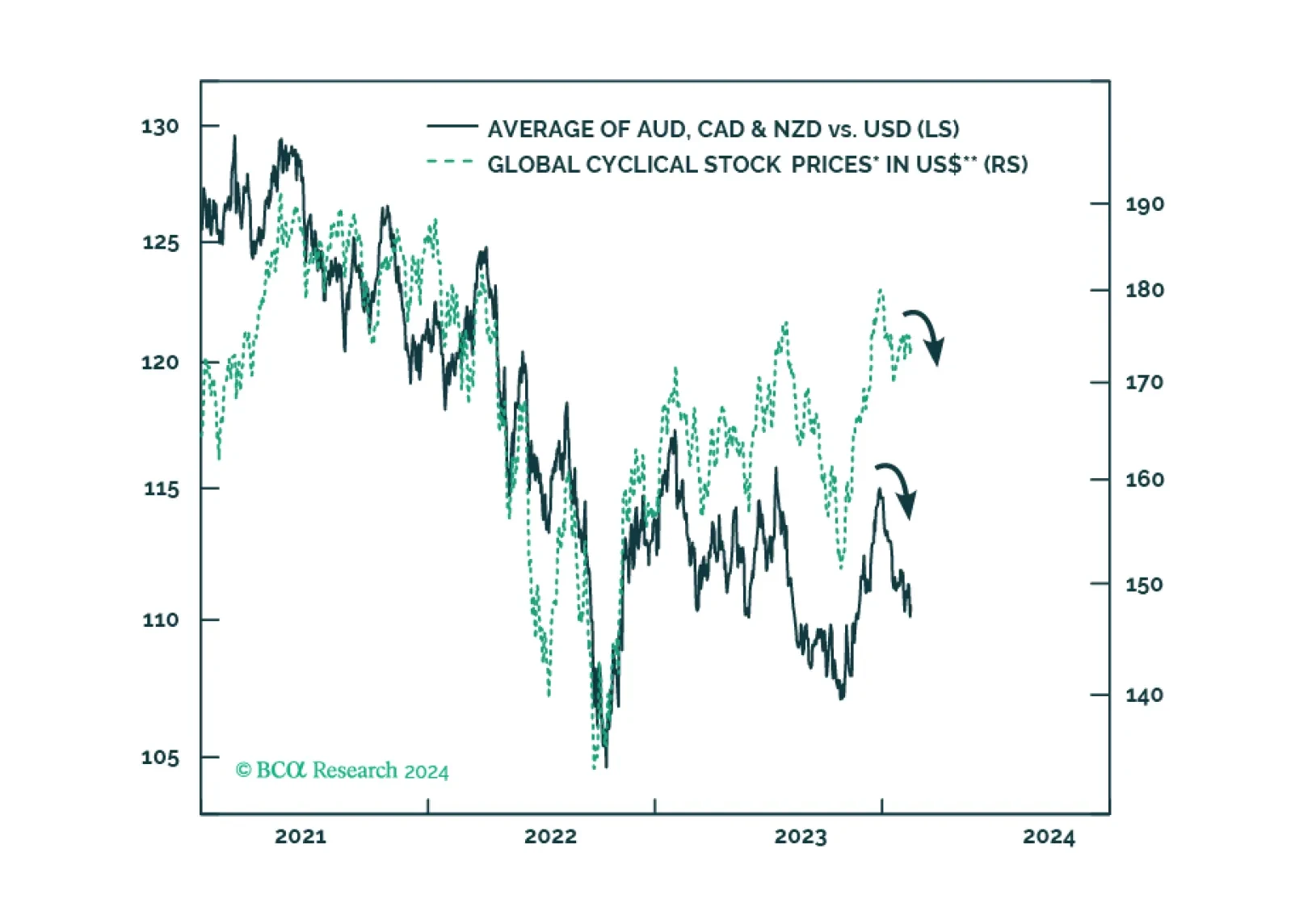

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.

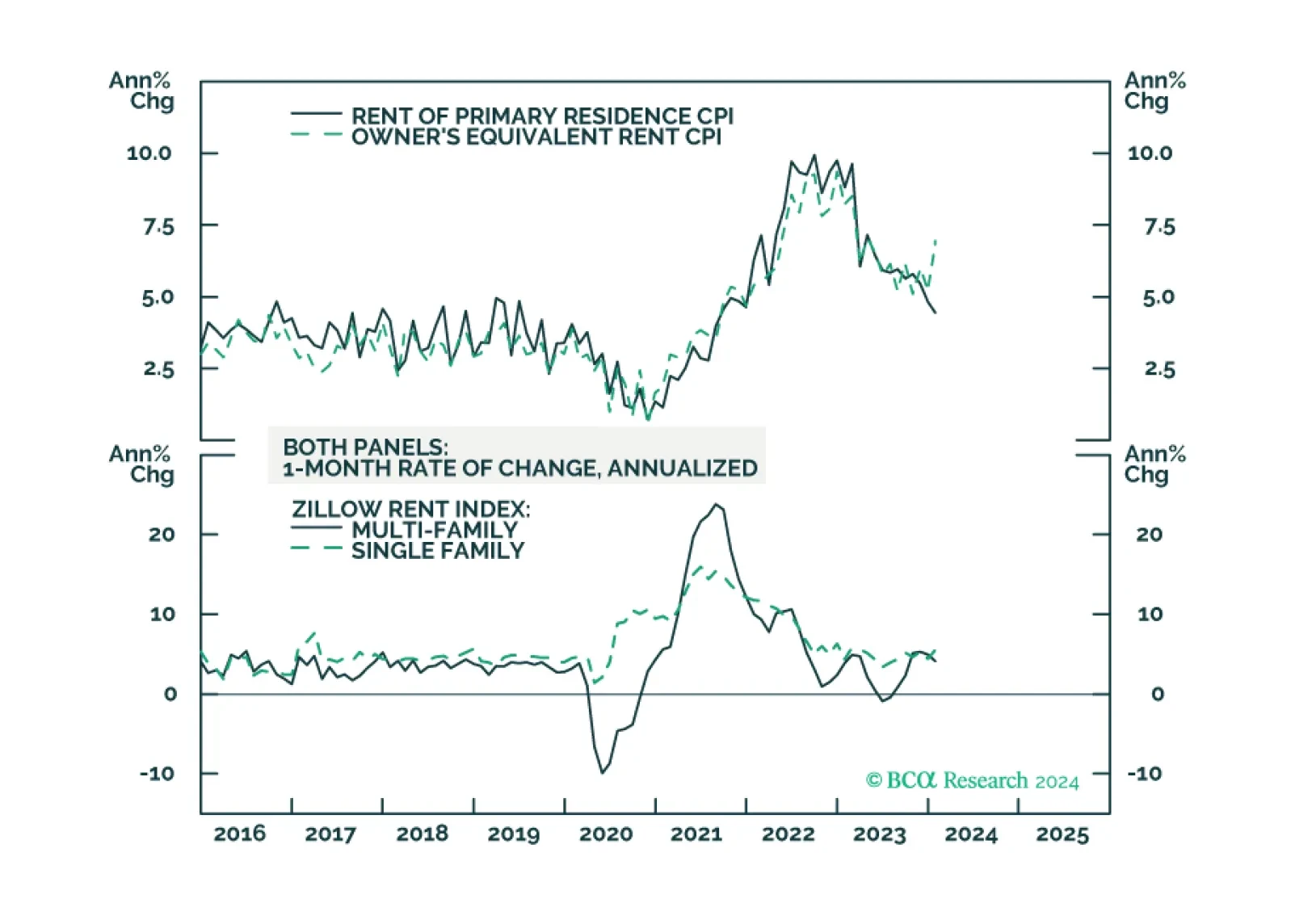

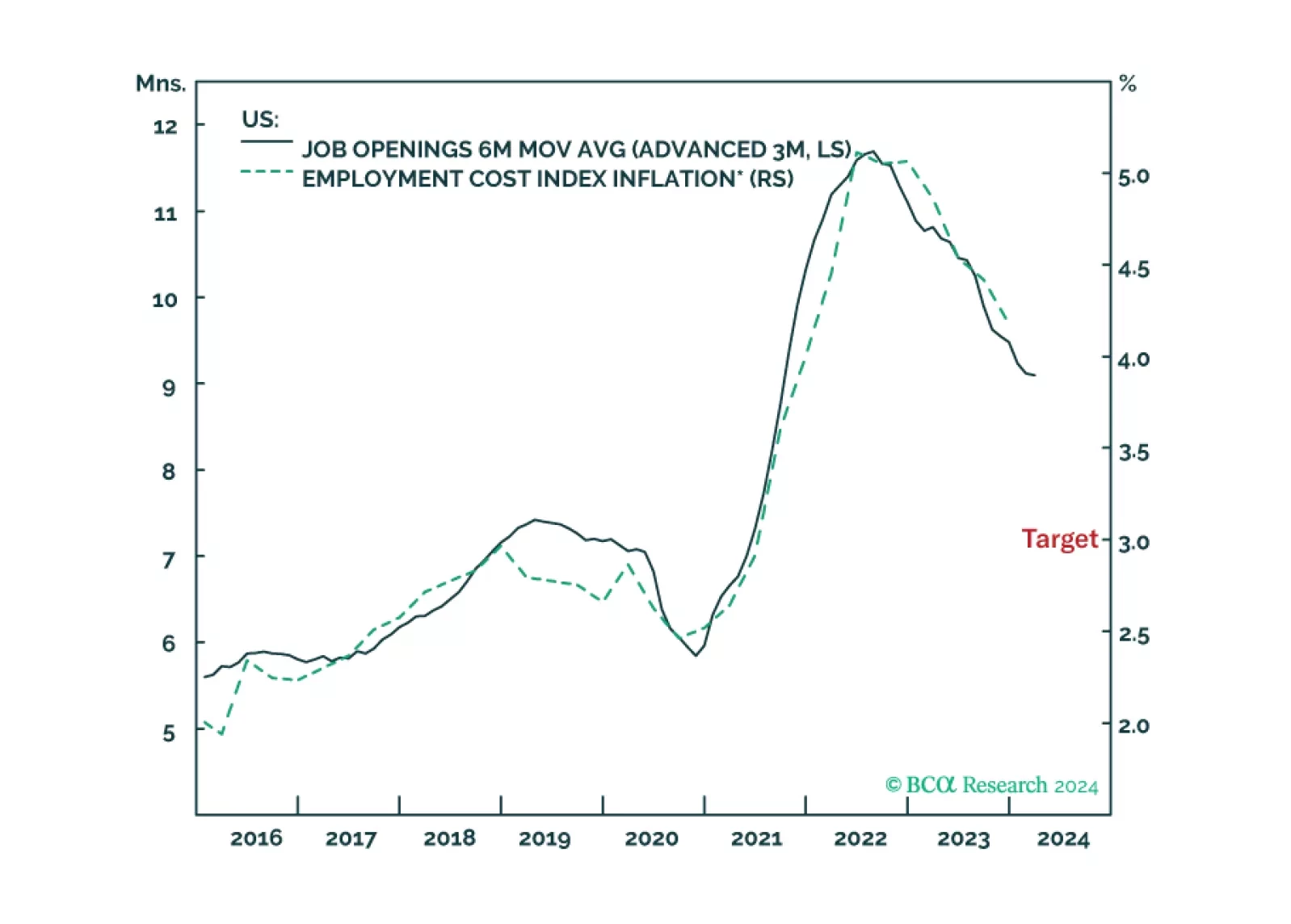

The disinflation to date has been benign because it has come almost entirely from improving supply. But the supply-side tailwind has exhausted, so the last mile of the journey to 2 percent inflation will be the hardest, especially in the US and the UK. We discuss the investment implications. Plus, we highlight an interesting sector pair-trade.