Fixed Income

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less than the moderation embedded in…

According to BCA Research’s European Investment Strategy service, the domestic picture indicates that Bund yields will stay rangebound over the next few months due to the tug-of-war between bond bullish and bond bearish forces in Europe. For now, the…

According to BCA Research’s Global Investment Strategy service, the BoC should have sufficient evidence of Canadian disinflation to cut rates this summer. The market is pricing in a similar amount of rate cuts for the BoC and the Fed over the next 12 months.…

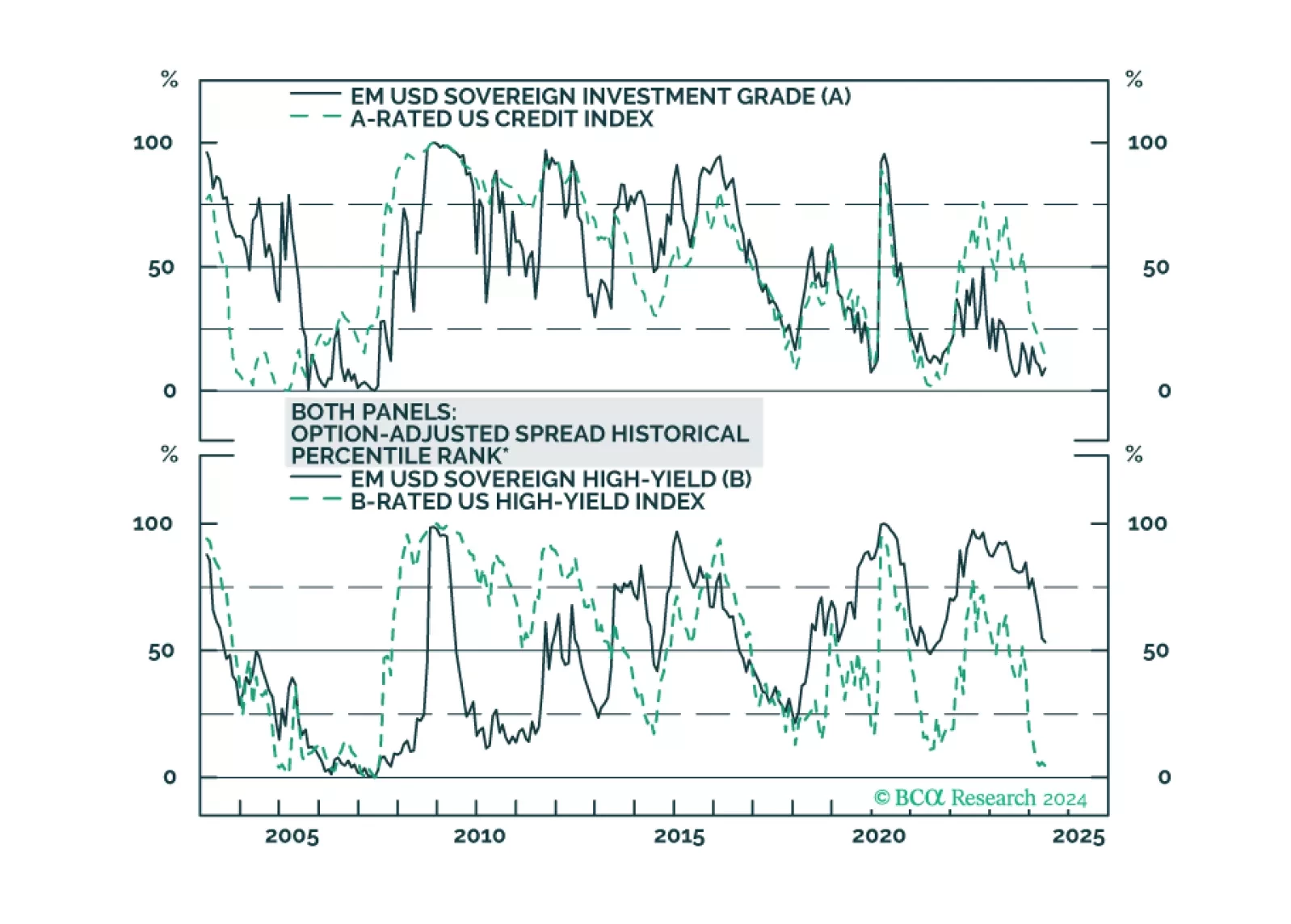

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

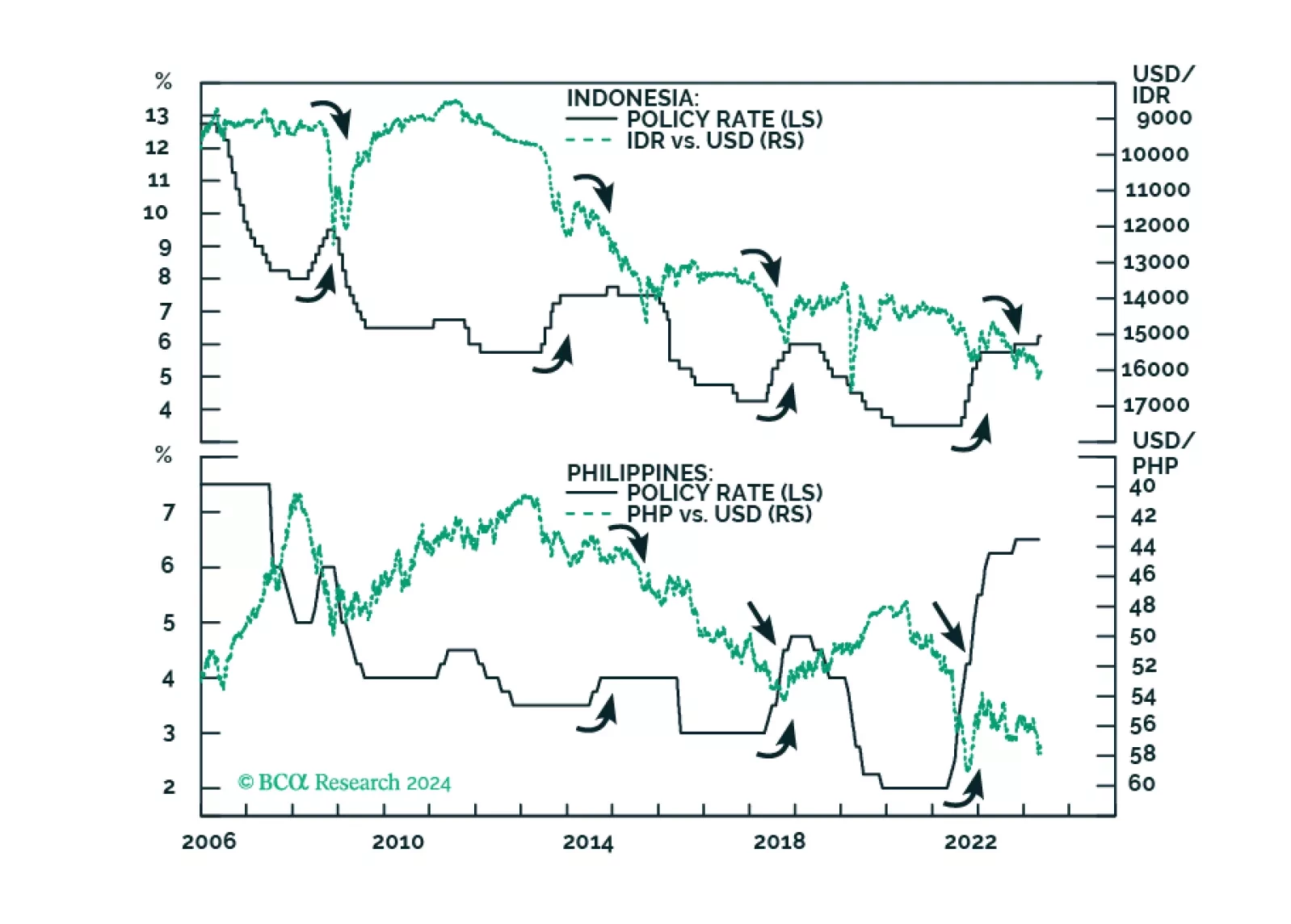

ASEAN stocks and currencies will weaken further as these economies face multiple headwinds. Raising policy rates did not stop a sliding currency in the past, it is unlikely to do so now.

US industrial production stalled in April against expectations of a moderate pace of growth (0.1% m/m) and March’s growth rate was revised lower from 0.4% m/m to 0.1% m/m. Notably, pro-cyclical manufacturing production unexpectedly contracted 0.3% m/m from a…

The rally in gold continues and spot prices flirted with their all-time highs last week. Interestingly, these gains have occurred despite the rise in real yields, with which they are usually strongly inversely correlated. Physical demand for gold has…

Credit spreads continue to price in a Goldilocks scenario. US investment grade and high-yield OAS have tightened 41 and 137 bps from their October peaks, resulting in handsome outperformance by both sectors relative to duration-equivalent Treasuries. …

US headline CPI inflation decelerated to a softer-than-expected 0.3% m/m (3.4% y/y) in April, from 0.4% m/m (3.5% y/y). Core CPI eased from 0.4% m/m (3.5% y/y) to 0.3% m/m (3.4% y/y). Declines in new (-0.4% m/m) and used vehicles (-1.4% m/m) prices largely…

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.