Fixed Income

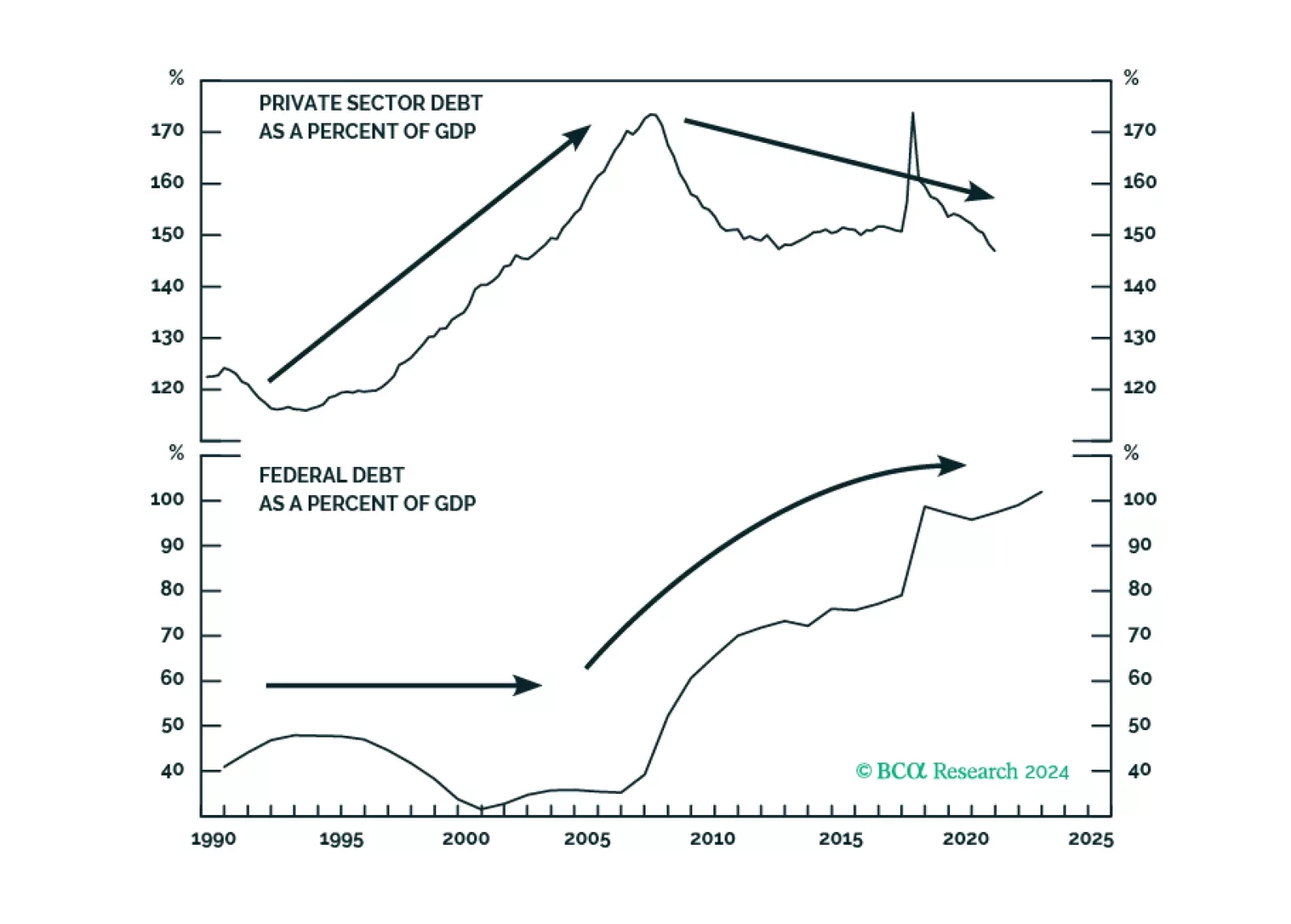

In a guest research report, Martin Barnes, BCA’s former Chief Economist, revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.

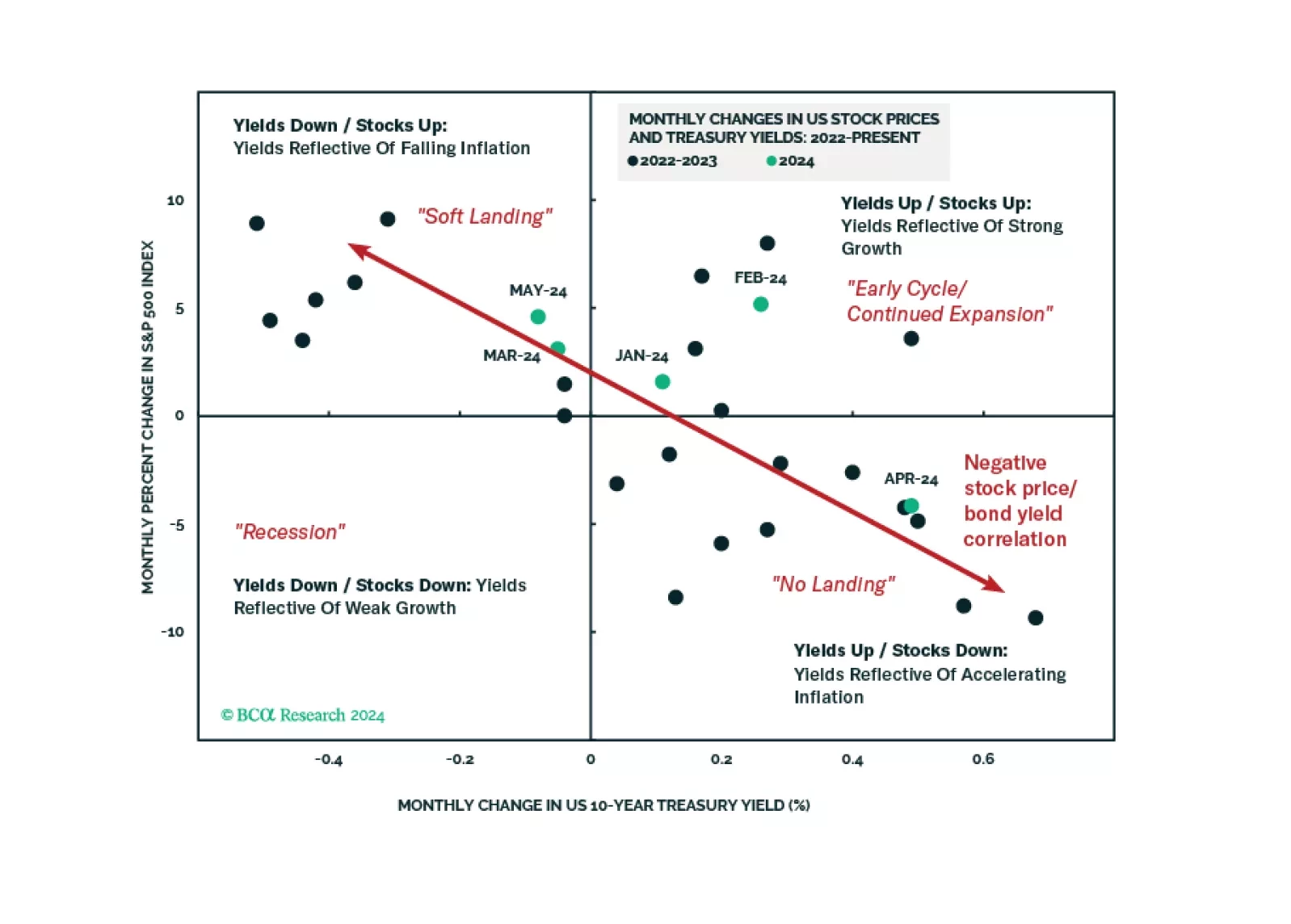

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.

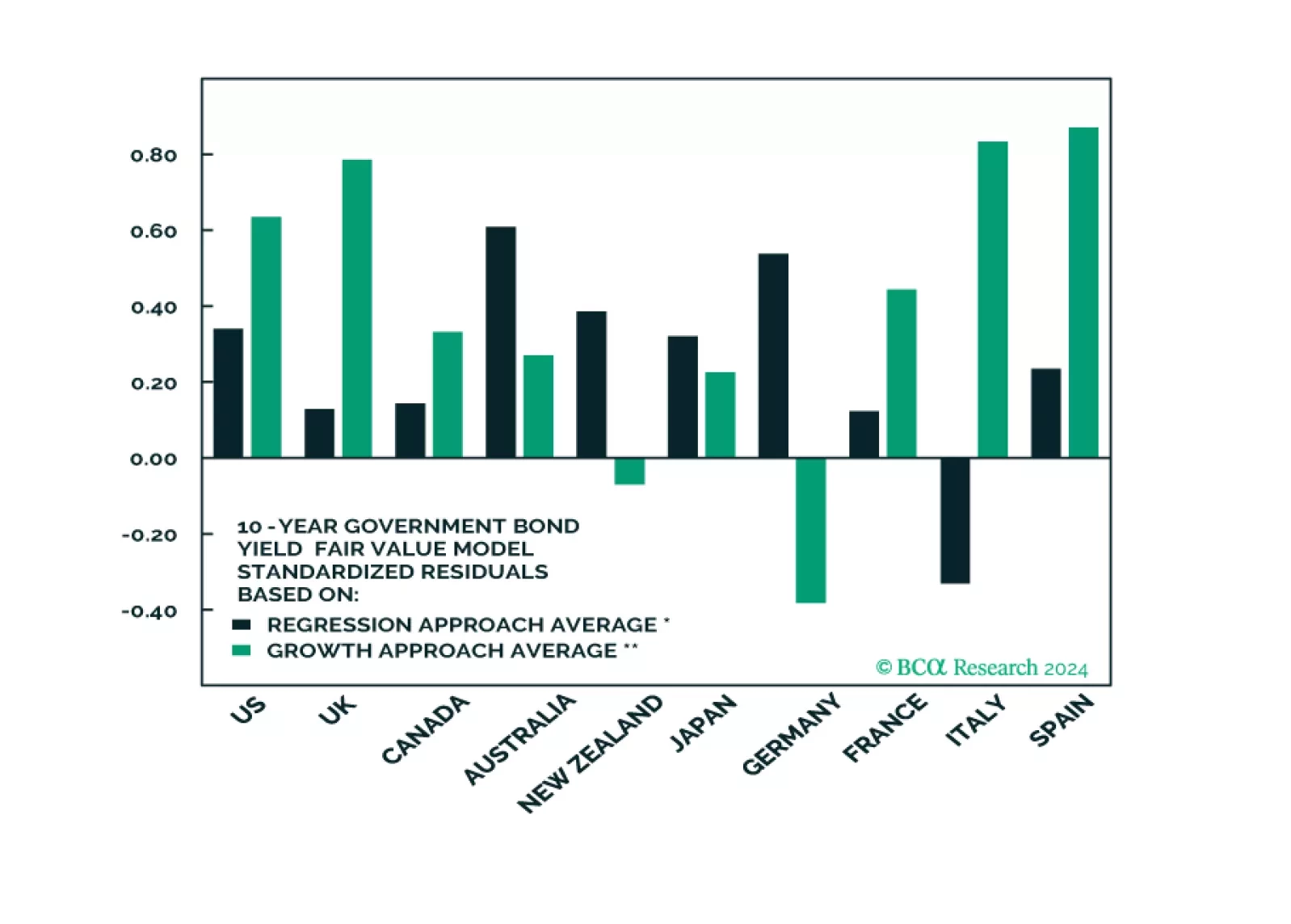

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

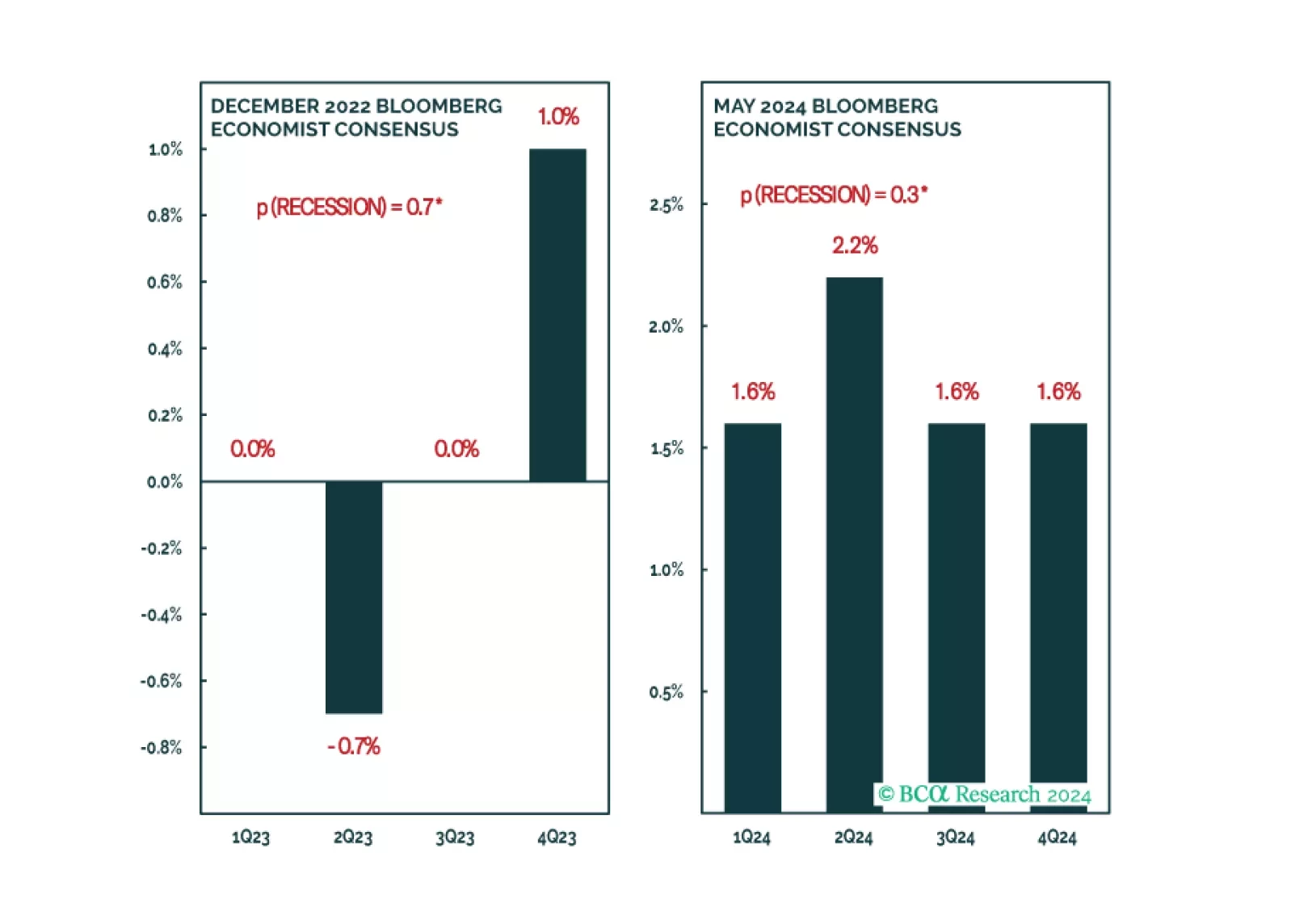

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

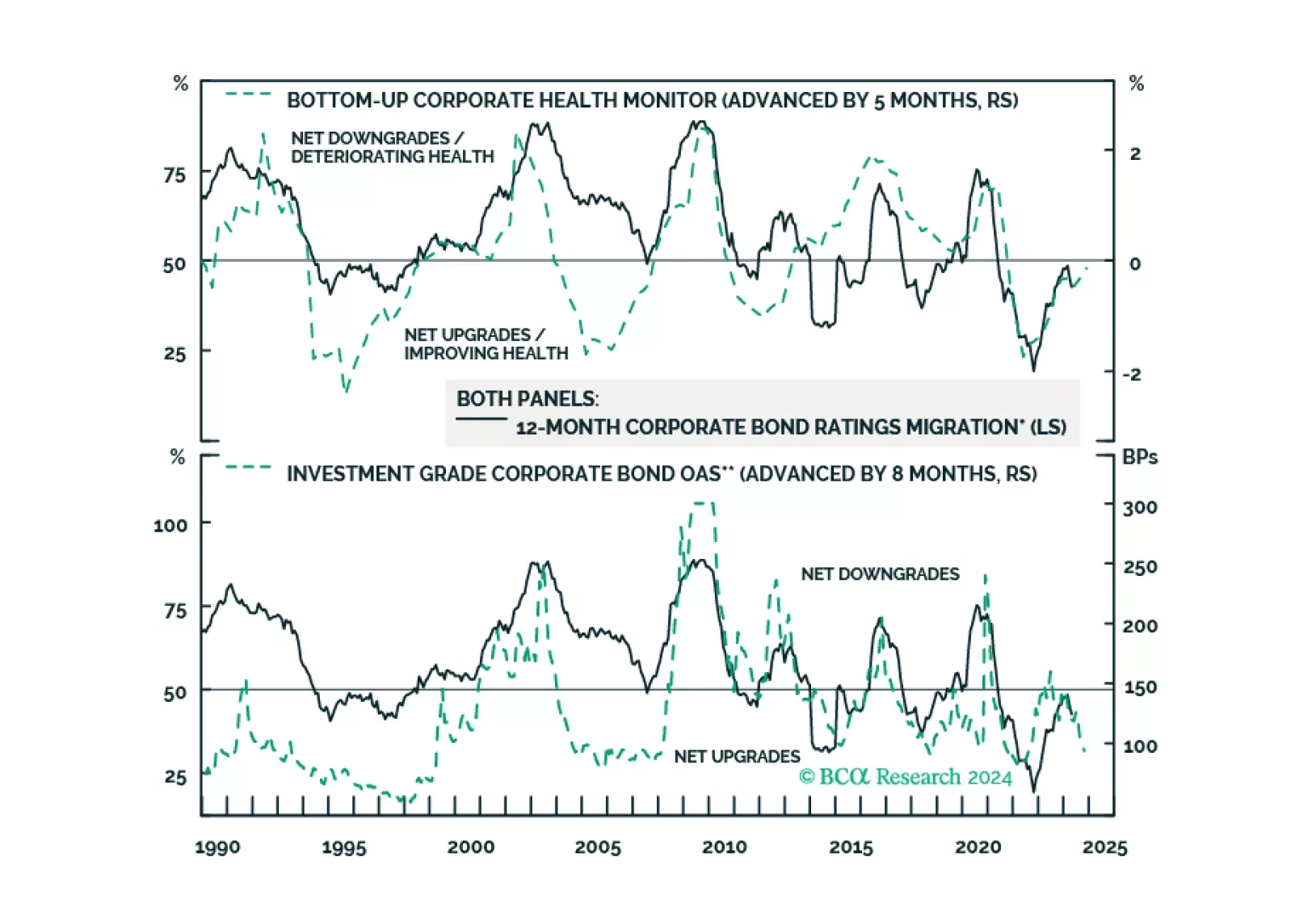

Nonfinancial corporate balance sheets are generally in good shape, but there are signs of deterioration at the bottom-end of the credit spectrum. We present evidence showing that credit deterioration at the bottom-end of the credit spectrum has a habit of migrating upwards.

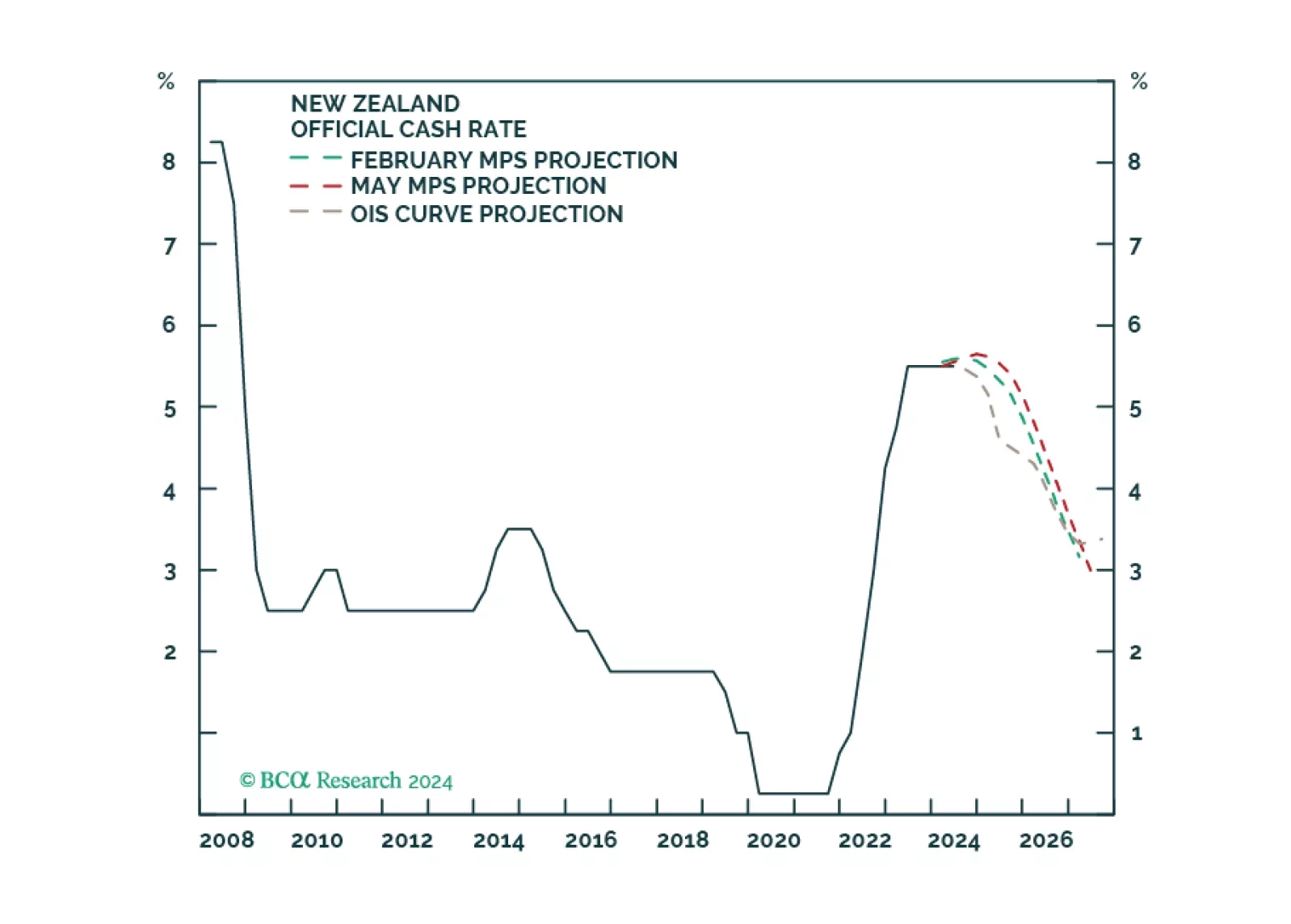

In this Insight, we revisit our "higher for longer" theme for the Reserve Bank of New Zealand, in light of the latest central bank meeting. In conclusion, we are inching towards a more dovish RBNZ ahead. Ergo, we recommend some fixed income and currency trades.