Fixed Income

This report looks at the likely path for the dollar and bond yields over the next 6-to-12 months.

The bond market priced out a lot of recession risk after this morning’s employment report, and the 10-year Treasury yield has moved back into the Soft Landing Zone. We assess the data and consider whether we need to change our cyclical positioning.

TIPS outperformed duration-equivalent nominal Treasuries by 86 bps so far in 2024 and our US bond strategists downgraded their allocation from neutral to underweight this week. The 10-year TIPS breakeven inflation rate remains comfortably in the middle of…

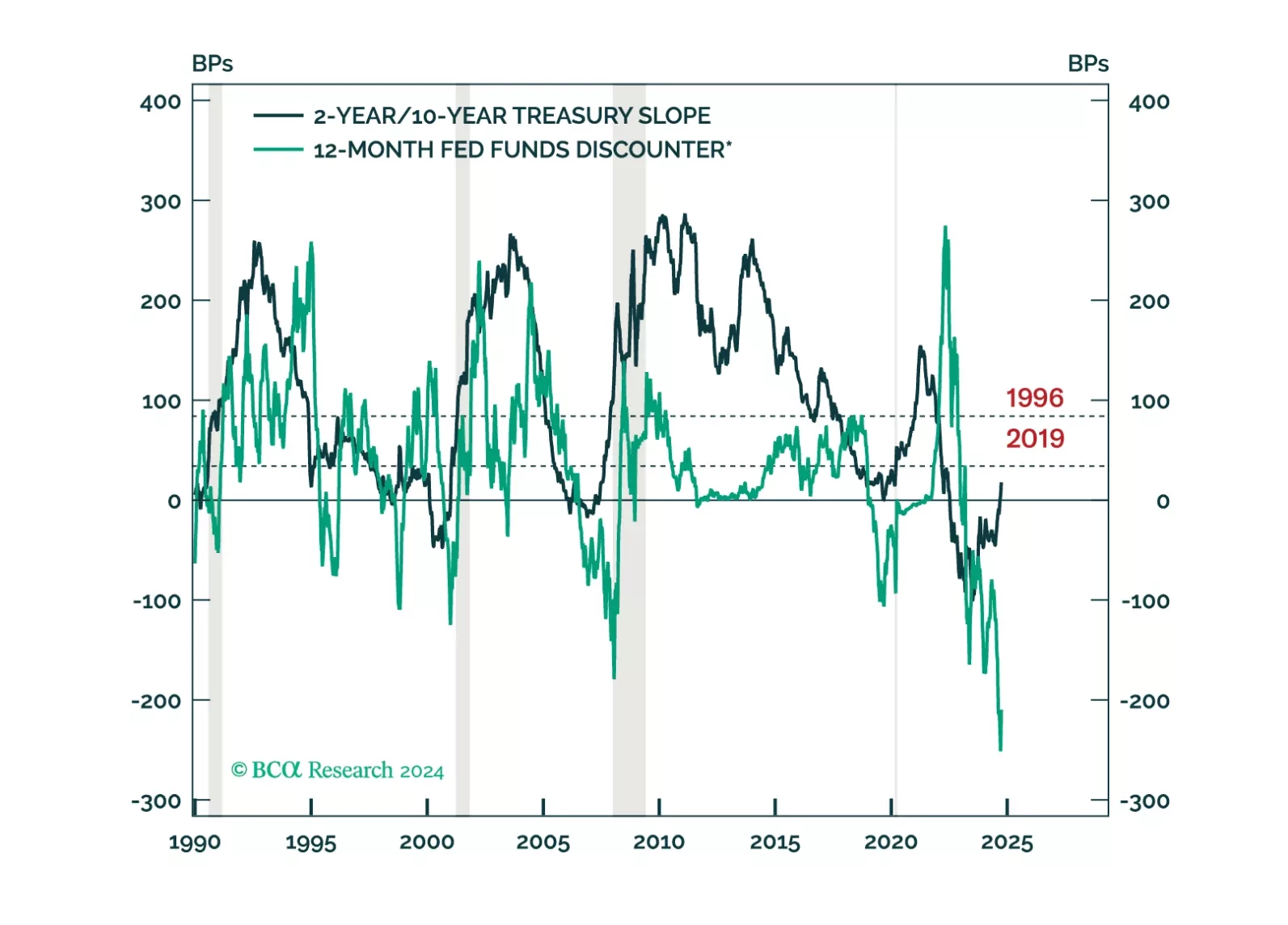

According to BCA Research’s Global Investment Strategy service, the consensus expectation of a soft landing is wishful thinking. Many investors have pointed to the mid-1990s as an example of when Fed easing paved the way for an economic boom.…

Our Portfolio Allocation Summary for October 2024.

The ISM manufacturing PMI remained constant in September at 47.2, against expectations of a slower pace of decline and extending a six-month contraction streak. Measures of production and domestic demand decelerated at a notably slower pace while foreign…

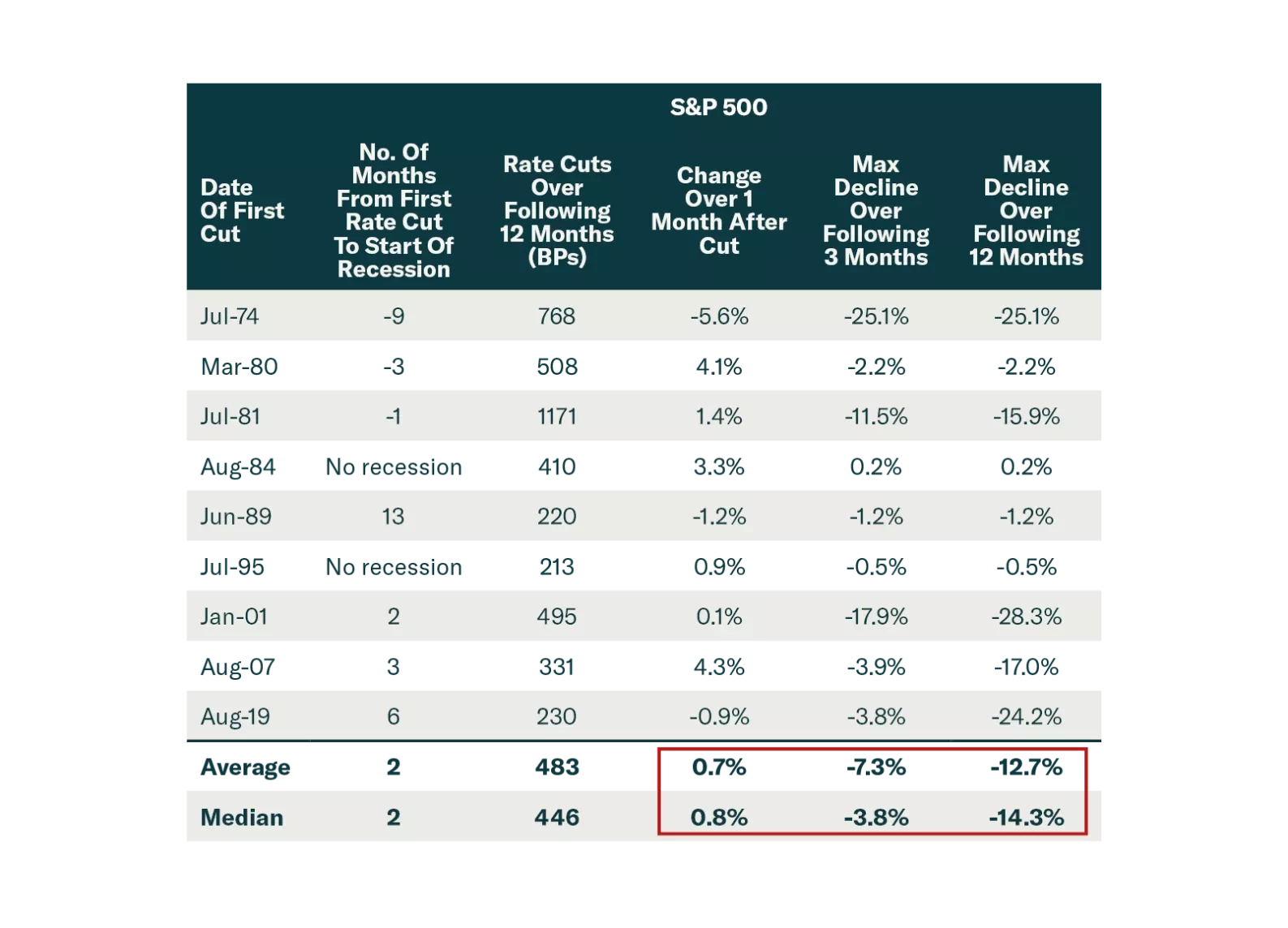

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.

US nominal personal income growth decelerated to a 0.2% pace in August, from 0.3% in July, missing expectations that it would accelerate. Nominal personal spending also disappointed, growing at a slower 0.2% pace from 0.5%. In real terms, spending barely…

France’s and Spain’s preliminary September CPI readings declined on a month-on-month basis, clocking in at 1.5% and 1.7% y/y respectively, and undershooting consensus expectations. Germany’s and Italy’s updates are due on Monday and the Eurozone CPI will be…

Annual BEA data revisions resulted in a significant upward revision in GDP growth since Q2 2020, led by stronger consumption growth and more robust real disposable income growth than previously believed. Revisions also show that the savings rate has been…