Fiscal Policy

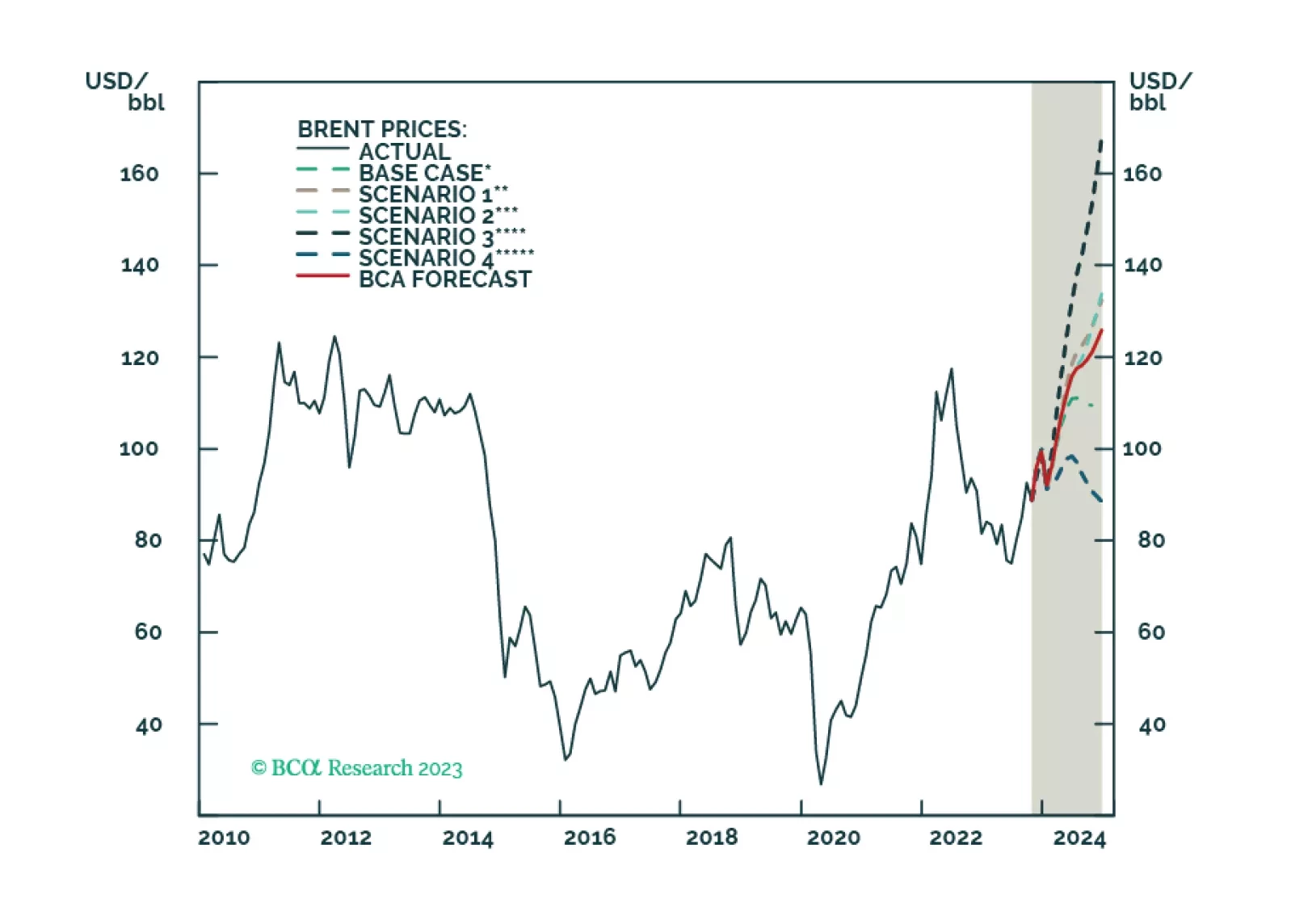

US and Chinese oil-demand strength will offset EU weakness next year. Incremental supply growth from non-OPEC 2.0 producers, coupled with a lower risk of the US enforcing its sanctions on Iranian oil exports, reduces our 2024 Brent price forecast by $6/bbl, and takes it to $112/bbl.

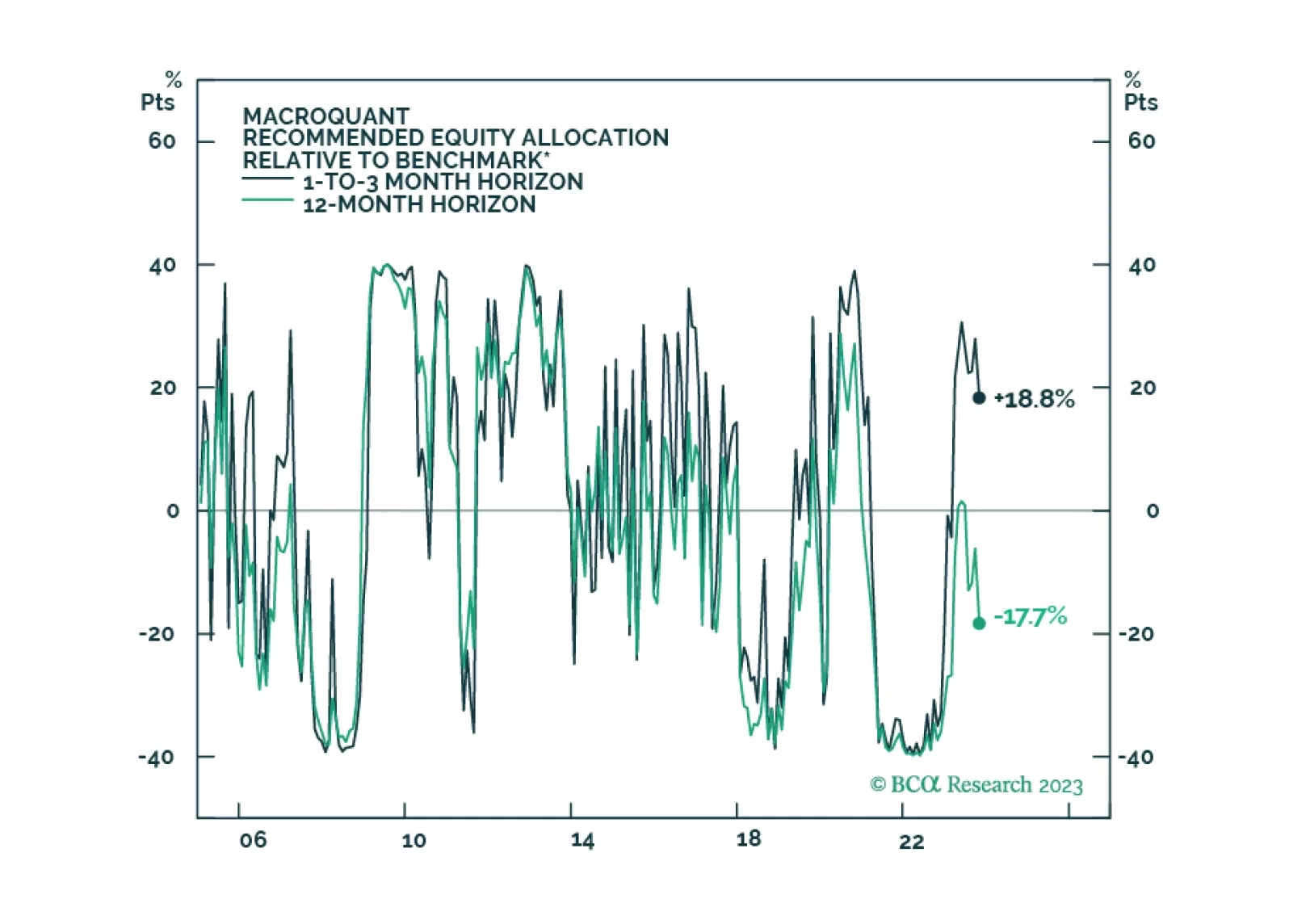

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

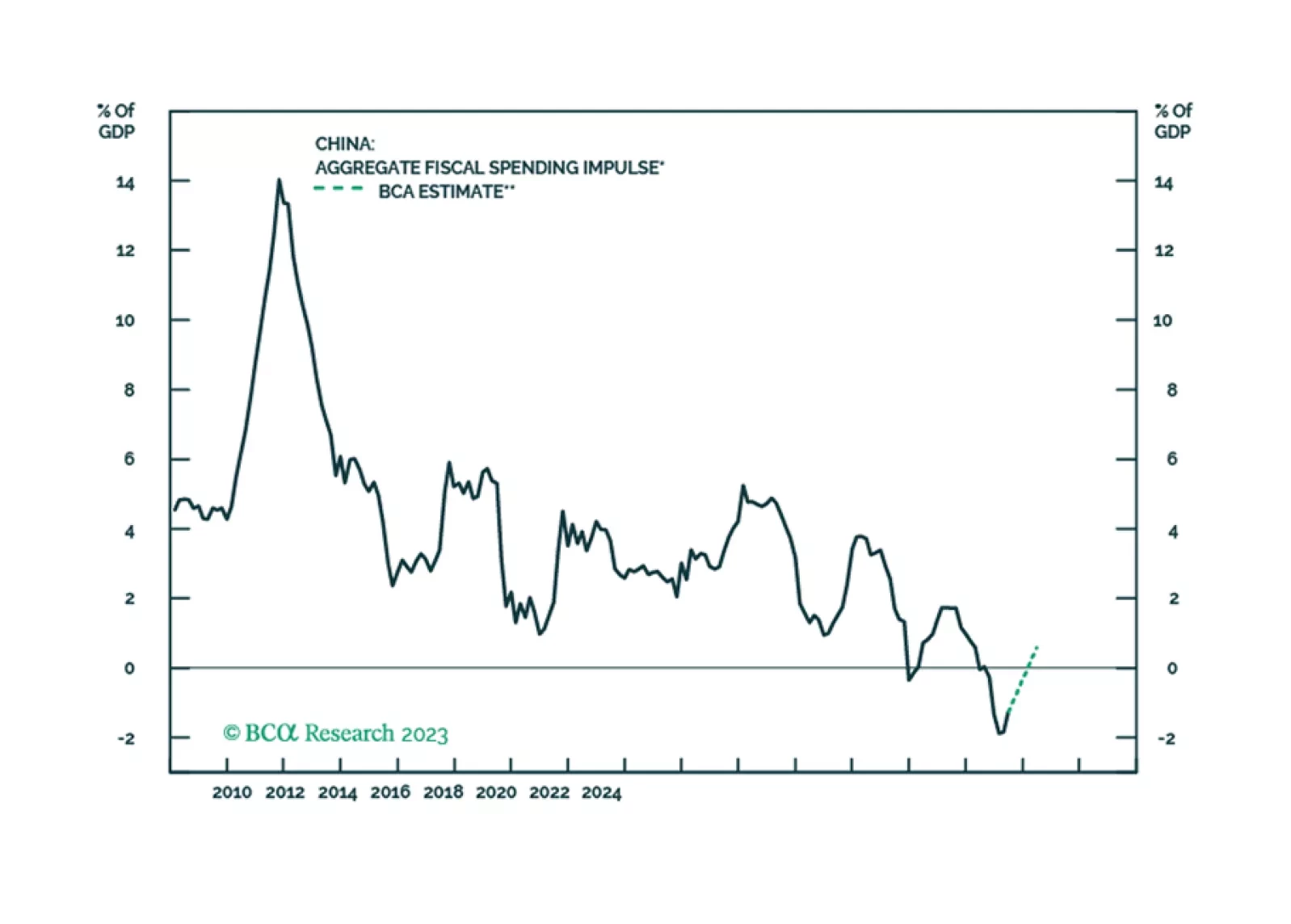

We maintain our view that China’s economic growth in the coming months will remain lackluster. Beijing's recent measures to provide additional financing may help to bridge the gap in government spending in the rest of 2023 and into 2024, but the impact on growth will be very limited.

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

The market has been held hostage by surging rates. Zombie companies are “alive” and are multiplying – they are highly sensitive to surging borrowing costs. Underweight Utilities to reduce portfolio duration. Maintain neutral positioning of Basic Materials but take a granular approach to allocations within the sector.

The bear market in US bonds will likely end with a bang rather than a whimper. Even during the secular US bond bull market of 1982-2021, cyclical bond bear markets ended only after an eruption of financial turmoil. It would be strange if this current ascent in bond yields ended without significant casualties in the global financial system.

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.

US fiscal, monetary, and foreign policies are unlikely to deliver any dovish surprises for investors in Q4, due to the impending government shutdown, persistent inflation, and instability among OPEC+ and China.

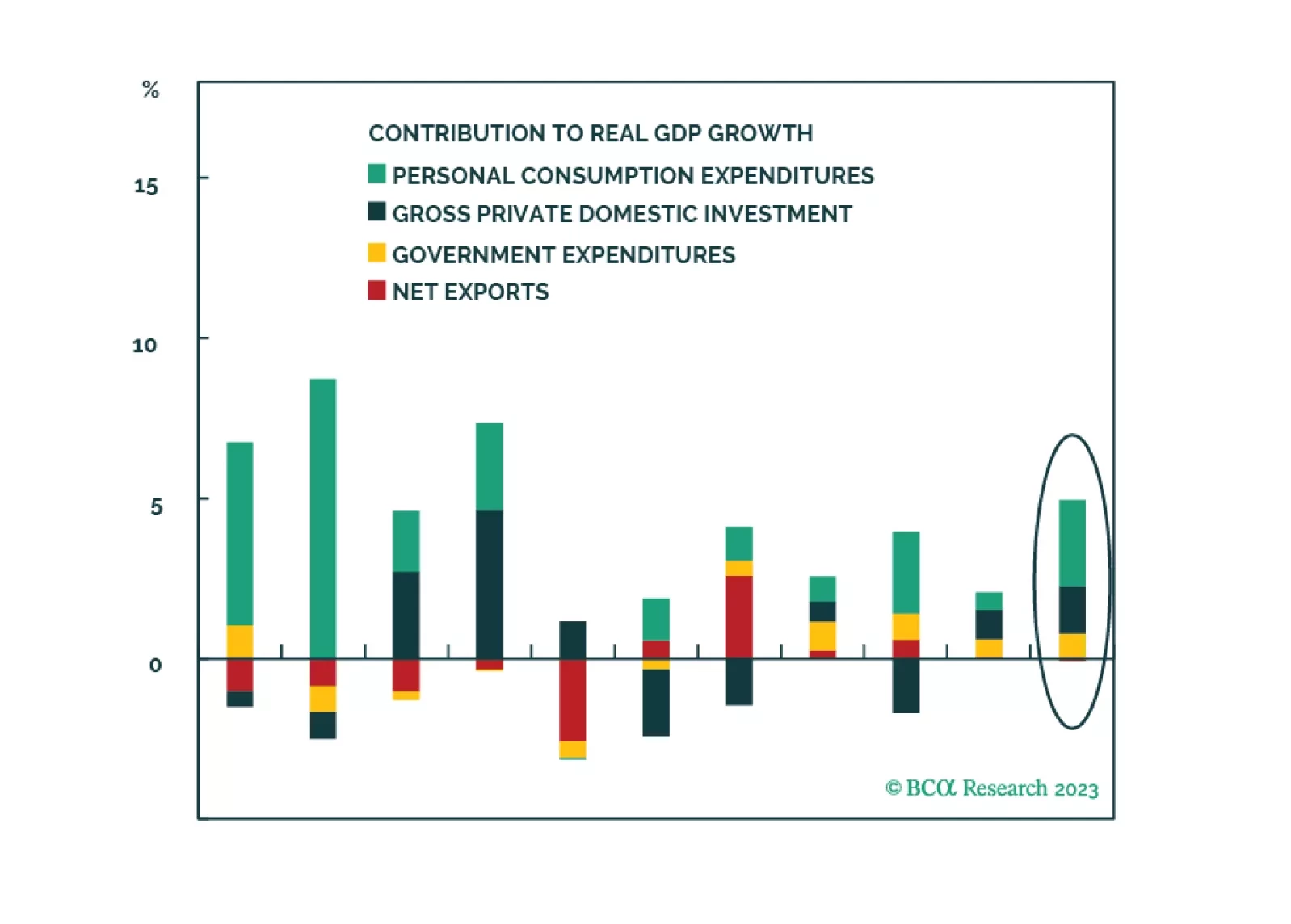

The global downturn will be shallower than it was in 2008 and in 2020 but will last for longer. The primary reason for a more prolonged downturn is that policymakers in the US, Europe, and China will be reluctant to proactively and aggressively stimulate. The combination of rising oil prices, an appreciating US dollar, and mounting US bond yields constitutes a triple whammy for US share prices.

The CCP’s fiscal measures and property-market support are important steps to deal with China’s liquidity trap. The fiscal measures are the first such direct aid to households and small firms seen since 2020, which included tax relief and waived social security contributions, according to the IMF. The size of the programs has not been disclosed. If they are successful, global commodity demand will get a boost at the margin, particularly oil and base metals. We remain long equity ETFs to retain exposure to energy and metal producers and refiners, and long the COMT ETF for direct commodity exposure.