Fiscal Policy

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

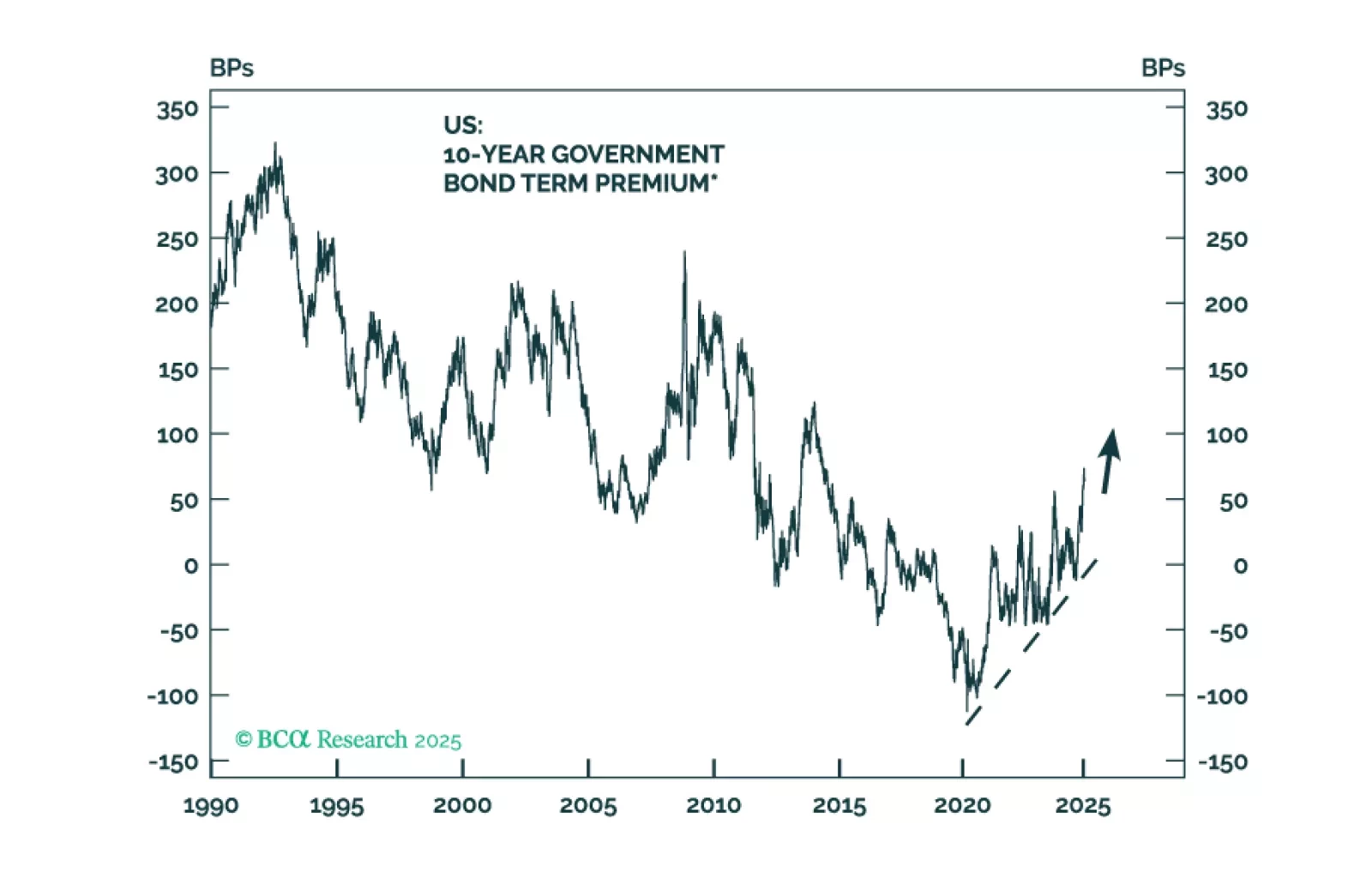

This is a follow-up report on Bessenomics – the policy mix that US Treasury Secretary Scott Bessent plans to pursue. The direction of US and global financial markets depends on the amount of fiscal tightening required to bring down US interest rates. Can the Trump administration cut fiscal spending just enough to bring down US bond yields but not cause a recession?

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

This month, our Here, There, And Everywhere chartpack reiterates our main thesis for 2025: the three main narratives driving markets today – fiscal profligacy, trade war, and geopolitical conflict – will peak at some point in 2025. Why does this matter? All three have been tailwinds to US assets, and their peak should help usher in the peak in US outperformance relative to RoW. We conclude with some slides on our bullish Europe thesis.

To produce a moderate economic recovery, at least RMB 3 trillion in additional government expenditures is needed in H1 2025. Our bias is that Beijing is not yet ready to launch such a massive fiscal support measure. Hence, volatility-adjusted equity returns in China will be poor.

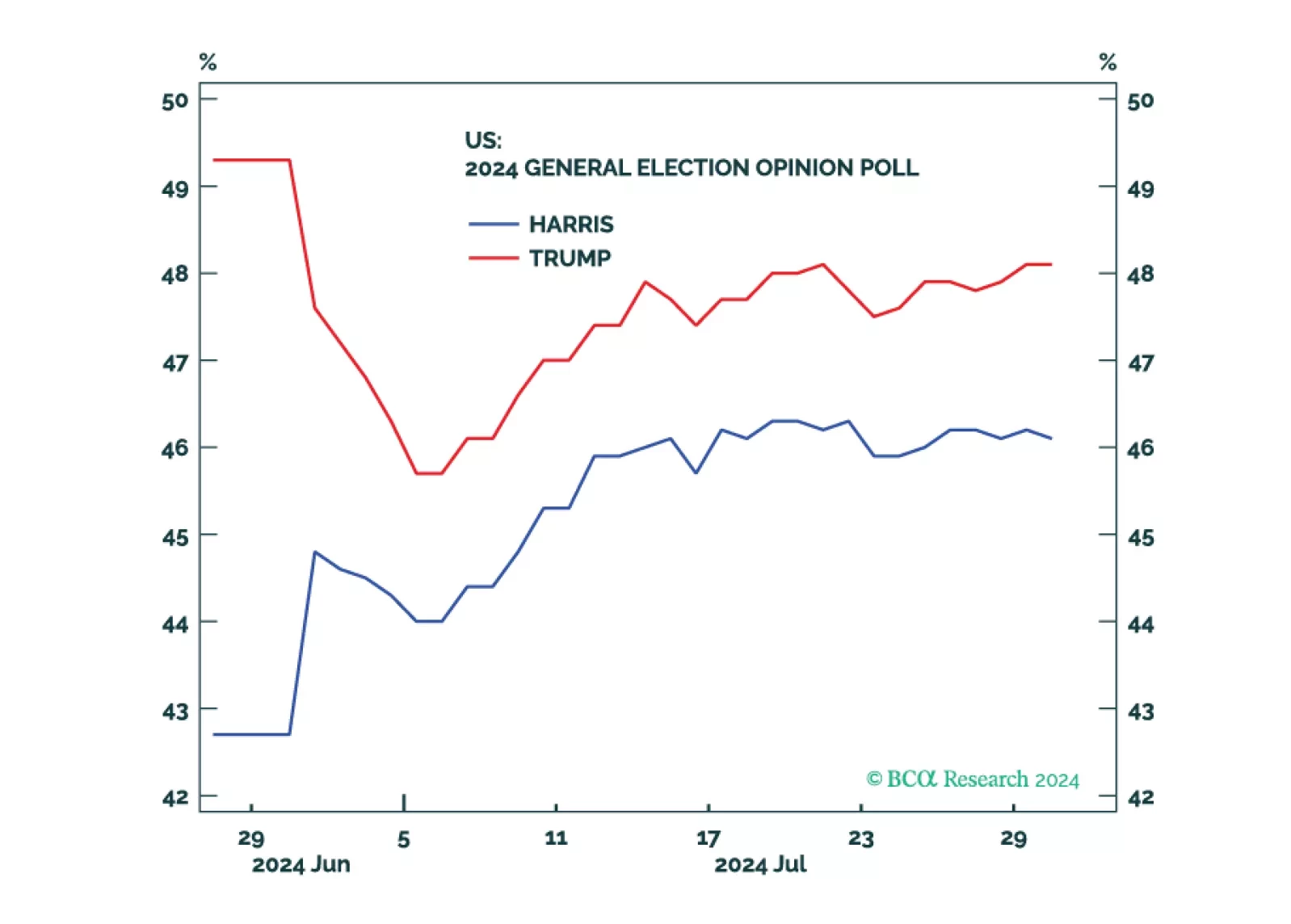

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

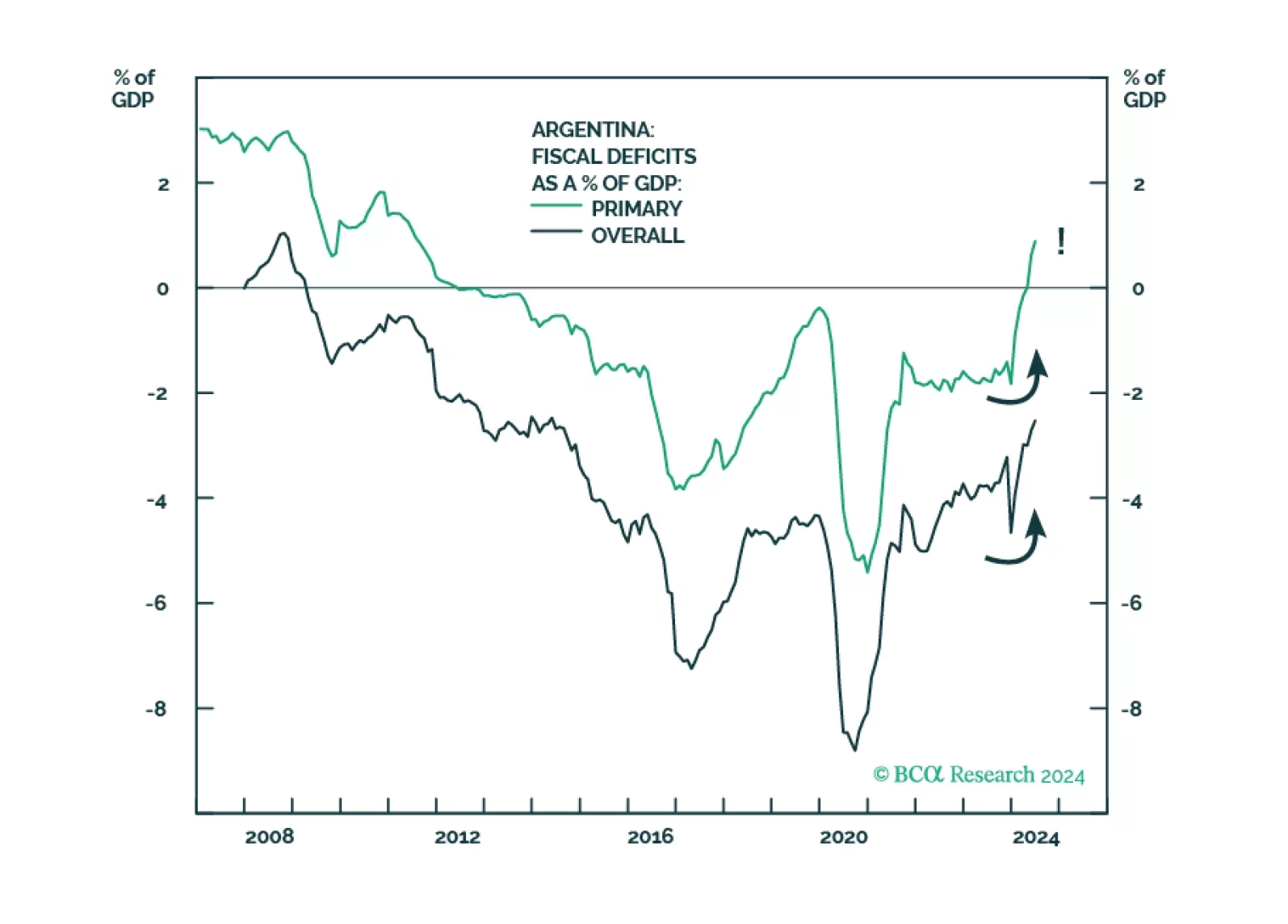

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.