Fiscal Policy

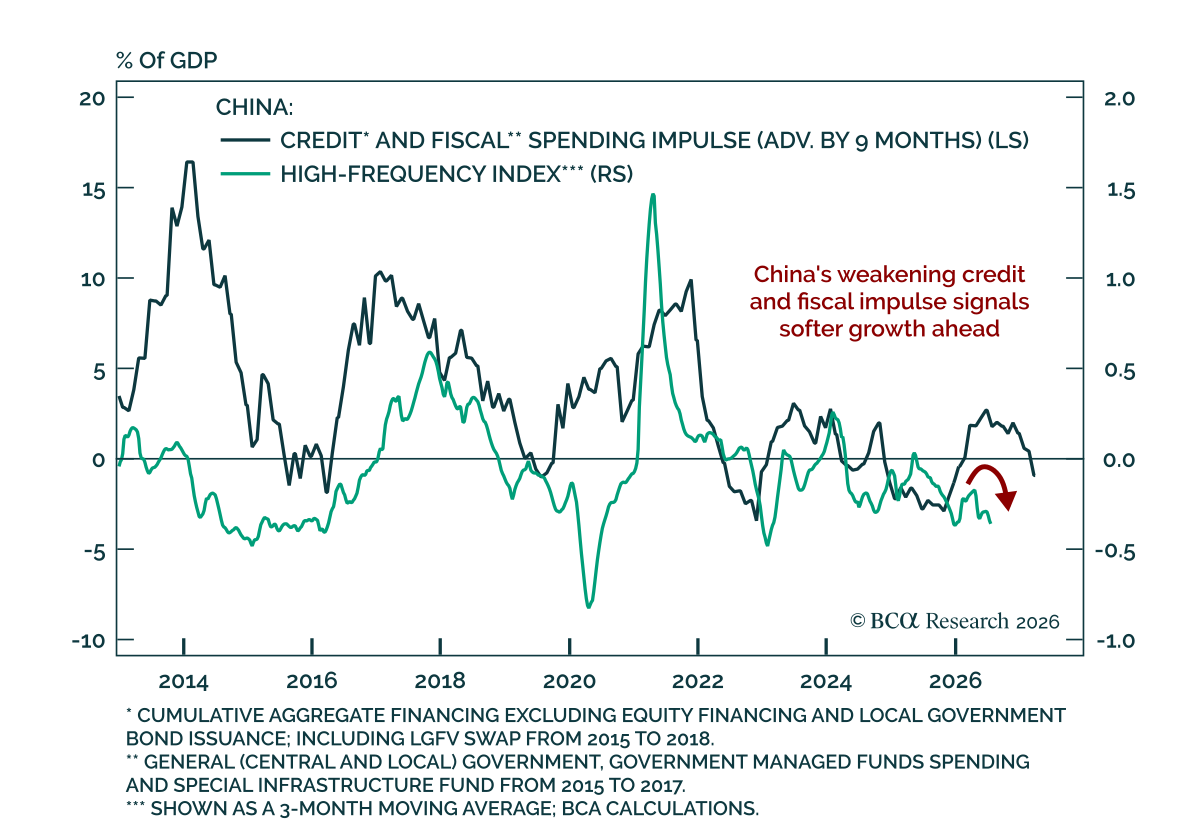

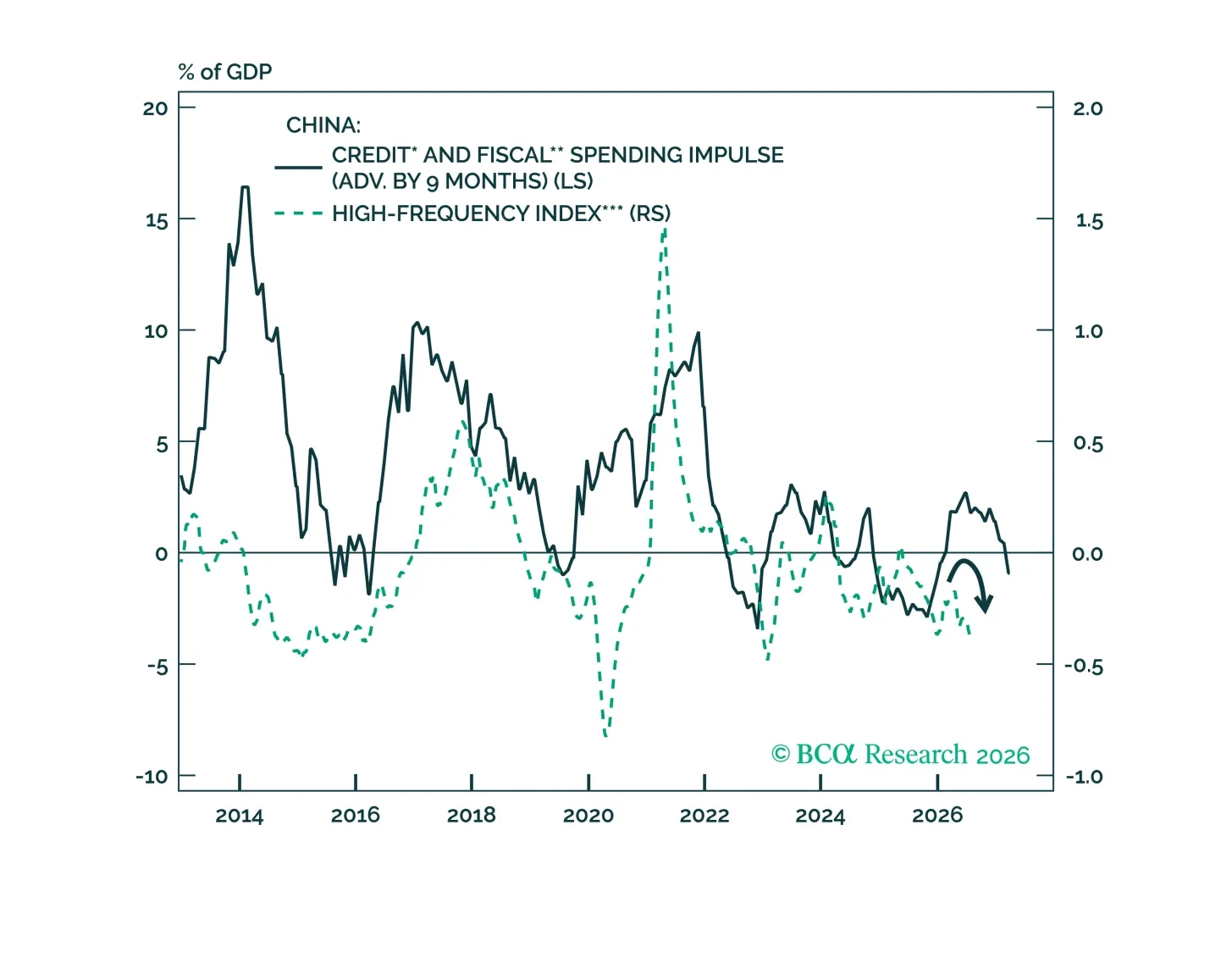

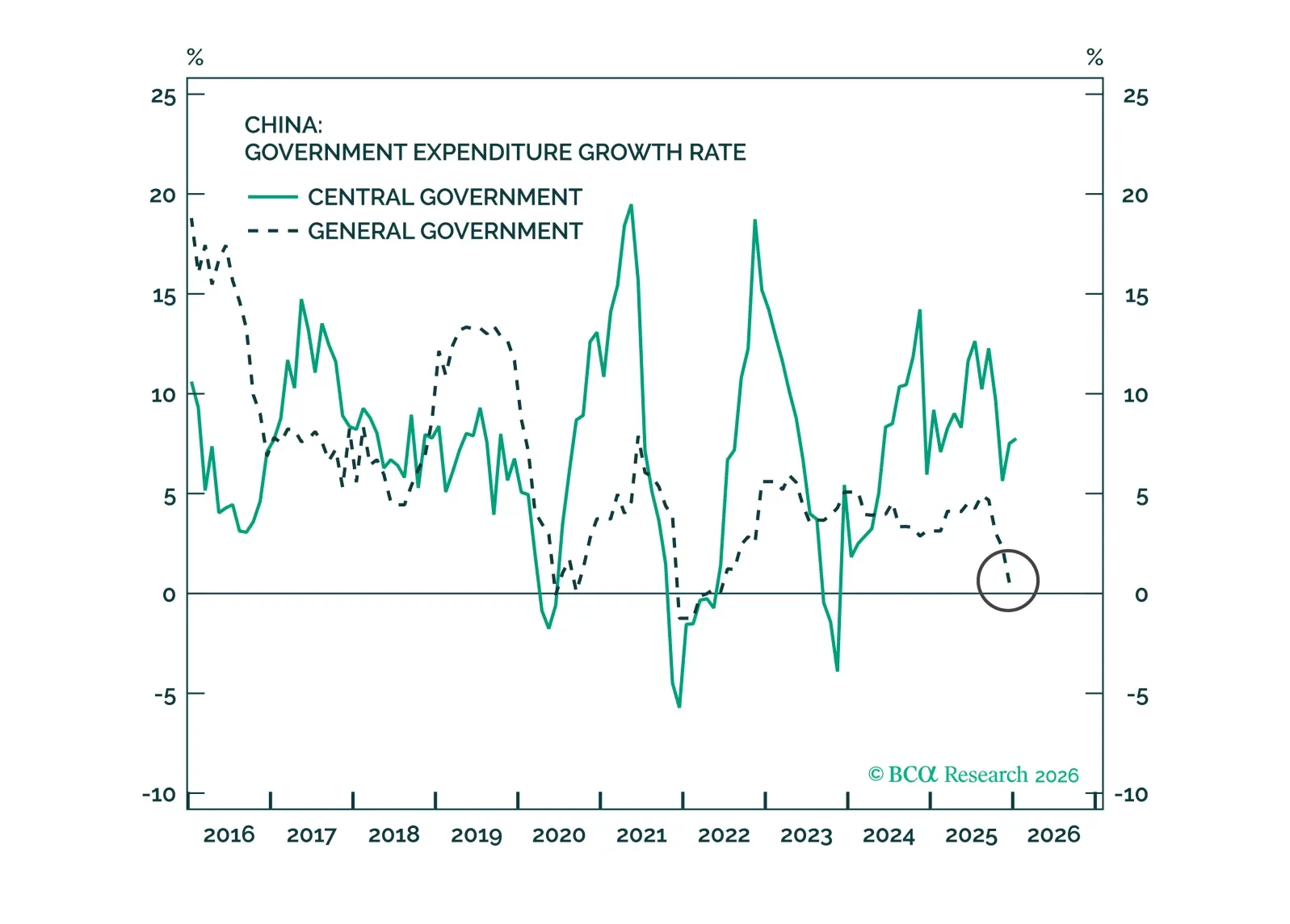

China's economy is slowing, but policymakers are unlikely to launch broad-based stimulus in H2. Meanwhile, the emergence of China's "Kimi moment" underscores Beijing's commitment to technological upgrading and the country's rapidly advancing AI capabilities.

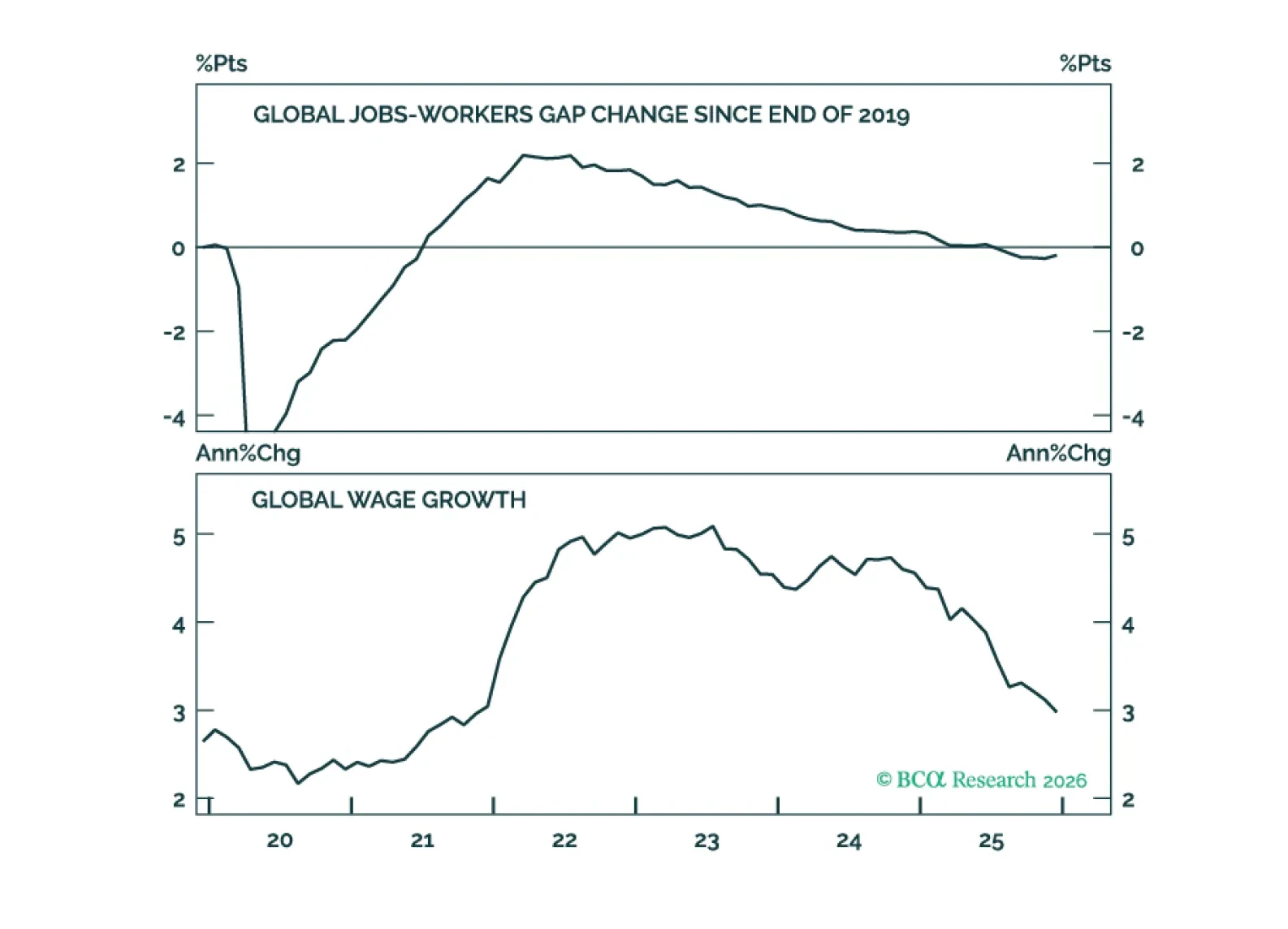

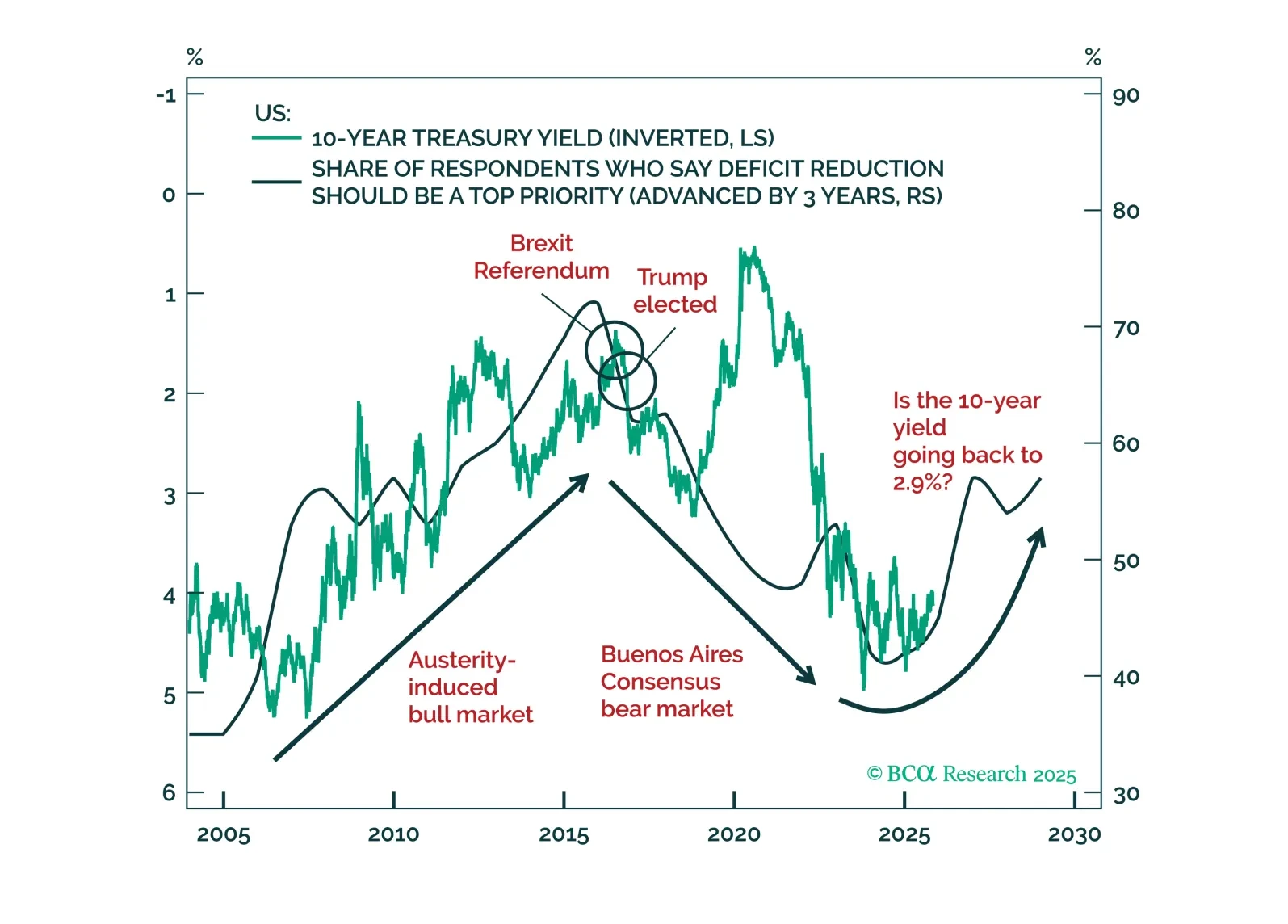

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.

China's slowdown coincides with at least a minor global oil shock – a combination we have long feared.

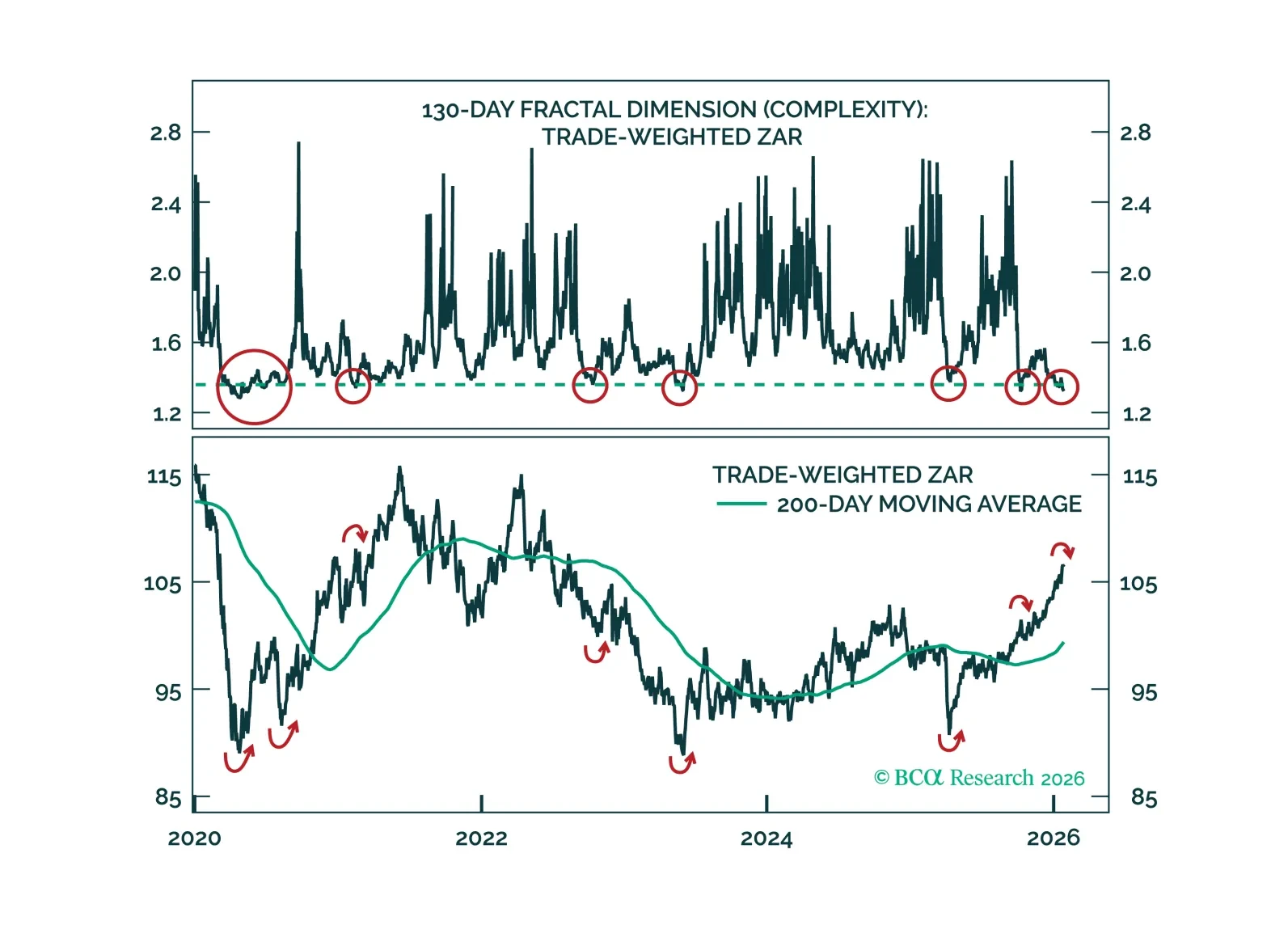

South Africa’s commodity boost is fading, but its cyclical headwinds remain. As growth weakens and capital inflows dry up, the rand looks increasingly vulnerable to a reversal.

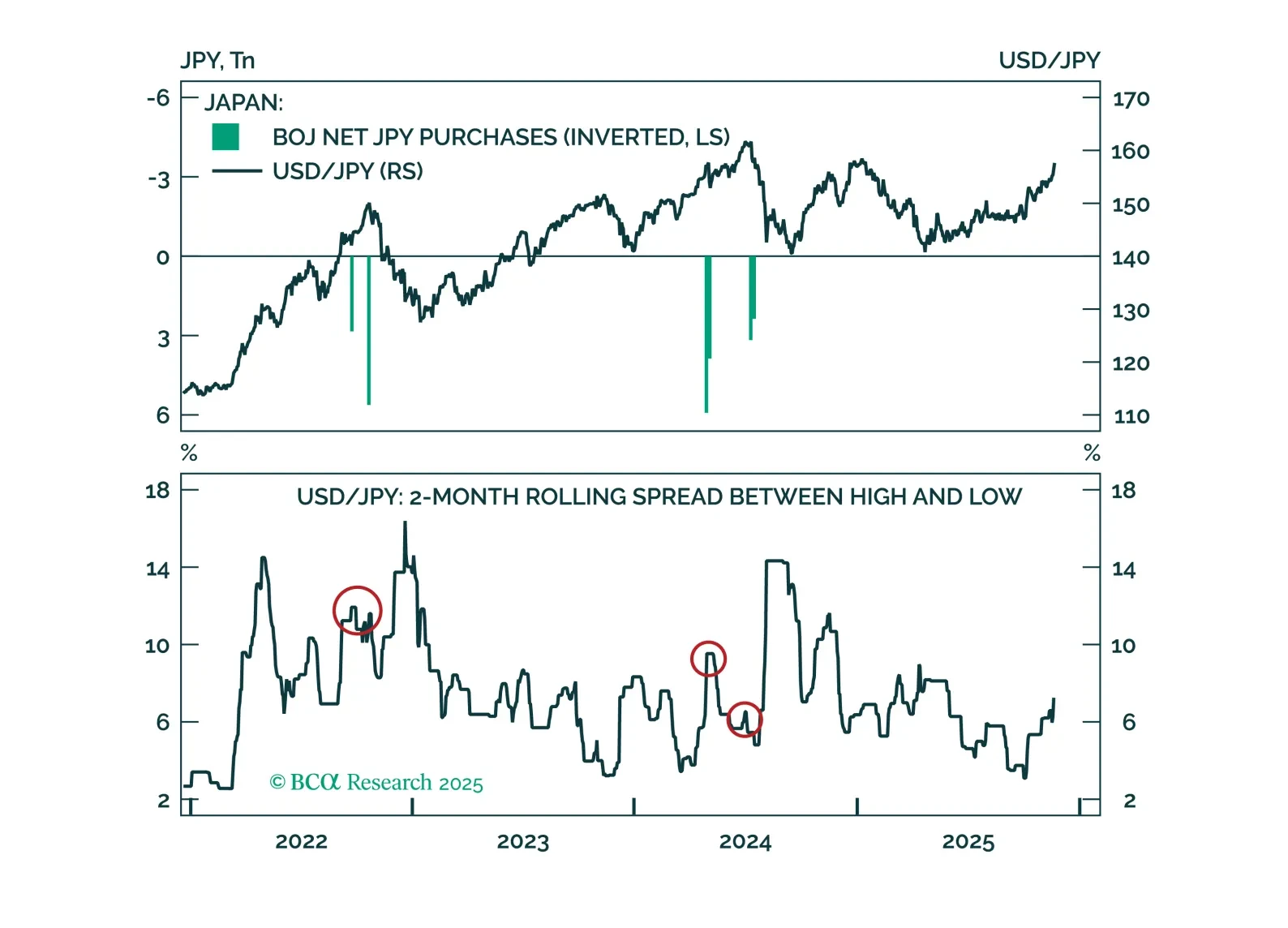

Markets are misreading Japan’s fiscal headlines. Our latest Insight examines what will shape BoJ policy next, when intervention might come, and the timing of a yen reversal.

Détente between China and the US is a big deal. Economic data continues to give the Fed reasons to cut. What is there to be worried about? Very little. But we chew on some bearish thoughts as we start thinking about 2026.

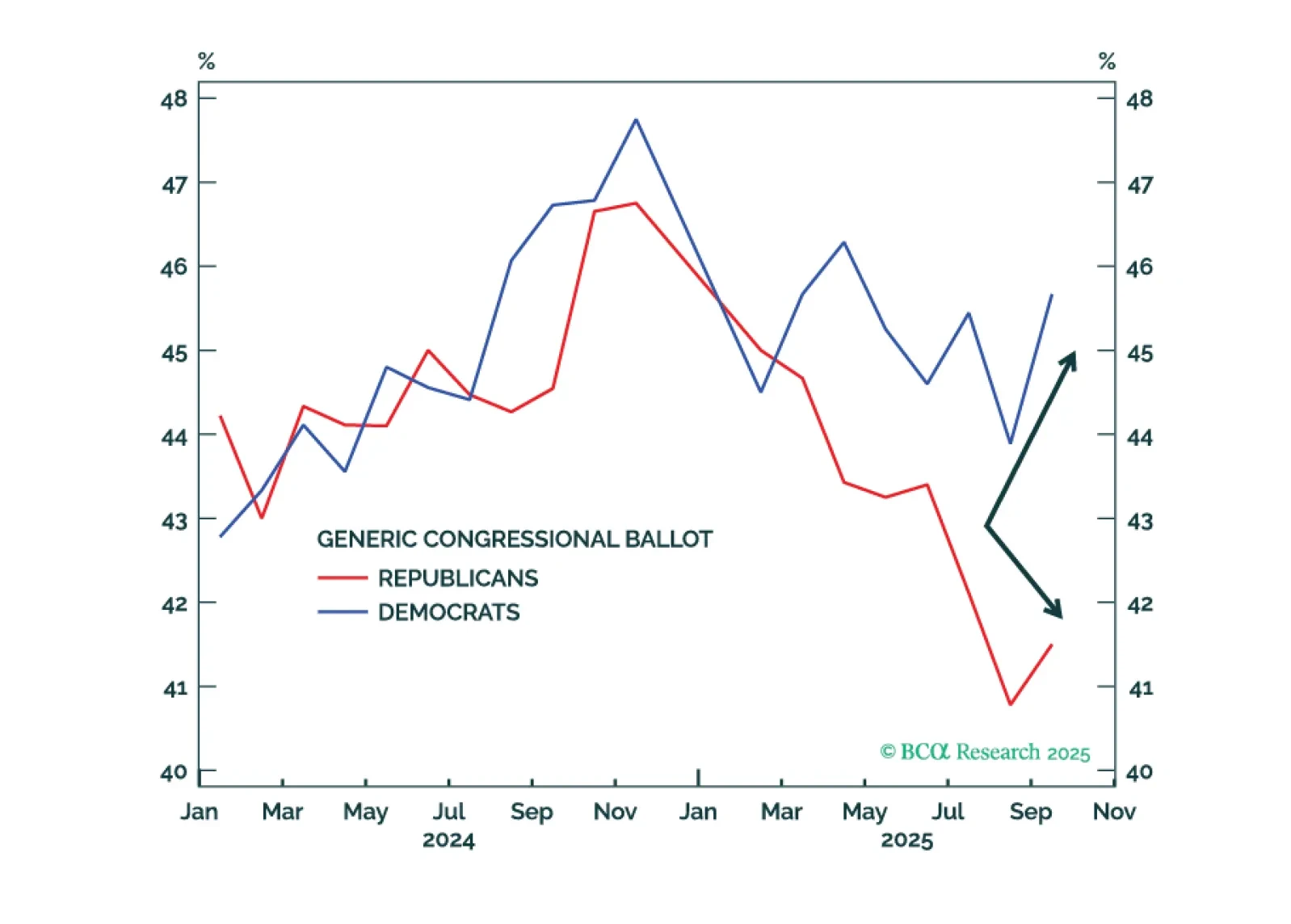

We give a one-third probability of a federal government shutdown. It probably will not happen before November. At worst, government shutdowns only cause temporary market volatility.

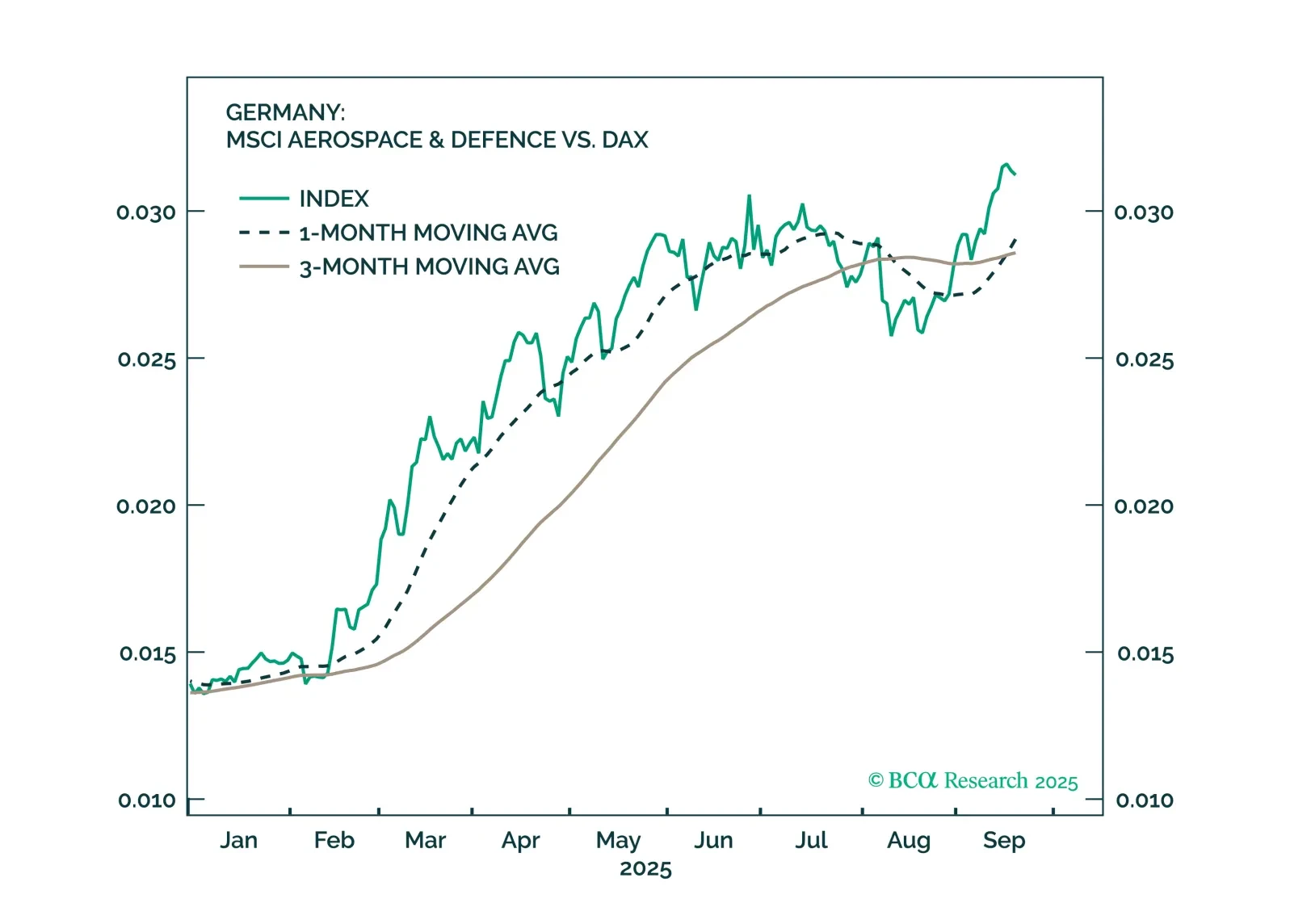

Germany is moving forward with implementing the large fiscal and defence spending announced earlier this year. Fiscal reforms are also positive, though they will fall short of expectations.

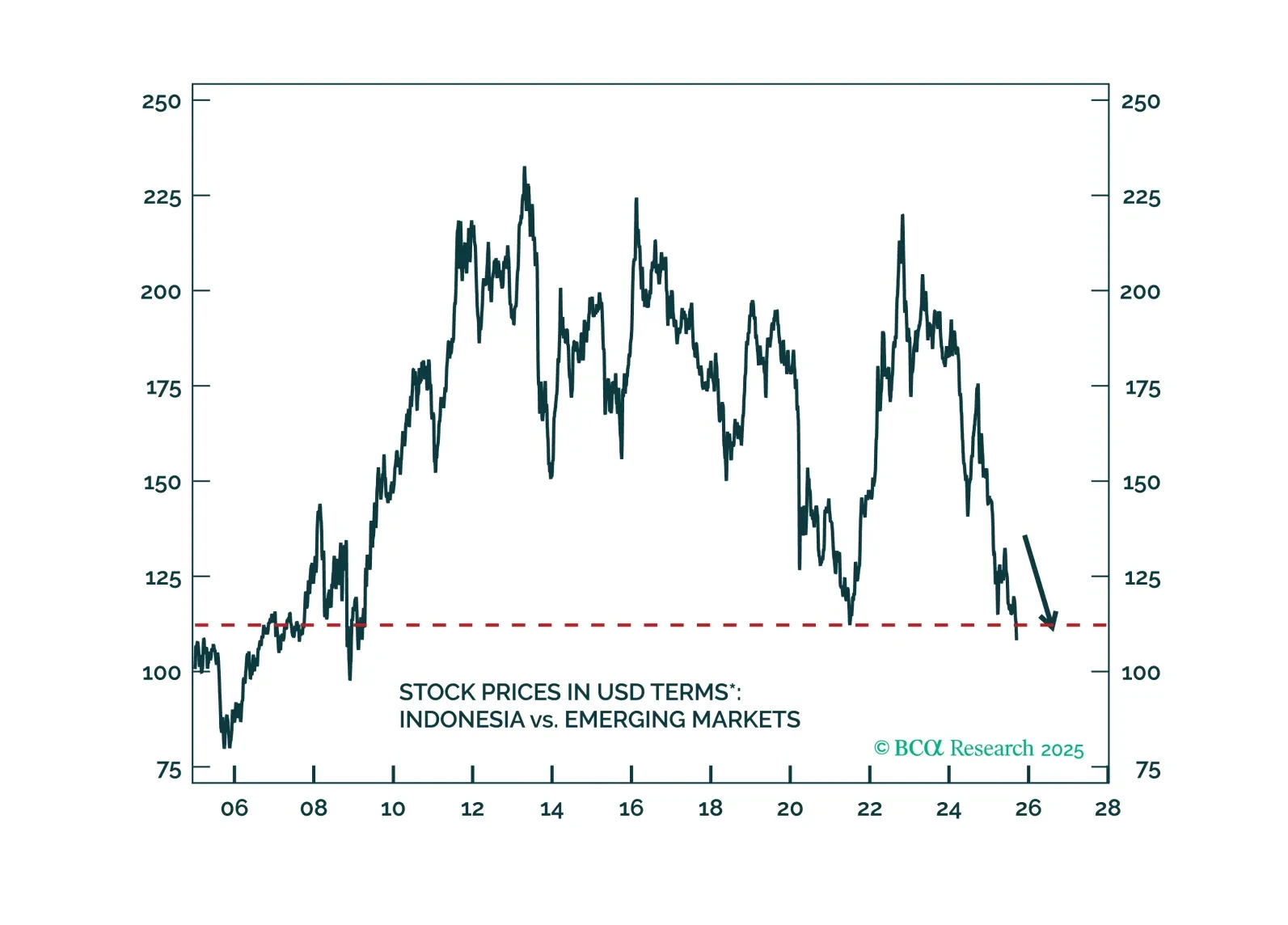

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.