Financials

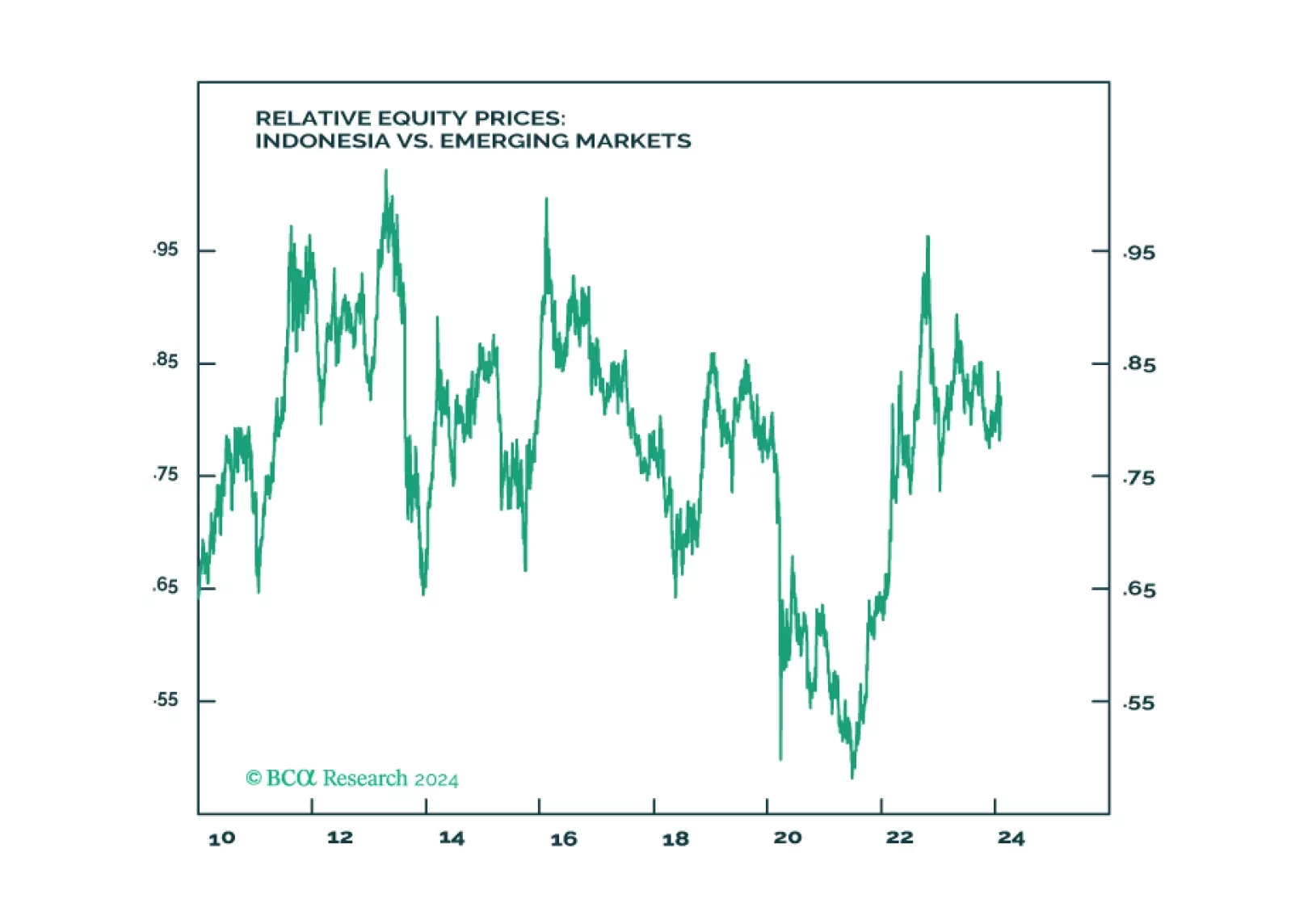

Indonesia will not revert to dictatorship. Yet the guardrails against authoritarianism are also constraining the actions of the next government in tackling near term domestic and regional challenges. For long-term positioning, use potential selloff from a “dictatorship scare” to build position as structural outlook for Indonesia is positive due to the China-West divorce and the global energy transition.

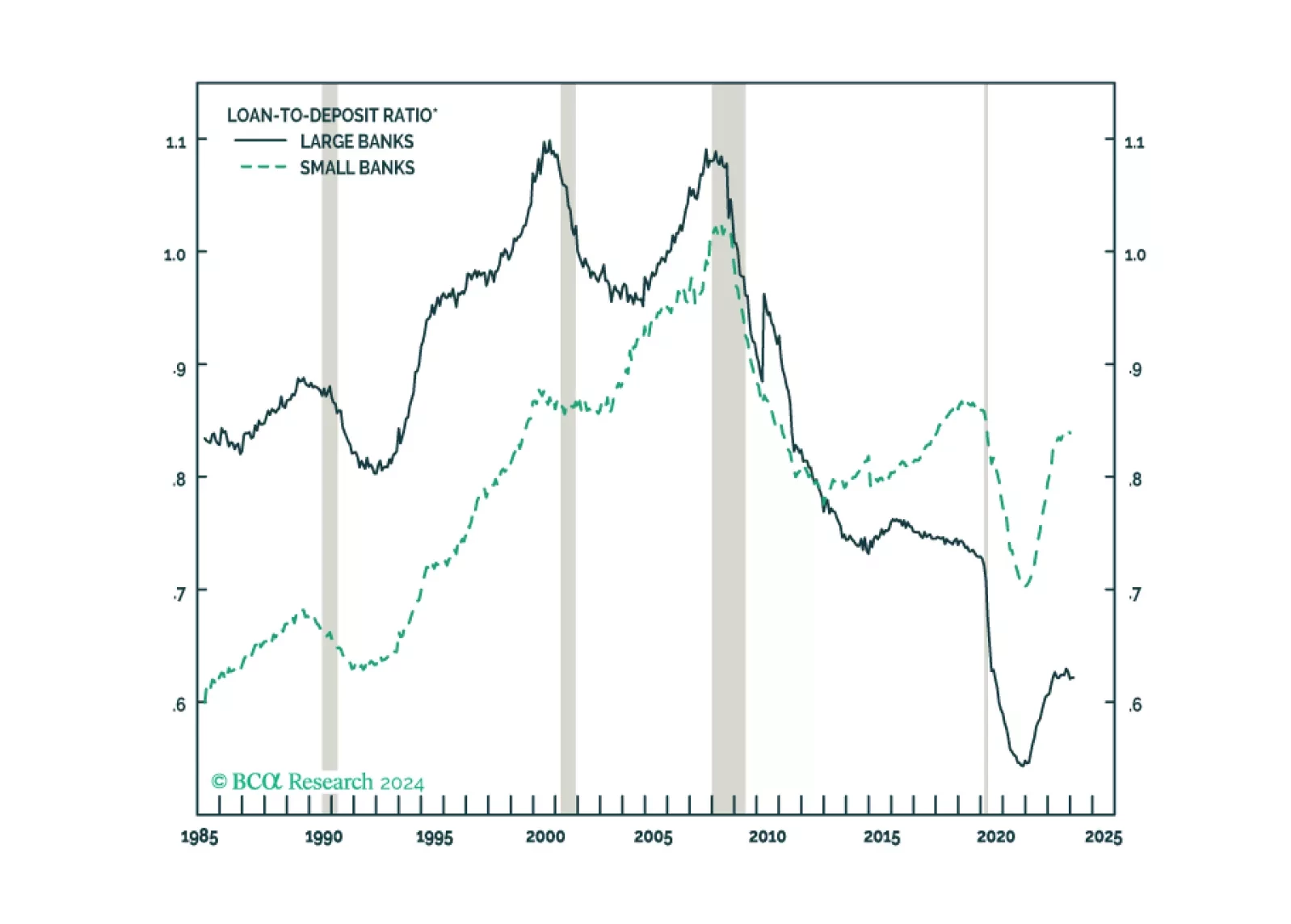

We do not believe that NYCB is a canary in the coal mine for a new round of bank distress. The MidCap 400 Regional Bank Index’s subsequent 10% decline looks to us like a juicy opportunity for stockpickers who can separate the wheat from the chaff. Our Special Report is meant to assist them with their initial winnowing.

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

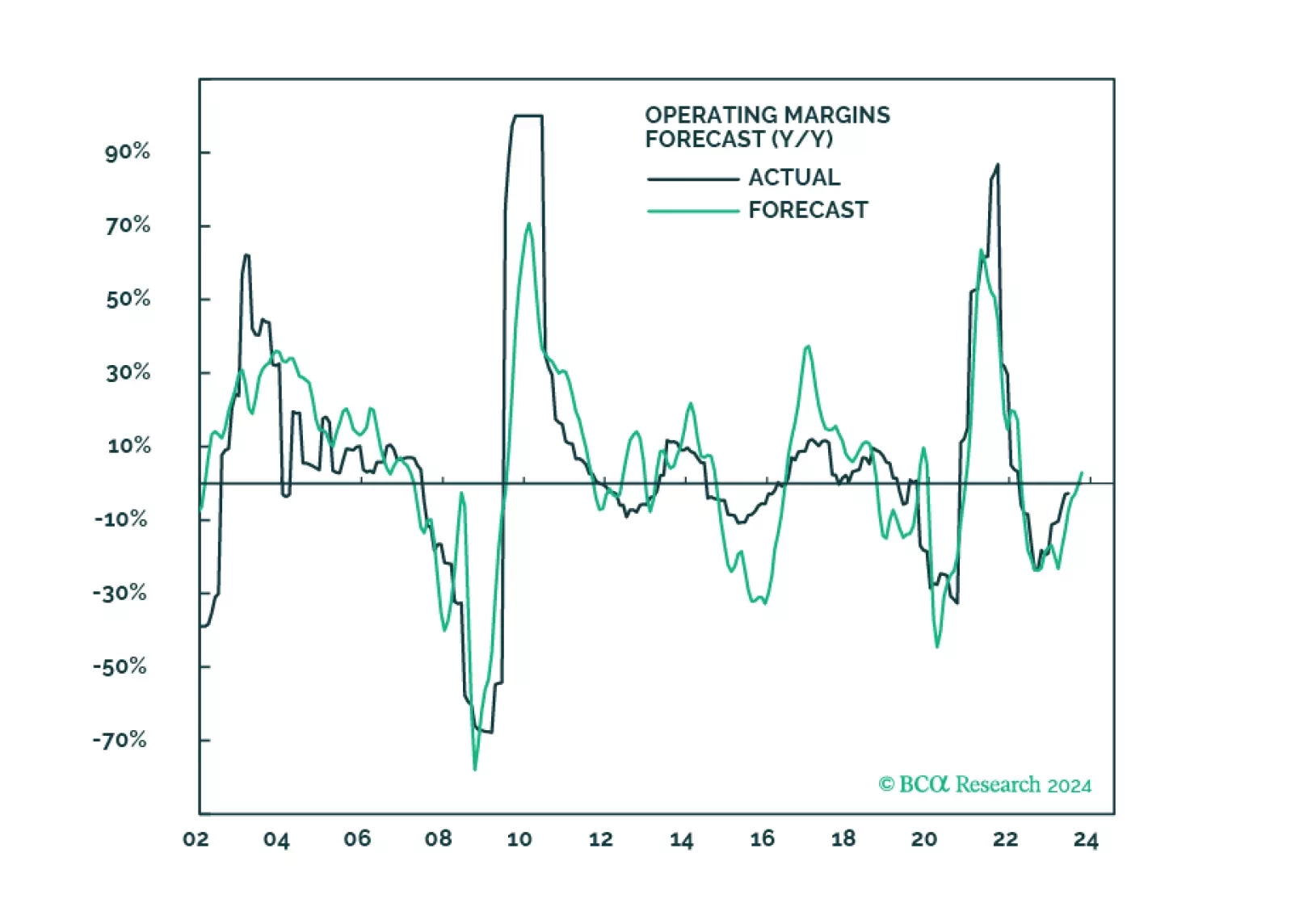

Disinflation coupled with sticky wage growth is likely to result in either a second wave of inflation or layoffs and a recession. In the meantime, market expectations for sales, growth, and margins are overly optimistic and are inconsistent with macroeconomic headwinds. We recommend gradually realigning the portfolio to a more defensive stance.

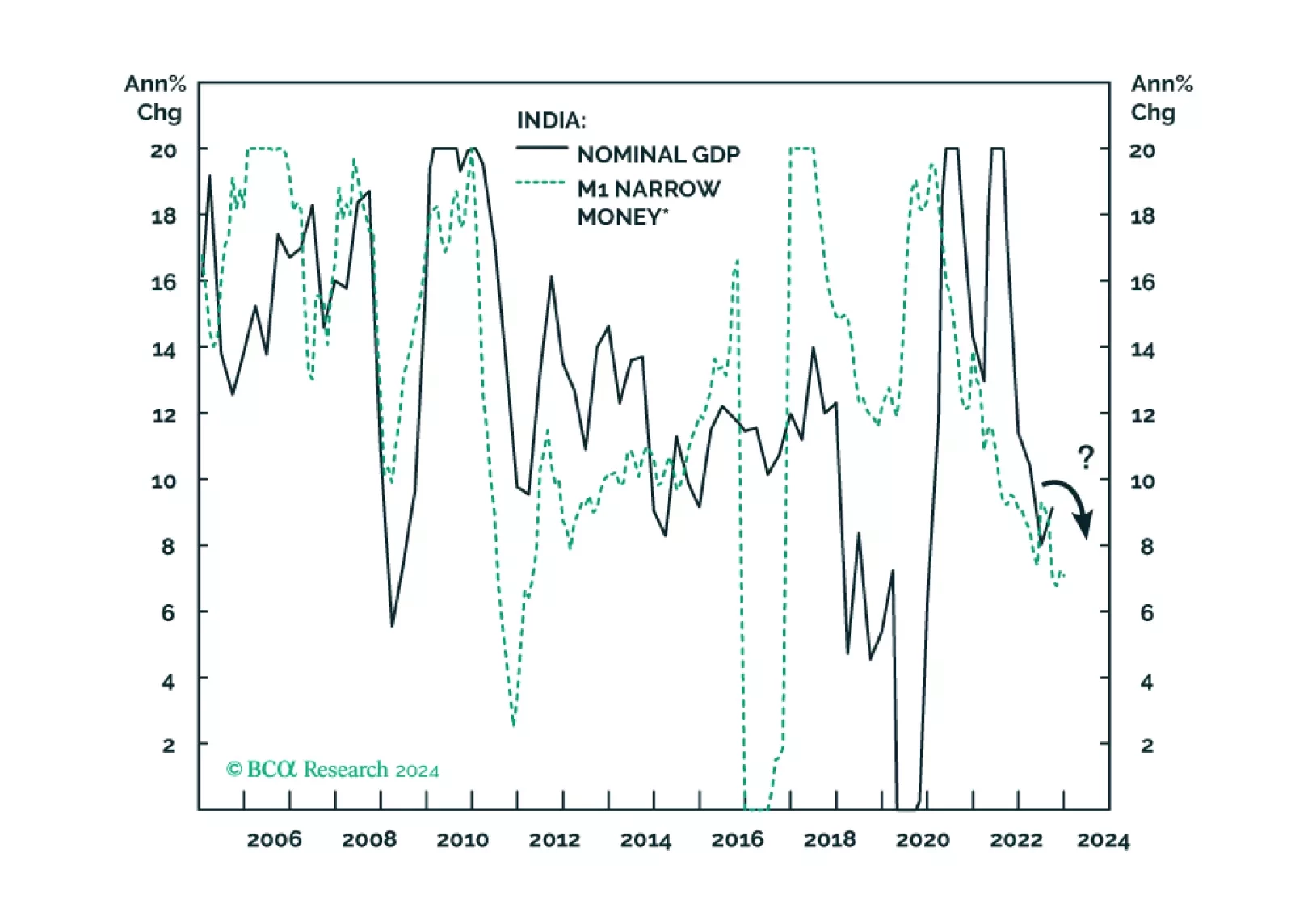

Decelerating nominal sales, a peaking credit cycle, and very high valuations - Indian stocks will not escape the carnage when risk assets globally begin to sell off.

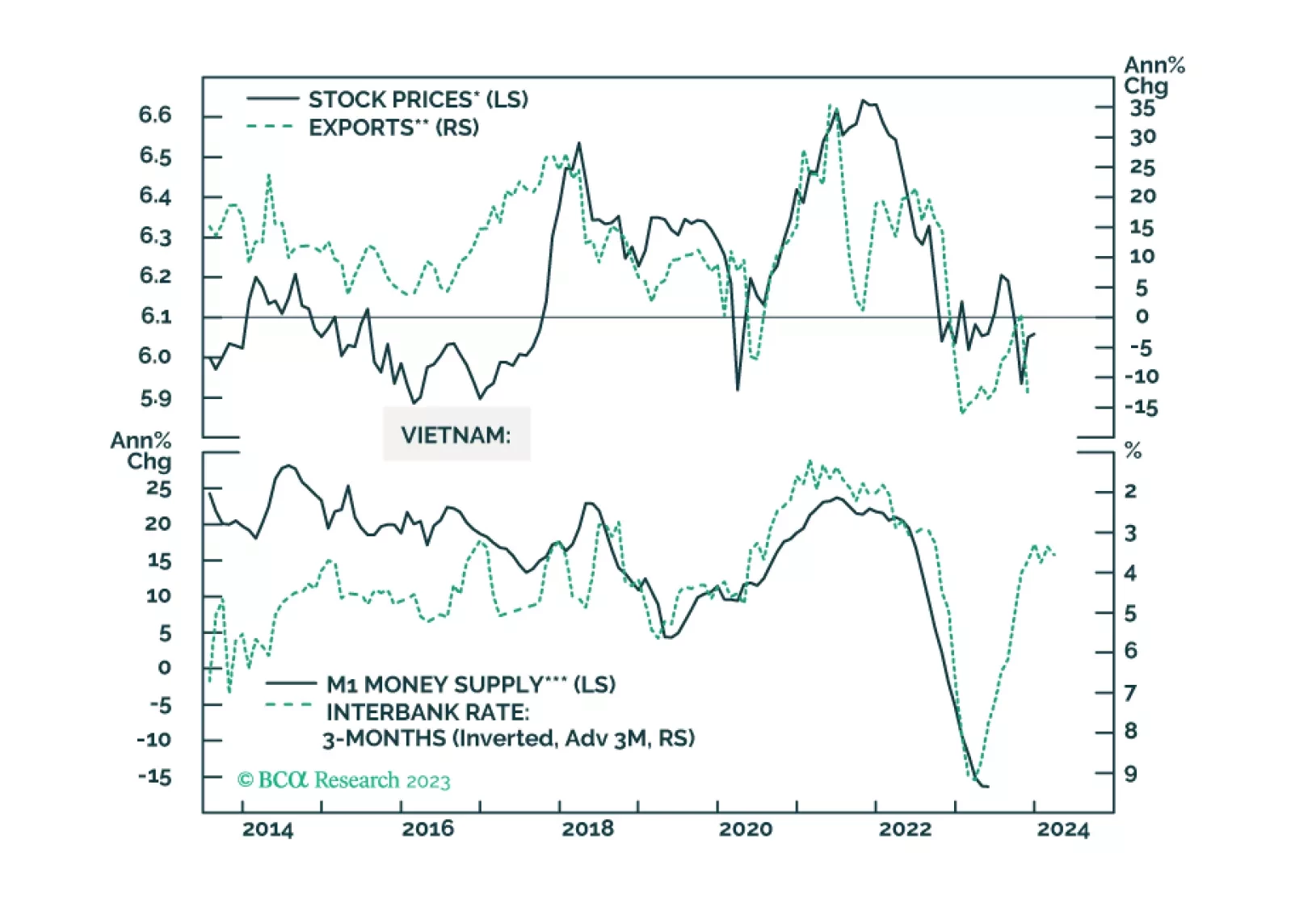

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

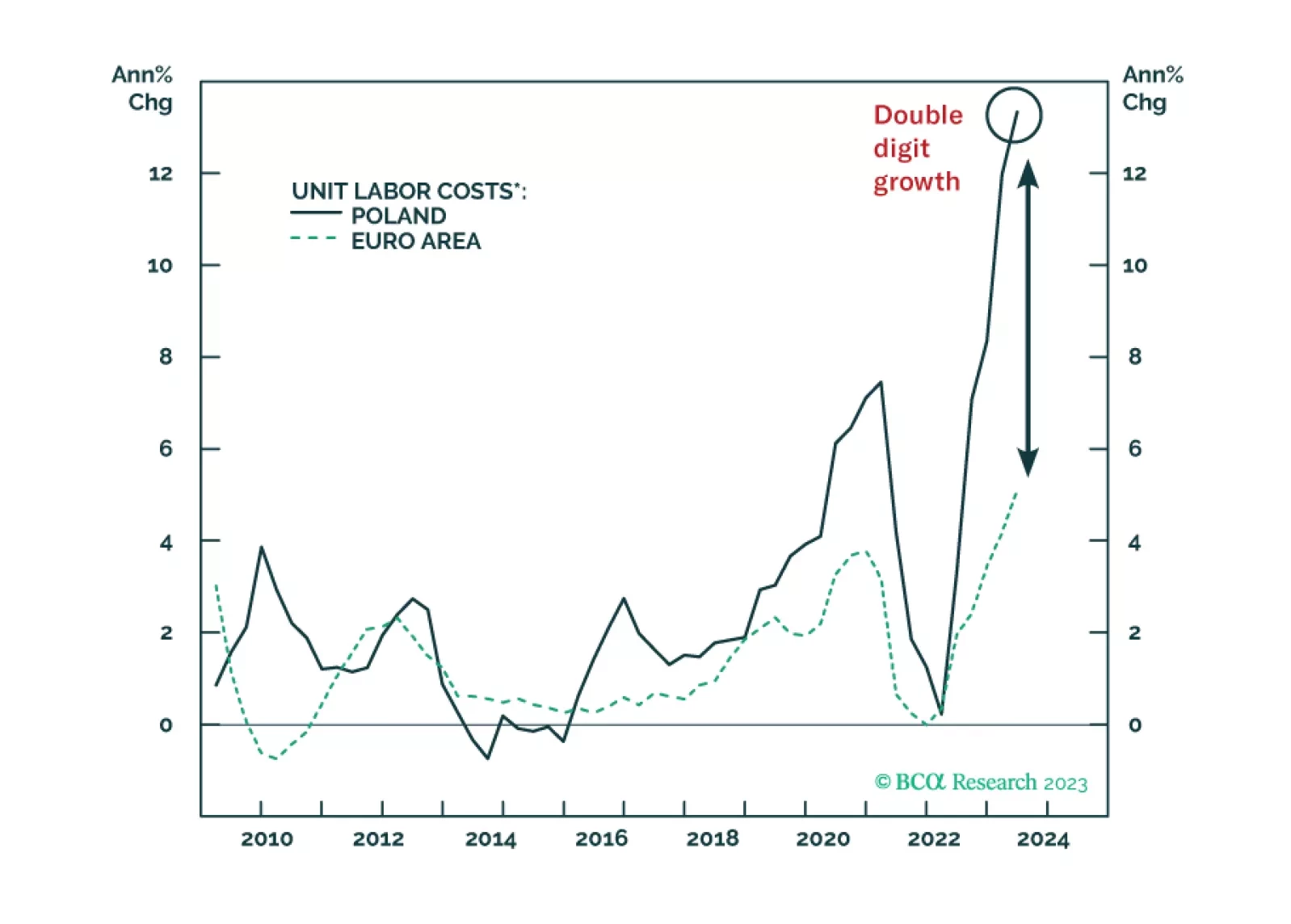

Poland’s inflation will stay elevated. And yet, its return to the European mainstream has improved its financial market outlook. Accordingly, we are recommending new trades on Polish equity, fixed income, and currency.