Financial Markets

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.

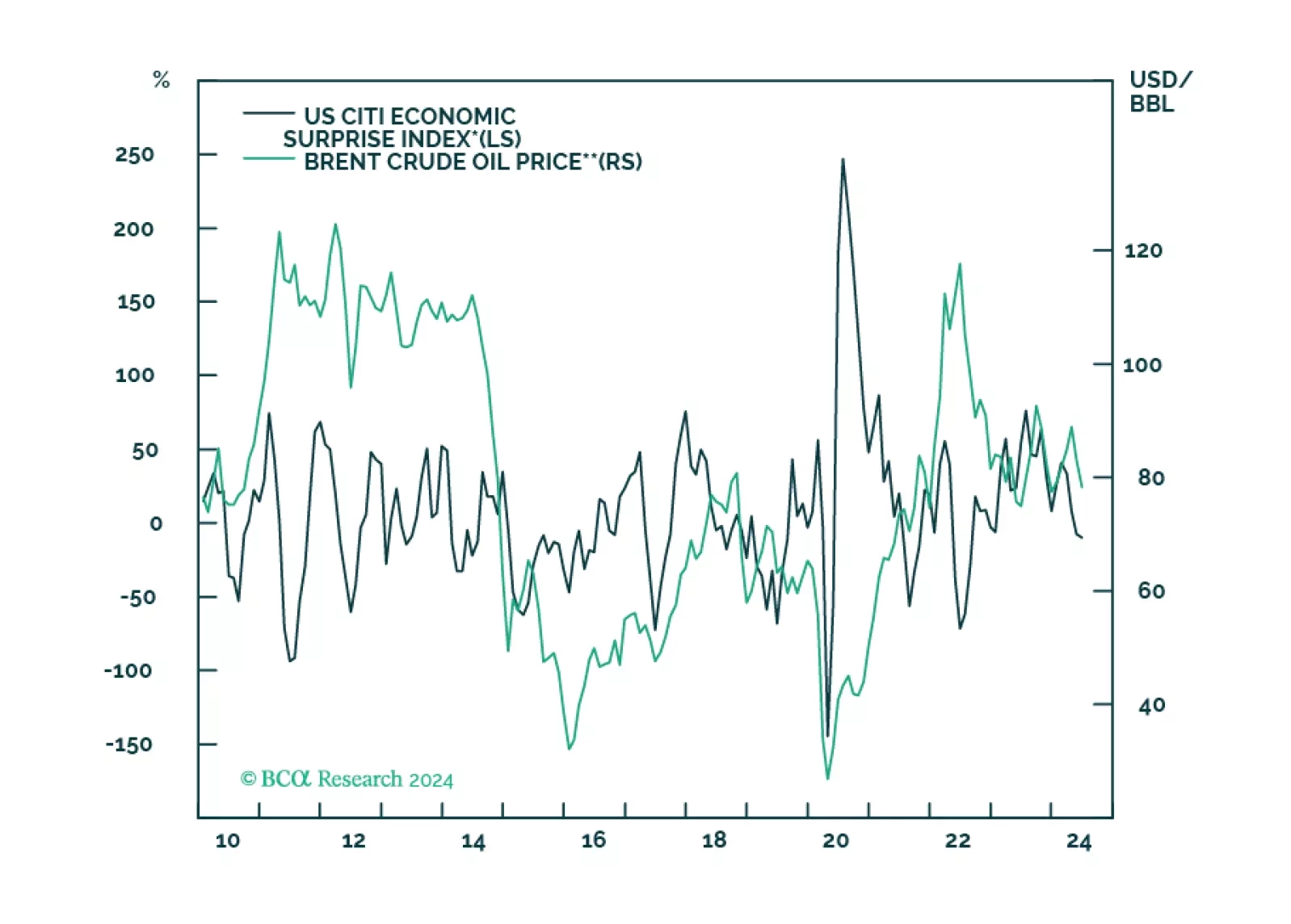

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

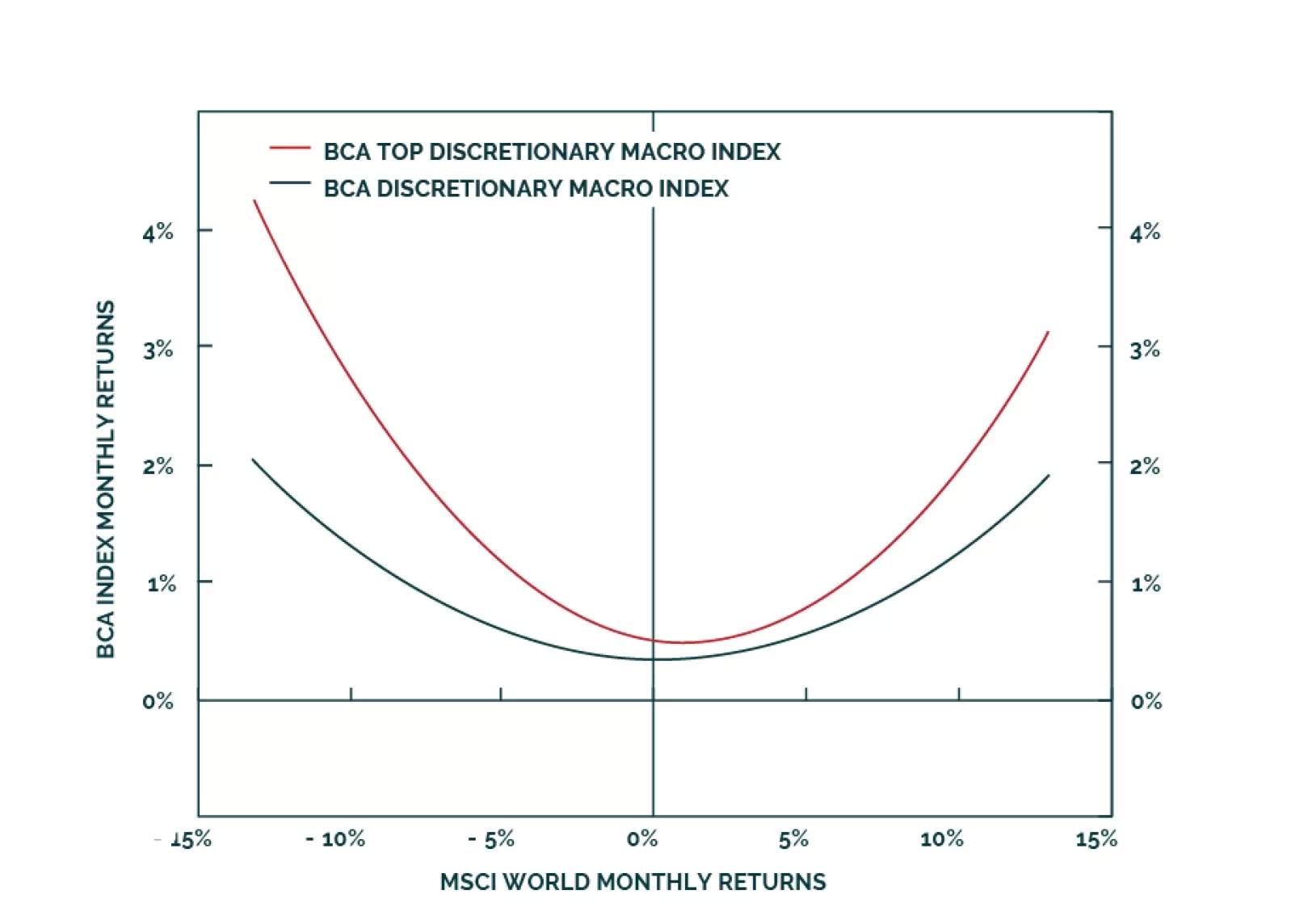

Investors often misjudge Global Macro managers. We outline key manager evaluation criteria and highlight the power of combining Macro Hedge Funds and Private Equity. Even for those who are not Macro Traders nor invest in Hedge Funds, this report may change the way you assess potential employees, partners, and even yourself—the most critical elements of any investment strategy.

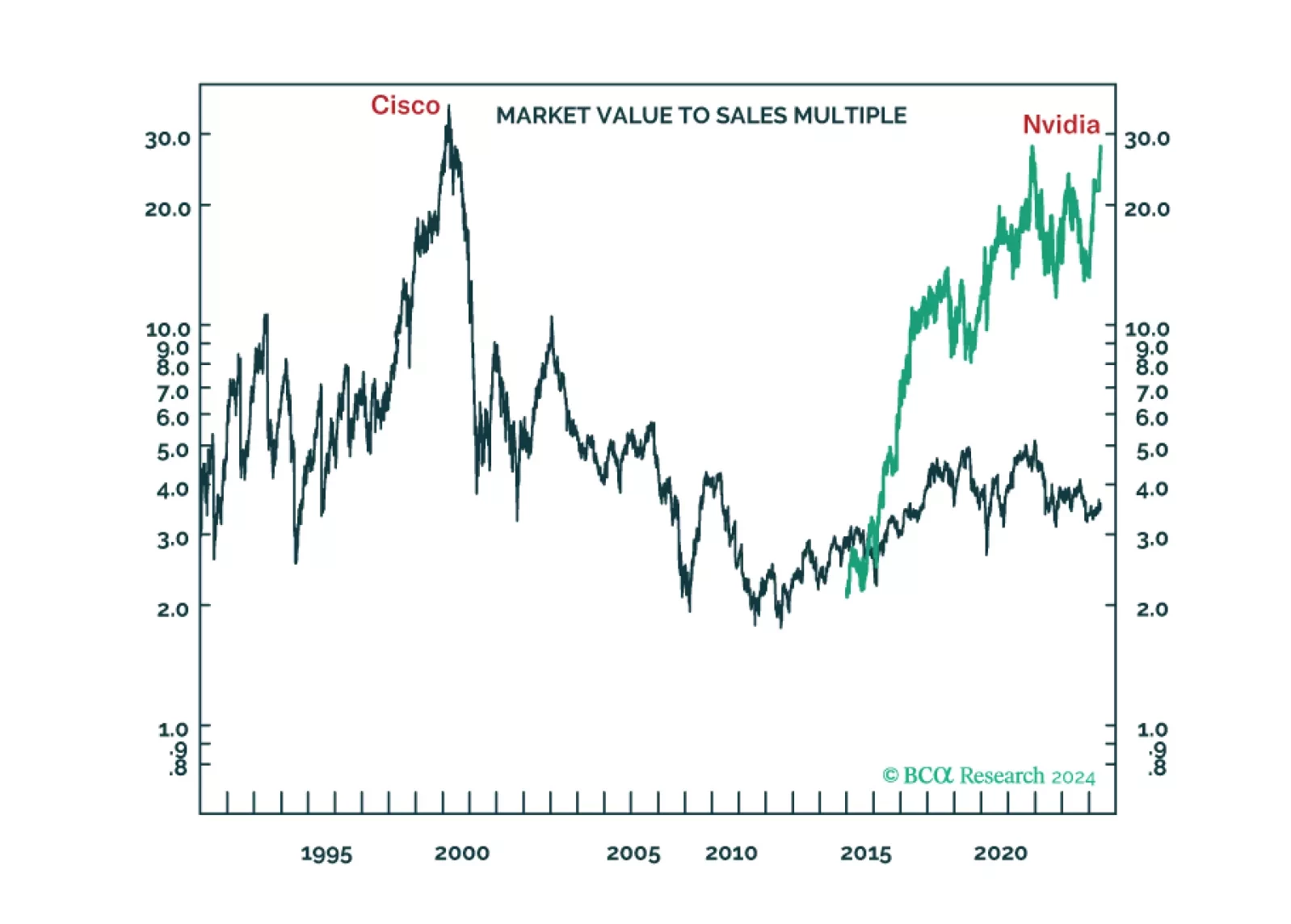

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

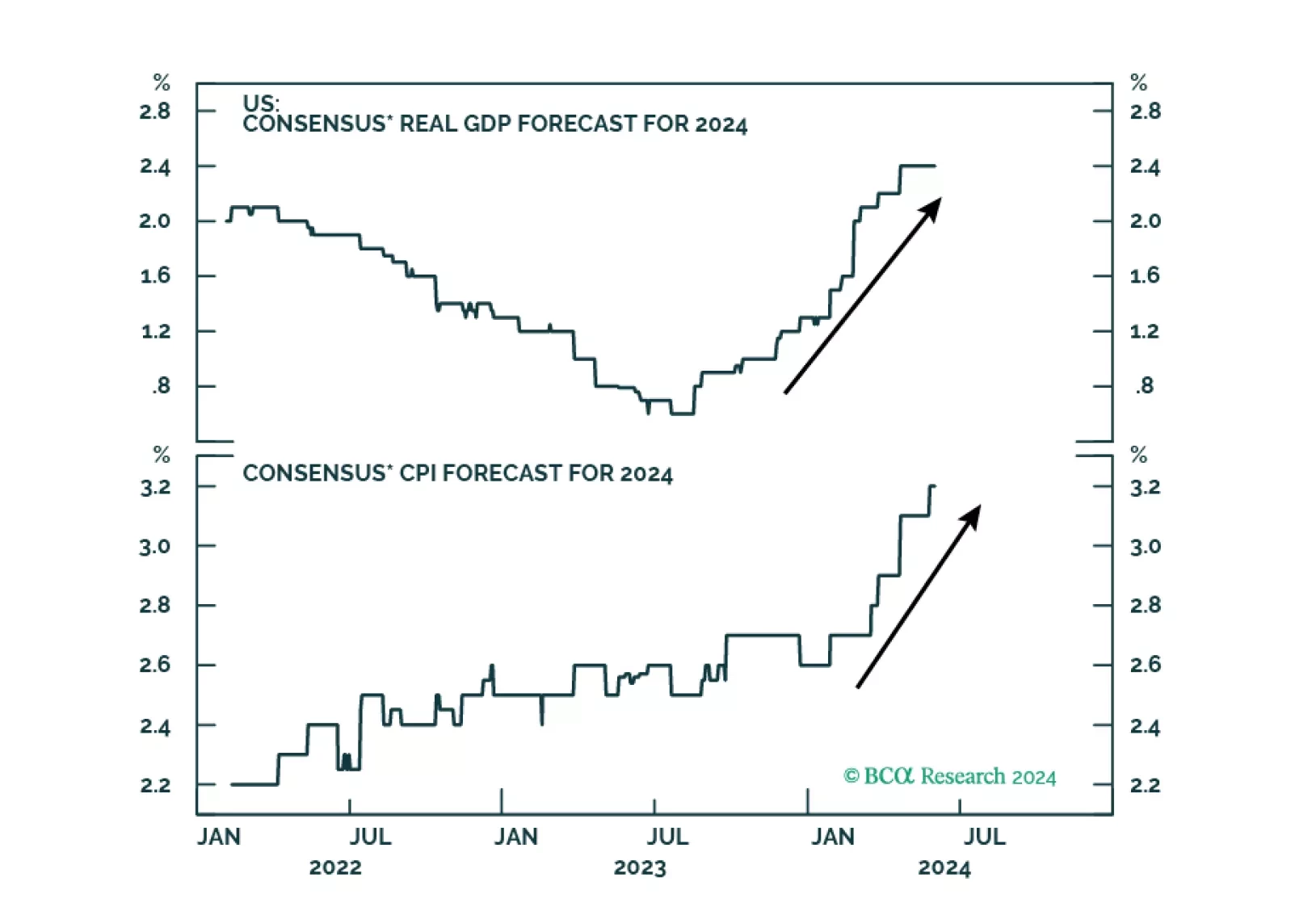

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

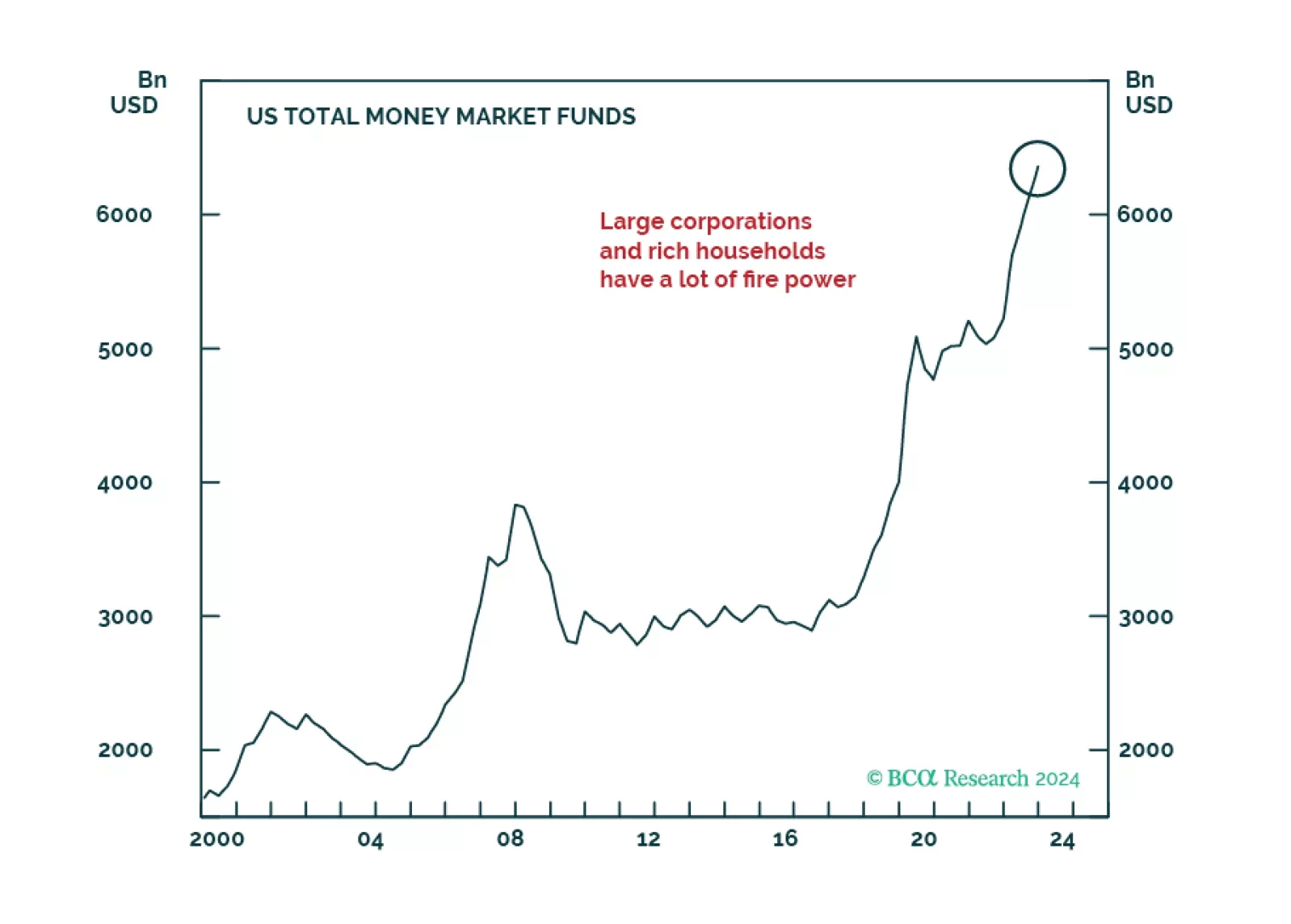

Generative AI-related rally resumed in May. Much of the recent market gains are down to excess liquidity that was begotten by the massive pandemic stimulus, creating a dichotomy between multiple economic challenges and exuberant markets. The Fed is unlikely to step in to prevent the bubble as it is currently more worried about the near-term downside for growth than financial stability.

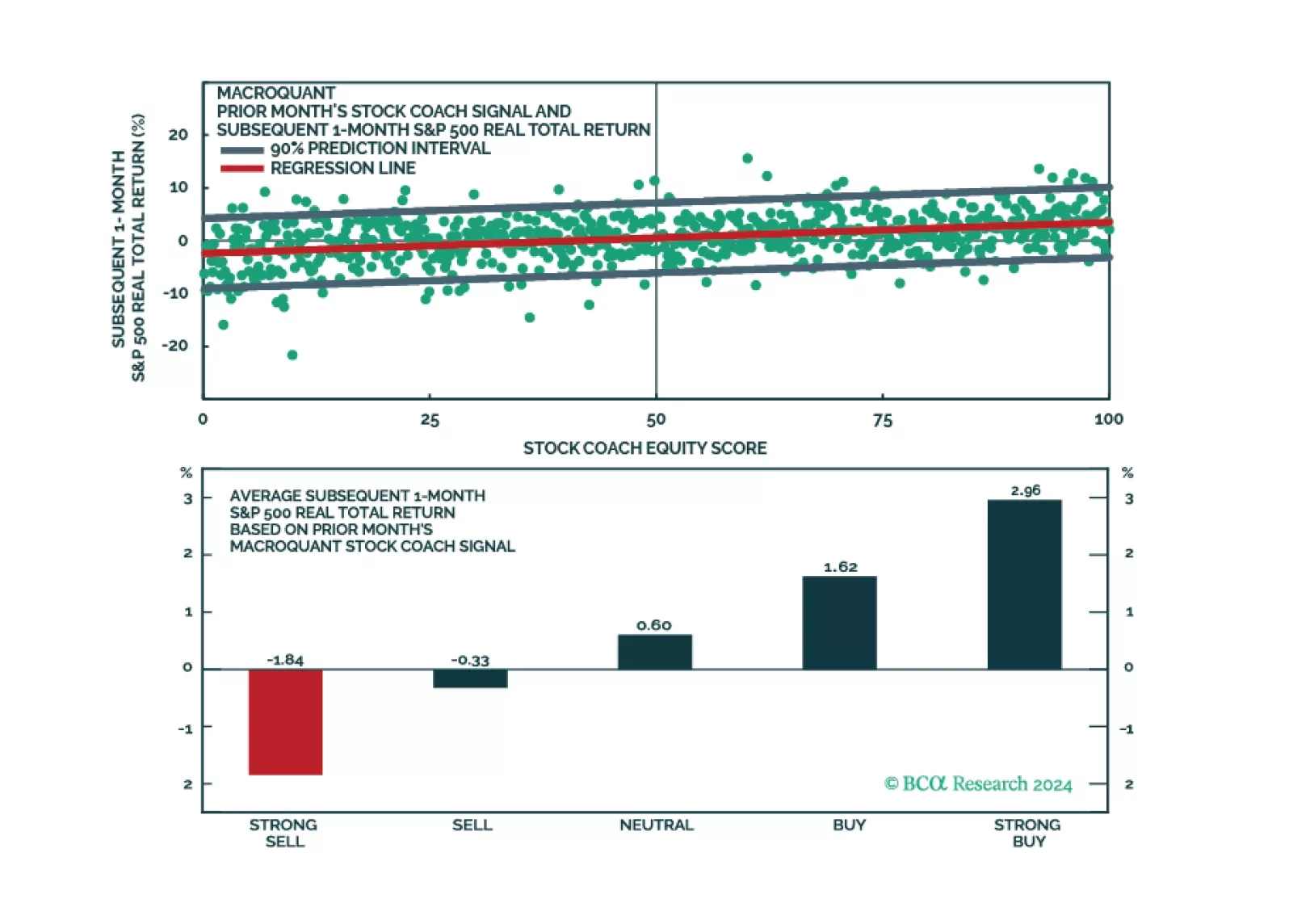

MacroQuant sees significant downside risks to stocks over a 1-to-3 month horizon and suggests increasing allocation to long-term bonds. The model favours defensive equity sectors but is also hedging its bets by overweighting materials.

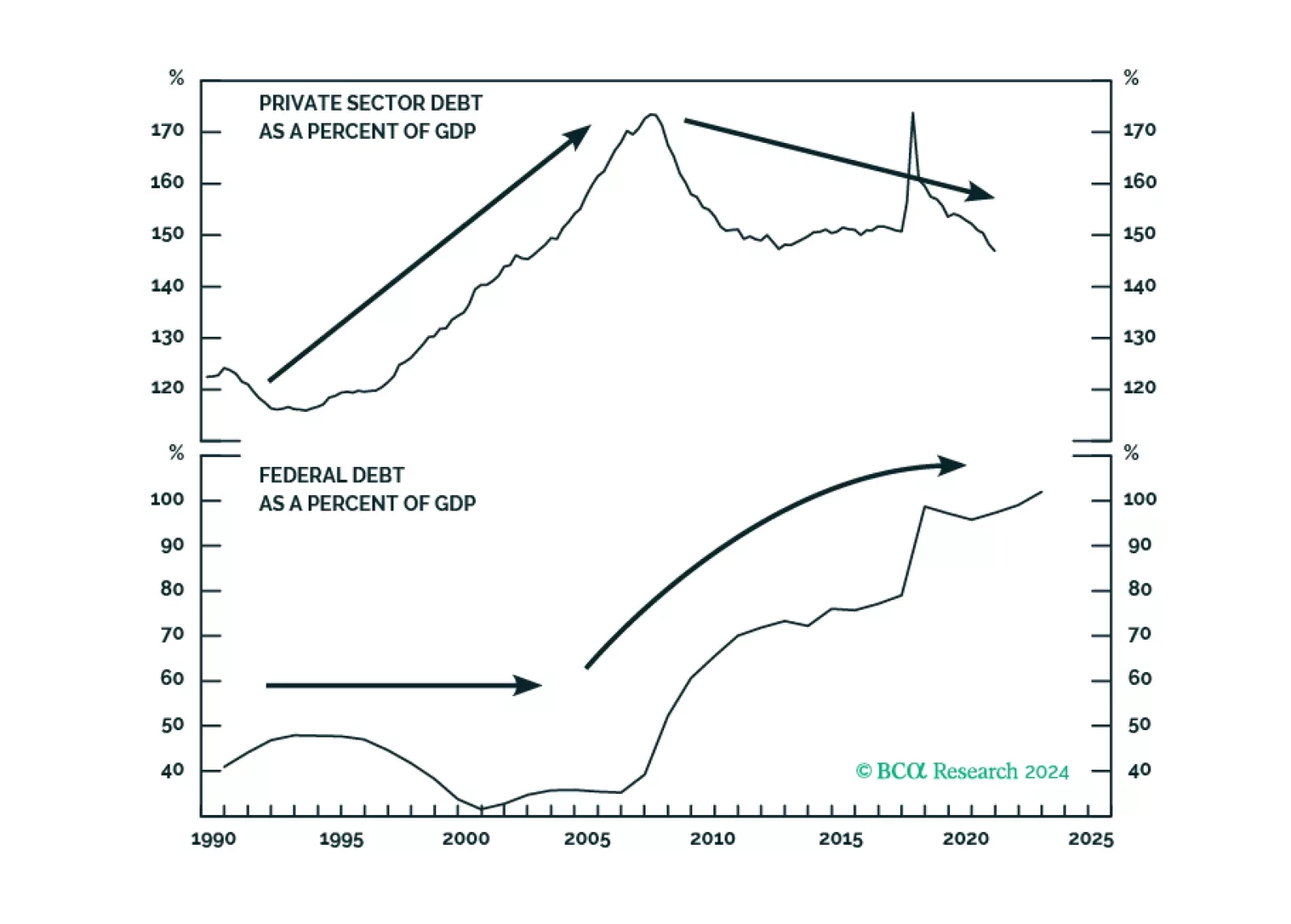

In a guest research report, Martin Barnes, BCA’s former Chief Economist, revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.