Europe

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

The attacks on Red Sea commercial tankers by Iran’s Yemeni proxies, the Houthi movement, are an inflation risk inasmuch as they lengthen voyage times for any shipping forced to avoid the Bab el-Mandeb Strait. The risk of an expansion of these attacks is, in our view, limited, given Iran’s inability to project naval power in the region.

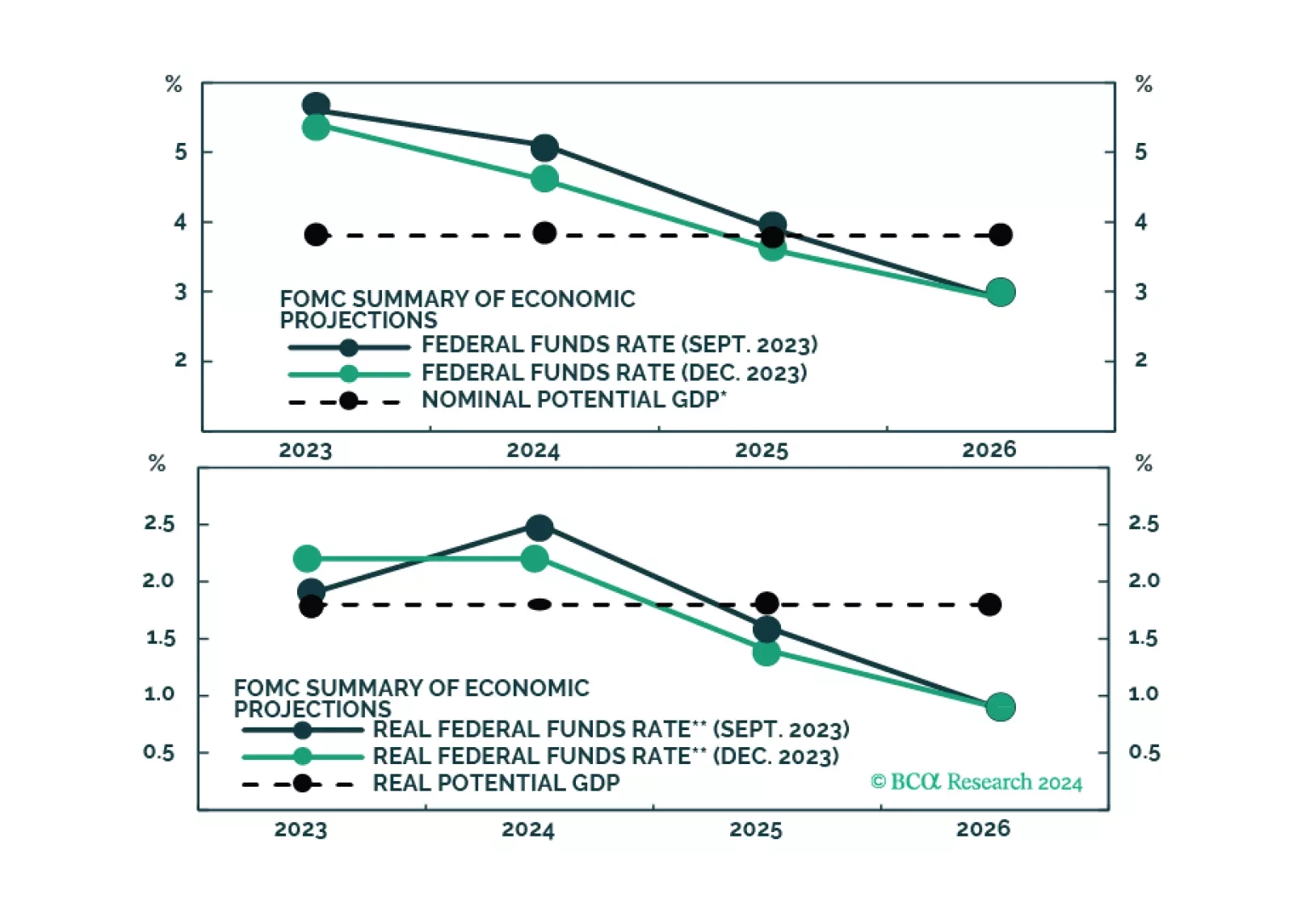

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

Explore the eight main themes that will drive the returns of European assets in 2024.

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.