Europe

Results of Germany’s IFO business climate survey for April sent a positive message on Tuesday. The overall Business Climate Index increased from 87.9 to 89.4, beating expectations of 88.9. Assessments of both the current business situation (increased from…

The resilience of the US economy has led economists to consistently revise up their consensus real GDP growth forecast for 2024, which now stands at 2.4%, up from 0.6% in July 2023. Conversely, the 2024 consensus Eurozone growth estimate has been trending…

Flash estimates for several European PMIs were released Tuesday. The results for manufacturing activity were somewhat disappointing. The German manufacturing PMI increased from 41.9 to 42.2, but underperformed expectations of 42.7. France’s manufacturing…

Euro Area small caps typically outperform large caps whenever the trade weighted euro appreciates and underperform whenever it depreciates. The rationale is simple. Most European large cap companies are large multinationals that export their products outside…

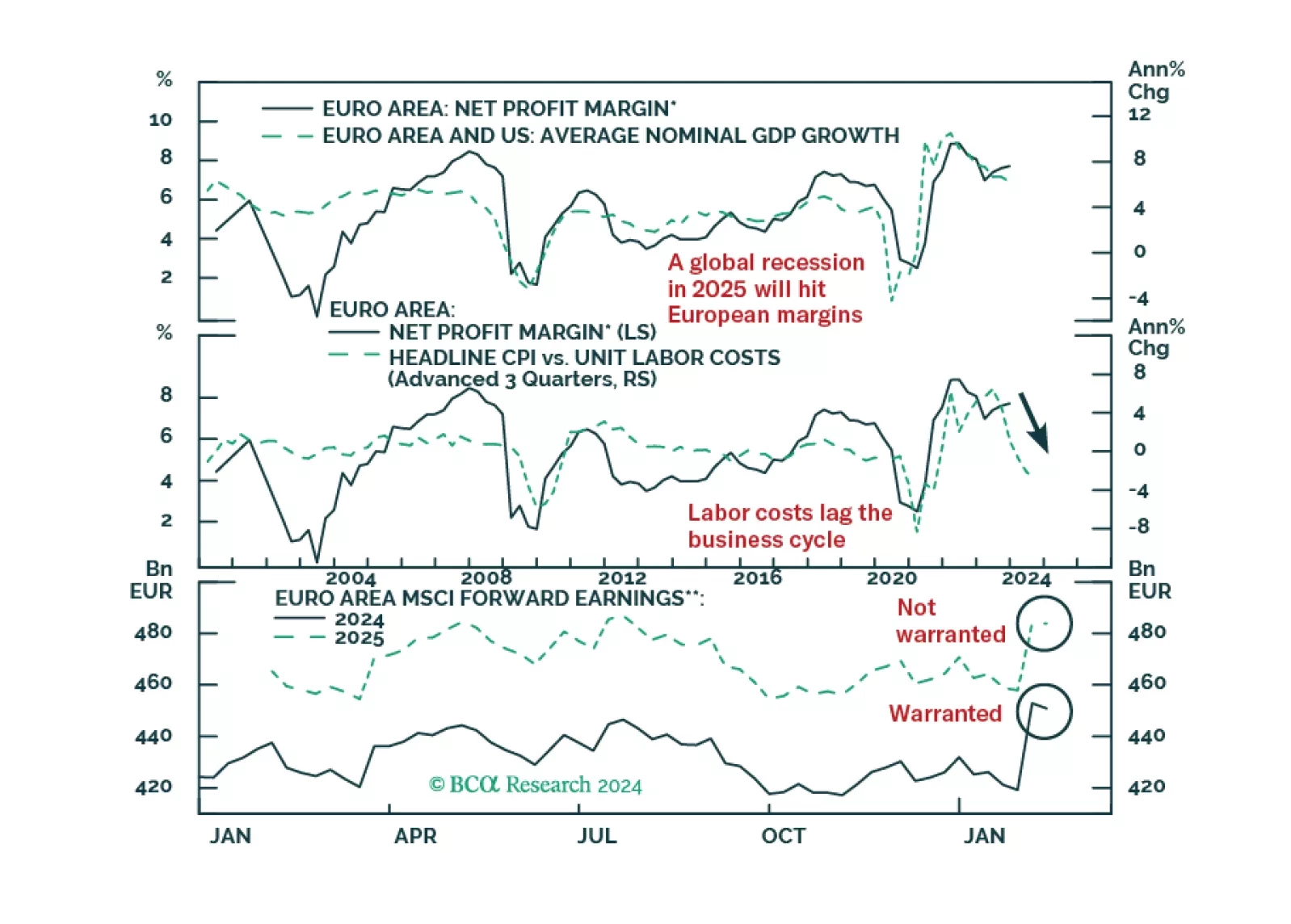

According to BCA Research's European Investment Strategy service, European profit margins have downside because they are both elevated and procyclical. European net margins stand at 7.7% above their long-term average of 5%. Analyst expectations…

European profits margins are elevated. Will a mild recession be enough to bring them down?

UK inflation came in hotter than expected in March. Headline CPI inflation was unchanged at 0.6% m/m – above expectations of a slowdown to 0.4% m/m. Moreover, while the headline and core measures both decelerated on an annual basis, they exceeded consensus…

UK stocks posted one of the largest positive abnormal returns (z-score) among the major financial markets we tracked in March. The MSCI UK index has gained 2% relative to Eurozone stocks since late February. However, the relative performance of UK equities…

Optimism about the future continues to boost investor confidence in the Euro Area. The ZEW Expectations series for the Eurozone (+10.4 to 43.9) and Germany (+11.2 to 42.9) surged and are now both at their highest in 26 months. Although investors’…

Headline inflation in Sweden came in at 4.1% in March. Lower food prices as well as lower inflation for recreation and culture were the main contributors to the drop. The biggest positive contributor was housing due to higher mortgage costs. The CPIF…