Equities

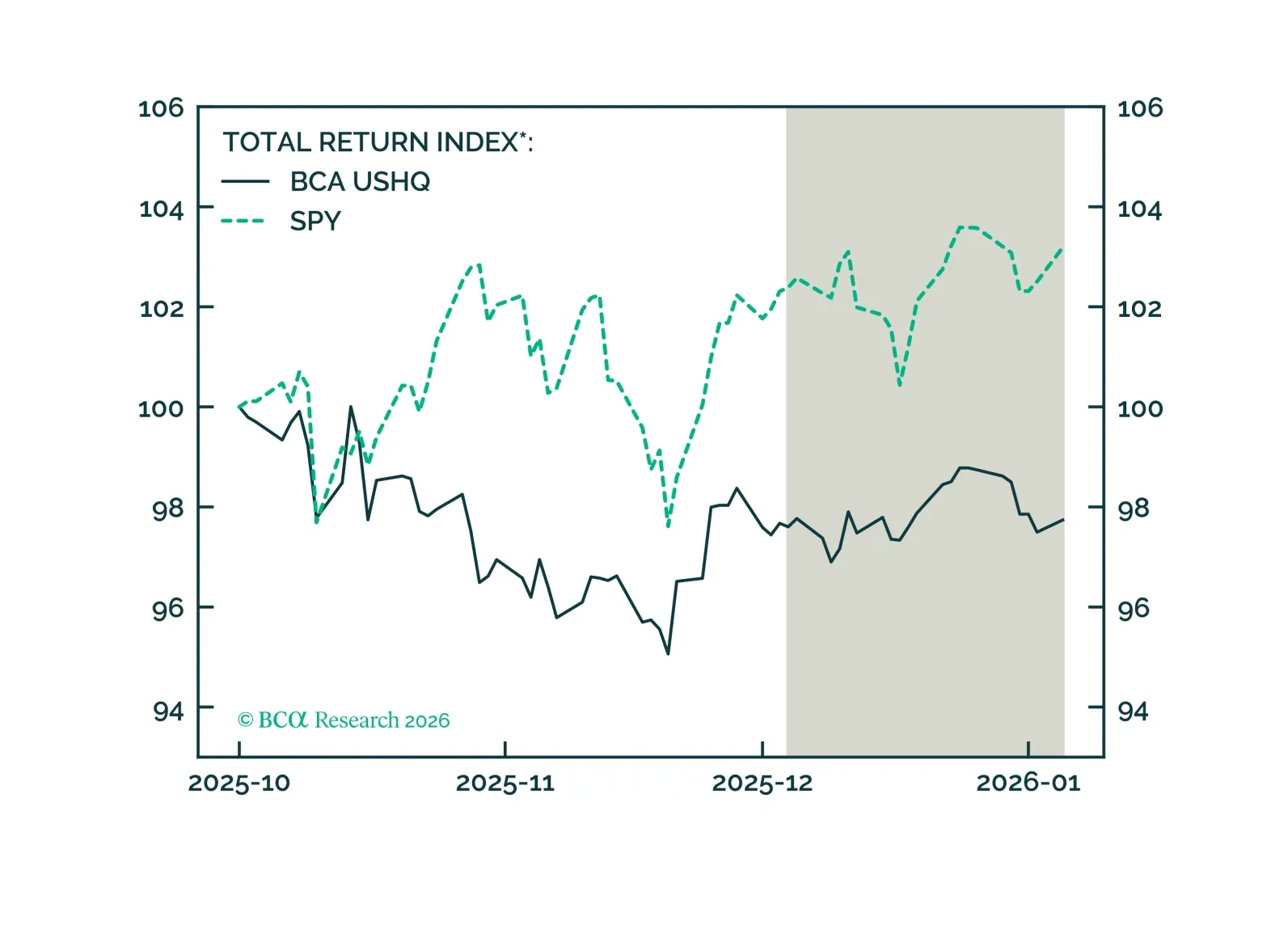

The US High Quality portfolio underperformed its benchmark through December, returning 0.14%, while its SPY benchmark returned 0.78%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 545bps.

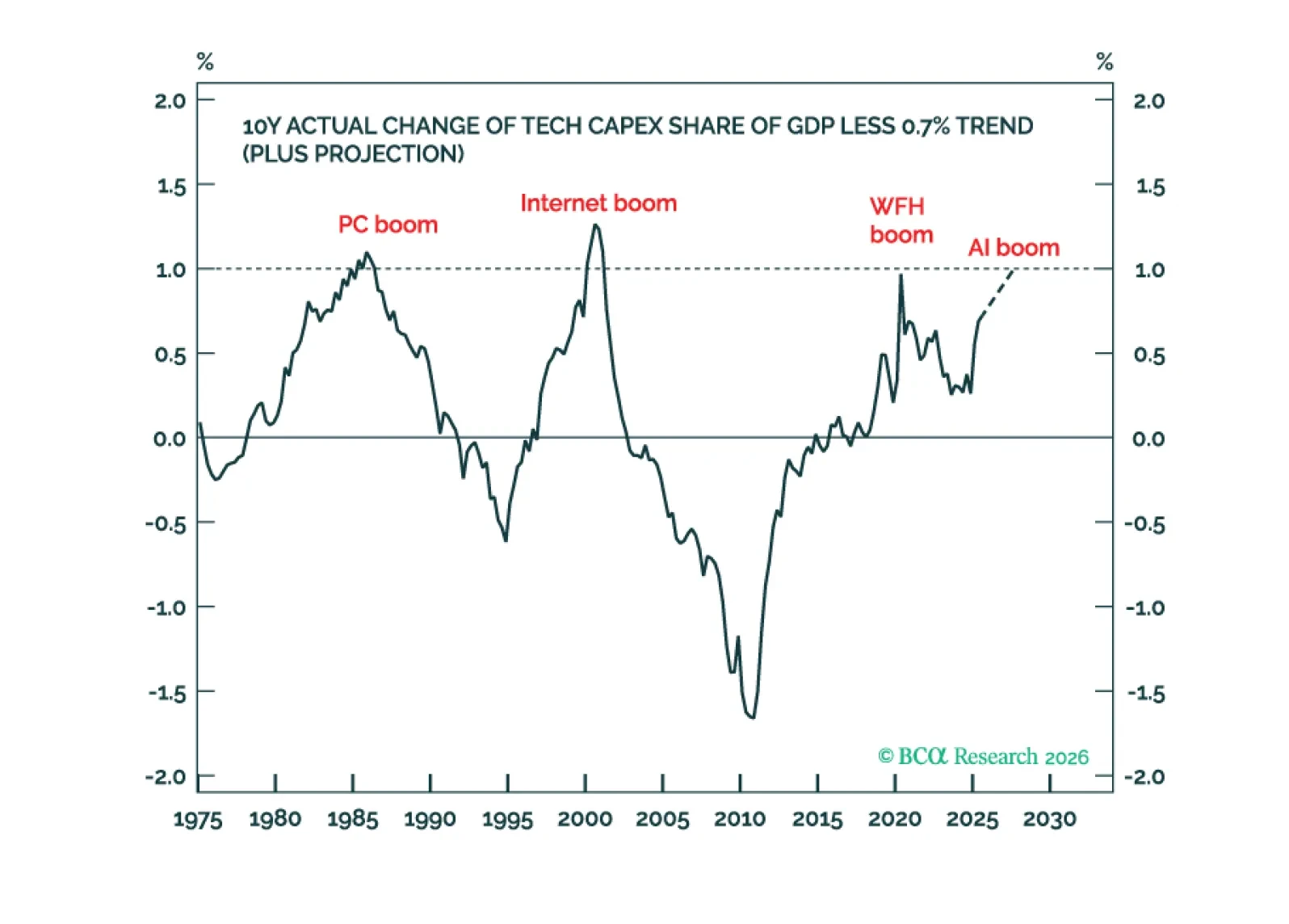

2026 has closer parallels with 2021 than with 2000 because an ultra-accommodative Fed can prolong the stock market rally even as a tech capex boom ends. Plus, a new tactical trade is short silver versus gold.

MacroQuant has downgraded equities to underweight, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is still bullish on gold.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

The bull versus bear battlelines are drawn for 2026: The friendliest Fed meets the most concentrated stock market rally ever. This last report of the year goes through the 10 key views for 2026 that emanate from this fascinating setup.

We are constructive on equities in 2026, as monetary easing, fiscal support, GenAI-related capex, and strong earnings growth are unequivocally positive for the asset class. Valuations are extended, but concerns about a bubble are overstated. Despite the favorable backdrop, we expect the S&P 500 to return only 5–10%, ending 2026 between 7,200 and 7,500.

Our 2026 Outlook presents our five key views for Europe’s macro landscape and markets in 2026 —a year poised to reveal the true strength of the recovery.

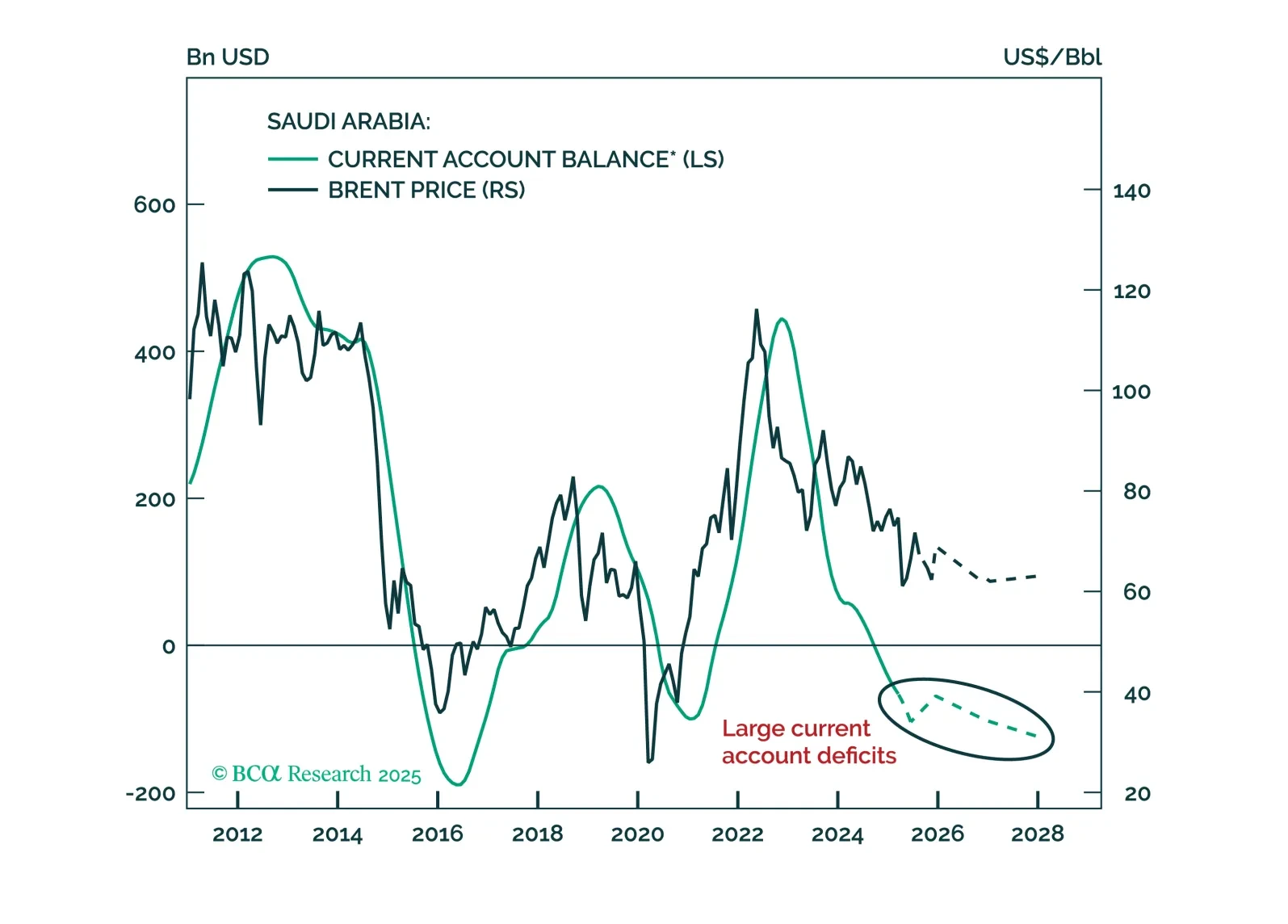

The Kingdom faces a troika of global factors in the next 12-18 months: (1) US policy rates will be cut considerably; (2) the US dollar will depreciate significantly; and (3) crude prices will remain low.

How should investors position themselves in this market?

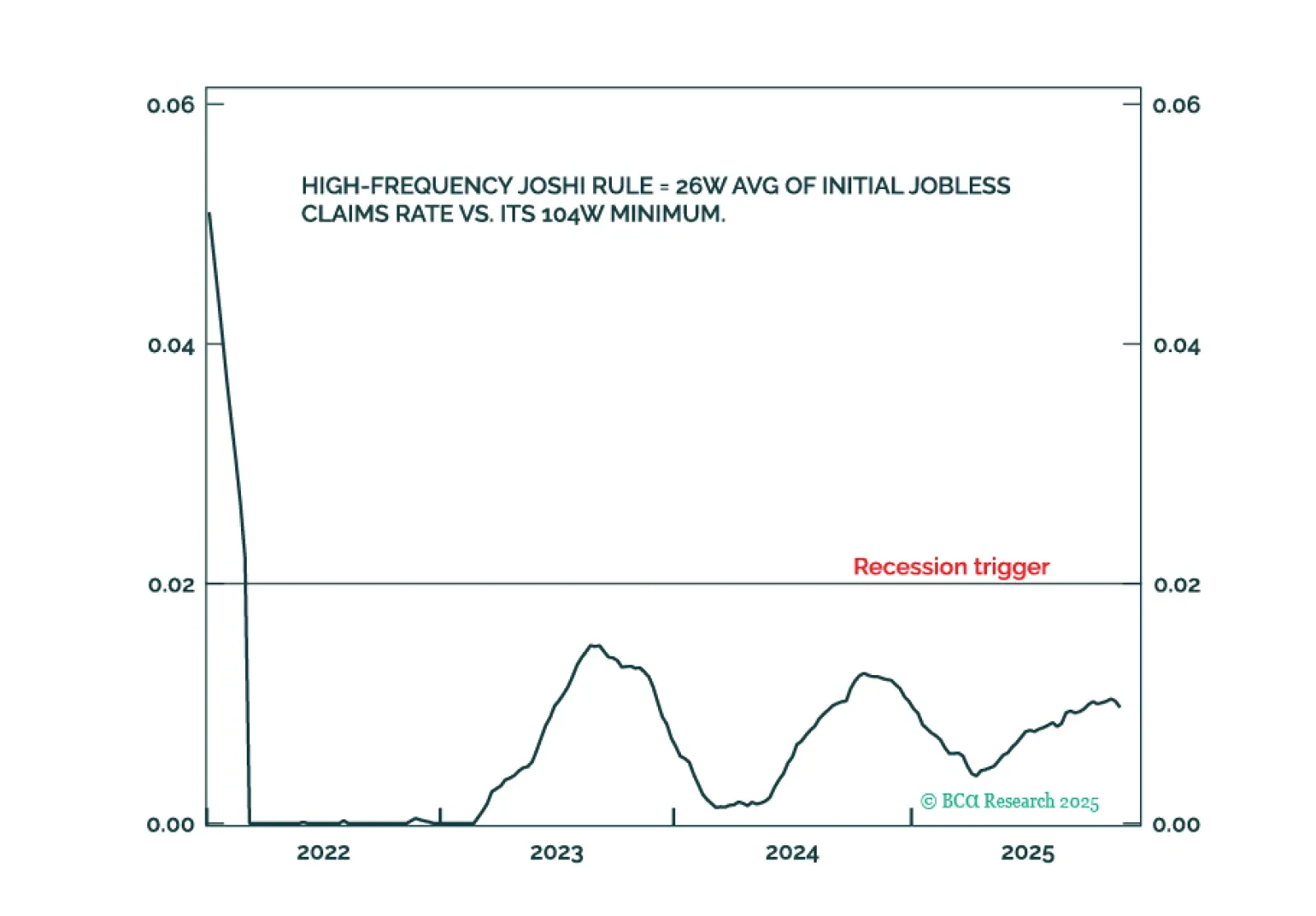

The high-frequency Joshi Rule confirms that the US labour market is holding up. Equity investors should regard 5-10 percent selloffs as tactical buying opportunities. Bond investors should stay underweight US duration. Plus, a new high-conviction trade is to go overweight the 30-year German bund versus the 30-year US T-bond.

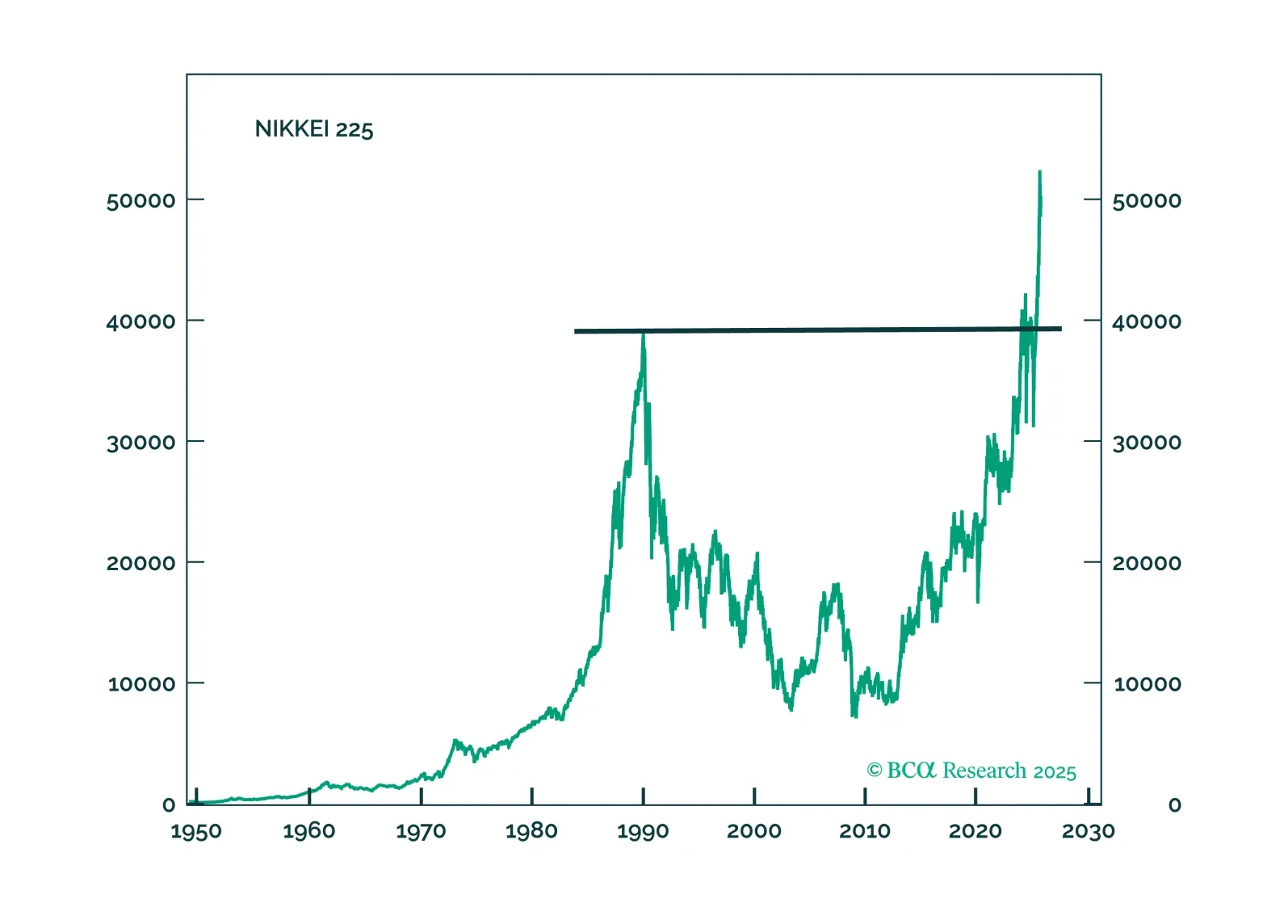

Japanese financial assets will finally have unfettered access to outsized returns. This performance will come in fits and starts, but we are comfortable laying our cards down on buying the yen, and Japanese industrial stocks.