Equities

The Bank of Japan’s Economy Watchers Survey – a gauge of sentiment among business owners – disappointed in April. The Current Conditions and the Outlook indices deteriorated from 49.8 to 47.4 (20-month low) and from 51.2 to 48.5 (16-month low), below…

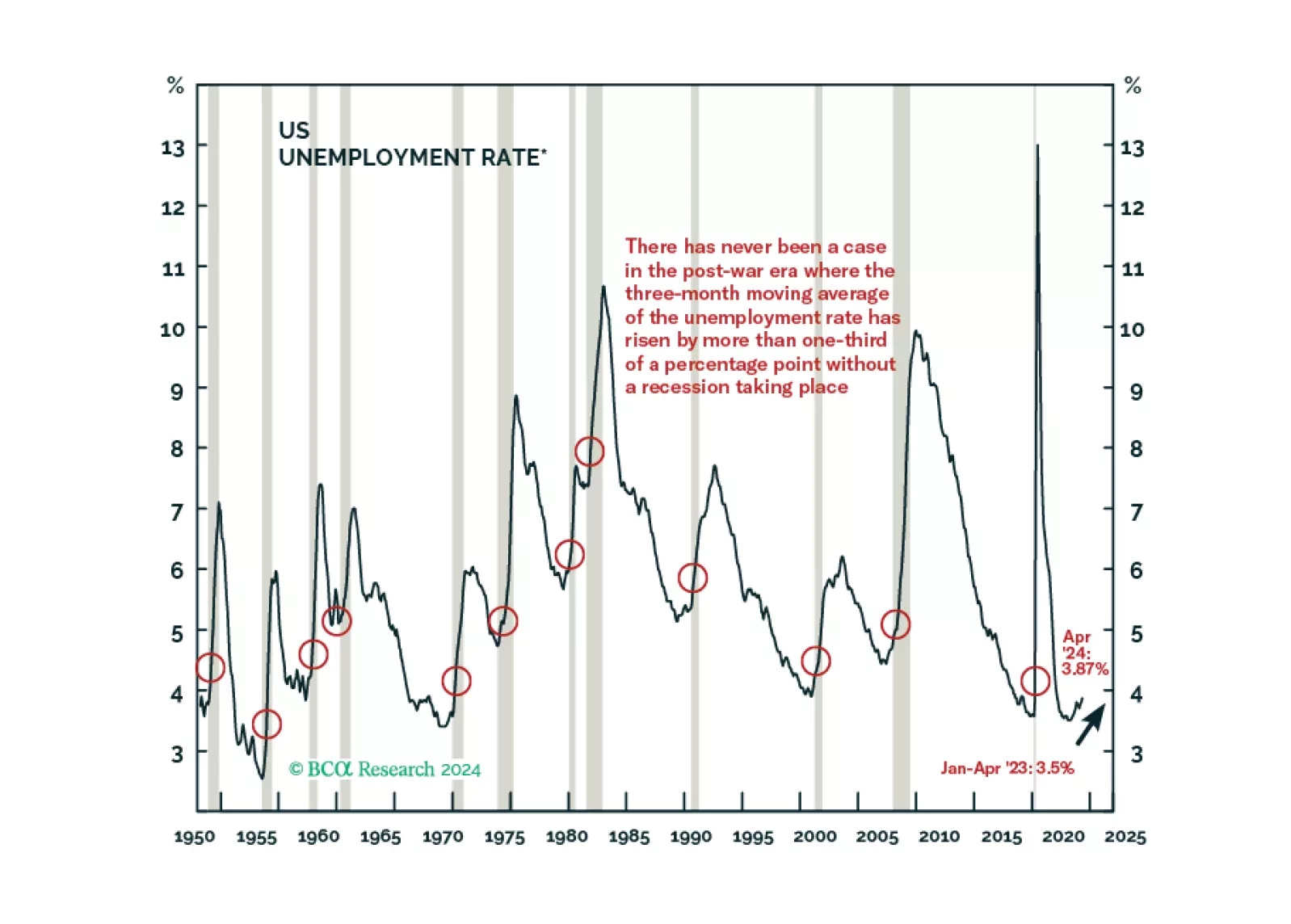

Emergency pandemic policies elongated the lag between Fed rate hikes and an observable slowdown in the economy. Notably, fiscal transfers and constrained consumption options endowed households with more than $2 trillion of savings they would not otherwise…

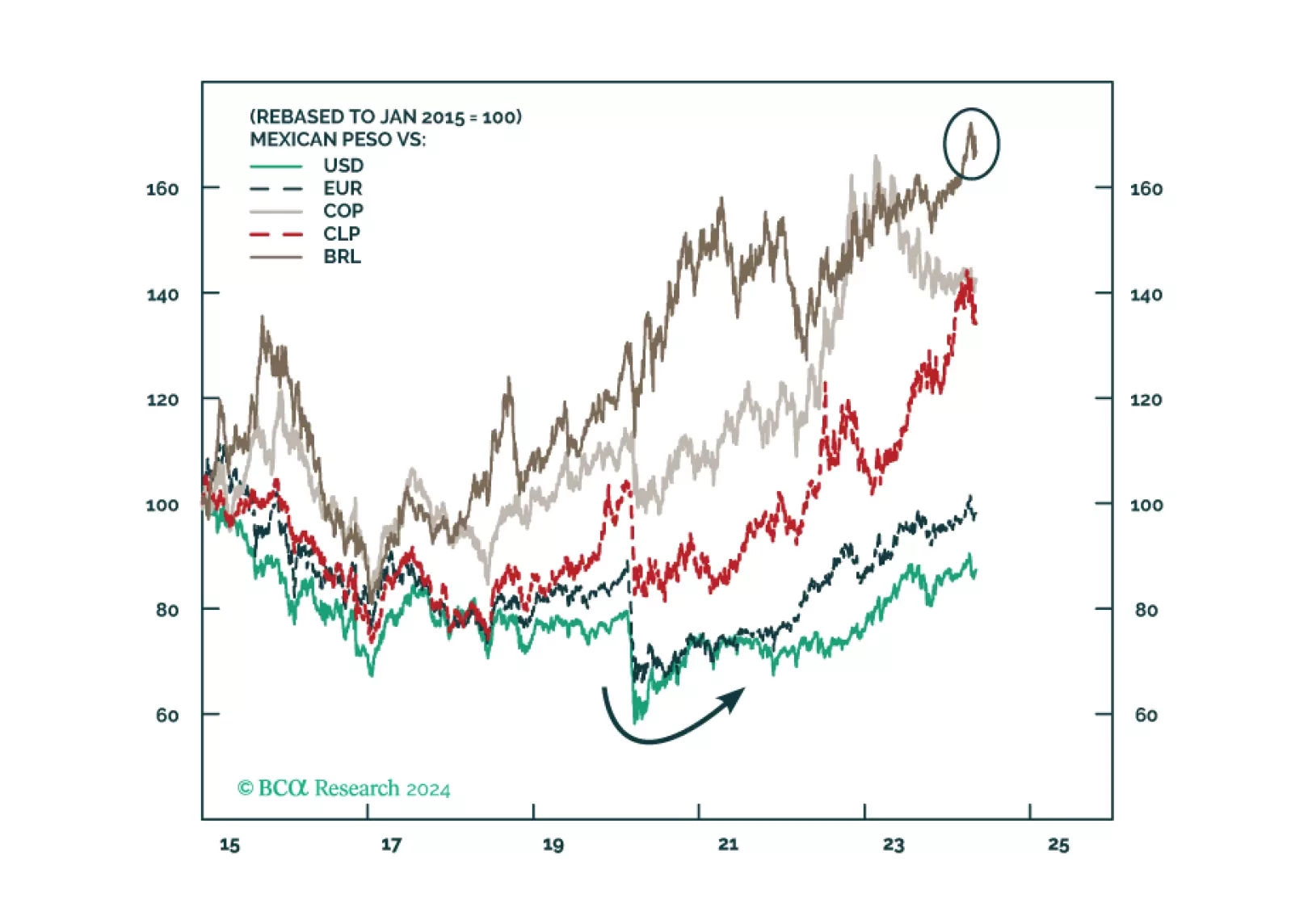

According to BCA Research’s Geopolitical Strategy service, Mexico’s presidential election on June 2 is likely to produce policy continuity, but a big win for the ruling party would be market-negative, at least initially. There is a 60% subjective…

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.

The idea that rising interest rates benefit value at the expense of growth has become consensus amongst market participants. The rationale is simple: Most of the cashflow that shareholders will receive from growth stocks are farther into the future than…

Upward growth revisions for China and India have led the IMF to recently upgrade its 2024 growth forecast for Asia to 4.5% from 4.2%. The regional growth forecast for 2025 remains unchanged at 4.3%. The IMF now expects the Chinese economy to grow at a 4.6%…

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

The revival in global growth momentum continued in April. The JPM Global Manufacturing PMI came in at 50.3, marking its third consecutive month of expansion. Details underscored solid demand conditions. Output and new orders continued to rise and new…

In a widely expected move, the Riksbank cut its policy rate by 25 basis points on Wednesday from 4% to 3.75%. The policy statement highlighted that inflation is approaching its 2% target, that leading indicators are pointing to further downside in prices and…

Health care stocks have underperformed the US broad market by over 20% since the beginning of 2023. Indeed, vaccination campaigns during the pandemic years had initially boosted health care companies’ earnings. However, this tailwind eventually faded.…