Equities

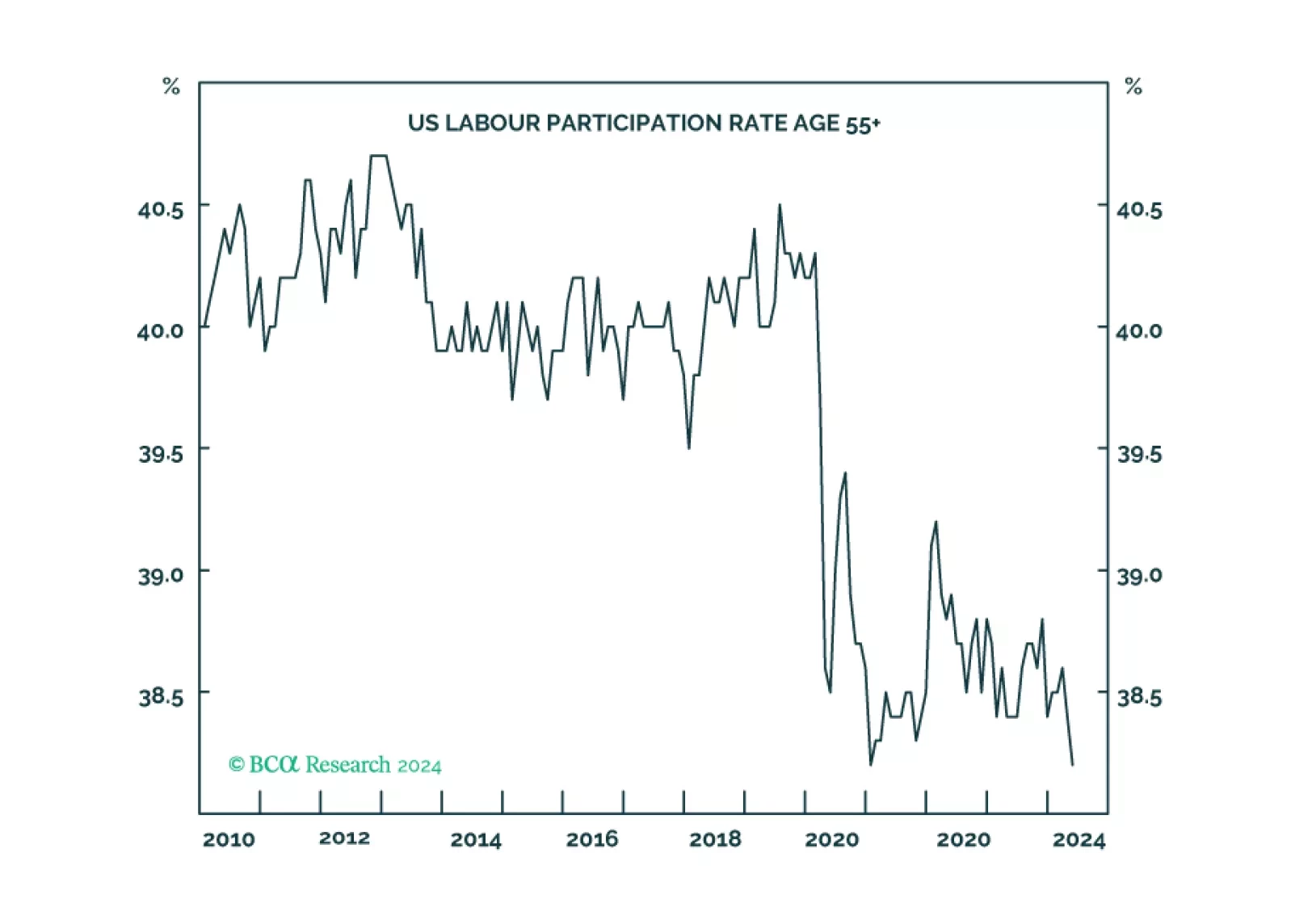

1 in 17 older Americans workers have gone missing either through ‘excess retirements’ or ‘excess mortality’. The consequent dislocation of the labour market means that the Fed’s work is not yet done. We go through some investment implications. Plus: the China and Japan rallies are exhausted.

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

Investors often misjudge Global Macro managers. We outline key manager evaluation criteria and highlight the power of combining Macro Hedge Funds and Private Equity. Even for those who are not Macro Traders nor invest in Hedge Funds, this report may change the way you assess potential employees, partners, and even yourself—the most critical elements of any investment strategy.