Equities

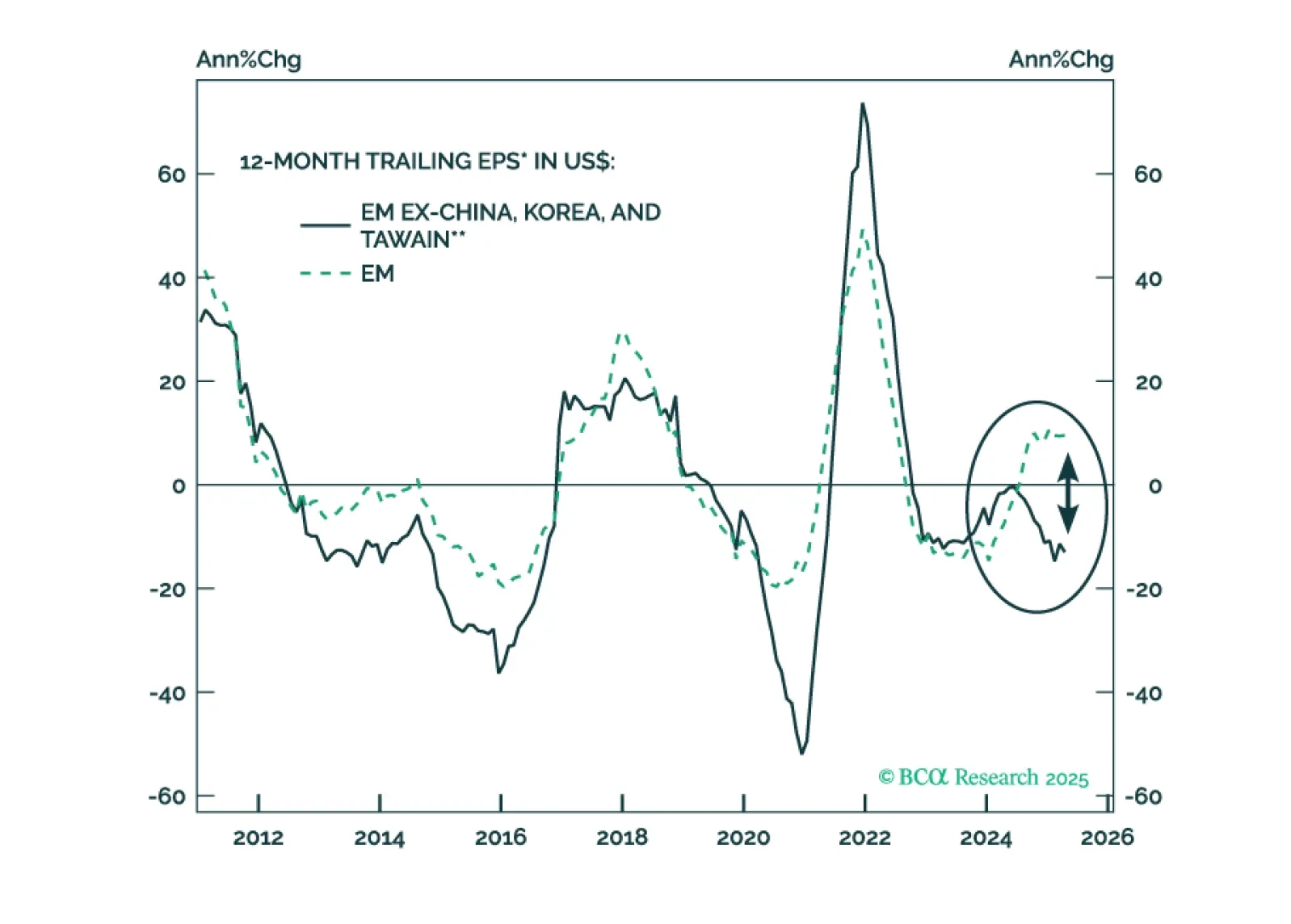

The EM EPS recovery has been narrow, solely driven by TMT stocks in China, Korea, and Taiwan. EM corporate profits are set to contract in the next six to nine months. Unlike in the past, US dollar weakness will be deflationary, not reflationary, for EM share prices.

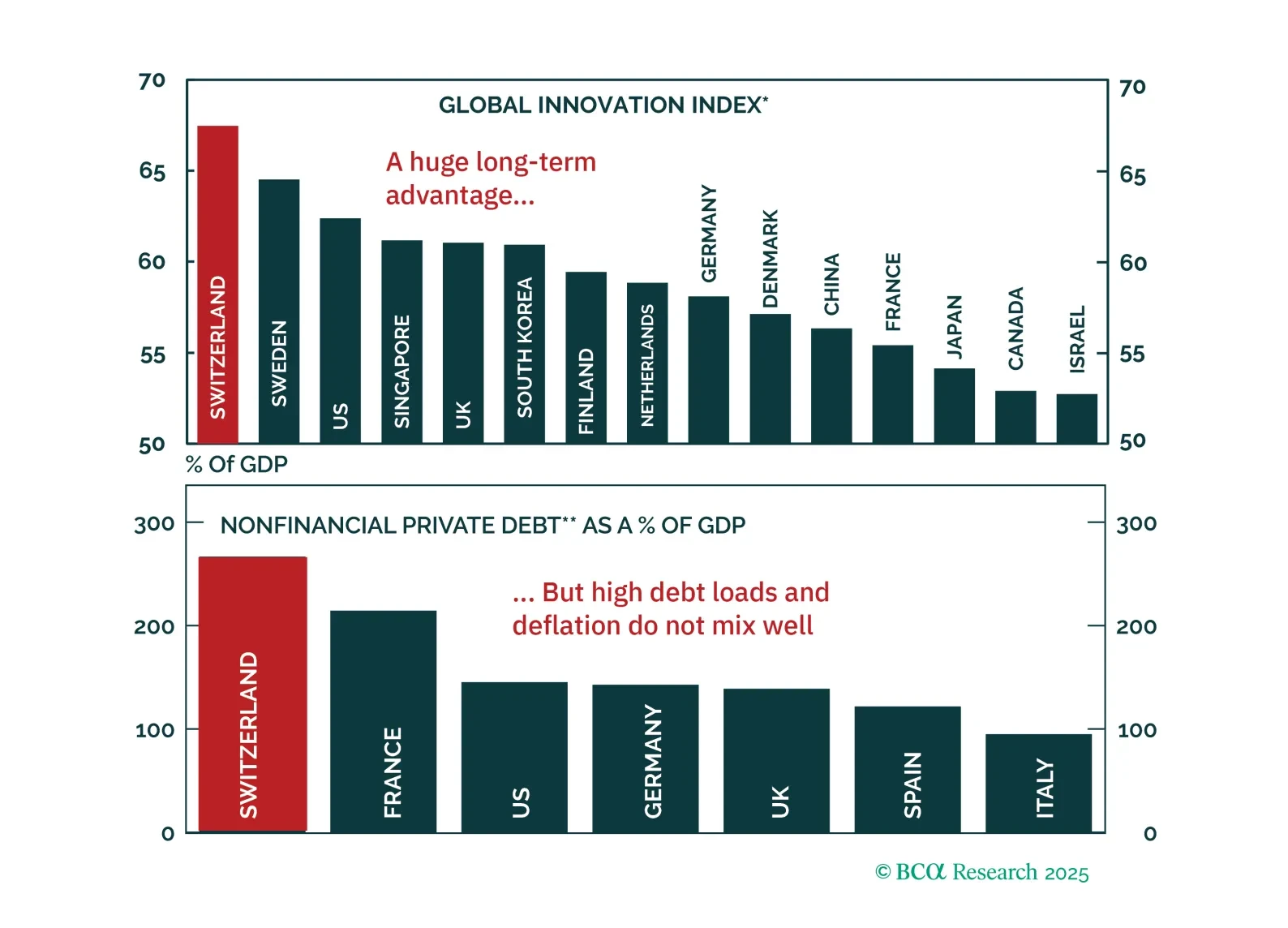

Switzerland looks pristine, but the near-term risks are mounting. Deflation pressures, overvalued assets, and a highly exposed export sector leave the economy vulnerable to a slowdown. This report explores why the SNB will ease more than markets expect, and how to position across CHF, equities, and bonds.

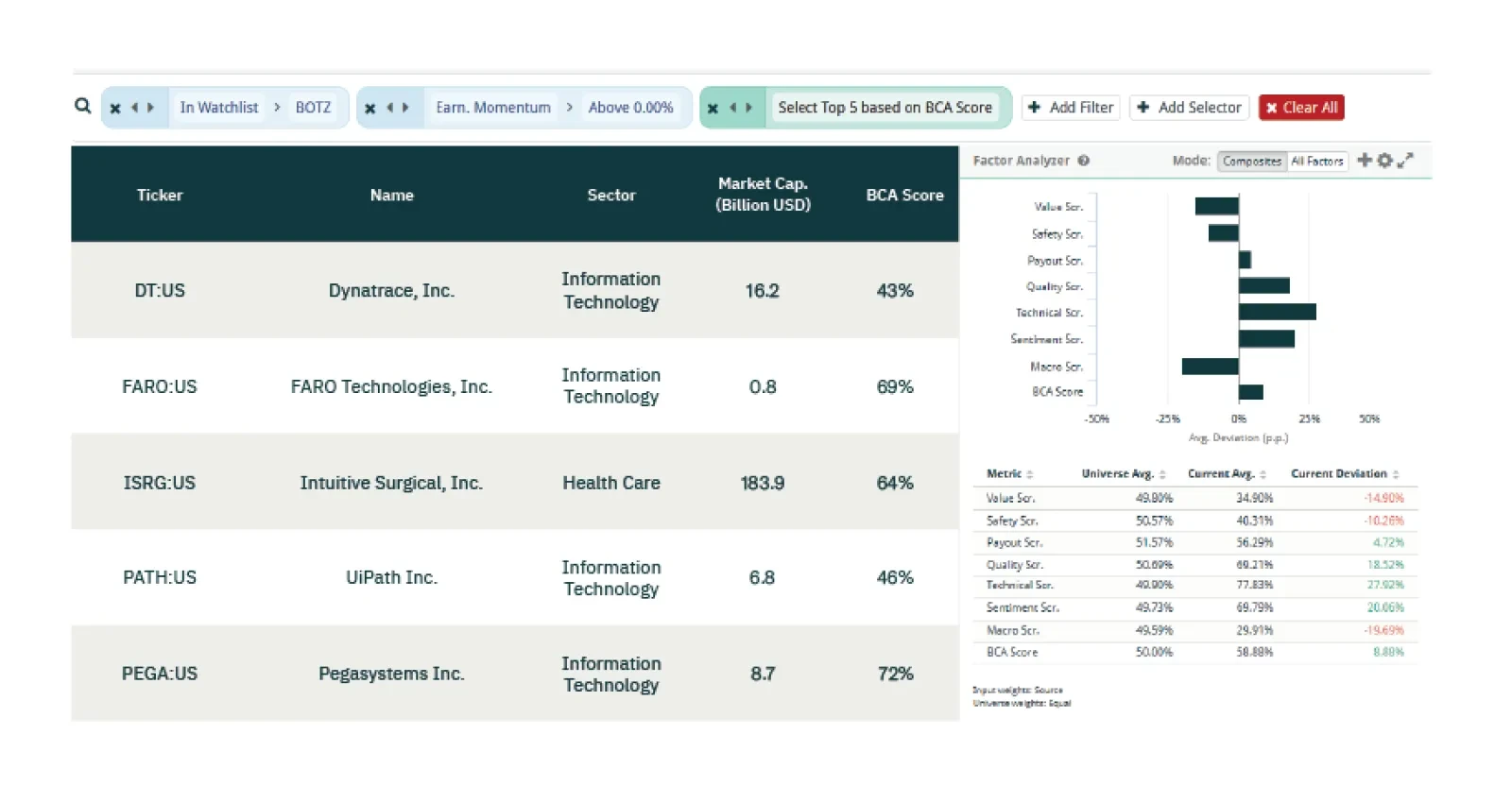

This week our three screeners explore equity trades in Robotics, European Quality and Technical, and Hong Kong.

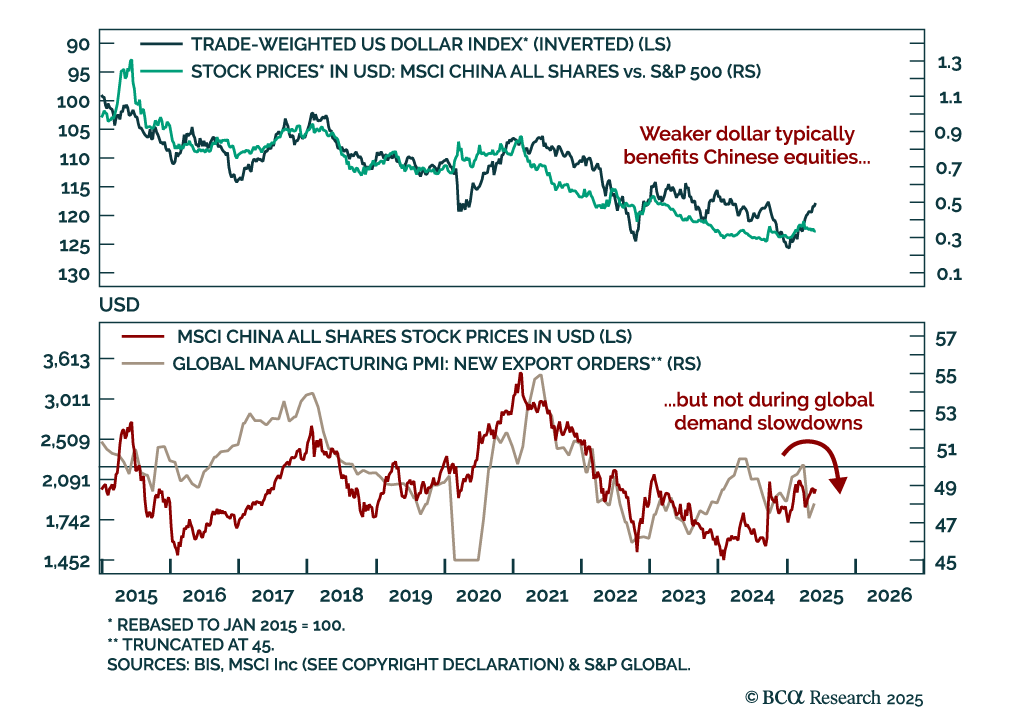

The London Sino-US trade talks offered hope of de-escalation, but Chinese equities remain under pressure from deflationary headwinds and lack a clear macro catalyst to trend higher.