Equities

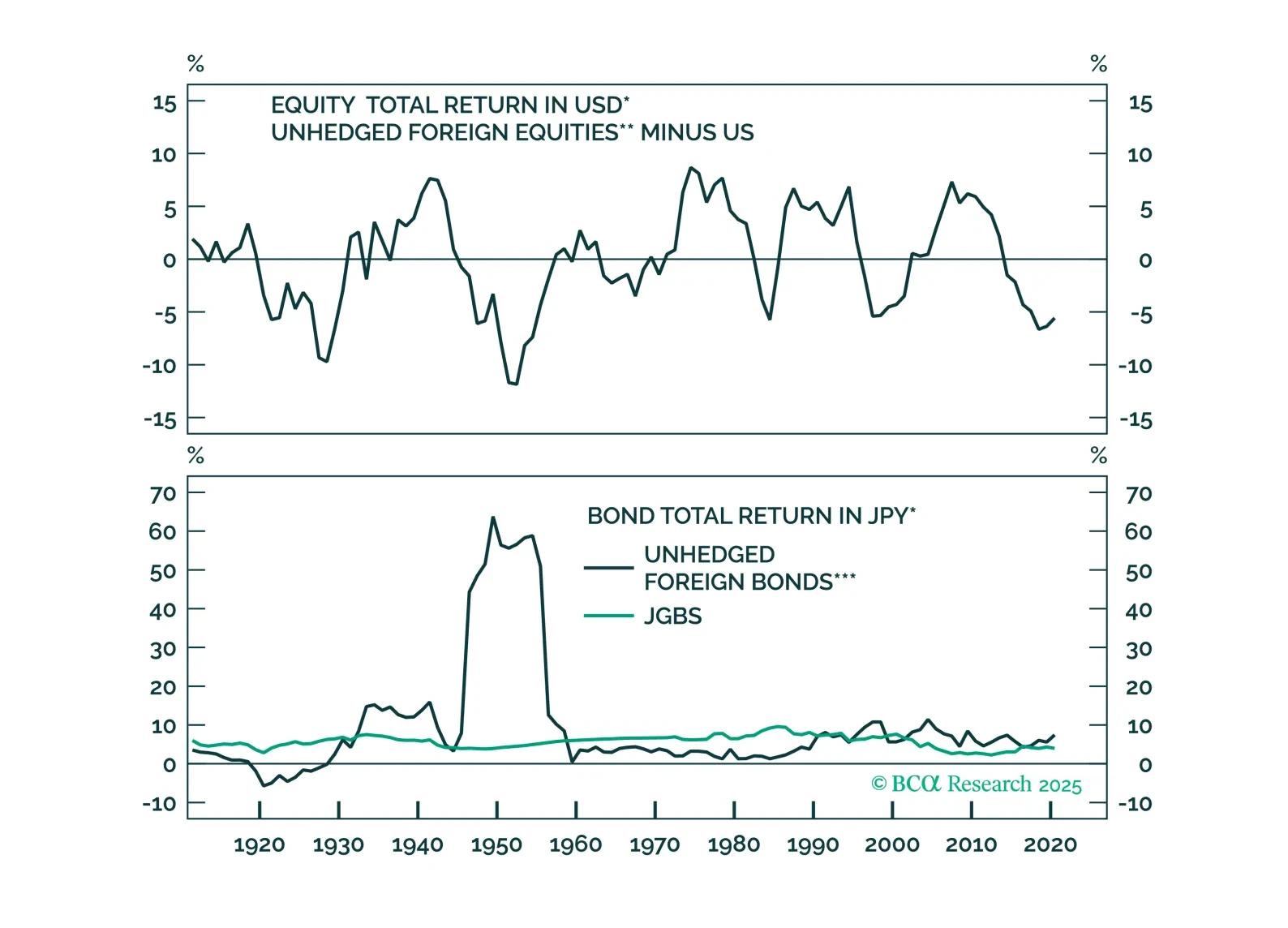

Our latest report analyzes home bias in bonds and equities across 15 countries. The verdict?

Hedged international bonds outperform domestic peers, especially during high inflation. In equities, even top markets like the US have had multi-year periods of underperformance. Allocators should leave patriotism aside when running their portfolios.

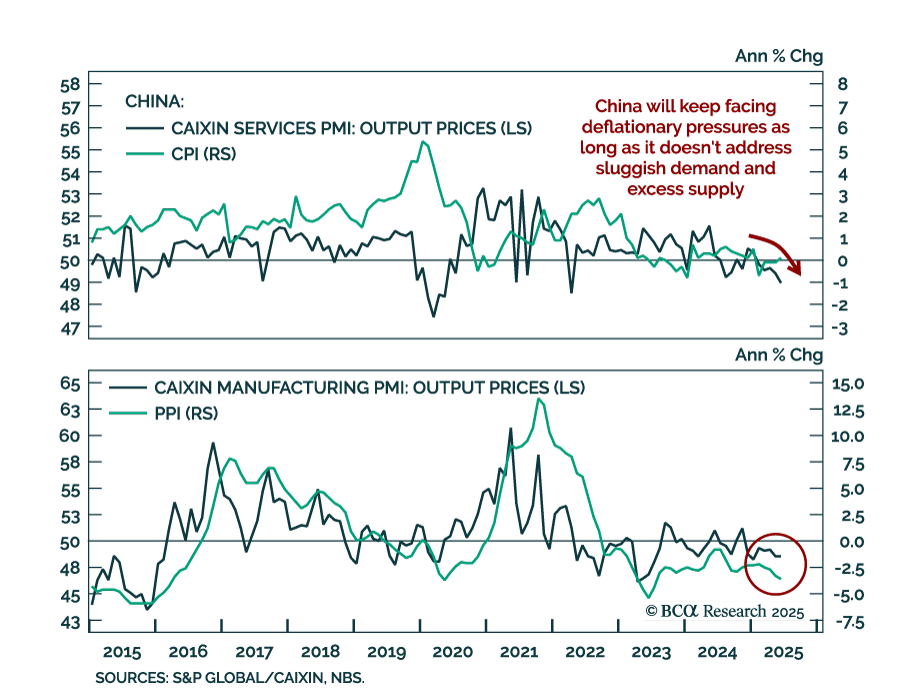

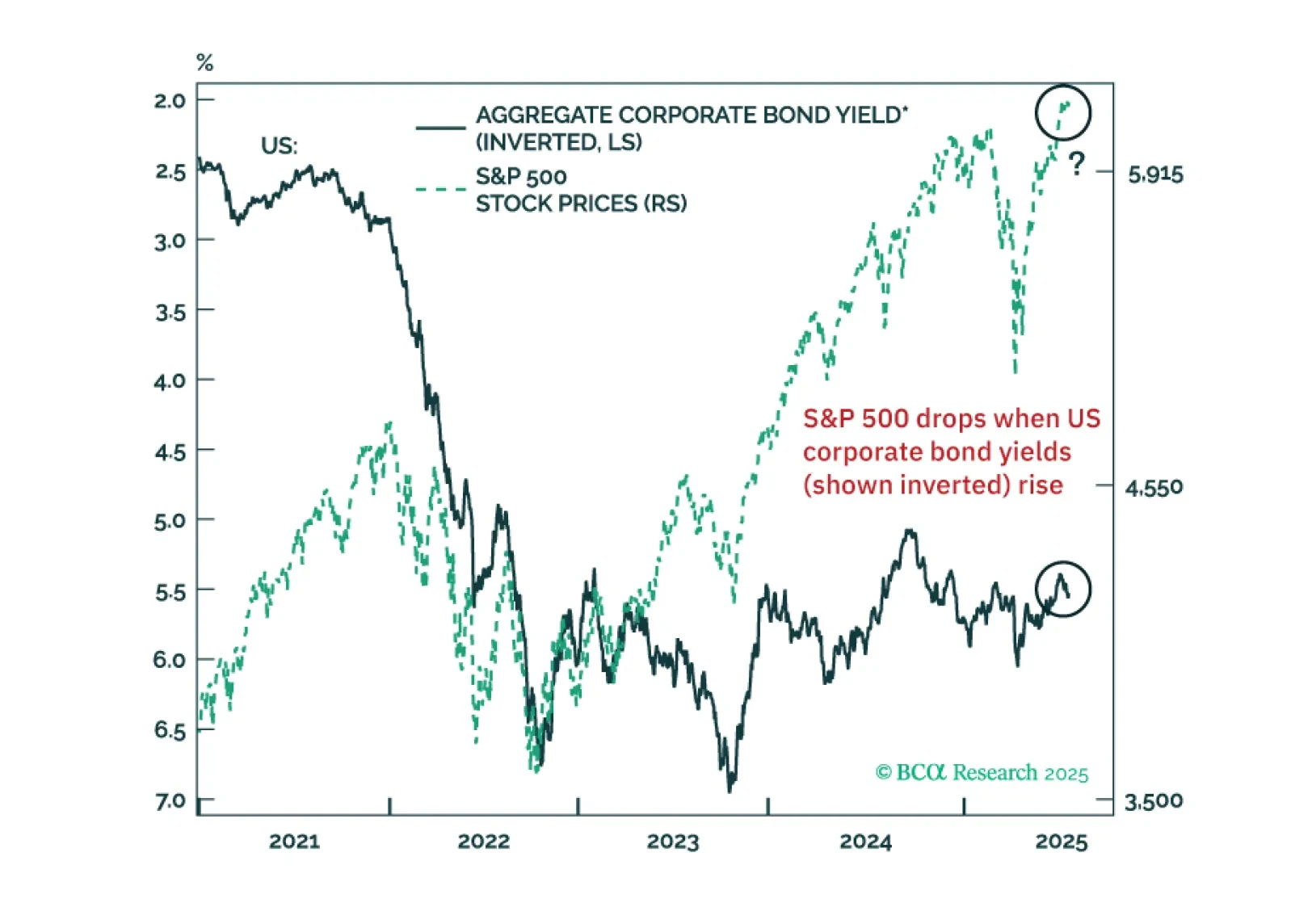

US equity investors should heed warning signals from US corporate bond yields. There are early red flags for EM share prices. Global trade will shrink in H2 2025. China’s economic tailwinds from H1 2025 – fiscal and export frontloading – are coming to an end.

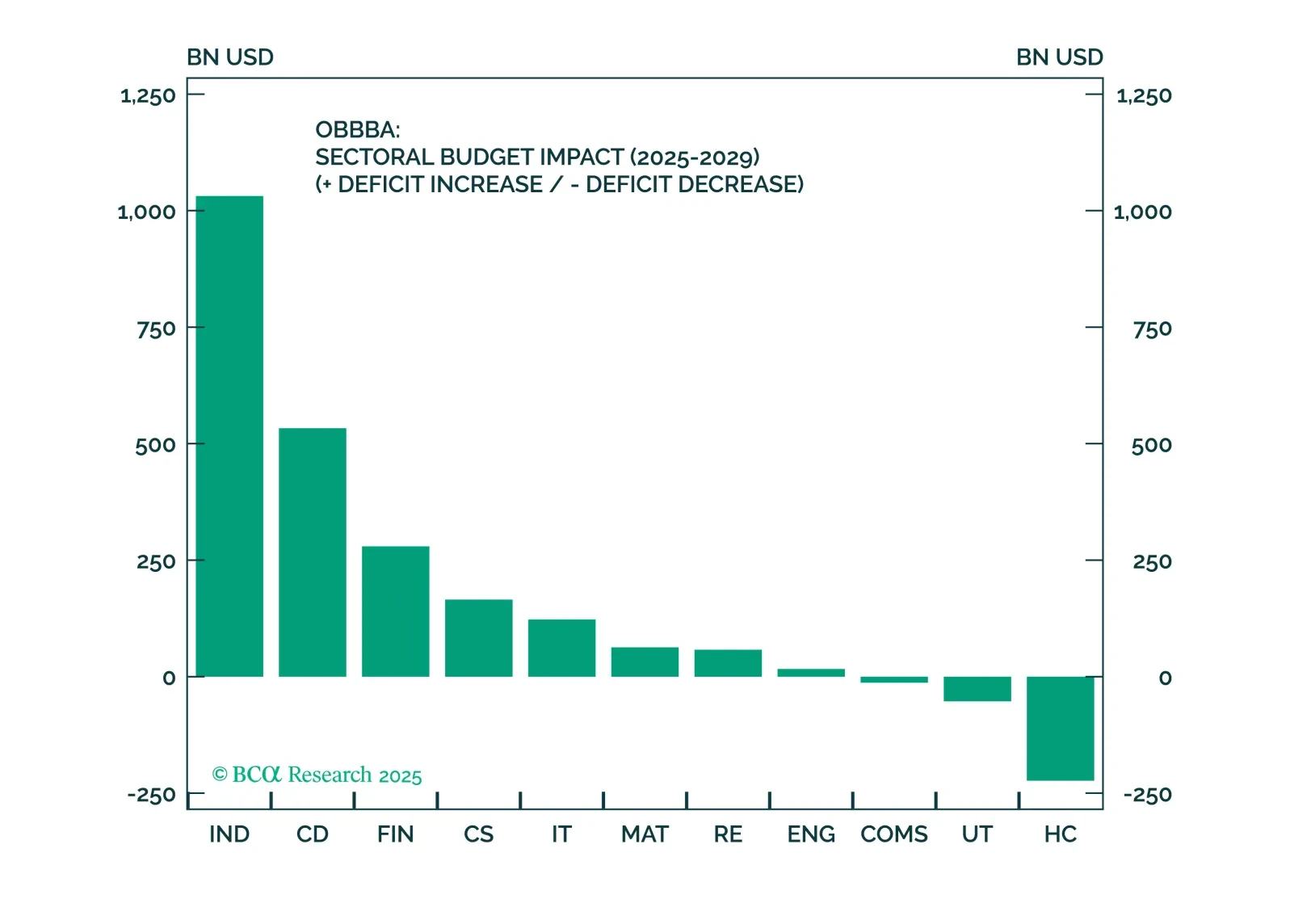

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

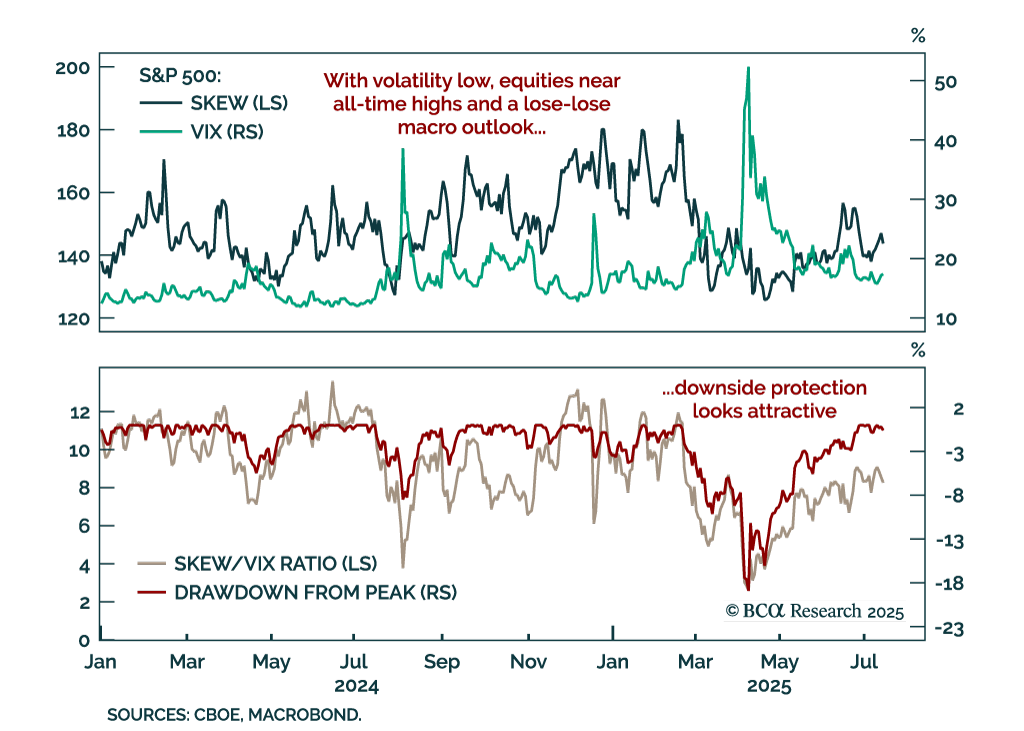

We still believe a recession looms, but it has yet to rear its ugly head. We continue to recommend investors position defensively, but we will change tack if clear signs of a recession don’t emerge soon.

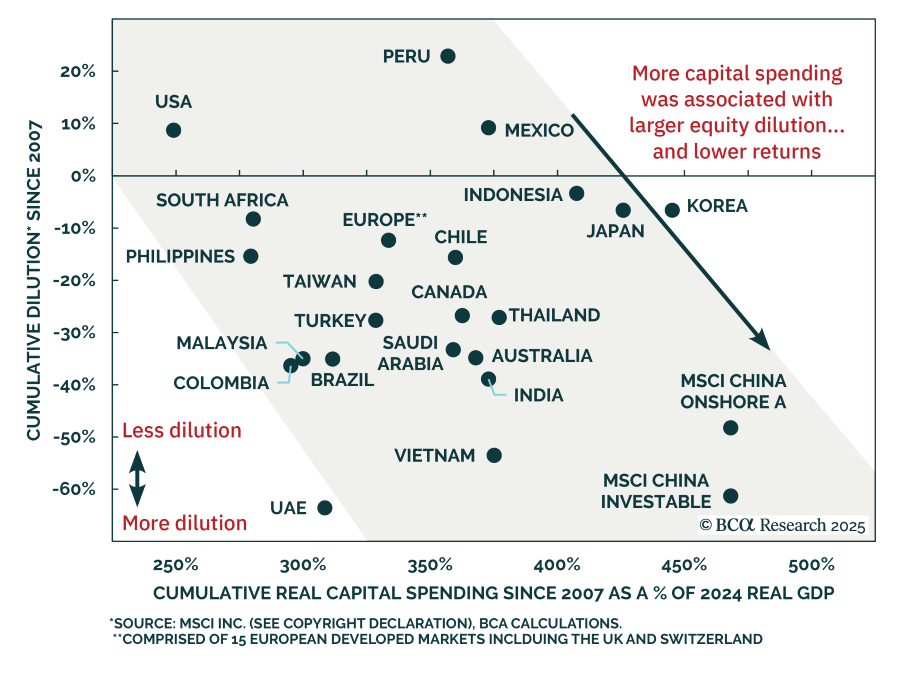

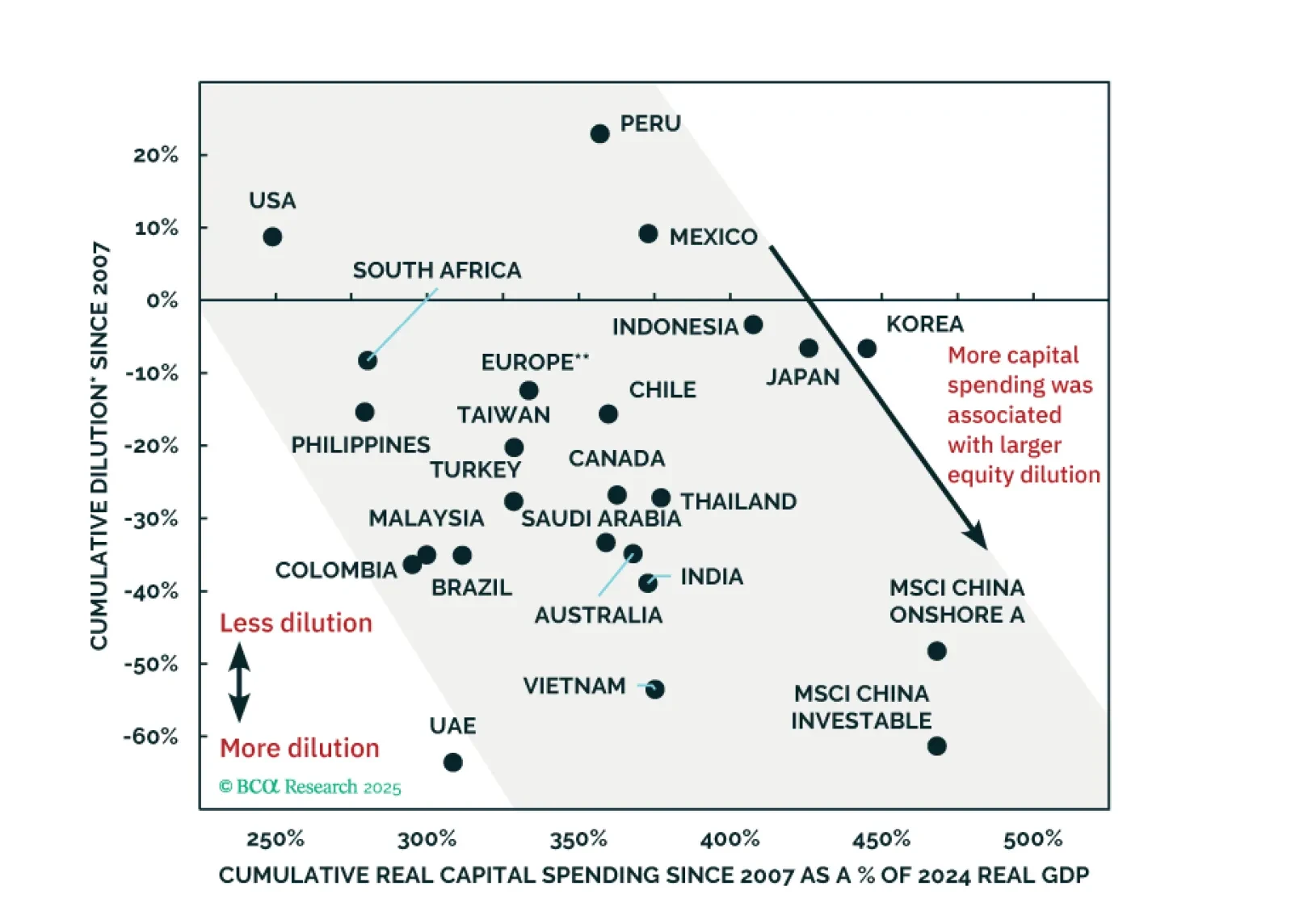

Economic growth and rapid expansions do not always translate into higher EPS and shareholder returns. One of the key reasons is dilution. We offer a typology of dilution: (1) “offensive”, (2) “defensive”, (3) corporate governance-linked, and (4) idiosyncratic cases.