Equities

Executive Summary Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Inflation is not about oil, food or used car prices. Looking at prices of individual components of a consumer basket is akin to missing the forest for the trees. Despite the latest drop in US headline inflation, various core CPI measures continue trending up and registered considerable month-on-month rises in July. Wages and, more specifically, unit labor costs are the true measure of genuine and persistent inflation. US wage growth is very elevated, and the pace of unit labor cost gains has surged to a 40-year high. The conditions for sustainable and persistent disinflation in the US are not yet present. US inflation will prove to be much stickier and more entrenched than many market participants presently believe. The recovery in China will be U- rather than V-shaped, with risks tilted to the downside. The mainland’s property market breakdown is structural, not cyclical. Excesses are very large, and problems are snowballing, rendering the enacted policy stimulus insufficient. Bottom Line: US core inflation lingering above 4% and easing financial conditions will compel the Fed to continue hiking rates. This will cap global risk asset prices and put a floor under the US dollar. We continue to recommend an underweight allocation to EM in global equity and credit portfolios. Consistently, we are also reluctant to chase EM currencies higher. Feature The bullish macro narrative circulating in the investment community is that conditions for a cyclical rally in global risk assets have fallen into place. Specifically: US inflation will drop sharply as US growth has crested and commodity prices have plunged; The Fed is nearing the end of a tightening cycle; China has stimulated sufficiently, and its economy is about to recover, which will boost economic conditions among its trading partners in general and EM in particular. These assumptions along with the fact that the S&P 500 index has found support at a 3-year moving average – a proven line of defense – suggest that US share prices have likely bottomed (Chart 1). Are we witnessing déjà vu of the 2011, 2016, 2018 and 2020 market bottoms? Chart 1Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

We have reservations about all of the above fundamental conjectures. We elaborate on these reservations in this report. On the whole, we contend that the current environment is different, and the roadmaps of all post-2009 equity market bottoms are not necessarily currently applicable. BCA’s Emerging Markets Strategy team believes that (1) US consumer price inflation is much more entrenched and will prove stickier than is commonly believed; and (2) the Chinese property market’s breakdown is structural, not cyclical; hence, the recovery will not gain traction easily. Is This The End Of The US Inflation Problem? Not Quite This week’s US inflation data confirmed that headline CPI inflation has probably peaked: prices in several categories plunged. However, inflation is not about oil, food or used car prices. Chart 2 reveals that historically there have been several episodes whereby core inflation remains elevated despite plunging oil prices. Chart 2US Core Inflation Does Not Always Follow Oil Prices

US Core Inflation Does Not Always Follow Oil Prices

US Core Inflation Does Not Always Follow Oil Prices

Looking at price dynamics among the individual components of the CPI basket is akin to missing the forest for the trees. Inflation is a very inert and persistent phenomenon. Underlying inflation does not change its direction often and/or quickly. That is why we believe that it is premature to celebrate the end of the US inflation problem. A few observations on this matter: Despite the drop in US headline inflation, various core CPI measures − like trimmed-mean CPI, median CPI and core sticky CPI − all continue trending up and registered substantial month-on-month rises in July (Chart 3). The range of core inflation based on these annual and month-month annualized rates is between 4-7%. In brief, the rate of genuine/sticky inflation is well above the Fed’s 2% target. Given its unconditional commitment to bringing inflation down to 2%, the Fed will continue hiking interest rates ceteris paribus. Chart 3US Core CPI Measures Are Still Very High

US Core CPI Measures Are Still Very High

US Core CPI Measures Are Still Very High

Chart 4US Wages Growth Has Been Surging

US Wages Growth Has Been Surging

US Wages Growth Has Been Surging

We continue to emphasize that wages and, more specifically, unit labor costs are the true measures of persistent and genuine inflation. We have written at length about why wages and unit labor costs are more important to inflation than oil or food prices. US wage growth is very elevated and is accelerating (Chart 4). Unit labor costs, calculated as hourly wages divided by productivity, have also been surging to a 40-year high (Chart 5, top panel). Chart 5Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

The reason for this very strong wage growth and swelling unit labor costs is the very tight labor market. The bottom panel of Chart 5 demonstrates that labor demand is still outpacing labor supply by a wide margin. Hence, wage inflation will not subside until the unemployment rate rises meaningfully. Bottom Line: Conditions for sustainable and persistent disinflation in the US are not yet present. Inflation will prove to be much stickier and more entrenched than many market participants presently believe. Core inflation lingering above 4% and easing financial conditions will compel the Fed to continue hiking rates. This will cap risk asset prices and put a floor under the US dollar. China: Is This Time Different? If one believes that China’s current business cycle is similar to all previous ones seen since 2009, odds are that a buying opportunity in China-related financial markets is at hand. Chart 6 illustrates that the credit and fiscal spending impulse leads the business cycle by about nine months. Given that this impulse bottomed late last year, a trough in the Chinese business cycle is due. Chart 6Is A Recovery In China's Business Cycle Imminent?

Is A Recovery In China's Business Cycle Imminent?

Is A Recovery In China's Business Cycle Imminent?

It is always risky to suggest that this time is different. Nevertheless, at the risk of being wrong, we contend that a combination of (1) property markets woes, (2) an impending export contraction, and (3) the dynamic zero-COVID policy will reduce the multiplier effect of current stimulus measures. Hence, a meaningful recovery in economic activity will likely fail to materialize in the coming months. The challenges facing the mainland property market are now well known. Yet, excesses are very large, and problems are snowballing, making policy stimulus insufficient. In particular: Authorities are contemplating bailout funds for property developers in the range of RMB 300-400 billion to enable them to complete housing that has been pre-sold. This is not sufficient financing for overall property construction. Table 1How Large Are Property Developers Bailout Funds?

Déjà Vu?

Déjà Vu?

Table 1 illustrates that these amounts are equal to just 3-4% of annual fixed-asset investment in real estate excluding land purchases, 1.5-2% of total financing of developers, and 3-4% of the advance payments that property developers received for pre-sold housing in 2021. Property developers will not be receiving any cash upon the completion and delivery of presold housing units because they were paid in advance. Hence, without liquidating their other assets, homebuilders cannot repay the bailout financing. Consequently, only state financing can work here because, from the viewpoint of providers of this financing, this scheme de-facto means throwing good money after bad. The property industry in China is extremely fragmented. This makes bailouts difficult to organize and execute. There are officially about 100,000 property developers in China. The overwhelming majority of them are not state-owned companies. Plus, the two largest property developers, Evergrande (before defaulting) and Country Garden, had only 3.8% and 3.3% of market share respectively in 2020. The failure of homebuilders to complete and deliver pre-sold housing units could unleash a death spiral for them. In recent years, 90% of housing units have been pre-sold, i.e., buyers made advance payments/prepayments, often taking out mortgages (Chart 7, top panel). Witnessing the inability of developers to deliver on presold units, a rising number of people may decide to wait to buy. The largest source of developers’ financing – advance payments for pre-sold housing units – might very well dry up. This source has accounted for 50% of real estate developers’ total financing in recent years (Chart 7, bottom panel). In brief, a vicious cycle is possible. The lack of financing for homebuilders bodes ill for construction activity (Chart 8). Chart 7China: Housing Presales And Pre-Payments Are Critical To Developers

China: Housing Presales And Pre-Payments Are Critical To Developers

China: Housing Presales And Pre-Payments Are Critical To Developers

Chart 8Lack Of Homebuilder Financing = Shrinking Construction Activity

Lack Of Homebuilder Financing = Shrinking Construction Activity

Lack Of Homebuilder Financing = Shrinking Construction Activity

Chart 9Chinese Property Developers Are Extremely Leveraged

Chinese Property Developers Are Extremely Leveraged

Chinese Property Developers Are Extremely Leveraged

Besides, property developers are very leveraged with an assets-to-equity ratio close to nine (Chart 9). They have grown accustomed to borrowing heavily to accumulate real estate assets. They have been starting but not completing construction (Chart 10, top panel). We have been referring to this phenomenon as the biggest carry trade in the world. The bottom panel of Chart 10 shows two different measures of residential floor space inventories held by property developers. One measure subtracts completed floor space from started floor space, and another one deducts sold floor space from started floor space. On both measures, residential inventories are enormous. In theory, they could raise funds by selling their real estate assets. However, if they all try to sell simultaneously, there will not be enough buyers, and asset prices will plunge, which could lead to a full-blown debt deflation spiral. The last time the real estate market was similarly distressed in 2014-15, the central bank launched the Pledged Supplementary Lending (PSL) facility. This was effectively a QE program to monetize housing. This was the reason why housing recovered strongly in 2016-2017. There is currently no such program up for discussion. On the whole, odds are that the current property market breakdown is structural, not cyclical. Financial markets – the prices of stocks and USD bonds of property developers – convey a similar message and continue to plunge (Chart 11). Chart 10Excessive Property Inventories

Excessive Property Inventories

Excessive Property Inventories

Chart 11No Green Light From Property Stocks And Corporate Bond Prices

No Green Light From Property Stocks And Corporate Bond Prices

No Green Light From Property Stocks And Corporate Bond Prices

Chart 12There Has Been No Recovery In China Without A Revival in Real Estate

There Has Been No Recovery In China Without A Revival in Real Estate

There Has Been No Recovery In China Without A Revival in Real Estate

Without an improvement in the housing market, a meaningful business cycle recovery is unlikely in China. Chart 12 illustrates that all recoveries in the Chinese broader economy since 2009 occurred alongside a revival in property sales. The importance of the property market goes beyond its size. Rising property prices lift household and business confidence, boosting aggregate spending and investment. The sluggish housing market and falling house prices will impair consumer and business confidence. This, along with uncertainty related to the dynamic zero-COVID policy, will dent consumer spending and private investments. Finally, the upcoming contraction in Chinese exports will dampen national income growth. Taken together, the multiplier effect of stimulus in the upcoming months will be lower than it has been in previous periods of stimulus. There are two areas that will see meaningful improvement in the coming months: infrastructure spending and autos. BCA’s China Investment Strategy service discussed the outlook for auto sales in a recent report. Chart 13Green Shoots In China's Infrastructure Investment

Green Shoots In China's Infrastructure Investment

Green Shoots In China's Infrastructure Investment

On the infrastructure front, there has been mixed evidence of an improvement in activity. The top and middle panels of Chart 13 demonstrate that Komatsu machinery’s operational hours and the number of approved infrastructure projects might be bottoming. However, the installation of high-power electricity lines has fallen to a 15-year low (Chart 13, bottom panel). As we elaborated in last month’s report, the new financing/stimulus for infrastructure development will not result in new investments. Rather, it will by and large offset the drop in local government (LG) revenues from land sales this year. In short, there is little new stimulus for infrastructure beyond what was approved in the budget plan earlier this year. Bottom Line: The recovery in China will be U- rather than V-shaped, with risks tilted to the downside. Investment Recommendations Our bias is that the rebound in global risk assets could last for a few more weeks. The basis is that investor positioning in risk assets was very light when this rebound began. Plus, falling oil prices could reinforce the idea among investors that US inflation is no longer a problem. Looking beyond the next several weeks, the outlook for global and EM risk assets is dismal. Markets will realize that the Fed cannot halt its tightening with core inflation well above 4-5%. Hawkish Fed policy and contracting global trade will boost the US dollar and weigh on cyclical assets. We continue to recommend an underweight allocation to EM in global equity and credit portfolios. Consistently, we are also reluctant to chase EM currencies higher. EM local bonds offer value, as we have argued over the past couple of months, but for now we prefer to focus on yield curve flattening trades. We continue betting on yield curve flattening/inversion in Mexico and Colombia and are long Brazilian 10-year domestic bonds while hedging the currency risk. In addition, we recommend investors continue receiving 10-year swap rates in China and Malaysia. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

S&P 500 Chart 1Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 2Profitability

Profitability

Profitability

Chart 3Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 4Uses Of Cash

Uses Of Cash

Uses Of Cash

Cyclicals Vs Defensives Chart 5Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 6Profitability

Profitability

Profitability

Chart 7Valuation And Technicals

Valuation And Technicals

Valuation And Technicals

Chart 8Uses Of Cash

Uses Of Cash

Uses Of Cash

Growth Vs Value Chart 9Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 10Profitability

Profitability

Profitability

Chart 11Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 12Uses Of Cash

Uses Of Cash

Uses Of Cash

Small Vs Large Chart 13Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 14Profitability

Profitability

Profitability

Chart 15Valuations and Technicals

Valuations and Technicals

Valuations and Technicals

Chart 16Uses Of Cash

Uses Of Cash

Uses Of Cash

Table 1Performance

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Table 2Valuations And Forward Earnings Growth

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Recommended Allocation

Executive Summary The constructive economic view that has us at odds with the consensus rests on three premises: excess pandemic savings will allow consumption to grow at trend, despite inflation; inflation will soon peak, moving to around 4% by year end; and inflation expectations will remain well anchored, keeping the Fed from moving immediately to stifle the economy. Our consumption thesis remains intact. Real consumption has kept pace despite falling real incomes, thanks to a steady, modest drawdown of excess savings. Though our calls for an inflation peak have been consistently premature, recent data suggest that inflation pressures are abating. Gasoline prices have been falling for seven weeks; the fever has broken in ISM survey price measures; and the labor market, notwithstanding July's potent employment report, is becoming less tight. Longer-run inflation expectations have resisted becoming unmoored despite soaring measured inflation and a breakout does not appear to be imminent. A Mighty Savings Cushion

A Mighty Savings Cushion

A Mighty Savings Cushion

Bottom Line: We continue to expect the economy will be surprisingly resilient, allowing equities to rally further before the Fed squashes the expansion. We doubt the rally will persist very far into 2023, however, so we are reducing equities to equal weight over a twelve-month timeframe. Feature We will be holding our quarterly webcast next Monday, August 15th at 9:00 a.m. Eastern time in lieu of publishing a Weekly Report. Please join us with your questions to make it a fully interactive event. We will resume our regular publication schedule on the 22nd. Last week, an investor we were meeting for the first time asked us how anyone could have published on a weekly basis this year. “Things are so uncertain and they’re moving so fast, how do you keep up? What have you been writing about?” At long last, we felt seen. Feeding the weekly beast is not easy under the best of circumstances and investors know that this year has been far from ideal. Related Report US Investment StrategyThe High Bar For Getting Worse Once the warm glow of unexpected empathy receded, we replied that we’ve been doing our best to anticipate how the key macro issues will impact financial markets over our cyclical 3-to-12-month timeframe, paying particular attention to consumers, inflation and the Fed. The outlook for consumption has been our primary focus from a growth perspective; we’ve been trying to assess how representative the key drivers of inflation are and how persistent they’ll be; and we’ve continuously monitored longer-run inflation expectations to determine if inflation has gotten far enough into economic agents’ heads to become self-reinforcing and compel the Fed to dislodge it, no matter the near-term economic cost. We review what we see on all three fronts in today’s report, and how events are unfolding relative to our expectations. The direction remains especially uncertain, but our theses remain intact, and we are sticking with our constructive outlook on risk assets and the economy for the rest of the year. We are pulling in our horns on our twelve-month optimism, however, in line with the BCA house view and the dawning realization that twelve months of equity outperformance is overly ambitious. We continue to believe the recession will arrive too late for the gloomy consensus of investors judged by their quarterly performance, forcing them back into risk assets, but the rebound may not persist beyond the FOMC’s first 2023 meeting at the beginning of February. The Consumer’s Staying Power Since CARES Act transfer payments began driving a surge in personal savings, we have viewed them as dry powder to support consumption once households regained the freedom to spend as they see fit. When the payments stopped flowing and the pandemic continued to delay a return to normal, that view came under some fire. We are of the mind that households merely deferred much of the services demand they would otherwise have slaked in 2020 and 2021; others argue that consumption deferred is consumption destroyed, as households will be reluctant to spend windfall transfers that they’d mentally sorted as savings. While it will take a while for data to confirm either thesis, we are encouraged by what we’ve seen so far. The savings rate has declined considerably so far in 2022, supporting the view that households would be willing to reach into their savings to maintain trend consumption (Chart 1). It dipped to 5.2% in the second quarter from 5.6% in the first quarter, well below February 2020’s 8.3% pre-pandemic level and 2011 to 2019’s 7.4% quarterly mean (Chart 2). Based on the series’ stability over the previous nine years, 2020’s and 2021’s forced savings rates amounted to 11- and 6-sigma post-crisis events and this year’s approximately -2.5-sigma drawdown suggests the pendulum has further to swing in the direction of dissaving. We disagree with knee-jerk conclusions that spending in excess of income is unsustainable – it’s plenty sustainable for households who socked away a mountain of savings over the previous eight quarters while bars, restaurants, stadiums, concert venues and resorts were idled. Chart 1Right On Target

Right On Target

Right On Target

Chart 22020 And 2021 Savings Were Enormous

2020 And 2021 Savings Were Enormous

2020 And 2021 Savings Were Enormous

The estimates of excess savings that we’ve been calculating every month since the summer of 2020 peaked just above $2.3 trillion last August and remained around that level before embarking on a steady decline in the first half to reach our current estimate above $2 trillion (Chart 3, bottom panel). Quoting that figure has been nagging at us lately, however, as one of the two assumptions we used to calculate households’ no-pandemic savings baseline – annualized disposable income growth of 4% – took 2% annual inflation as given, a condition that no longer applies after a twelve-month stretch in which year-over-year CPI inflation has averaged 7.1%. Chart 3Nominal Excess Savings

Taking Stock

Taking Stock

To determine how much households' purchasing power has eroded, we deflated our monthly excess savings estimates to a level equating to 2% annualized inflation (Chart 4, top panel). The adjustment knocked $450 billion off our current estimate, trimming it to $1.6 trillion (Chart 4, bottom panel). Perhaps more importantly for the outlook, our adjustment doubled the year-to-date burn rate to $500 billion. We have always worked with the (deliberately conservative) assumption that households would spend half of their excess savings; if inflation doesn’t decelerate soon, their cushion may not last very far beyond the end of the year. Chart 4Adjusted Excess Savings

Taking Stock

Taking Stock

Bottom Line: Households have been willing to dip into savings to maintain trend consumption so far this year, in line with our hypothesis. We expect they will continue to do so, and the savings rate will remain around 5% or fall even lower, but inflation has eaten up some of their dry powder. Will Inflation Ever Peak? Shredding widely shared expectations that inflation would peak sometime in the first half, the year-over-year increase in headline CPI has kept climbing, all the way to 9% in June. July should finally provide some relief, as the average national retail gasoline price has fallen for seven consecutive weeks and ended July 13% below its June 30 level (Chart 5). Last week’s ISM manufacturing and services PMIs also suggested that inflation has begun to ease its grip somewhat, with the manufacturing input prices series plunging by nearly 20 points to its two-decade mean (Chart 6, top panel) and the services prices component cooling by 8 points, though it remains quite high (Chart 6, bottom panel). Chart 5Four Bucks A Gallon Is High, But Not Unfamiliar

Four Bucks A Gallon Is High, But Not Unfamiliar

Four Bucks A Gallon Is High, But Not Unfamiliar

Chart 6The Fever May Have Broken ...

The Fever May Have Broken ...

The Fever May Have Broken ...

Chart 7... Though The Job Market Is Still Quite Hot

... Though The Job Market Is Still Quite Hot

... Though The Job Market Is Still Quite Hot

The tight-as-a-drum labor market has been a fertile source of inflation worries, but there are signs that it is becoming less tight. Job openings remain 40% above their pre-COVID high but declined by 600,000 in June and are 10% off of March’s all-time peak (Chart 7). Elevated quits reveal that it's still easy to get a job, but the net share of small businesses in the NFIB survey planning to hire in the next three months is down 40% from its peak last summer (Chart 8). The July employment report challenged the under-the-radar indicators’ implication that the labor market is cooling, as net payroll expansion reaccelerated along with average hourly earnings growth (Chart 9). We are confident that net payroll growth will slow but compensation clearly has the cyclical wind at its back, and it is not certain that labor’s structural headwind will largely offset it, as per our thesis. Chart 8Hiring Intentions Are Back To More Normal Levels ...

Hiring Intentions Are Back To More Normal Levels ...

Hiring Intentions Are Back To More Normal Levels ...

Chart 9... But Wage Growth Remains Elevated

... But Wage Growth Remains Elevated

... But Wage Growth Remains Elevated

Inflation Expectations Longer-run inflation expectations are a critical piece of the puzzle because they are the pathway for rising inflation to become self-reinforcing. If they expect persistently higher inflation, workers will negotiate more fiercely for larger compensation increases to stay ahead of it; businesses will push more vigorously to pass on their increased costs to preserve profit margins; lenders and bond investors will demand higher interest rates to protect their real returns; and consumers will seek to buy more now to get the most from their dwindling purchasing power, exacerbating supply-demand imbalances and keeping the heat on near-term inflation readings. We are therefore closely watching inflation expectations. Market-based measures like TIPS break-evens and CPI swaps shed some light on investor and business expectations, while the monthly University of Michigan consumer sentiment survey offers insight into households’ views. Market-based measures remain well-anchored: intermediate-term expectations as implied by TIPS break-evens are just nosing above the top of the Fed’s preferred 2.3-2.5% range (Chart 10, middle panel) while long-term expectations remain below it, as they have for most of the year (Chart 10, bottom panel). Intermediate- and long-term expectations derived from CPI swaps remain 20 to 30 basis points higher but are in the same position relative to their year-to-date path (Chart 11, bottom two panels). Chart 10Market-Based Inflation Expectations ...

Market-Based Inflation Expectations ...

Market-Based Inflation Expectations ...

Chart 11... Are Not Problematic

... Are Not Problematic

... Are Not Problematic

Chart 12Just Say No (To Bottleneck Prices)

Just Say No (To Bottleneck Prices)

Just Say No (To Bottleneck Prices)

The Michigan survey doesn’t betray any pressing long-run concerns. The preliminary 3.3% June reading hinting at a breakout turned out to be a false alarm, as June’s final figure was 3.1% and July’s was 2.9%. Survey respondents continue to shun big-ticket purchases because they expect prices will fall from their current levels (Chart 12). 2-year TIPS and swaps price in an optimistic near-term outlook that is likely to be disappointed, as we think inflation will prove to be sticky around the 4% level, and that disappointment could bleed into higher longer-run expectations. While expectations are not problematic now, investors will need to watch them carefully going forward. Investment Implications It was policy, monetary and fiscal, that inspired our bullish turn in 2020 once we digested the COVID shock. We thought the macro backdrop would come down to policymakers versus the virus and our money was on the former. We remained bullish across 2021 on the idea that monetary and fiscal support would remain in place well after they ceased to be necessary. Mindful that there is no such thing as a free lunch, we expected that the emergency pandemic measures would ultimately have the effect of overstimulating demand, but we entered 2022 thinking that equities and credit would enjoy one more year of sizable excess returns over Treasuries and cash before the overstimulation manifested itself. Overweighting (underweighting) equities in a multi-asset portfolio is our default position when monetary policy is easy (tight), though we will override that default when appropriate. We have no appetite for overriding it once it becomes clear that market expectations for 2023 rate cuts are going to be disappointed and tight policy is just around the bend. Given our view that inflation will linger around 4% after easing smartly over the rest of this year, we expect that the Fed will impose restrictive monetary policy settings by the second half of 2023 in its quest to drive inflation back down to its 2% target. Markets’ overly rosy Fed expectations look sure to be disappointed and they could face a reckoning after the FOMC’s January 31-February 1 meeting. Chart 13Consolidation Now, 10%+ By The End Of The Year

Consolidation Now, 10%+ By The End Of The Year

Consolidation Now, 10%+ By The End Of The Year

That meeting could herald an inflection for risk assets’ relative performance and we are therefore joining our colleagues in adopting a neutral 12-month view on equities. We continue to differ from the BCA consensus, however, in expecting a meaningful equity rally before year end. While we expect technical resistance at 4,200 will restrain the S&P 500 in the immediate term (Chart 13), we think it will find its way back into the mid-to-high 4,000s before the Fed signals that it will take the funds rate to 4% or above, dashing hopes for a February peak around 3.5%. We still want to overweight equities in multi-asset portfolios, but only until year-end or 4,500 to 4,600, whichever comes first. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

Executive Summary The US economy is experiencing a period of stagflation: booming nominal economic growth amid a lack of volume expansion. Very strong nominal growth (due to high inflation), a tight labor market, and more evidence of a wage-price spiral will cause the Fed to err on the side of hawkishness. Global trade volumes will contract and commodity prices will drop further. The former is bearish for Emerging Asian financial markets and the latter is negative for Latin American markets. Equities are currently rallying from very oversold levels and the rebound could continue in the coming weeks. However, if we are correct about our outlook on US inflation, Fed policy and global trade, then risk assets will resume their decline and the US dollar will rally. Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

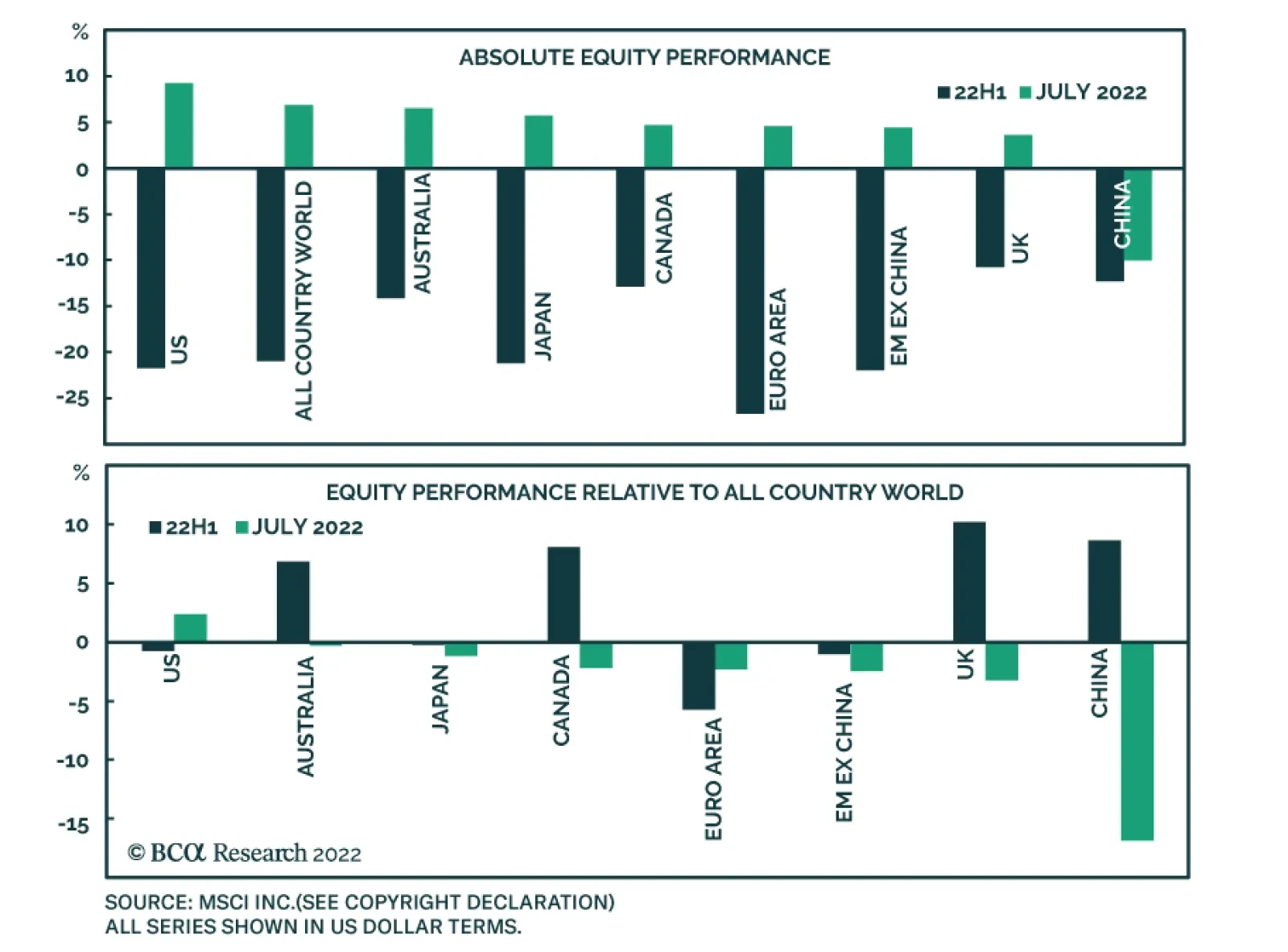

Bottom Line: Stay defensive and continue underweighting EM in global equity and credit portfolios. The greenback will resume its uptrend sooner rather than later. This will depress EM share prices and fixed-income markets. Financial markets interpreted Fed chairman Powell’s comments in last Wednesday’s (July 27) FOMC press conference as a dovish pivot, catalyzing a sharp rebound in the S&P500. Is the bear market over? Should investors buy risk assets, including EM ones? Chart 1No Strong Rebound In EM Share Prices

No Strong Rebound In EM Share Prices

No Strong Rebound In EM Share Prices

We are hesitant to declare an end to the bear market and to recommend higher exposure to EM risk assets and currencies. In fact, the rebound in EM stocks has been feeble (Chart 1, top panel). As a result, the relative performance of EM equities versus their DM peers has fallen back to its lows of earlier this year (Chart 1, bottom panel). Overall, we reiterate what we wrote two weeks ago “…our macro themes of Fed tightening amid slowing global growth, the US dollar overshooting, and China’s disappointing recovery remain intact. These factors still warrant a defensive investment strategy, despite a possible near-term rebound in the S&P 500. EMs will lag and underperform in this rebound.” Can The Fed Afford To Pivot? With entrenched and persistent inflation in the US running well above the Fed’s target, the Fed cannot afford to – and will not – pivot for now. A simple rollover in inflation that reflects falling commodity and goods prices will not be sufficient for the Fed to make a policy U-turn and cut rates by 50 basis points next year (as fixed-income markets expect). We have been arguing that the US is already experiencing broad-based genuine inflation and has developed a wage-price spiral. Chart 2US Wage Growth Is At Its Fastest Rate In 40 years

US Wage Growth Is At Its Fastest Rate In 40 years

US Wage Growth Is At Its Fastest Rate In 40 years

US wage growth has surged to a 40-year high of 5.7% (Chart 2). Even though the labor market is set to soften on the margin, its tightness will keep wage growth elevated. Importantly, real wages have fallen significantly, and employees will be demanding higher wages to offset lost purchasing power. US companies have been raising their prices at the fastest rate in decades. Prices charged by non-farm businesses rose at an annual rate of 8-9% in Q2, the highest in the past 40 years (Chart 3). Chart 3US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

Chart 4Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Even though volumes have stagnated, corporate profits have been holding up because companies have been able to raise prices. Final sales to domestic purchasers in real terms registered zero growth in Q2 from Q1(Chart 4). This entails that the US economy is currency experiencing stagflation. Given that companies are able to raise prices (generating strong nominal sales) and are facing very tight labor market conditions, they might be willing to raise wages further. In brief, a wage-price spiral is unfolding in the US. US core inflation is running well above the Fed’s 2% target. The average of seven core PCE and CPI measures – our “super core” gauge of consumer price inflation − stands at 5.5% (Chart 5). Although falling commodity and goods prices (Chart 6) could cap the upside in core inflation, they are unlikely to bring it down below 4%. Hence, core inflation will remain well above the Fed’s target of 2%. This will lead the Fed to keep tightening monetary policy. Chart 5US Super Core Inflation Is At 5.5% and Rising

US Super Core Inflation Is At 5.5% and Rising

US Super Core Inflation Is At 5.5% and Rising

Chart 6US Import Prices From Asia Will Fall

US Import Prices From Asia Will Fall

US Import Prices From Asia Will Fall

Finally, in our opinion, financial markets are underappreciating how entrenched and persistent US inflation has become and are overlooking the unfolding wage-price spiral. The latest easing in US financial conditions will cause the Fed to refocus on inflation rather than growth. That is why we maintain our theme that the Fed and US equity markets remain on a collision course. We are open to the idea that the Fed could ultimately pivot earlier than required and eventually cut rates. However, odds are that the Fed has not yet pivoted and will ramp up its hawkishness in the coming months. The bar for the Fed to turn dovish is currently much higher than at any other time in the past 35 years, as inflation is much more entrenched and higher today. In our view, Powell would not like to be remembered as the chairman under whose watch inflation became enduring. He would prefer to be remembered as Paul Volcker, and not as Arthur Burns. Under the latter’s watch in the 1970s, the US experienced a devastating era of high and persistent inflation. Global equities, credit markets and US Treasurys were very oversold a few weeks ago. That is why even a minor hint from the Fed of a possible end to the hiking cycle produced such a strong rebound in stocks and fixed-income markets. This rally could persist in the coming weeks. However, if we are correct about the outlook on US inflation, Fed policy and global trade (see the section below), then risk assets will resume their decline and the US dollar will rally. Bottom Line: The US economy is experiencing a period of stagflation: booming nominal economic growth amid a lack of volume expansion. Very strong nominal growth (due to high inflation) a tight labor market, and more evidence of a wage-price spiral will cause the Fed to err on the side of hawkishness. As a result, the current rally in risk assets is unsustainable. Global Manufacturing / Trade Contraction Global manufacturing and trade are entering a period of contraction: According to manufacturing PMI data for July, Taiwanese new export orders for overall manufacturing and the semiconductor industry have plunged to 37 and 34, respectively (Chart 7). Meanwhile, their customer inventories have surged to a 10-year high (Chart 8). Taiwan is a major supplier of semiconductors and other inputs to many industries around the world. Hence, these data suggest that industrial companies globally have stopped ordering chips and other inputs. This development is a sign of broad-based industrial weakness. Therefore, we believe that global trade volumes are set to shrink in H2 this year. Chart 7Taiwan: Overall And Semiconductor New Orders Have Plunged...

Taiwan: Overall And Semiconductor New Orders Have Plunged...

Taiwan: Overall And Semiconductor New Orders Have Plunged...

Chart 8...And Customer Inventories Have Surged

...And Customer Inventories Have Surged

...And Customer Inventories Have Surged

A similar situation is unfolding in the Korean semiconductor sector. The DRAM DXI index (revenue proxy) is falling, and DRAM and NAND spot prices are deflating (Chart 9). Notably, Korea’s overall export sector is also reeling. Business confidence among Korean exporters is plunging – this includes the latest datapoint from August (Chart 10, top panel). The nation’s export volume growth is already close to zero and export value growth is only holding up because of higher prices (Chart 10, bottom panel). Chart 9Korea: Semiconductor Prices Are Deflating

Korea: Semiconductor Prices Are Deflating

Korea: Semiconductor Prices Are Deflating

Chart 10Downside Risks For Korean Exports

Downside Risks For Korean Exports

Downside Risks For Korean Exports

Chart 11US Goods Imports Are Set To Contract

US Goods Imports Are Set To Contract

US Goods Imports Are Set To Contract

US import volumes are set to shrink in the coming months. This will deepen the global trade slump. Chart 11 illustrates that US consumption of goods-ex autos has been contracting and retail inventory of goods ex-autos has skyrocketed. Together, these developments foreshadow a major contraction in US imports and global trade volumes. Commodity prices are heading south. Chinese commodity consumption will remain in the doldrums, and US/EU demand for commodities will weaken as global manufacturing contracts. The sanctions imposed on Russia initially led buyers to increase their precautionary and speculative purchases of various commodities, creating a tailwind for prices earlier this year. However, these precautionary and speculative purchases have since been halted or reversed, causing commodity prices to plunge. We made the case for falling oil prices in our July 21 report, and BCA’s China Investment Strategy’s Special Report on copper from July 27 concludes that copper prices will decline further. Chart 12China: Has The Post-Reopening Bounce Ran Its Course?

China: Has The Post-Reopening Bounce Ran Its Course?

China: Has The Post-Reopening Bounce Ran Its Course?

Finally, the Chinese manufacturing PMI rolled over in July following the rebound in May and June. New orders, backlog orders and import subcomponents have relapsed anew (Chart 12). The Chinese economy is facing considerable headwinds from the property market, rolling lockdowns resulting from the dynamic zero-COVID policy and a contraction in exports. As we argued in our July 13 report, policy stimulus has so far been insufficient. Bottom Line: Global trade volumes will contract and commodity prices will drop further. The former is bearish for Emerging Asian financial markets and the latter is negative for Latin American markets. Investment Strategy Although the rebound in global risk assets could persist for several weeks, their risk-reward profile is not attractive. Stay defensive and continue underweighting EM in global equity and credit portfolios. The Fed’s hawkish bias as well as contracting global trade are bullish for the US dollar. As a result, the greenback will resume its uptrend sooner rather than later. This will cap the upside in EM stocks and fixed-income markets. We continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP, and IDR. In addition, we recommend shorting HUF vs. CZK, KRW vs. JPY, and BRL vs. MXN. Although we find good value in many EM local yields, we do not yet recommend buying them aggressively. The basis is our view on EM currencies versus the US dollar. For now, we prefer to bet on flattening yield curves. Our current favorite markets for flatteners are Mexico and Colombia. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Counterpoint’s August schedule: Next week, I am travelling to see clients in Australia, New Zealand, and Singapore, so we will send you a report on China’s 20th National Party Congress written by our Chief Geopolitical Strategist, Matt Gertken. Given that the outlook for the $100 trillion Chinese real estate market is crucial for the global economy and markets, Matt’s insights will be very interesting. Then on August 18, I will host the monthly Counterpoint webcast, which I hope you can join. We will then take a week’s summer holiday and return with a report on September 1. Executive Summary In the topsy-turvy recession of 2022, real wages have collapsed. This means profits have stayed resilient and firms have not laid off workers. Making this recession a ‘cost of living crisis’ rather than a ‘jobs crisis’. If inflation comes down slowly, then the ‘cost of living crisis’ will persist. But if inflation comes down quickly while wage inflation remains sticky, firms will lay off workers to protect their profits, turning the ‘cost of living crisis’ into a ‘jobs crisis’. Either way, this will keep a choke on consumer spending, and particularly the spending on goods, which is likely to remain in recession. Meanwhile, until mortgage rates move meaningfully lower, housing investment will also remain in recession. The double choke on growth means that the bear market in the 30-year T-bond is likely over. This suggests that the bear market in stock market valuations is also over, but that ‘cyclical value’ is now vulnerable to profit downgrades. Hence, equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Fractal trading watchlist: GBP/USD and Hungarian versus Polish bonds. In The 2008 Recession, Real Wage Rates ##br##Went Up So Employment Went Down…

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

…But In The 2022 Recession, Real Wage Rates##br##Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

Bottom Line: The bear market in the 30-year T-bond and stock market valuations is likely over, but equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Feature The US economy has just contracted for two consecutive quarters, meeting the rule-of-thumb definition of a recession. Other major economies are likely to follow. Yet many economists and strategists are in denial. This cannot be a ‘proper’ recession, they say, because the economy remains at full employment. But the recession-deniers are wrong. It is a recession, albeit it is a ‘topsy-turvy’ recession in which employment remains high (so far) because real wage rates have collapsed, circumventing the need for lay-offs. This contrasts with a typical recession when real wage rates remain high, forcing the need for lay-offs.1 The Topsy-Turvy Recession Of 2022 When do firms lay off workers? The answer is, when they need to protect their profits. Profits are nothing more than revenues minus costs, and in a typical recession revenues slow much faster than the firms’ biggest cost, the wage bill. In this event, the only way that firms can protect their profits is to lay off workers. Chart I-1 confirms that every time that nominal sales have shrunk relative to wage rates, the unemployment rate has gone up. Without exception. Chart I-1Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

But what happens during a recession in which nominal sales do not shrink relative to wage rates? In this event, profits stay resilient, so firms do not need to lay off workers. Welcome to the topsy-turvy recession of 2022! In the topsy-turvy recession of 2022, there has been much greater inflation in consumer prices and nominal sales than in nominal wage rates (Chart I-2). The result is that real wage rates have collapsed, profits have stayed resilient, and firms have not needed to lay off workers… so far. Chart I-2...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

In a typical recession, the pain falls on the minority of workers who lose their jobs, as well as on profits. Paradoxically, for the majority that keep their jobs, real wages go up. This is because sticky wage inflation tends to hold up more than collapsing price inflation. For example, in the 2008 recession, the real wage rate surged by 4 percent (Chart I-3), and in the 2020 recession it rose by 2 percent. Chart I-3In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

Yet in the 2022 recession, the real wage rate has shrunk by 4 percent, meaning that the pain of the recession has fallen on all of us (Chart I-4). In one sense therefore, this recession is ‘fairer’ because ‘we’re all in it together’. This is confirmed by the current malaise being characterised not as a ‘jobs crisis’, but as a ‘cost of living crisis’. In another sense though, the recession is unfair because the pain has not been shared by corporate profits, which have remained resilient… so far. Chart I-4...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

The crucial question is, what happens next? Using the US as our template, wage rates are growing at 5-6 percent, and this growth rate is typically stickier than sales growth. Assuming inflation drifts lower, nominal sales growth will also drift lower from its current 7 percent clip, meaning that it could soon dip below sticky wage growth. Once the growth in firms’ revenues has dipped below that in nominal wage rates, profits will finally keel over. To repeat, profits are nothing more than revenues minus costs, where the biggest cost is the wage bill (Chart I-5).2 Chart I-5Profits Are Nothing More Than Revenues Minus Costs

Profits Are Nothing More Than Revenues Minus Costs

Profits Are Nothing More Than Revenues Minus Costs

At this point, the downturn will become more conventional. To protect profits, firms will be forced to lay off workers who will bear the pain of the downturn alongside falling profits. Meanwhile, with inflation easing, real wage growth for the majority that keep their jobs will turn positive. But to repeat, this is the typical pattern in a recession. Accelerating real wage rates are entirely consistent with a contracting economy as we witnessed in both 2008 and 2020. As Two Huge Imbalances Correct, Demand Will Be Pegged Back All of this assumes that real demand will remain under pressure, so the question is what is pegging back real demand? The answer is: corrections in two huge imbalances in the global economy. A breakdown of the -1.3 percent contraction in the US economy reveals these two corrections:3 Spending on goods, which contributed -1.2 percent Housing investment, which contributed -0.7 percent. These corrections are not over. As we presciently explained back in February in A Massive Economic Imbalance, Staring Us In The Face: “The pandemic overspend on goods constitutes one of the greatest imbalances in economic history. An overspend on goods is corrected by a subsequent underspend; but an underspend on services is not corrected by a subsequent overspend. The pandemic overspend on goods constitutes one of the greatest imbalances in economic history. This unfortunate asymmetry means that the recent overspend on goods at the expense of services makes the economy vulnerable to a recession. And the risk is exacerbated by central banks’ intentions to hike rates in response to inflation” (Chart I-6). Chart I-6The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

Then, in The Global Housing Boom Is Over, As Buying Becomes More Expensive Than Renting, we identified a second major imbalance that is starting to correct. Specifically, the global housing boom of the past decade, which has doubled the worth of global real estate to $370 trillion, was predicated on ultra-low mortgage rates that made buying a home more attractive than renting. But in many parts of the world now, buying a home has become more expensive than renting (Chart I-7). Disappearing US and European homebuyers combined with a flood of home-sellers will weigh on home prices and housing investment – at least until policymakers are forced to bring down mortgage rates (Chart I-8 and Chart I-9). Chart I-7Buying A Home Has Become More Expensive Than Renting!

Buying A Home Has Become More Expensive Than Renting!

Buying A Home Has Become More Expensive Than Renting!

Chart I-8Homebuyers Have Disappeared...

Homebuyers Have Disappeared...

Homebuyers Have Disappeared...

Chart I-9...While Home-Sellers Are Flooding The Market

...While Home-Sellers Are Flooding The Market

...While Home-Sellers Are Flooding The Market

Meanwhile, as Chinese policymakers try and gently let the air out of the $100 trillion Chinese real estate market, a collapse in Chinese property development and construction activity will have negative long-term implications for commodities, emerging Asia, and developing countries that produce raw materials. More Investment Conclusions In addition to the long-term investment conclusions just described, we can draw some shorter-term conclusions: If inflation comes down slowly, then the current ‘cost of living crisis’, which is pummelling everyone’s real incomes, will persist. But if inflation comes down quickly while wage inflation remains sticky, firms will be forced to lay off workers to protect their profits, turning the ‘cost of living crisis’ into a ‘jobs crisis’. Either way, this will keep a choke on consumer spending, and particularly the spending on goods, which is likely to remain in recession. Meanwhile, until mortgage rates move meaningfully lower, housing investment will also remain in recession. Equityinvestors should stick with ‘defensive growth’, specifically healthcare and biotech. This double choke on growth is likely to keep a lid on ultra-long bond yields, even if central banks need to hike short-term rates more than expected to slay inflation. Our proprietary fractal analysis confirms that the sell-off in the 30-year T-bond is likely over (Chart I-10). Chart I-10The Bear Market In The 30-Year T-Bond Is Likely Over

The Bear Market In The 30-Year T-Bond Is Likely Over

The Bear Market In The 30-Year T-Bond Is Likely Over

For the stock market, this suggests that the valuation bear market is now over, but that ‘cyclical value’ sectors are now vulnerable to profit downgrades. Hence, equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Fractal Trading Watchlist This week we noticed that the sudden 20 percent collapse of Hungarian versus Polish 10-year bonds, has reached the point of short-term fractal fragility that suggests an imminent rebound. Hence, we are adding this to our watchlist. Go long GBP/USD. But our trade is GBP/USD. UK political risk is diminishing, the BoE is likely to be as, or more, hawkish than the Fed, and the 260-day fractal structure of GBP/USD is at the point of fragility that has signalled major turning points in 2014, 15, 16, 18 and 21 (Chart I-11). Accordingly the recommendation is long GBP/USD, setting the profit target and symmetrical stop-loss at 5 percent. Chart I-11Go Long GBP/USD

Go Long GBP/USD Go Long GBP/USD

Go Long GBP/USD Go Long GBP/USD

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Chart 1CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

Chart 2Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Chart 3Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Chart 4US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 5CAD/SEK Is Reversing

CAD/SEK Is Reversing

CAD/SEK Is Reversing

Chart 6Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Chart 7The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

Chart 8The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

Chart 9FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

Chart 10Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Chart 11The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

Chart 12The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 13Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Chart 14German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

Chart 15Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Chart 16ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

Chart 17The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

Chart 18The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

Chart 19A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 20Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 21Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Chart 22Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Chart 23Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Chart 24USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

Chart 25The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

Chart 26A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 27US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

Chart 28The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The best measure of wage rates is the employment cost index (ECI) because it includes all forms of compensation including benefits and bonuses. 2 In fact, stock market profits are even more cyclical because, as well as wages, there are other sticky deductions from revenues such as interest and taxes. 3 All expressed as annualised rates. Fractal Trading System Fractal Trades

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

6-12 Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Executive Summary Biden Taps China-Bashing Consensus

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

House Speaker Nancy Pelosi’s visit to Taiwan reflects one of our emerging views in 2022: the Biden administration’s willingness to take foreign policy risks ahead of the midterm elections. Biden’s foreign policy will continue to be reactive and focused on domestic politics through the midterms. Hence global policy uncertainty and geopolitical risk will remain elevated at least until November 8. Biden is seeing progress on his legislative agenda. Congress is passing a bill to compete with China while the Democrats are increasingly likely to pass a second reconciliation bill, both as predicted. These developments support our view that President Biden’s approval rating will stabilize and election races will tighten, keeping domestic US policy uncertainty elevated through November. These trends pose a risk to our view that Republicans will take the Senate, but the prevailing macroeconomic and geopolitical environment is still negative for the ruling Democratic Party. We expect legislative gridlock and frozen US fiscal policy in 2023-24. Close Recommendation (Tactical) Initiation Date Return Long Refinitiv Renewables Vs. S&P 500 Mar 30, 2022 25.4% Long Biotech Vs. Pharmaceuticals Jul 8, 2022 -3.3% Bottom Line: While US and global uncertainty remain high, we will stay long US dollar, long large caps over small caps, and long US Treasuries versus TIPS. But these are tactical trades and are watching closely to see if macroeconomic and geopolitical factors improve later this year. Feature President Biden’s average monthly job approval rating hit its lowest point, 38.5%, in July 2022. However, Biden’s anti-inflation campaign and midterm election tactics are starting to bear fruit: gasoline prices have fallen from a peak of $5 per gallon to $4.2 today, the Democratic Congress is securing some last-minute legislative wins, and women voters are mobilizing to preserve abortion access. These developments mean that the Democratic Party’s electoral prospects will improve marginally between now and the midterm election, causing Senate and congressional races to tighten – as we have expected. US policy uncertainty will increase. Investors will see a rising risk that Democrats will keep control of the Senate – and conceivably even the House – and hence retain unified control of the executive and legislative branches. This “Blue Sweep” risk will challenge the market consensus, which overwhelmingly (and still correctly) expects congressional gridlock in 2023-24. A continued blue sweep would mean larger tax hikes and social spending, while gridlock would neutralize fiscal policy for the next two years. Investors should fade this inflationary blue sweep risk and continue to plan for disinflationary gridlock. First, our quantitative election models still predict that Democrats will lose control of both House and Senate (Appendix). Second, Biden’s midterm tactics face very significant limitations, particularly emanating from geopolitics – the snake in this report’s title. Pelosi’s Trip To Taiwan Raises Near-Term Market Risks One of Biden’s election tactics is our third key view for 2022: reactive foreign policy. Initially we viewed this reactiveness as “risk-averse” but in May we began to argue that Biden could take risky bets given his collapsing approval ratings. Either way, Biden is using foreign policy as a means of improving his party’s domestic political fortunes. In particular, he is willing to take big risks with China, Russia, Iran, and terrorist groups like Al Qaeda. The template is the 1962 congressional election, when President John F. Kennedy largely defied the midterm election curse by taking a tough stance against Russia in the Cuban Missile Crisis (Chart 1). If Biden achieves a foreign policy victory, then Democrats will benefit. If he instigates a crisis, voters will rally around his administration out of patriotism. Nancy Pelosi’s visit to Taipei is the prominent example of this key view. The trip required full support from the US executive branch and military and was not only the swan song of a single politician. It was one element of the Biden administration’s decision to maintain the Trump administration’s hawkish China policy. Thus while Congress passes the $52 billion Chips and Science Act to enhance US competitiveness in technology and semiconductor manufacturing, Biden is also contemplating tightening export controls on computer chip equipment that China needs to upgrade its industry.1 Biden is reacting to a bipartisan and popular consensus holding that the US needs to take concrete measures to challenge China and protect American industry (Chart 2). This is different from the old norm of rhetorical China-bashing during midterms. Chart 1Biden Provokes Foreign Rivals

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Chart 2Biden Taps China-Bashing Consensus

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Reactive US foreign policy will continue through November and possibly beyond – including but not limited to China. The US chose to sell long-range weapons to Ukraine and provide intelligence targeting Russian forces, prompting Russia to declare that the US is now “directly” involved in the Ukraine conflict. The US decision to eradicate Al Qaeda leader Ayman Al-Zawahiri also reflects this foreign policy trend. Reactive foreign policy will increase the near-term risk of new negative geopolitical surprises for markets. Note that the 1962 Cuban Missile Crisis analogy is inverted when it comes to the Taiwan Strait. China is willing to take much greater risks than the US in its sphere of influence. The same goes for Russia in Ukraine. If US policy backfires then it may assist the Democrats in the election – but not if Biden suffers a humiliation or if the US economy suffers as a result. Chart 3US Import Prices Will Stay High From Greater China

US Import Prices Will Stay High From Greater China

US Import Prices Will Stay High From Greater China

US import prices will continue to rise from Greater China (Chart 3), undermining Biden’s anti-inflation agenda. Supply kinks in the semiconductor industry will become relevant again whenever demand rebounds (Chart 4). Global energy prices will also remain high as a result of the EU’s oil embargo and Russia’s continued tightening of European natural gas supplies. Chart 4New Semiconductor Kinks Will Appear When Demand Recovers

New Semiconductor Kinks Will Appear When Demand Recovers

New Semiconductor Kinks Will Appear When Demand Recovers

OPEC has decided only to increase oil production by 100,000 barrels per day, despite Biden’s visit to Saudi Arabia cap in hand. We argued that the Saudis would give a token but would largely focus on weakening global demand rather than pumping substantially more oil to help Biden and the Democrats in the election. The Saudis know that Biden is still attempting to negotiate a nuclear deal with Iran that would free up Iranian exports. So the Saudis are not giving much relief, and if Biden fails on Iran, oil supply disruptions will increase. Bottom Line: Price pressures will intensify as a result of the US-China and US-Russia standoffs – and probably also the US-Iran standoff. Hawkish foreign policy is not conducive to reducing inflationary ills. Global policy uncertainty and geopolitical risk will remain high throughout the midterm election season, causing continued volatility for US equities. Abortion Boosts Democratic Election Odds Earlier this year we highlighted that the Supreme Court’s overturning of the 1972 Roe v. Wade decision would lead to a significant mobilization of women voters in favor of the Democratic Party ahead of the midterm election. The first major electoral test since the court’s ruling, a popular referendum in the state of Kansas, produced a surprising result on August 2 that confirms and strengthens this thesis. Kansas is a deeply religious and conservative state where President Trump defeated President Biden by a 15% margin in 2020. The referendum was held during the primary election season, when electoral turnout skews heavily toward conservatives and the elderly. Yet Kansans voted by an 18% margin (59% versus 41%) not to amend the constitution, i.e. not to empower the legislature to tighten regulations on abortion. Voter turnout is not yet reported but likely far higher than in recent non-presidential primary elections. Kansans voted in the direction of nationwide opinion polling on whether abortion should be accessible in cases where the mother’s health is endangered. They did not vote in accordance with more expansive defenses of abortion, which are less popular (Chart 5). If the red state of Kansas votes this way then other states will see an even more substantial effect, at least when abortion is on the ballot. Chart 5Abortion Will Mitigate Democrats’ Losses

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

The question is how much of this Roe v. Wade effect will carry over to the general congressional elections. The referendum focused exclusively on abortion. Voters did not vote on party lines. Voters never like it when governments try to take away rights or privileges that have previously been granted. But in November the election will center on other topics, including inflation and the economy. And midterm elections almost always penalize the incumbent party. Our quantitative election models imply that Democrats will lose 22 seats in the House and two seats in the Senate, yielding Congress to the Republicans next year (Appendix). Still, women’s turnout presents a risk to our models. Women’s support for the Democratic Party has not improved markedly since the Supreme Court ruling, as we have shown in recent reports (Chart 6). But the polling could pick up again. Women’s turnout could be a significant tailwind in a year of headwinds for the Democrats. Bottom Line: Democrats’ electoral prospects have improved, as we anticipated earlier this year (Chart 7). This trend will continue as a result of the mobilization of women. Republicans are still highly likely to take Congress but our conviction on the Senate is much lower than it is on the House. Chart 6Biden’s And Democrats’ Approval Among Women

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Chart 7Democrats’ Odds Will Improve On Margin

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Reconciliation Bill: Still 65% Chance Of Passing Ultimately Democrats’ electoral performance will depend on inflation, the economy, and cyclical dynamics. If inflation falls over the course of the next three months, then Democrats will have a much better chance of stemming midterm losses. That is why President Biden rebranded his slimmed down “Build Back Better” reconciliation bill as the “Inflation Reduction Act.” We maintain our 65% odds that the bill will pass, as we have done all year. There is still at least a 35% chance that Senator Kyrsten Sinema of Arizona could defect from the Democrats, given that she opposed any new tax hikes and the reconciliation bill will impose a 15% minimum tax on corporations. A single absence or defection would topple the budget reconciliation process, which enables Democrats to pass the bill on a simple majority vote. We have always argued that Sinema would ultimately fall in line rather than betraying her party at the last minute before the election. This is even more likely given that moderate-in-chief, Senator Joe Manchin of West Virginia, negotiated and now champions the bill. But some other surprise could still erase the Democrats’ single-seat majority, so we stick with 65% odds. Most notably the bill will succeed because it actually reduces the budget deficit – by an estimated $300 billion over a decade (Table 1). Deficit reduction was the original purpose of lowering the number of votes required to pass a bill under the budget reconciliation process. Now Democrats are using savings generated from new government caps on pharmaceuticals (a popular measure) to fund health and climate subsidies. Given deficit reduction, it is conceivable that a moderate Republican could even vote for the bill. Table 1Democrats’ Inflation Reduction Act (Budget Reconciliation)

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Bottom Line: Democrats are more likely than ever to pass their fiscal 2022 reconciliation bill by the September 30 deadline. The bill will cap some drug prices and reduce the deficit marginally, so it can be packaged as an anti-inflation bill, giving Democrats a legislative win ahead of the midterm. However, its anti-inflationary impact will ultimately be negligible as $300 billion in savings hardly effects the long-term rising trajectory of US budget deficits relative to output. The bill will add to voters’ discretionary income and spur the renewable energy industry. And if it helps the Democrats retain power, then it enables further spending and tax hikes down the road, which would prove inflationary. The reconciliation bill, annual appropriations, and the China competition bill were the remaining bills that we argued would narrowly pass before the US Congress became gridlocked again. So far this view is on track. Investment Takeaways Companies that paid a high effective corporate tax rate before President Trump’s tax cuts have benefited relative to those that paid a low effective rate. They stood to suffer most if Trump’s tax cuts were repealed. But Democrats were forced to discard their attempt to raise the overall corporate tax rate last year. Instead the minimum corporate rate will rise to 15%, hitting those that paid the lowest effective rate, such as Big Tech companies, relative to high-tax rate sectors such as energy (Chart 8, top panel). Tactically energy may still underperform tech but cyclically energy could outperform and the reconciliation bill would feed into that trend. Similarly, companies that faced high foreign tax risk, because they made good income abroad but paid low foreign tax rates, stand to suffer most from the imposition of a minimum corporate tax rate (Chart 8, bottom panel). Again, Big Tech stands to suffer, although it has already priced a lot of bad news and may not perform poorly in the near term. Chart 8Market Responds To Minimum Corporate Tax

Market Responds To Minimum Corporate Tax

Market Responds To Minimum Corporate Tax

Chart 9Market Responds To New Climate Subsidies

Market Responds To New Climate Subsidies

Market Responds To New Climate Subsidies

Renewable energy stocks have rallied sharply on the news of the Democrats’ reconciliation bill getting back on track (Chart 9). We are booking a 25.4% gain on this tactical trade and will move to the sidelines for now, although renewable energy remains a secular investment theme. Health stocks, particularly pharmaceuticals, have taken a hit from the new legislation as we expected. However, biotech has not outperformed pharmaceuticals as we expected, so we will close this tactical trade for a loss of 3.3%. The reconciliation bill will cap drug prices for only the most popular generic drugs and does not pose as much of a threat to biotech companies (Chart 10). Biotech should perform well tactically as long bond yields decline – they are also historically undervalued, as noted by Dhaval Joshi of our Counterpoint strategy service. So we will stick to long Biotech versus the broad market. US semiconductors remain in a long bull market and will be in heavy demand once global and US economic activity stabilize. They are also likely to outperform competitors in Greater China that face a high and persistent geopolitical risk premium (Chart 11). Chart 10Market Responds To Drug Price Caps

Market Responds To Drug Price Caps

Market Responds To Drug Price Caps

Chart 11Market Responds To China Competition Bill

Market Responds To China Competition Bill

Market Responds To China Competition Bill