Equities

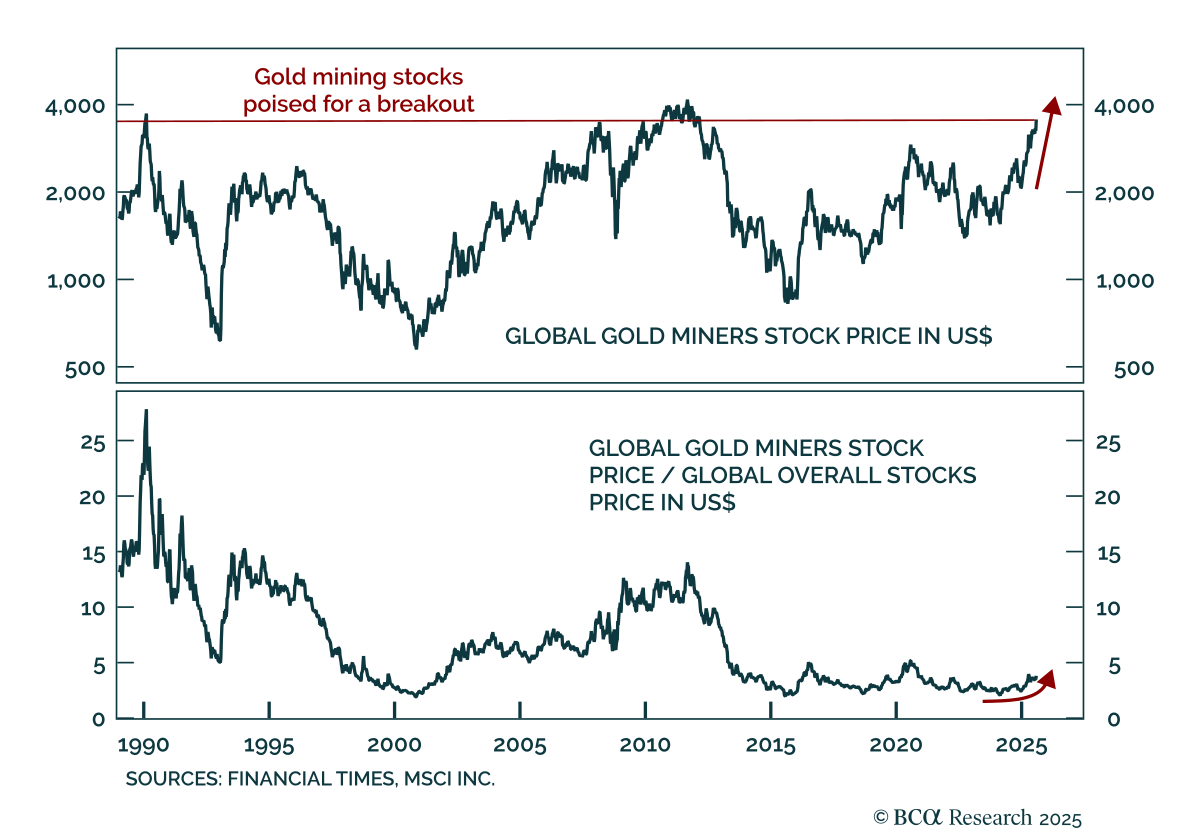

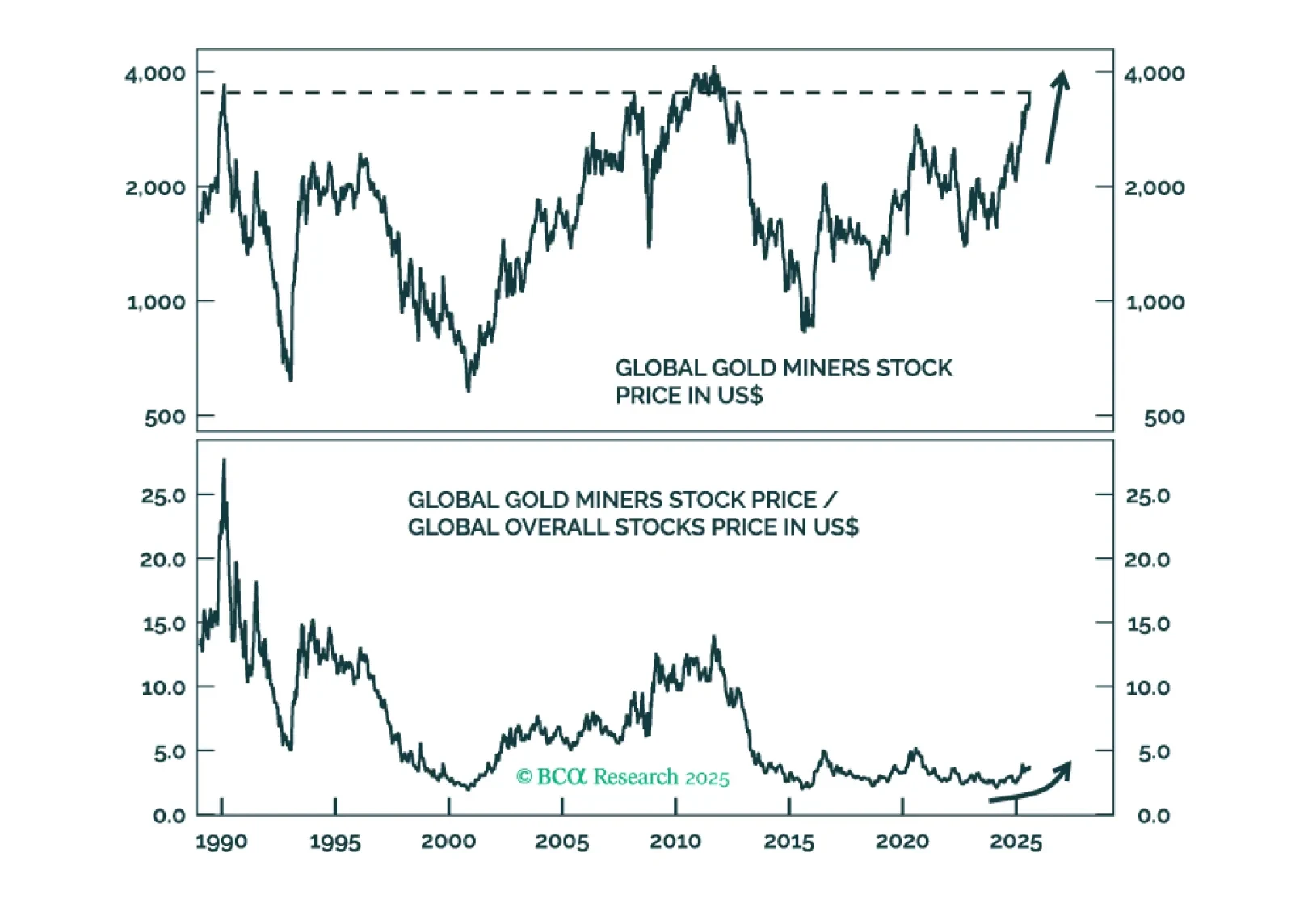

The fact that the yellow metal’s rally has defied headwinds from key cyclical drivers suggests that the bull market is structural, not cyclical. Buy gold and gold mining stocks in absolute and relative terms.

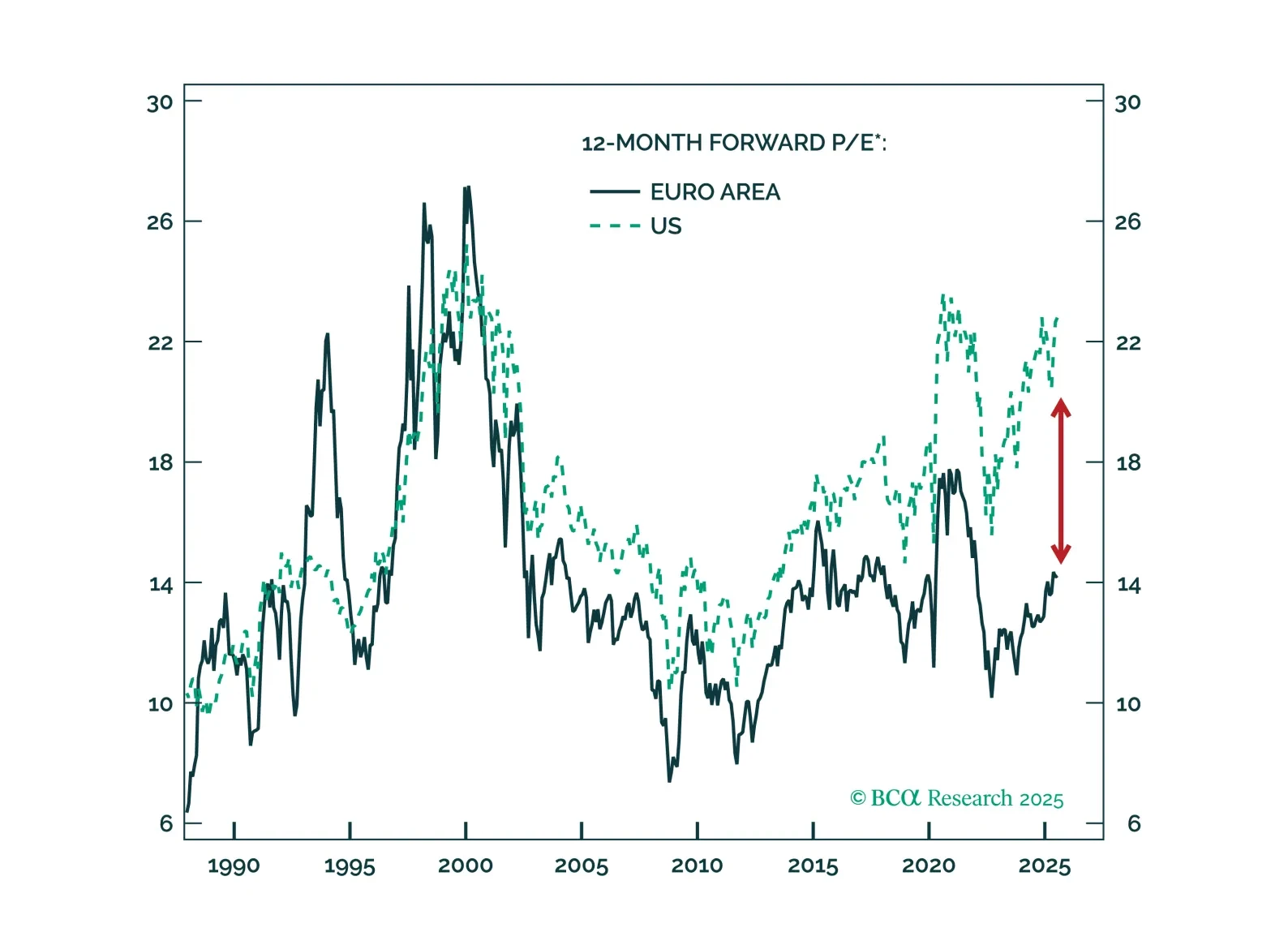

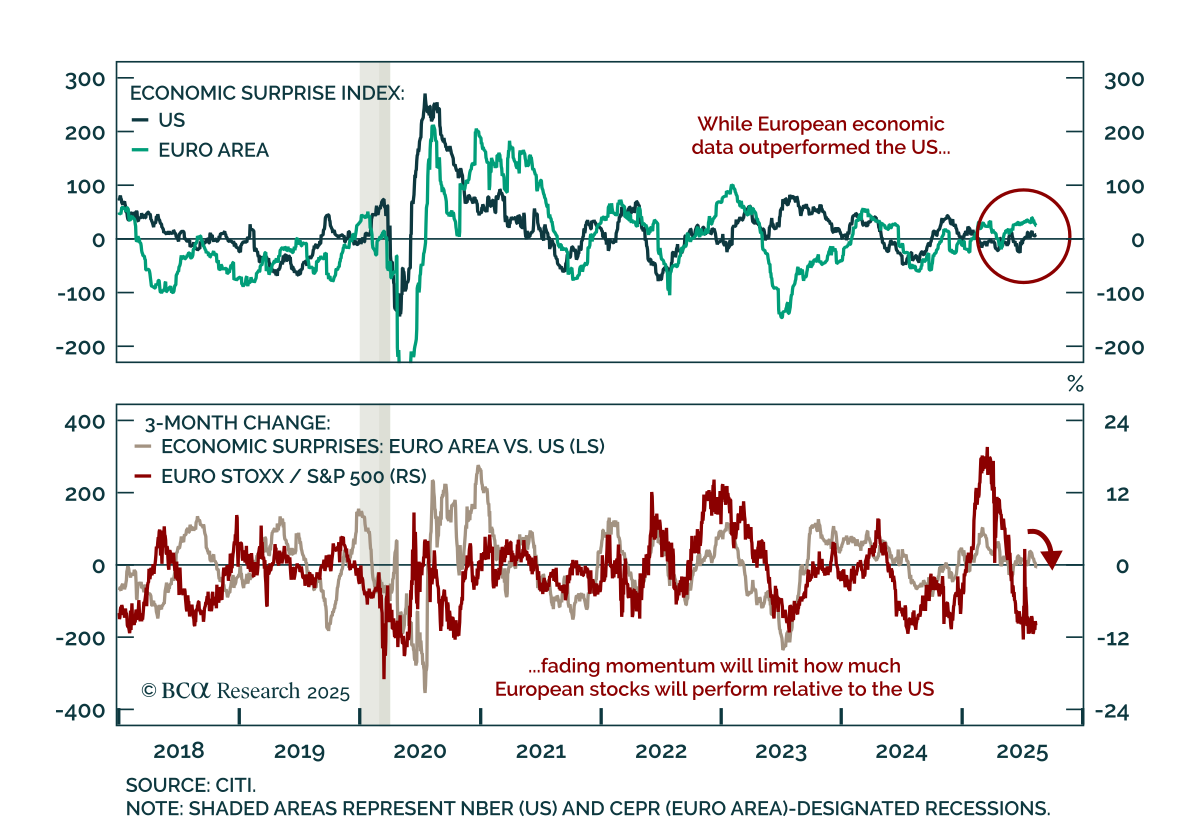

The outlook for European equities is becoming more appealing relative to US equities. Many structural headwinds are fading in Europe, and valuations remain historically cheap. Investors should position accordingly to benefit from the region’s cyclical rerating.

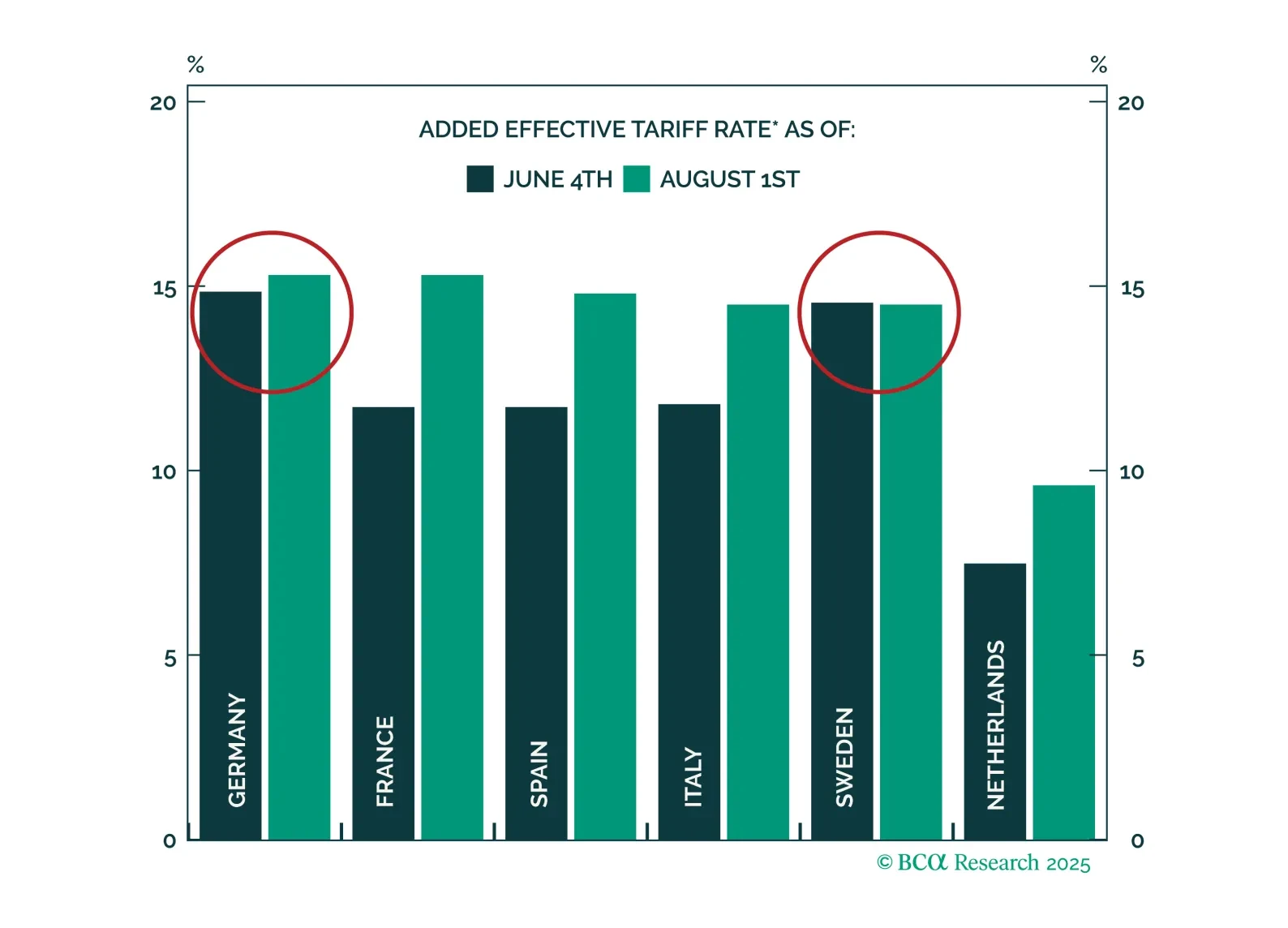

US tariffs will not derail the low-inflation economic recovery underway in the Euro Area. Investors should overweight European equities, focusing on parts of the market more insulated from tariffs.

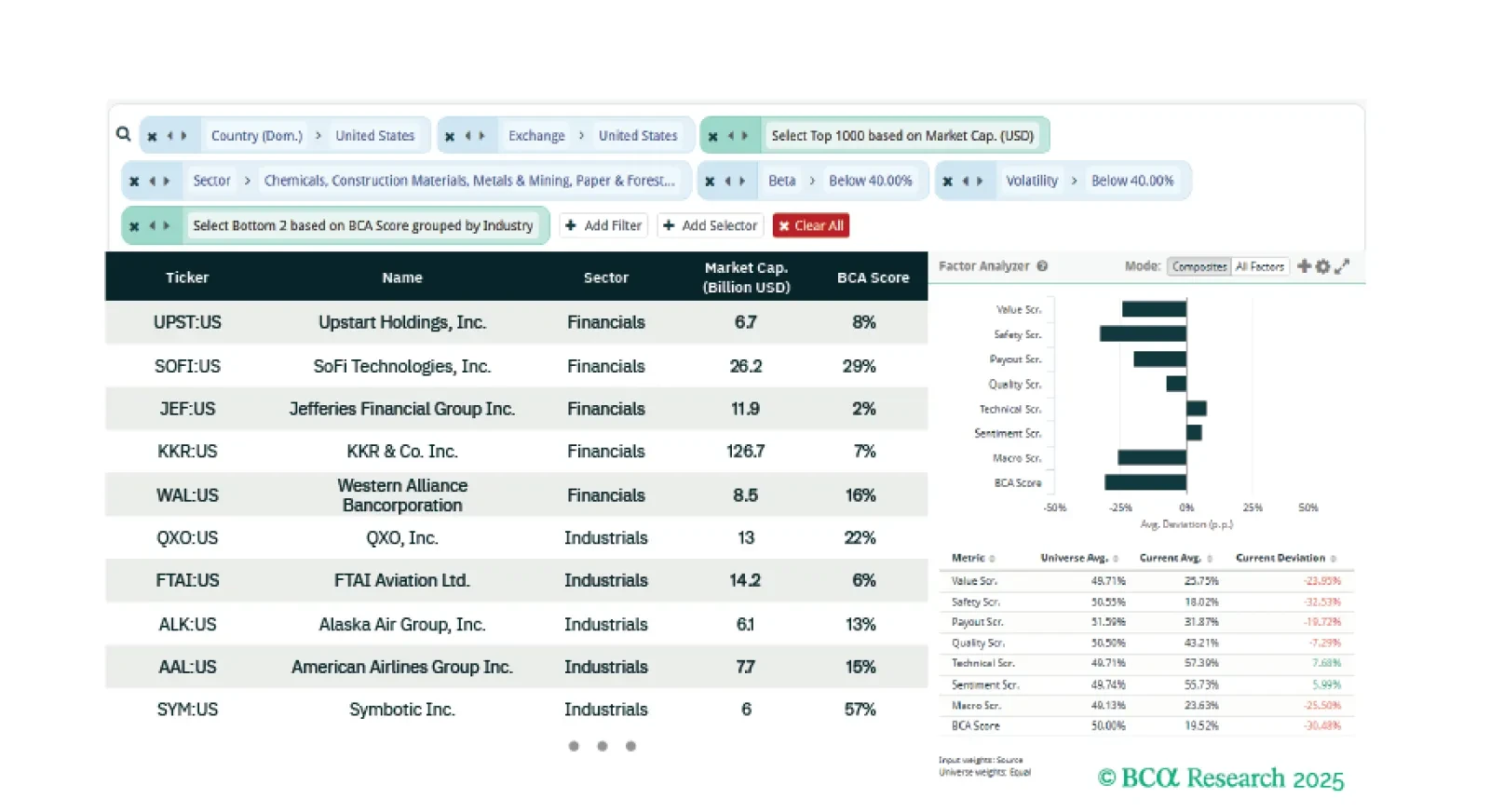

This week we develop two ideas with three screeners. The first identifies deep cyclical sectors that continue to outperform post Liberation Day in the US. We provide two screens to identify equity opportunities for this. Our final screener identifies momentum stocks that are cheap and trending and will benefit from a soft landing.