Equities

Following the release of the Bank Credit Analyst’s annual outlook, we unveil our key views for 2023. The investment strategy takeaway is that we want to lean into risk in the early part of the year but reduce exposure to it in the second half.

We explore the eight major themes that will define economic and market trends for Europe next year.

Prefer government bonds over stocks, defensive sectors over cyclicals, and large caps over small caps. Favor North America over other markets. Favor emerging markets like Southeast Asia and Latin America over Greater China, Turkey, and emerging Europe. Stick with aerospace/defense stocks.

Prefer government bonds over stocks, defensive sectors over cyclicals, and large caps over small caps. Favor North America over other markets. Favor emerging markets like Southeast Asia and Latin America over Greater China, Turkey, and emerging Europe. Stick with aerospace/defense stocks.

In this <i>Strategy Outlook</i>, we present the major investment themes and views we see playing out next year and beyond.

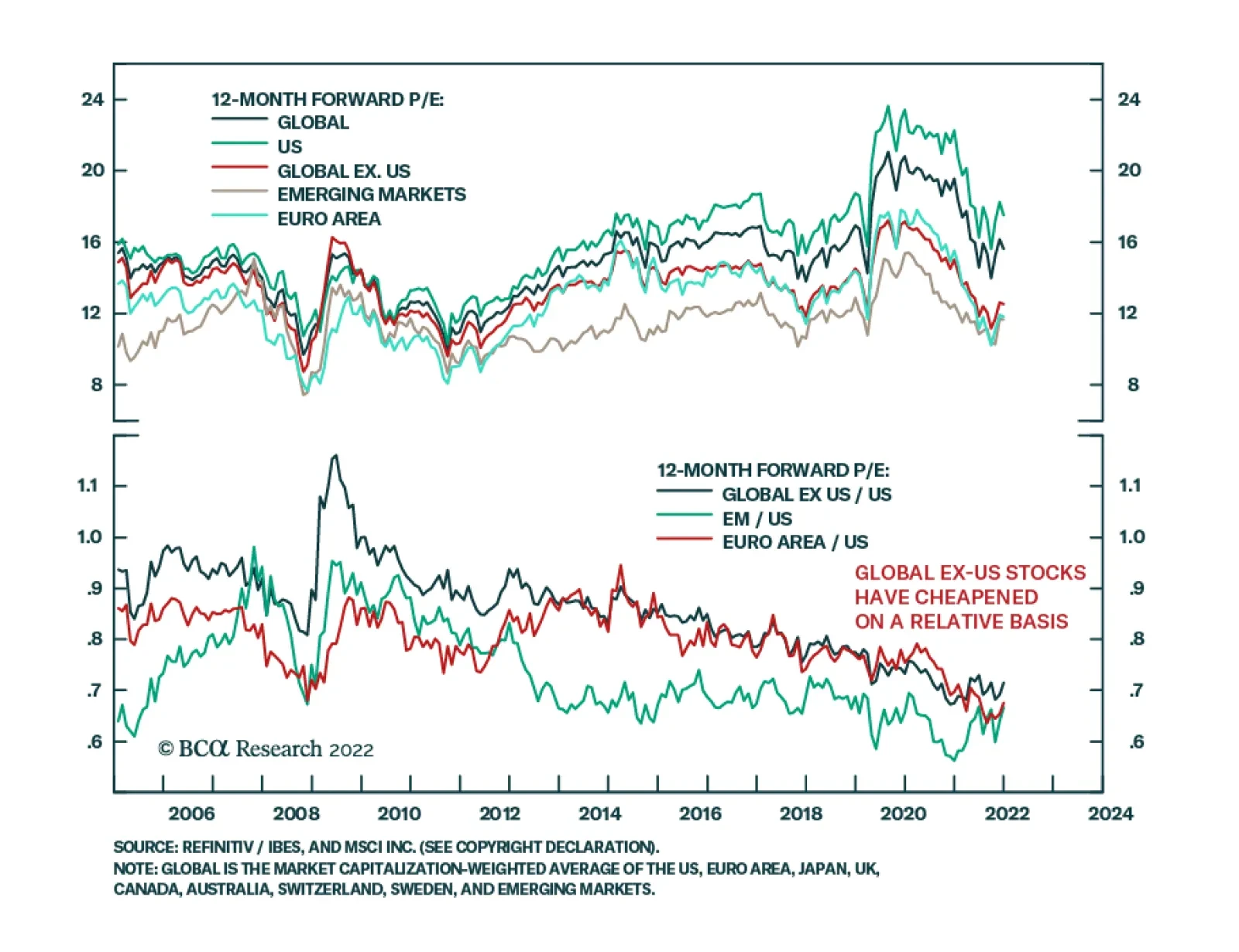

For the first time in decades, the Fed is raising rates while the US Leading Economic Indicator has fallen into contractionary territory and the global manufacturing PMI’s new orders sub-index has dropped below 50. Hence, the outlook for global stocks is currently poor. However, the underperformance of EM equities versus the US is in a late stage. We are putting EM stocks on an upgrade watch list and recommend buying EM domestic bonds opportunistically.

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

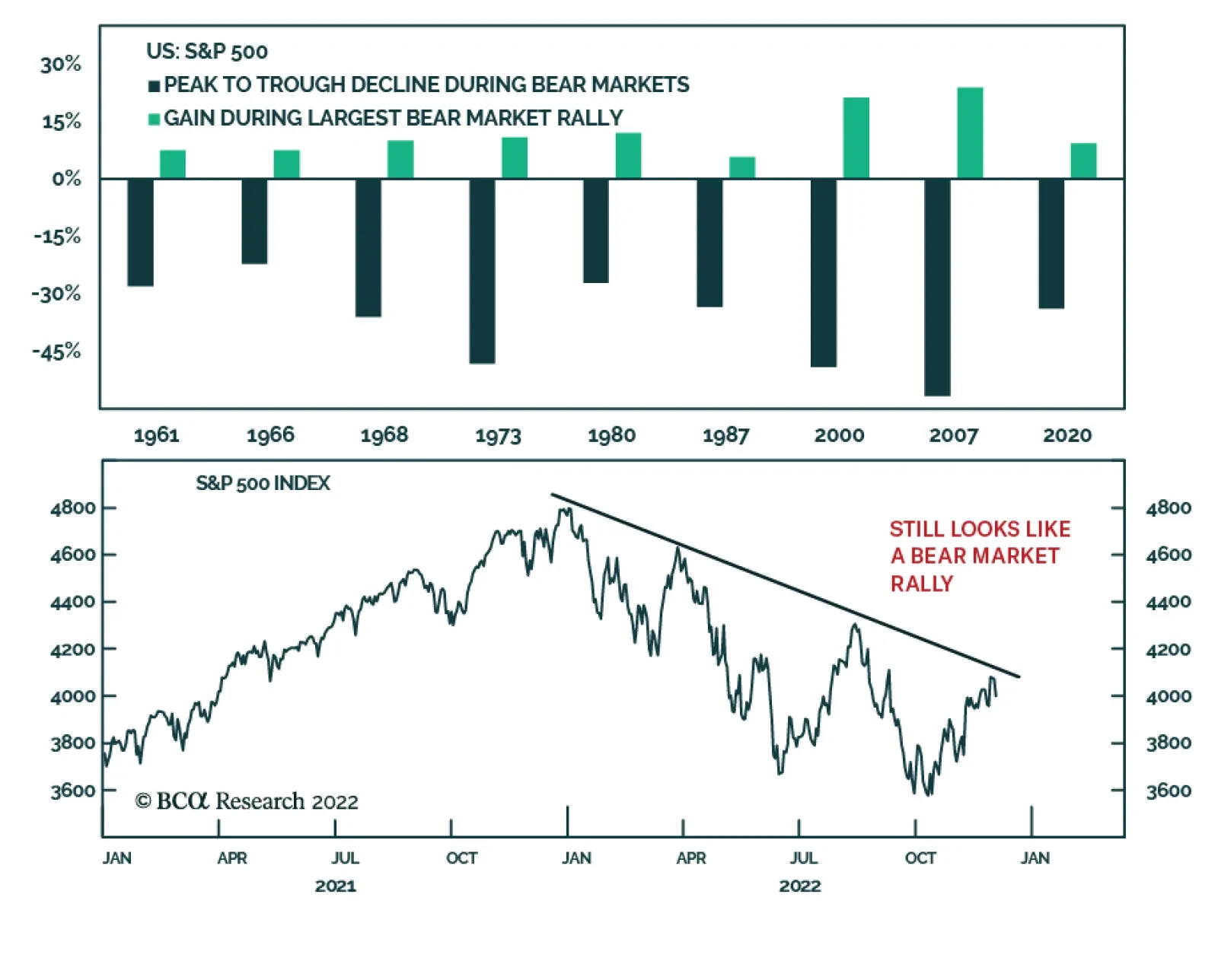

Investors should maintain a conservative and defensive strategy until recession risks are clearly reduced.