Equities

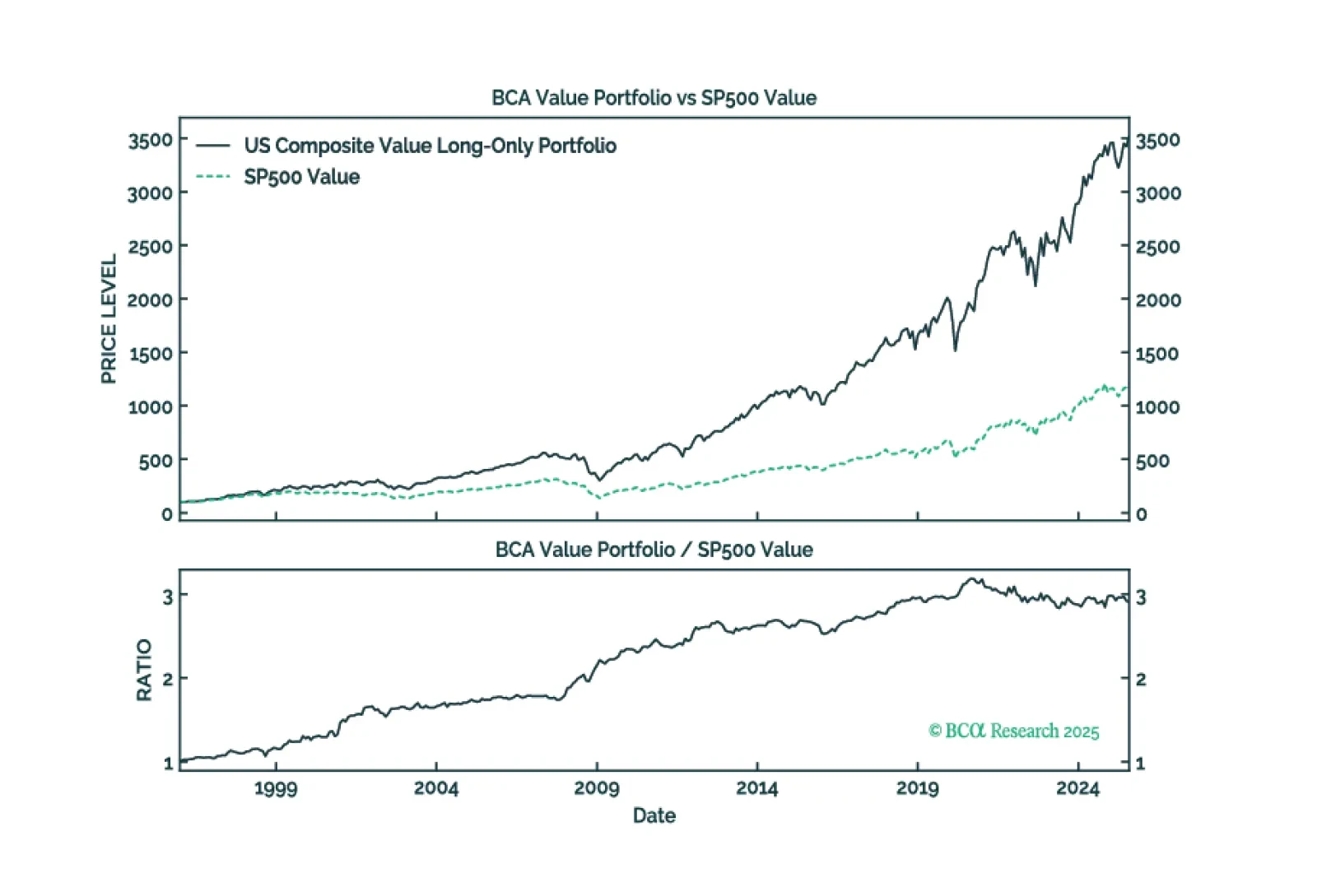

Commercial indices’ limitations have made Value a fertile ground for stock pickers. Our Composite Value model has shown promise in circumventing these flaws and capturing alpha.

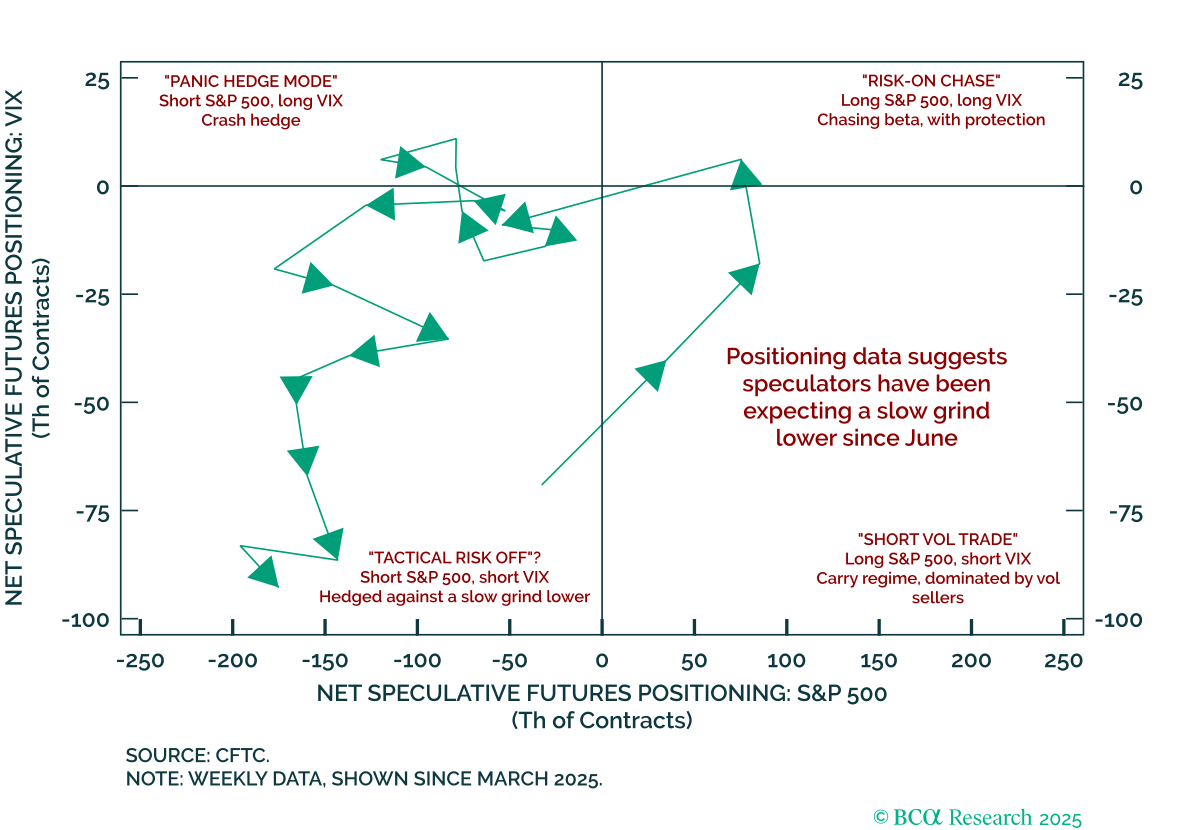

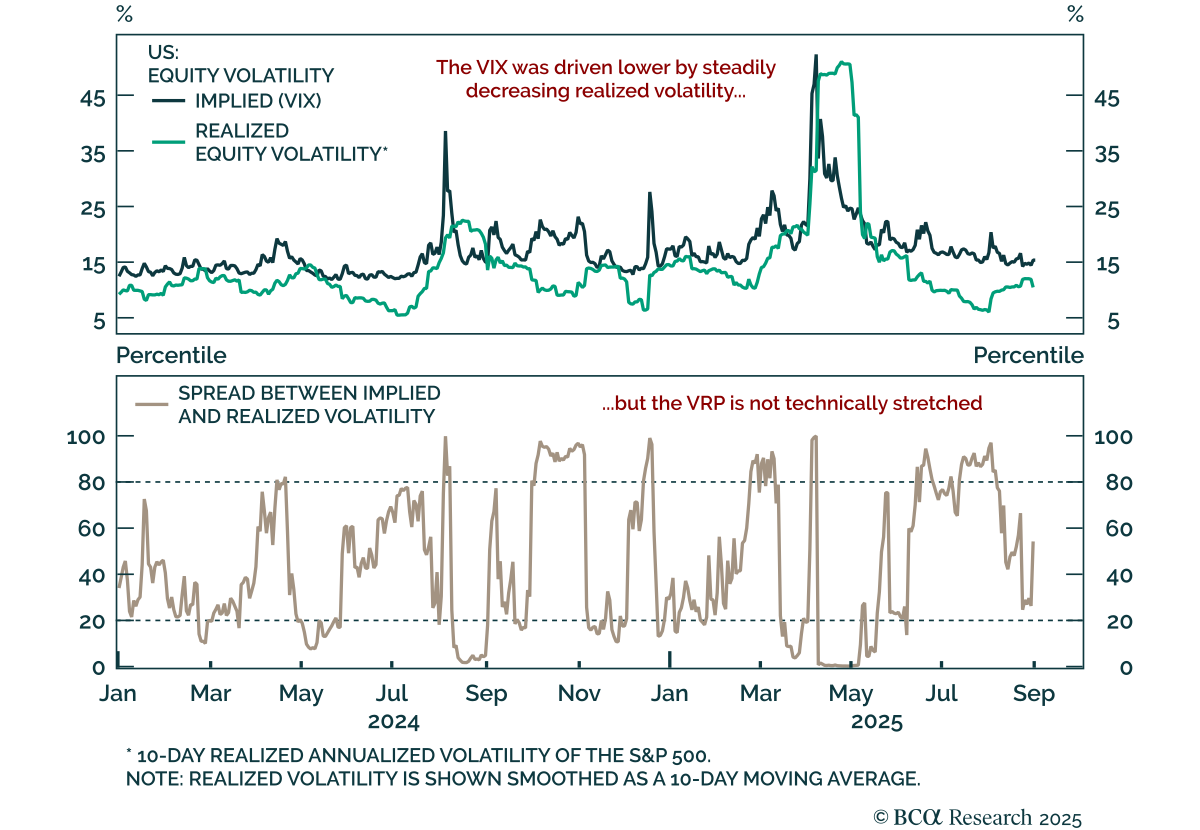

Volatility has fallen to 2025 lows even as positioning data show caution despite the S&P 500’s steady rebound. US equities have climbed back to all-time highs with minimal drawdown, steadily compressing realized volatility and pulling implied…

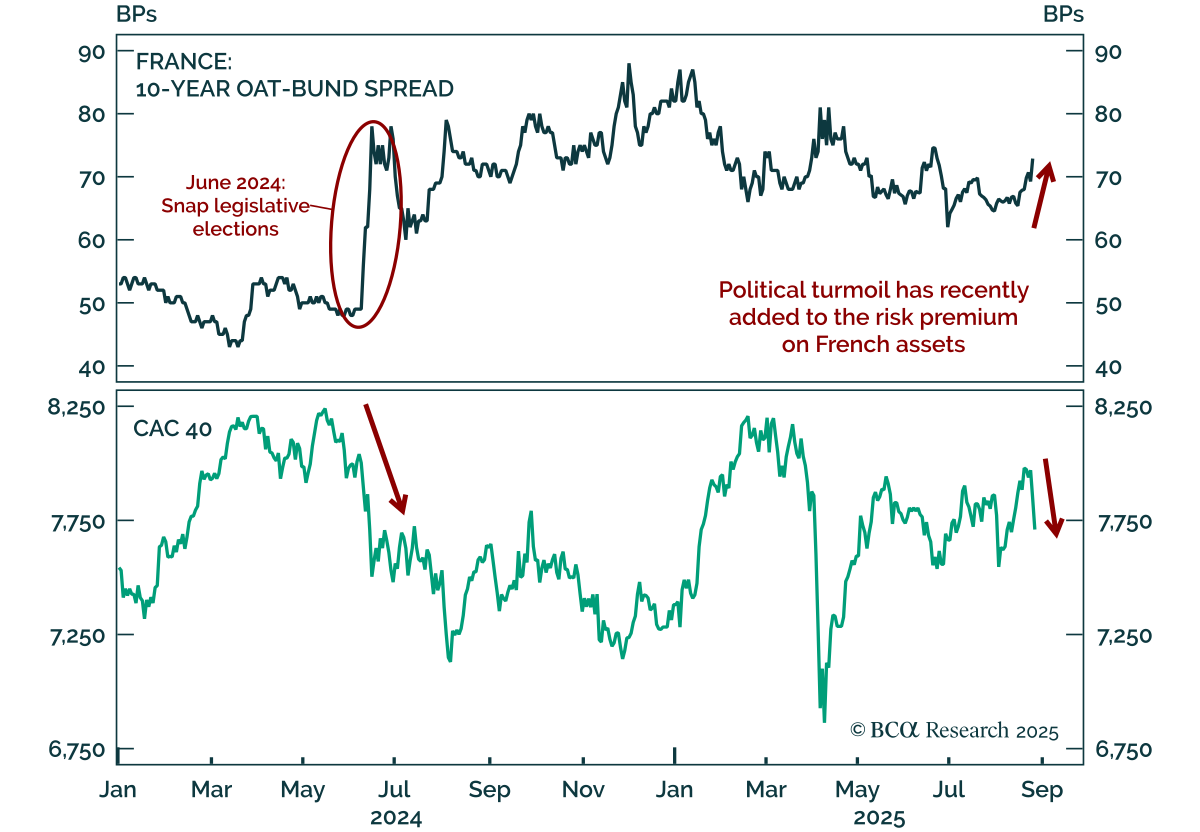

France’s renewed political turmoil highlights fiscal risks for OATs, but creates opportunities to buy French equities on dips. PM Bayrou has called a September 8 confidence vote over his deficit-cutting budget proposals, triggering a selloff in the…

The post-Liberation Day rally has broadened, reducing skepticism and strengthening the case for US outperformance versus Europe. The S&P 500’s climb to all-time highs has been unusually smooth, compressing realized volatility and pulling the VIX…

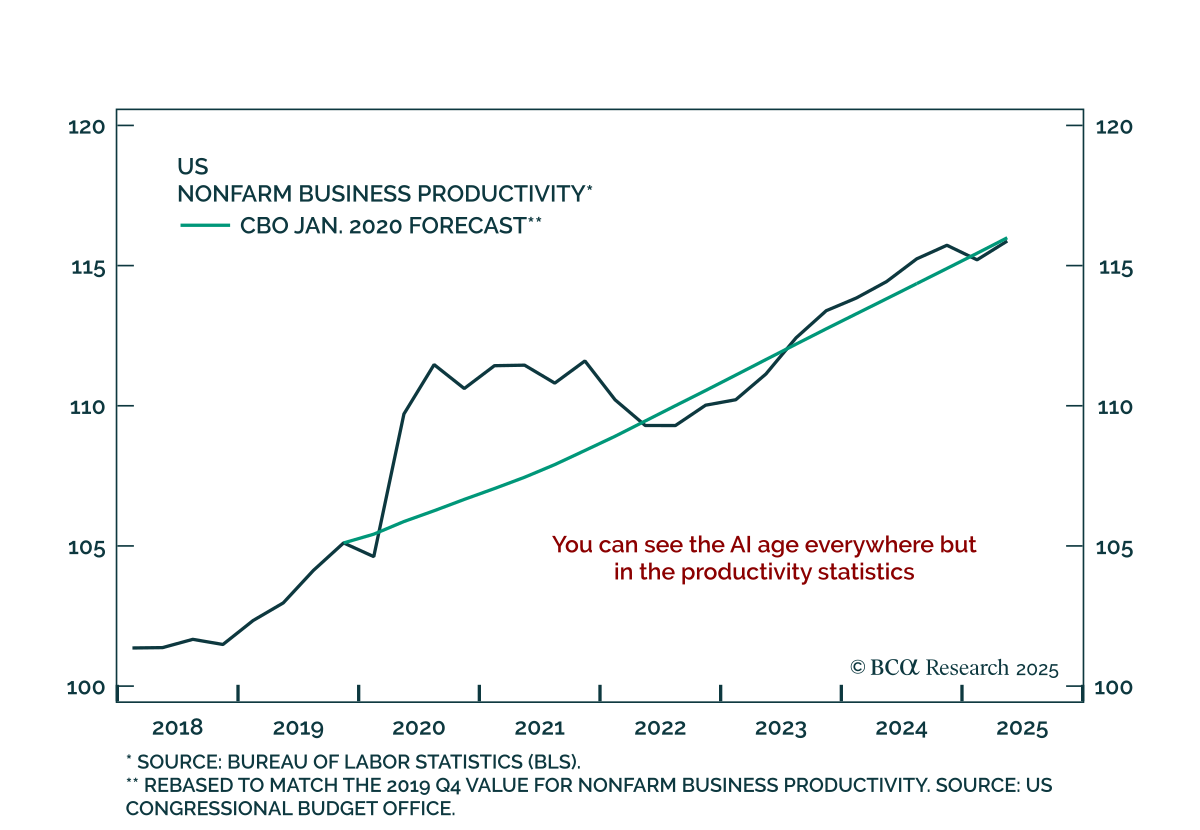

Our Global Investment strategists caution that AI’s economic impact remains limited, and investor patience may wane before fundamentals catch up to valuations. While AI has dominated equity narratives in recent years, its tangible effect on the US…

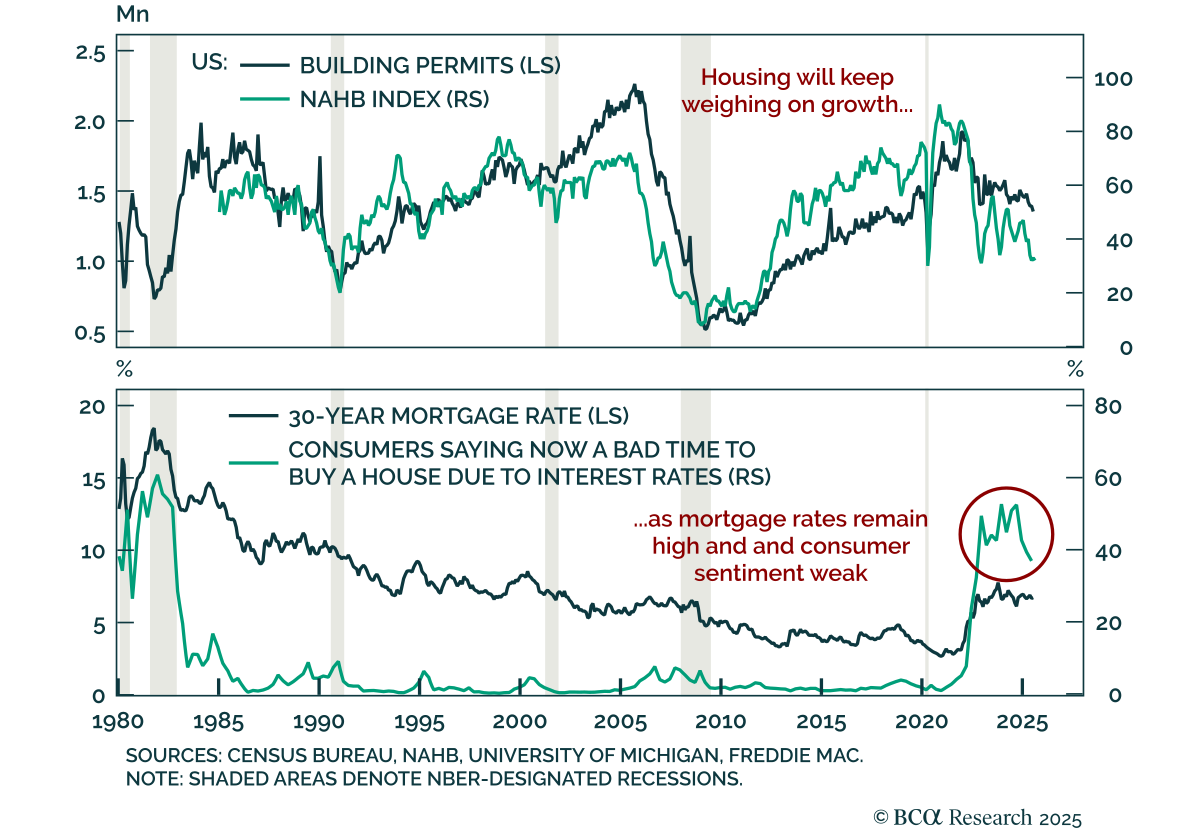

US housing data remain weak, reinforcing a fragile growth backdrop and the need for equity downside protection. July housing starts rose 5.2% m/m (annualized), but building permits fell 2.8% following a small June decline. The August NAHB Housing Market…

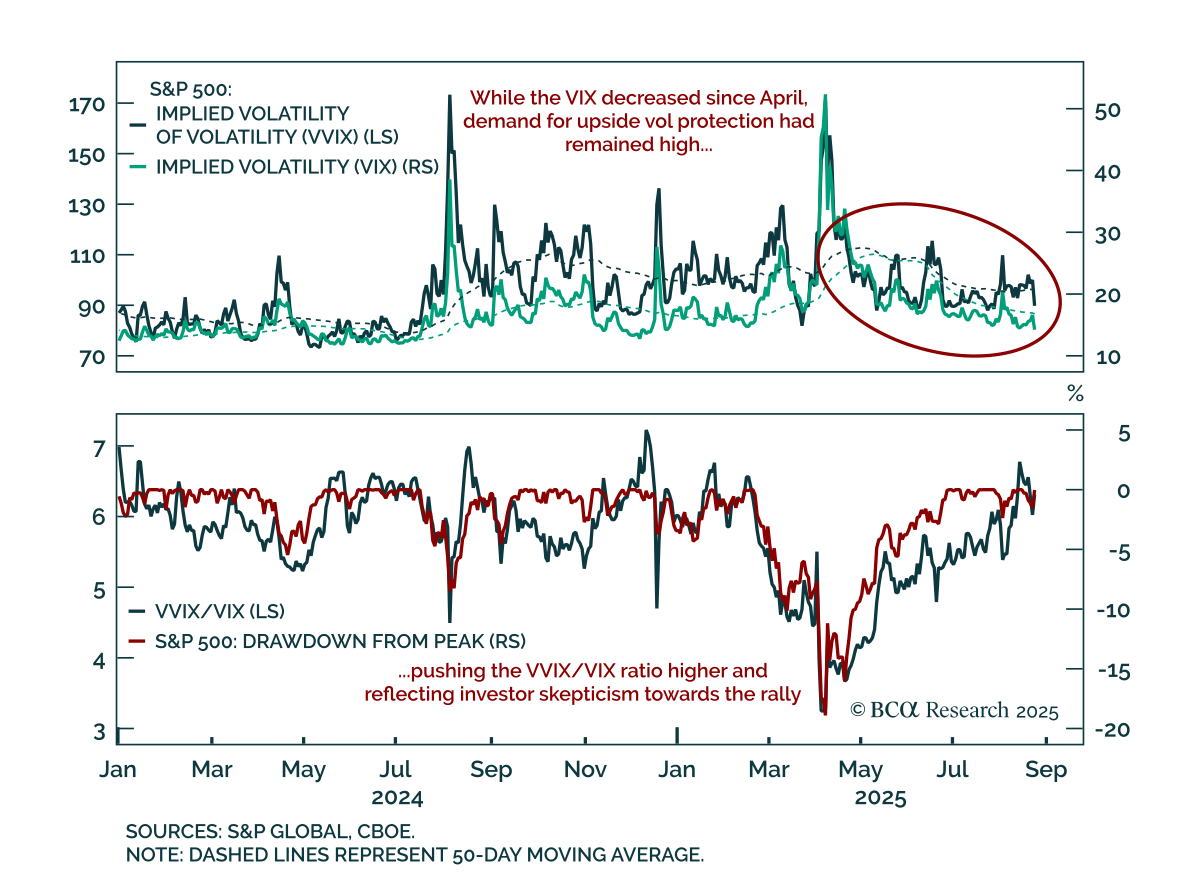

A smooth S&P 500 rally has crushed volatility, but stretched signals argue for buying protection. The index has climbed back to all-time highs with almost no drawdown, producing a steady decline in realized volatility. This has pushed implied…

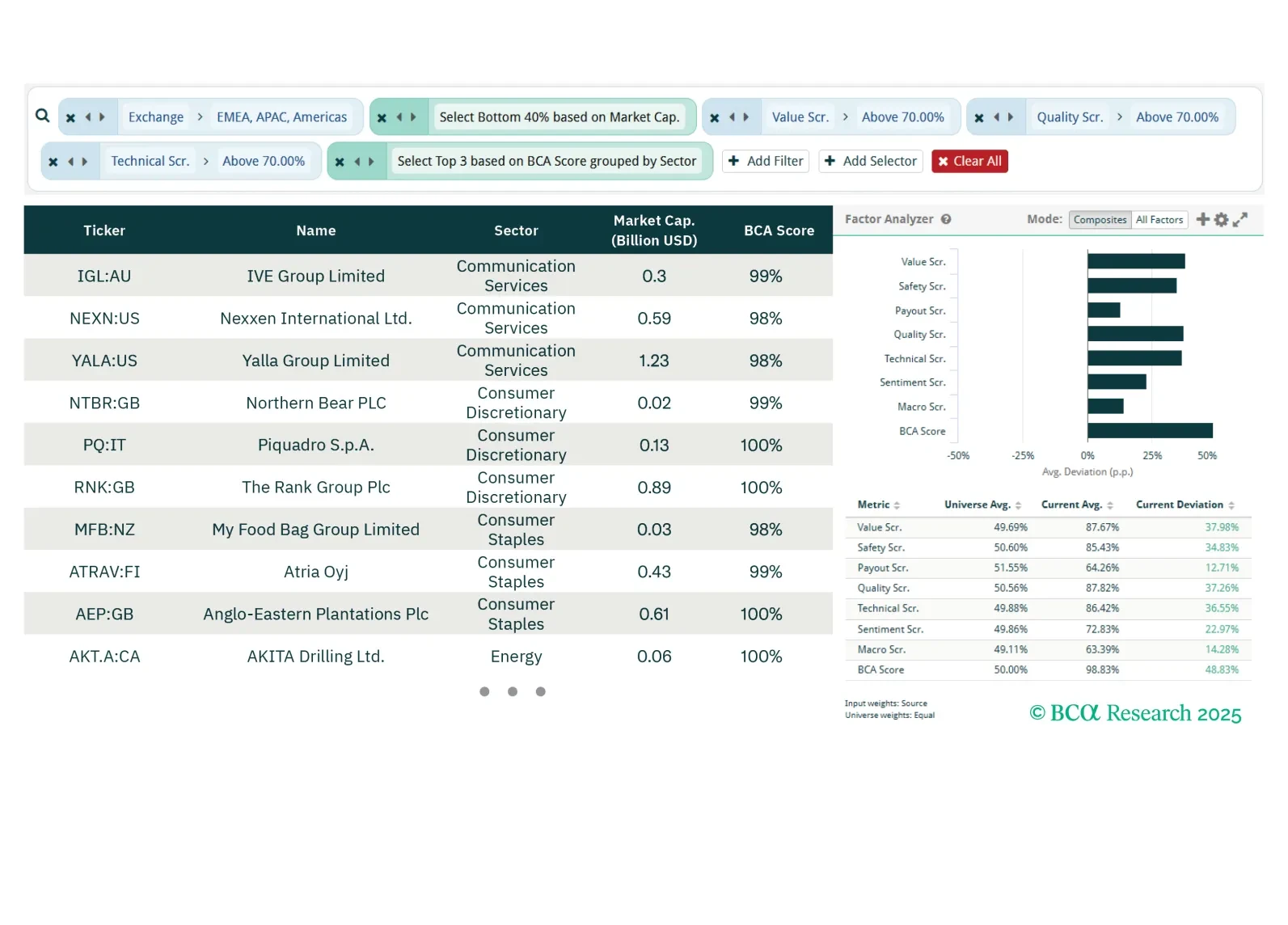

This week our three screeners highlight plays in global small-cap value stocks, gold miners, and stocks exposed to an exciting structural investment theme: Space.

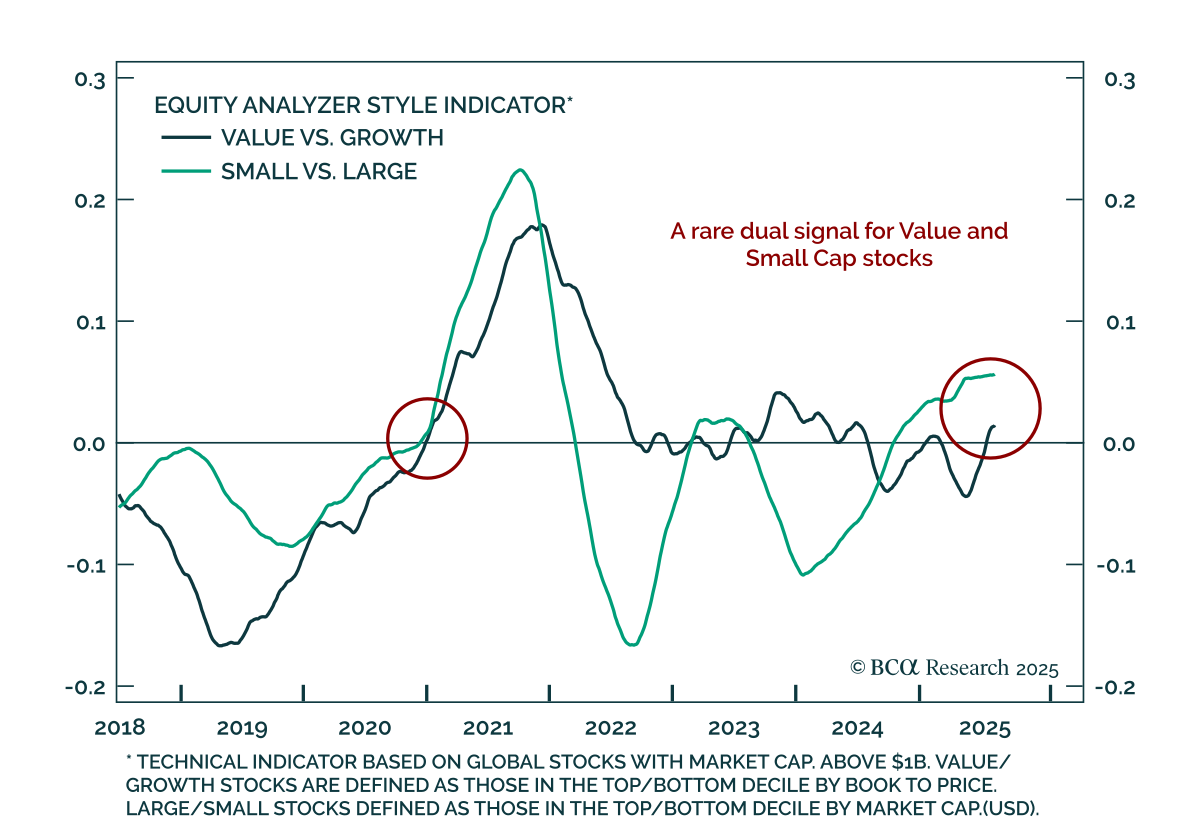

Momentum is building behind small-cap and value stocks, signaling a rare dual tailwind for cyclical styles. Our Chart Of The Week comes from Guy Russell, strategist for Equity Analyzer.While market attention remains focused on the Mag 7 and Tech, Equity…

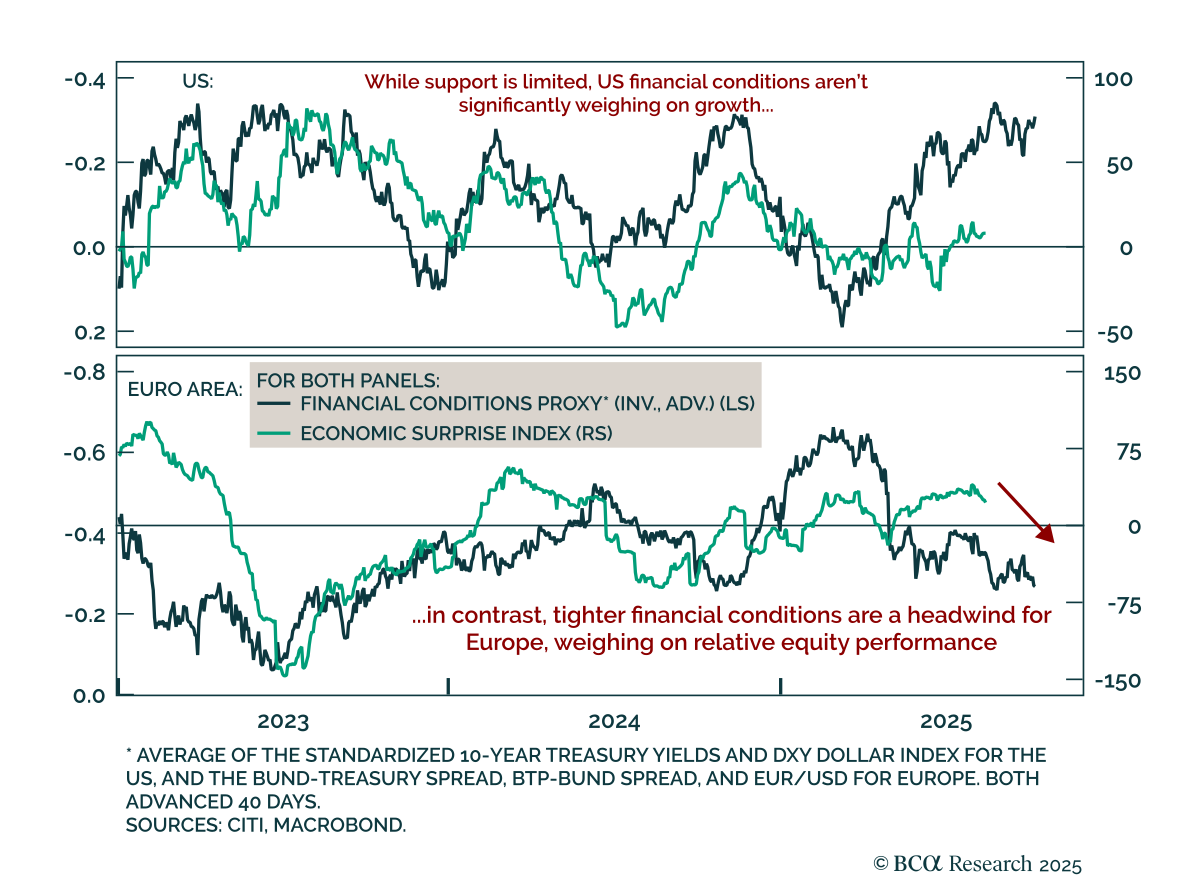

Dollar softness has had little growth impact, and European equities should keep lagging. A key 2025 trend has been USD depreciation, but the associated easing in financial conditions has offered minimal support to US growth, reflecting higher term premia…