Equities

European assets have enjoyed a stunning outperformance since October 2022. Can these strong returns last in 2023?

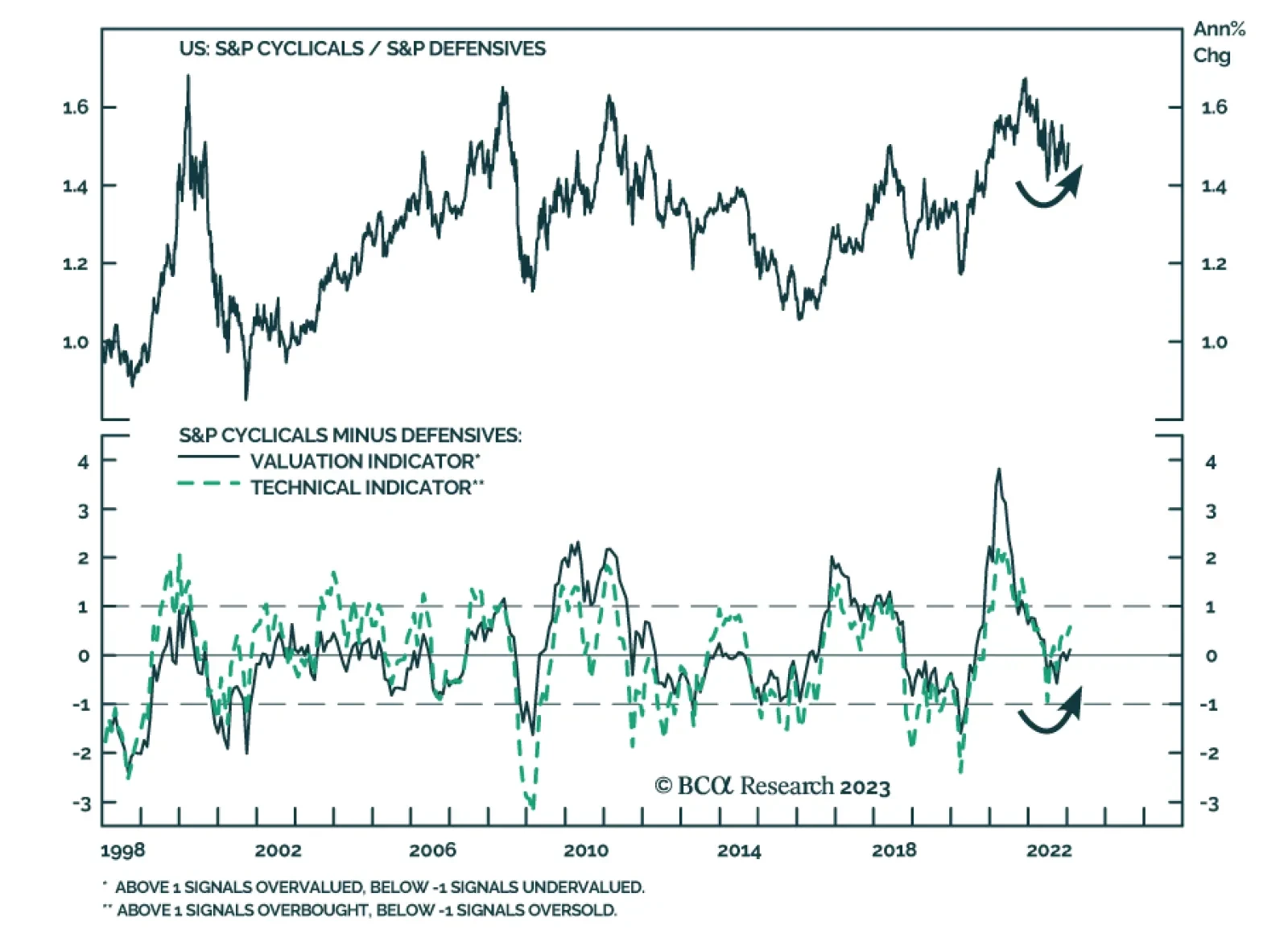

Hopes of a soft landing for the US economy will intensify over the coming months, allowing equities to rally. However, even if an equilibrium of high employment and low inflation is reached, it will be difficult to keep the economy there. Investors should remain tactically bullish on stocks but look to turn defensive in the second half of 2023.

In EM ex-China, growth will continue decelerating. Some economies will experience an outright recession, while most will have a growth recession. Nearly every single economy will experience a cyclical drop in inflation (with the exception of Turkey).

China's reopening is much more positive for the Chinese economy than it is for the rest of the world, as it will boost its domestic service sector activity and consumer spending much more than the industrial economy. A slowdown in Chinese industrial activity will put downward pressure on its demand for raw materials and energy, helping the world avoid another spike in inflation. Upgrade Macau casinos to overweight as the key beneficiaries of reopening. Off-shore TMT and bank shares face structural headwinds.

In response to lower energy prices and China’s reopening, European assets prices are outperforming. Will the ECB spoil the party?