Equities

The equity market is back to the 2019 level on an inflation-adjusted basis. However, it is still not cheap as it is not pricing in the possibility of a prolonged and deep earnings recession or a higher interest rates regime. Many areas of the market that appear cheap, are cheap for a reason. The only industries that are cheap because they are growing into their valuations are Energy and Airlines. We are upgrading Airlines to equal weight.

The Chilean economy is entering a recession. Inflation will drop rapidly and the central bank will cut rates meaningfully in H2 2023. We continue to recommend a structural overweight across Chilean risk assets on the basis of falling inflation and local yields, record cheap valuations, and dissipated political volatility.

A run of hot January data shook up financial markets, but we think they overreacted. We remain constructive on equities and the economy in the near term.

Rather than teetering into recession, global growth has firmed since the start of the year. While we still expect inflation to decline, the risk that central banks will need to lift rates more than discounted has increased. Long-term focused investors should start raising cash allocations by trimming their equity holdings.

US domestic politics, hypo-globalization, and Great Power Competition favor a revival of US manufacturing capacity. The industrial sector will benefit from the attempt to rebuild US manufacturing. Go long physical infrastructure and defense stocks. Find opportunities to take a long position on the universe versus the metaverse.

China’s housing market adjustment will be protracted, causing several years of sub-par growth in the world’s second largest economy. We go through the major investment implications.

The rebound in growth is pushing up inflation. More aggressive monetary policy is likely to trigger recession over the next 12 months or so. Investors should stay defensive.

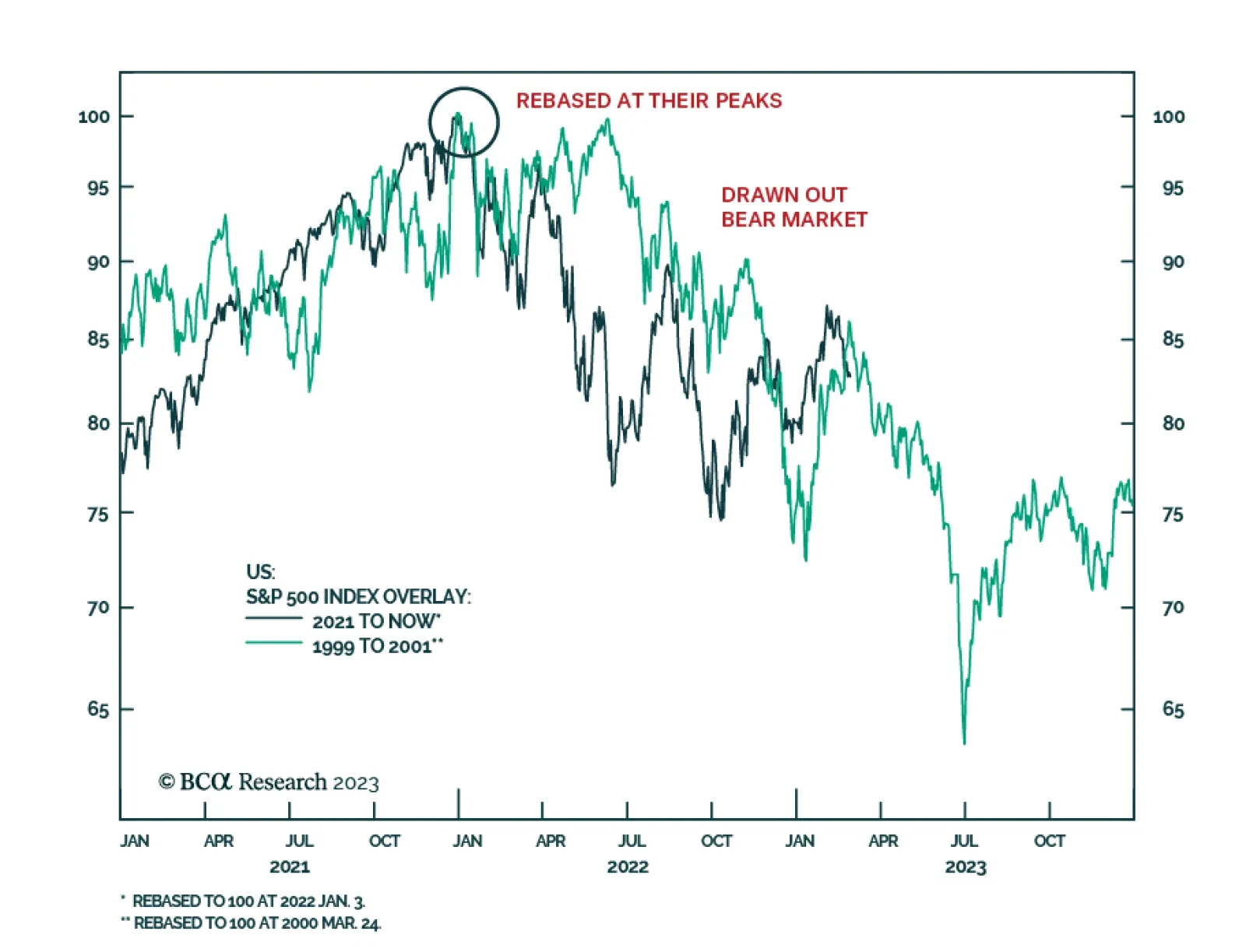

Bulls and bears are perplexed because they suffer from recency bias. The investment roadmap and framework of the past 15 to 20 years should not be used to analyze current US financial markets. US corporate earnings will likely plunge substantially even in the case of a mild recession.

It is easy to conclude that European equities are attractively valued by looking at multiples; however, a method rooted in fundamentals is essential to find out which bourses are genuinely cheap.