Equities

The odds of achieving a goldilocks scenario in the US where inflation drops amidst robust growth are low. If US bank woes do not escalate, the Fed will continue hiking amid a contraction in US corporate profits and global trade. The recovery in China’s industrial economy will disappoint. Commodity prices are breaking down.

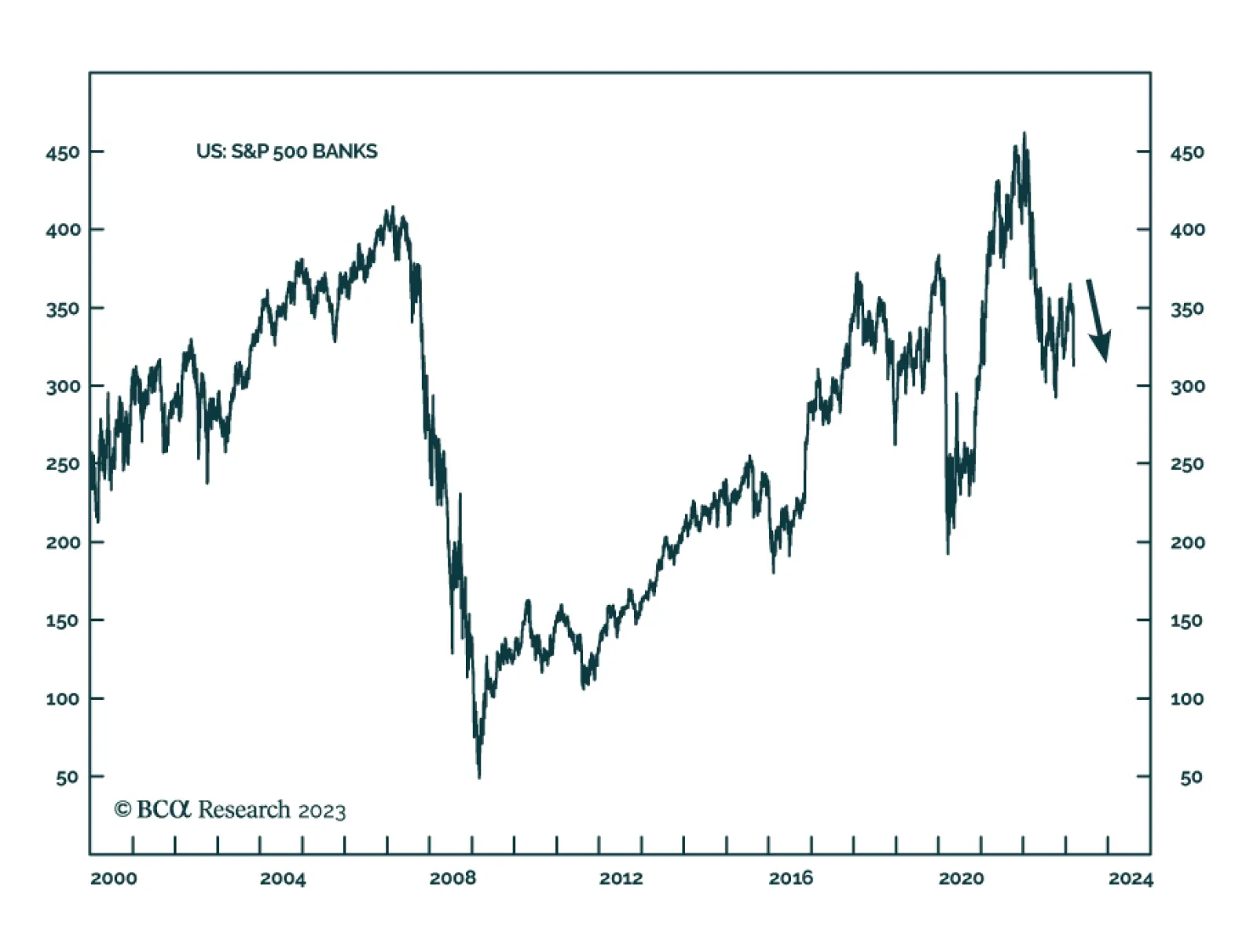

Bank failures are another ‘canary in the coal mine’ warning that a US recession is imminent, yet stocks, bonds, and the oil price are still a long way from fully pricing it.

The growth and inflation profiles of the three central European countries are set to diverge. The outlook for Polish and Hungarian Bonds are not attractive anymore. Book profits on them. Instead, initiate a new trade: pay Polish / receive Czech 10-year swap rates.

Generative AI is a major technological breakthrough that holds tremendous economic and investment promise and will have sweeping effects on wide swaths of the economy. We are bullish on generative AI as a long-term investment theme. However, at the moment we observe hallmarks of an investment frenzy. We believe that there will be a more attractive entry point for patient investors.

The UK economy is more resilient than was feared last year. While this will not help UK stocks, the Footsie’s long term prospects are appealing.

Investors in Europe and the American West are already starting to think about the implications of the 2024 election, given that sticky inflation and tighter monetary policy keep the risk of recession elevated.

The first legislative meeting of Xi Jinping’s third term suggests that Chinese policy is continuous and consistent with the previous ten years, which is negative for long-term productivity.

This week’s <i>Special Report</i>, written by Miroslav Aradski, highlights the worrisome deterioration in health trends in the US, which began before the pandemic. Over the long haul, this could weigh on labor supply and productivity, put upward pressure on bond yields, and hurt equity multiples.

There has been a paradigm shift in Beijing’s approach to policy stimulus. The main purpose of government policy is now managing downside risks to the economy in both the short and long term. The priority for the central government is to build an economic and financial system resilient against potential negative shocks, including external threats.