Equities

It is too early to know whether the drop in bond yields will offset the drag on growth from tighter lending standards. But if it does, the net effect on equity valuations could be positive. This is enough to justify a modest tactical overweight to equities, with the proviso that investors should look to reduce equity exposure later this year in advance of a mild recession in 2024.

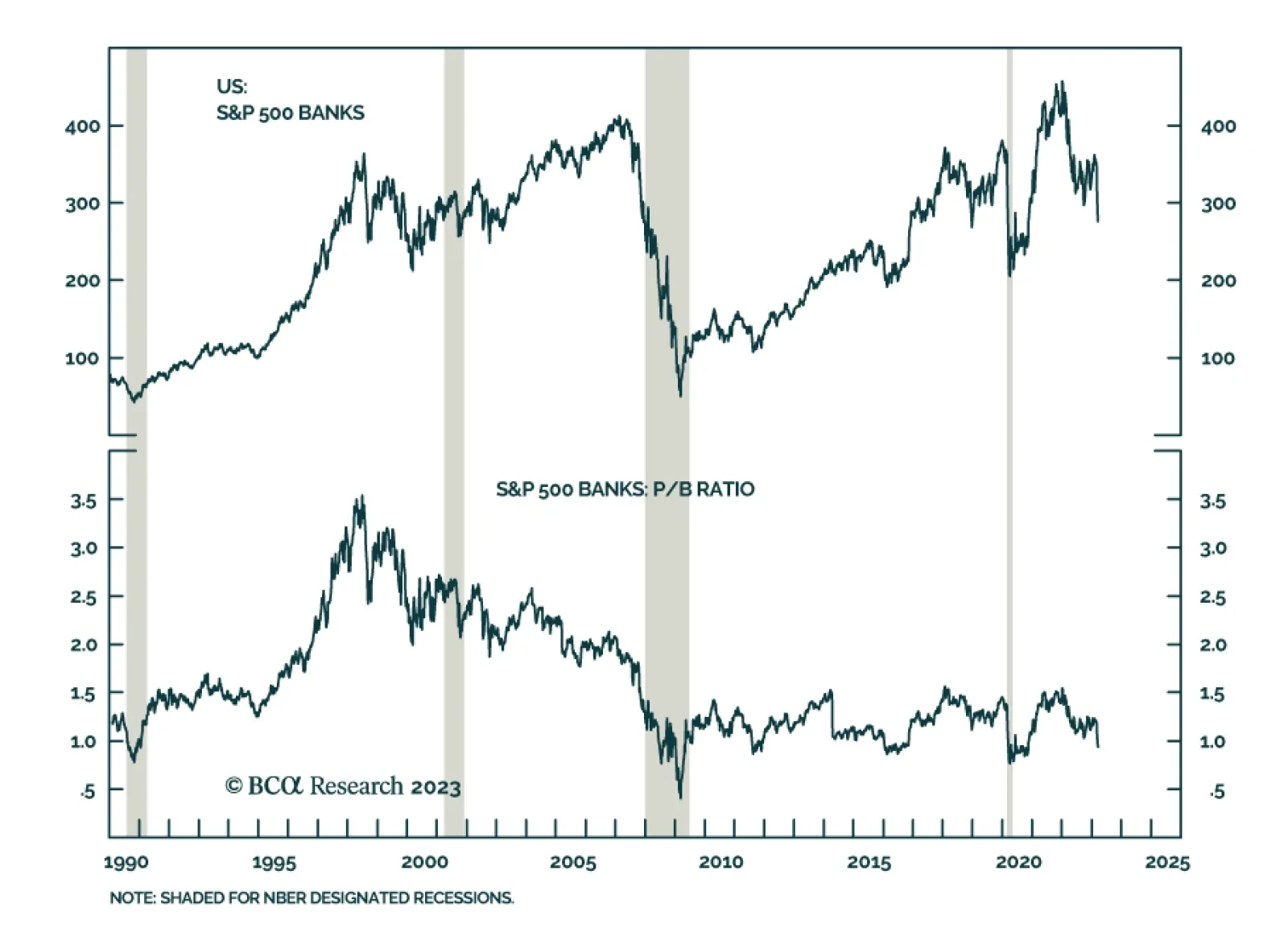

US financial instability reinforces our bearish investment outlook by weighing on economic growth and corporate earnings while also increasing US policy uncertainty and geopolitical risk.

Have global equity markets reached a riot point? Is the Fed going on hold a sufficient condition for stocks to stage a cyclical rally? If not, what would be needed to produce such a rally? Does the Fed’s recent balance sheet expansion foreshadow a rise in the US money supply? This report provides answers to all these questions.

The banking crisis has hit European shores and engulfed CS; is this all bad news for Europe or have the odds of a policy mistake declined?

The turmoil in US regional banks will weigh on economic growth. Arguably, it would be better for the broader stock market if growth slowed because banks became more conservative in their lending than if it slowed because the Fed had to raise rates to over 6%. In both cases, economic growth would decelerate but at least in the former scenario, the discount rate applied to earnings would not be as high.